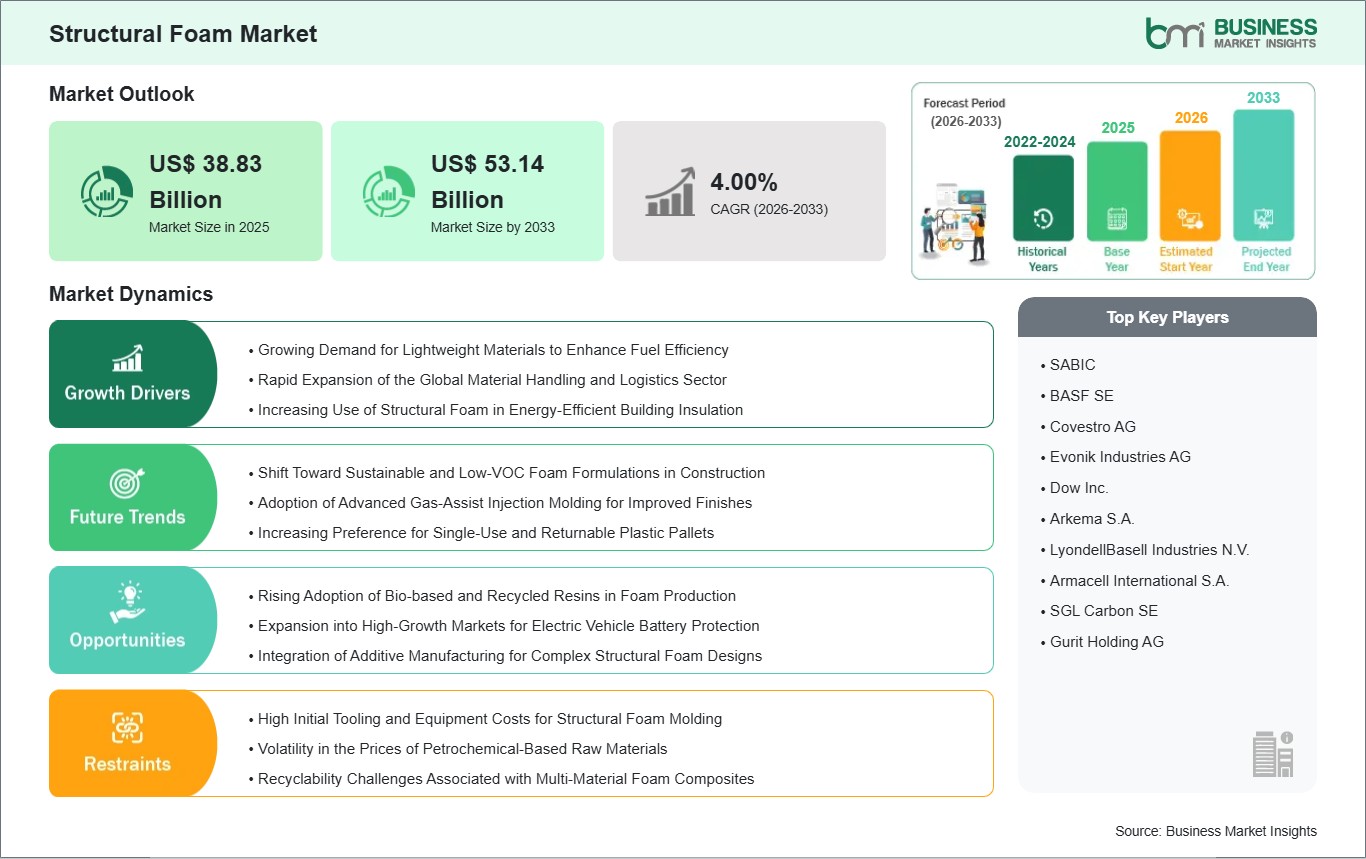

The Structural Foam Market size is expected to reach US$ 53.14 billion by 2033 from US$ 38.83 billion in 2025. The market is estimated to record a CAGR of 4.00% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The Global Structural Foam Market is an important segment of the Advanced Materials industry, offering critical lightweighting and structural solutions for a broad array of high-growth markets. The market, which has a unique sandwich structure, has witnessed a strong demand trend as various sectors, including the automotive industry, aim at striking a balance between high mechanical properties and substantial weight reduction. Currently, polypropylene holds a strong position as a dominant material type, driven by its flexibility and cost-effectiveness, whereas the automotive industry remains the largest application area, driven by the global trend towards electric mobility. The industry is currently witnessing a strategic shift towards sustainability, with increased investments going into recycled resins and energy-efficient molding technologies, driven by changing global environmental norms. The industry, from a strategic standpoint, is witnessing a strong trend towards technological integration, including simulation software for designing optimized foam cell structures as well as automated molding cells.

