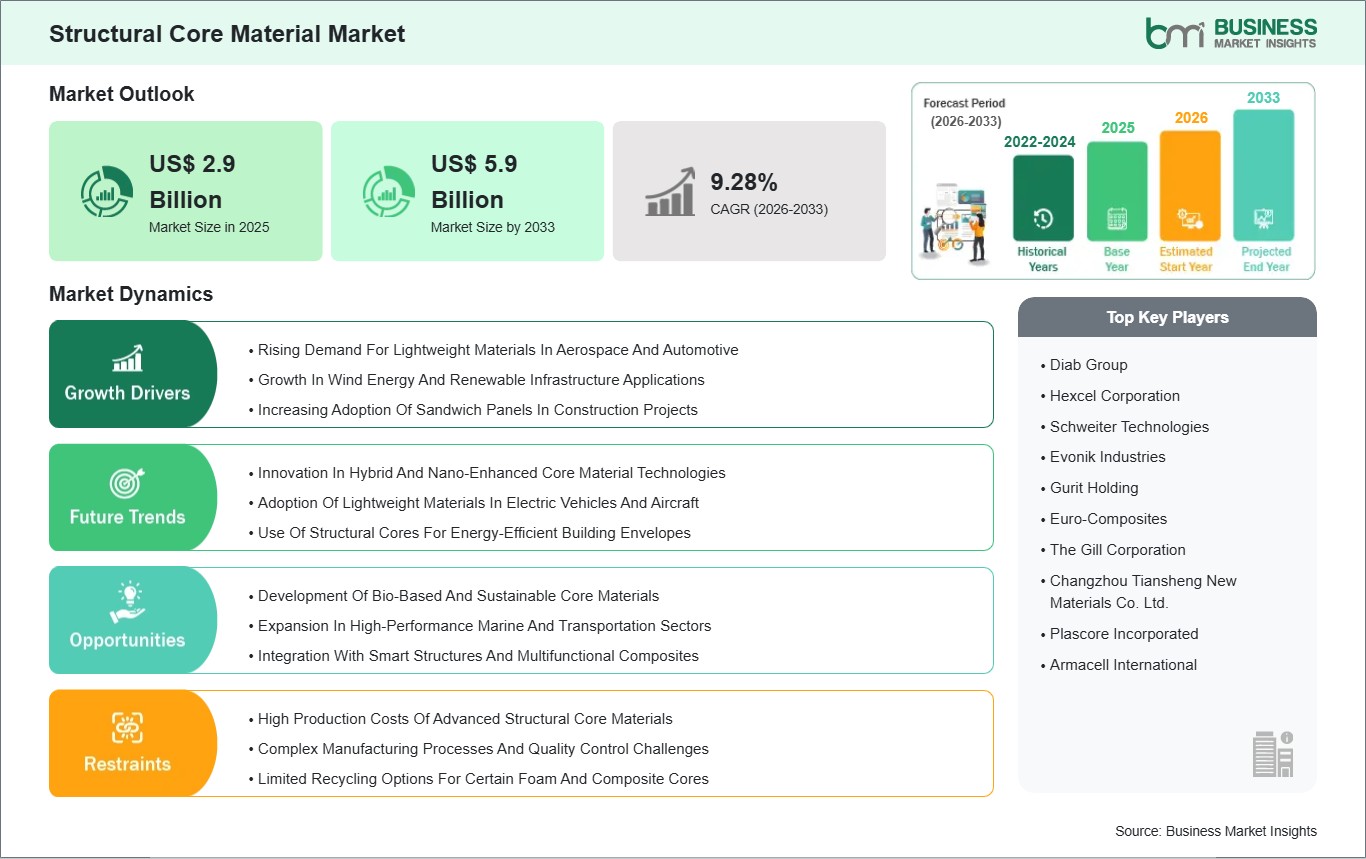

The Structural Core Material Market size is expected to reach US$ 5.9 billion by 2033 from US$ 2.9 billion in 2025. The market is estimated to record a CAGR of 9.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global structural core material market experiences rapid growth because industries require engineered products that maintain lightweight design optimal performance, and sustainable environmental practices. Structural core materials—such as foam cores, honeycomb cores, balsa wood, and other engineered core solutions—are essential components in composite structures that require high strength-to-weight ratios. The materials function as the internal framework of sandwich constructions to deliver rigidity and impact resistance together with full structural stability while reducing total weight. The materials serve crucial functions in multiple industries, which include aerospace and automotive, marine and wind energy and construction because they provide necessary performance and durability. The market experiences its primary growth driver because global markets are shifting towards using lightweight composite materials.