From a competitive standpoint, North America currently holds a dominant position, driven by a strong automotive and construction industry base, whereas the Asia-Pacific region remains a growing hub, driven by its manufacturing industry base. Despite challenges such as raw material price fluctuations, the market remains robust, anchored by the fundamental need for durable, lightweight, and long-lasting industrial products. Looking forward, the emergence of bio-based materials and the expansion of the e-commerce logistics chain are expected to be the primary drivers of market growth through 2030. Despite challenges such as raw material price fluctuations, the market remains robust, anchored by the fundamental need for durable, lightweight, and long-lasting industrial products. Looking forward, the emergence of bio-based materials and the expansion of the e-commerce logistics chain are expected to be the primary drivers of market growth in future.

Structural Foam Market - Strategic Insights:

Get more information on this report

Structural Foam Market Segmentation Analysis:

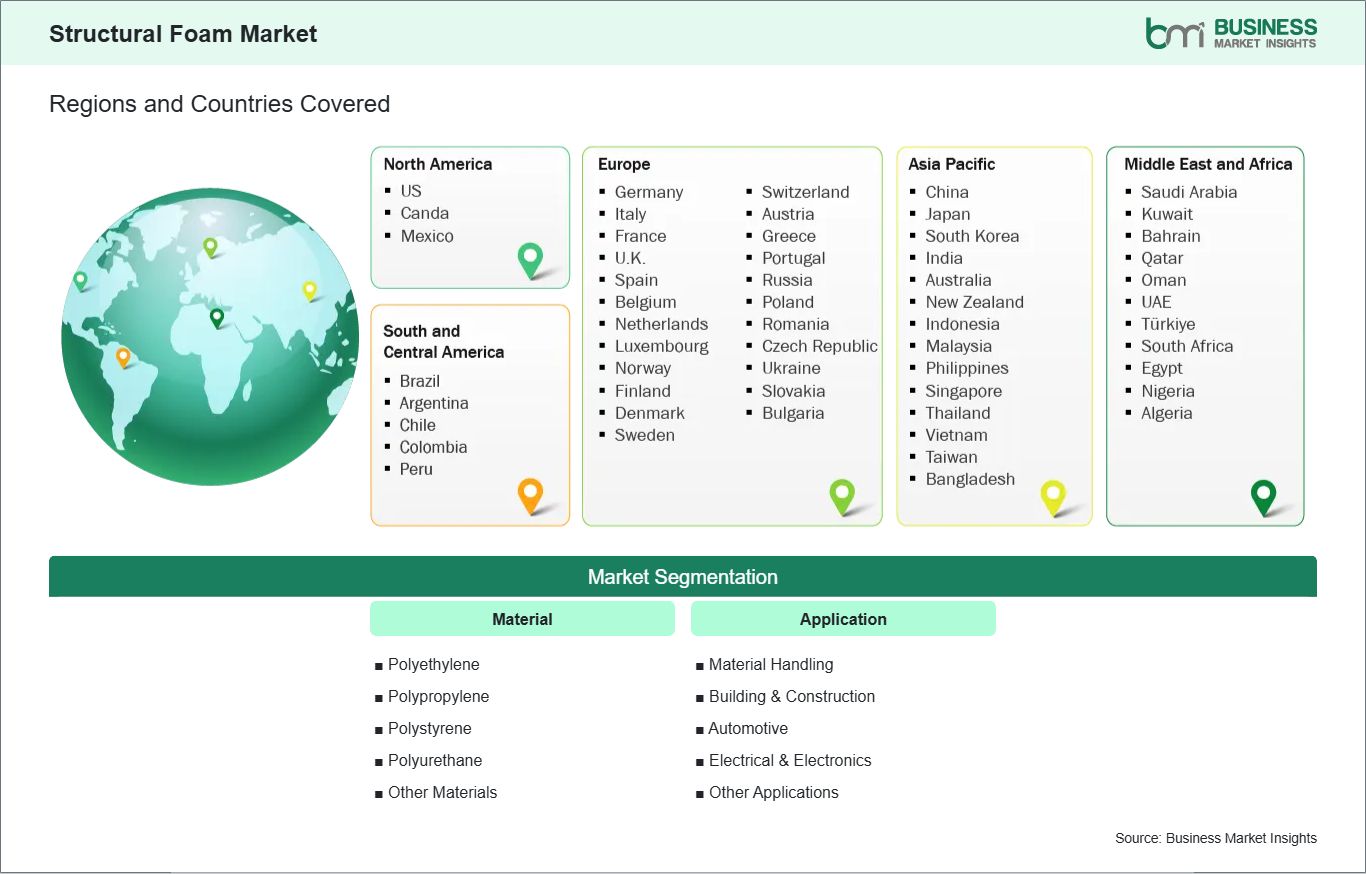

Key segments that contributed to the derivation of the Structural Foam market analysis are material and application.

By material, the market is segmented into Polyethylene, Polypropylene, Polystyrene, Polyurethane, and Others. The Polypropylene segment dominated the market in 2025.

By application, the market is segmented into Material Handling, Building & Construction, Automotive, Electrical & Electronics, and Others. The Automotive segment dominated the market in 2025.

Structural Foam Market Drivers and Opportunities:

Growing Demand for Lightweight Materials

The global manufacturing landscape is currently centered on the "lightweighting" revolution, particularly within the transportation and aerospace sectors. Structural foam has emerged as a key technology in this movement because it allows for the production of large, rigid parts that are significantly lighter than their solid plastic or metal counterparts. By utilizing a cellular core surrounded by a solid skin, structural foam provides the necessary stiffness for structural applications without the weight penalty of solid materials. This is critical for the automotive industry, where reducing vehicle mass is the most direct way to improve fuel economy and extend the range of electric vehicles.

Beyond weight reduction, structural foam offers the unique advantage of part consolidation. Engineers can design complex, multi-functional components that replace several smaller metal parts, thereby reducing assembly time and the number of potential failure points. This consolidation not only simplifies the supply chain but also enhances the overall durability of the structure. As regulatory bodies worldwide implement stricter CO2 emission targets, the reliance on structural foam to achieve these benchmarks has made it an indispensable material in the transition toward more efficient and sustainable transportation systems.

The demand is further amplified by the versatility of structural foam in handling varied mechanical stresses. Its high strength-to-weight ratio makes it ideal for exterior panels, under-the-hood components, and interior structural frames. Manufacturers are increasingly moving away from traditional materials toward these high-performance foams because they offer better dent resistance and vibration damping. As the cost of advanced composites remains high, structural foam provides a commercially viable middle ground that balances extreme weight savings with the scalability required for mass production.

Rising Adoption of Bio-based and Recycled Resins

Environmental sustainability has moved from a corporate social responsibility goal to a core business strategy, creating a massive opportunity for the development of bio-based and recycled structural foam resins. Traditionally, structural foams have relied heavily on virgin, petroleum-derived polymers like polypropylene and polystyrene. However, the introduction of high-performance bio-resins and the improvement of chemical recycling processes now allow manufacturers to produce structural foam parts with a significantly lower carbon footprint. This shift is particularly attractive to the building and construction and consumer electronics sectors, where "green" building certifications and eco-labeling drive consumer choice.

The adoption of recycled content in structural foam does not necessarily compromise the material's integrity. Because the structural foam process creates a sandwich-like structure, manufacturers can often utilize recycled materials in the foamed core while maintaining a high-quality virgin or reinforced skin for aesthetic and protective purposes. This "closed-loop" potential is a major selling point for material handling companies that use millions of plastic pallets and crates annually. By transitioning to recycled structural foam, these companies can drastically reduce their environmental impact and comply with emerging extended producer responsibility laws.

Moreover, advancements in polymer science are enabling the creation of bio-polymers that mimic the mechanical properties of traditional resins. These materials, derived from renewable sources like corn or sugarcane, offer a hedge against the price volatility of crude oil. As the technology matures and production scales, bio-based structural foams are expected to become price-competitive with traditional materials. Companies that lead the way in validating these sustainable materials for structural applications will capture a growing segment of environmentally conscious industrial and commercial clients.

Structural Foam Market Size and Share Analysis:

The global Structural Foam market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material and application highlighting their respective contributions to overall market performance.

By material, the Polypropylene subsegment dominated the market in 2025 because its low density significantly reduces the overall weight of finished parts while maintaining the structural rigidity needed for heavy-duty industrial use, offering a superior cost-to-performance ratio compared to other polymers.

By application, the Automotive subsegment dominated the market in 2025 driven by the material's ability to replace heavy metal parts with lightweight foam structures that provide excellent crashworthiness, acoustic insulation, and vibration damping in modern vehicle architectures.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

SABIC

BASF SE

Covestro AG

Evonik Industries AG

Dow Inc.

Arkema S.A.

LyondellBasell Industries N.V.

Armacell International S.A.

SGL Carbon SE

Gurit Holding AG

Get more information on this report

Structural Foam Market Report Coverage and Deliverables:

The "Structural Foam Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Structural Foam market size and forecast at the regional and country levels for segments covered under the scope

Structural Foam market trends, as well as drivers, restraints, and opportunities

Structural Foam market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Structural Foam market

Detailed company profiles, including SWOT analysis

Structural Foam Market Geographic Insights:

The geographical scope of the Structural Foam market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintained its leadership in the Global Structural Foam Market in 2025, supported by a highly developed industrial base and a strong emphasis on technological innovation in the automotive and logistics sectors. The United States, in particular, drives regional demand through its massive material handling industry, which relies heavily on structural foam for the production of heavy-duty pallets, bulk containers, and specialty crates used in cross-border trade. Furthermore, the region`s dominance is reinforced by the presence of major automotive OEMs who have pioneered the use of structural foam for vehicle lightweighting and battery protection in response to North American fuel efficiency standards (CAFE).

The region also benefits from a robust construction sector that is increasingly adopting structural foam for specialized insulation and architectural components. Strict building codes in Canada and the U.S. regarding energy efficiency have made high-performance foam materials a standard in modern commercial and residential projects. Additionally, North America is a hub for R&D in sustainable polymer science, with many leading chemical companies headquartered in the region focusing on the development of low-VOC and bio-attributed resins. This combination of advanced manufacturing capabilities, high regulatory standards, and a strong culture of material innovation ensures that North America will remain the primary value center for the global structural foam market.

Get more information on this report

Structural Foam Market Research Report Guidance:

The report includes qualitative and quantitative data in the Structural Foam market across material, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Structural Foam market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Structural Foam market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Structural Foam market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the Structural Foam market segments by material, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Structural Foam market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Structural Foam Market News and Key Development:

The Structural Foam market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Structural Foam market are:

In June 2024, Sheela Foam Limited announced that it had strengthened its product portfolio and manufacturing capabilities in India, rolling out new foam-based comfort and technical products, including structural foam solutions for furniture, automotive, and industrial applications.

In March 2022, Sheela Foam Limited announced that it was focusing on high-margin technical foam products, including polyurethane structural foams, as part of its strategic move to expand into automotive, acoustics, and industrial end-use markets.

Key Sources Referred:

Society of Plastics Engineers (SPE)American Chemistry Council (ACC)Polyurethane Foam Association (PFA)European Association of Foamed Plastics (EAFP)International Association of Plastics Distribution (IAPD)ASTM International - Committee on Plastics and FoamsCompany WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Structural Foam Market

SABIC

BASF SE

Covestro AG

Evonik Industries AG

Dow Inc.

Arkema S.A.

LyondellBasell Industries N.V.

Armacell International S.A.

SGL Carbon SE

Gurit Holding AG

Frequently Asked Questions

How big is the Structural Foam Market?

The Structural Foam Market is valued at US$ 38.83 Billion in 2025, it is projected to reach US$ 53.14 Billion by 2033.

What is the CAGR for Structural Foam Market by (2026 - 2033)?

As per our report Structural Foam Market, the market size is valued at US$ 38.83 Billion in 2025, projecting it to reach US$ 53.14 Billion by 2033. This translates to a CAGR of approximately 4.00% during the forecast period.

What segments are covered in this report?

The Structural Foam Market report typically cover these key segments-

Material (Polyethylene, Polypropylene, Polystyrene, Polyurethane, Other Materials)

Application (Material Handling, Building & Construction, Automotive, Electrical & Electronics, Other Applications)

What is the historic period, base year, and forecast period taken for Structural Foam Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Structural Foam Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Structural Foam Market?

The Structural Foam Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

SABIC

BASF SE

Covestro AG

Evonik Industries AG

Dow Inc.

Arkema S.A.

LyondellBasell Industries N.V.

Armacell International S.A.

SGL Carbon SE

Gurit Holding AG

Who should buy this report?

The Structural Foam Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Structural Foam Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Structural Foam Market

Get Free Sample For Structural Foam Market