The aerospace industry demands advanced core materials for wings, floor panels and interior components because customers want better fuel economy and operational efficiency. Automotive manufacturers utilize structural core materials for body panels, battery enclosures and chassis components because these materials enhance energy efficiency and crash protection without reducing vehicle safety.

The renewable energy sector especially wind turbine blade manufacturing, drives high market demand for strong yet lightweight core materials, which rotor blades need to endure mechanical forces throughout their extended service periods. Construction professionals increasingly select sandwich panels that contain strong core materials for their facade and roofing system and modular building needs because these panels maintain both structural integrity and thermal insulation functions. The market encounters specific limitations that exist despite strong demand factors that drive market growth. The high-performance core materials industry faces production cost challenges that restrict their use in budget-restricted markets.

Manufacturers face difficulties in producing advanced honeycomb and high-performance foam cores because these materials need exact manufacturing methods and complete production control. The choice of materials is being affected by sustainability issues, which research into environmentally friendly material options because traditional core materials contain non-renewable materials and create recycling problems after their useful life ends. The market will experience growth through ongoing development of core design and manufacturing technologies and hybrid material integration methods.

The next generation of structural core materials is being developed through the rising need for multifunctional cores that combine thermal management with vibration damping and embedded sensor capabilities. The global structural core material market will continue to expand because industries across the world are now focusing on performance, sustainability and weight reduction.

Structural Core Material Market - Strategic Insights:

Get more information on this report

Structural Core Material Market Segmentation Analysis:

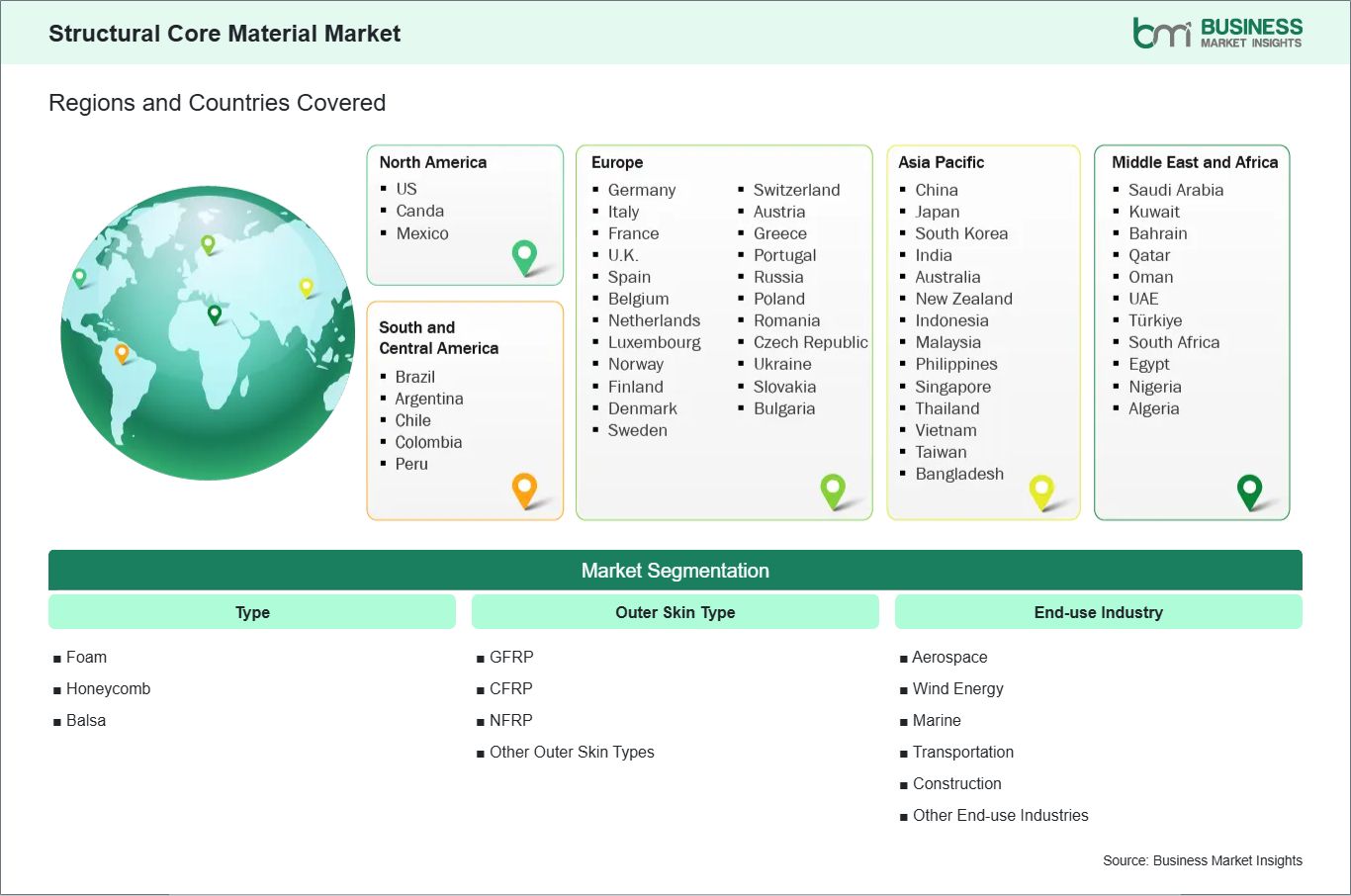

Key segments that contributed to the derivation of the structural core material market analysis are type, outer skin type, and end‑use industry.

By type, the structural core material market is segmented into foam, honeycomb, balsa. The foam segment dominated the market in 2025.

Based on outer skin type, the structural core material market is categorized into GFRP, CFRP, NFRP, other outer skin types. The GFRP (Glass Fiber Reinforced Polymer) segment dominated the market in 2025.

In terms of end‑use industry, the structural core material market is categorized into aerospace, wind energy, marine, transportation, construction, other end‑use industries. The aerospace segment dominated the market in 2025.

Structural Core Material Market Drivers and Opportunities:

Rising Demand For Lightweight Materials In Aerospace And Automotive

The structural core material market is growing because aerospace and automotive industries need lightweight materials. Manufacturers are using honeycomb cores and foam cores, and balsa wood to create aircraft components, automotive body panels and battery enclosures which need lightweight materials that still offer structural strength. Lightweight cores make aerospace operations more efficient by reducing fuel consumption, and they also improve electric vehicles energy use and driving range, which makes them crucial for environmentally friendly transportation projects.

Advanced composites, which use high-performance cores serve aerospace applications through their use in fuselage panels, interior partitions and wing structures. The aerospace industry needs materials that create strong aircraft components that must remain lightweight while withstanding high-stress situations. The automotive industry uses structural cores to create electric and hybrid vehicle systems, which include crash structures and floor panels, and energy storage enclosures that provide both safety and operational efficiency.

Core material producers, aerospace OEMs and automotive manufacturers work together to create partnerships that help their technologies gain wider acceptance. North America and Europe lead in using advanced cores because their aerospace and automotive sectors have reached maturity while Asia-Pacific accelerates production to fulfill increasing market requirements. The ongoing development of technological solutions and material enhancements establishes structural cores as essential elements for achieving lightweight design throughout worldwide transportation systems.

Development Of Bio-Based And Sustainable Core Materials

Sustainability is increasingly influencing the structural core material market, prompting the development of bio-based and environmentally friendly cores. Manufacturers are exploring renewable resources, such as balsa wood, natural fiber composites, and bio-derived foams, to replace traditional petroleum-based cores. These materials provide similar mechanical properties while reducing environmental impact, appealing to industries prioritizing eco-friendly practices.

The construction sector has been a major driver for sustainable core materials, with sandwich panels, roofing, and facades integrating bio-based cores to enhance energy efficiency and reduce carbon footprint. In aerospace and automotive, manufacturers are testing hybrid cores combining natural fibers with lightweight polymers, aiming to balance performance, weight reduction, and sustainability. These innovations address end-of-life disposal challenges and align with growing regulatory pressure for greener material usage in manufacturing.

Collaborations between material scientists, research institutes, and industrial manufacturers are crucial to commercializing these sustainable cores. North America and Europe are at the forefront of research and adoption due to advanced R&D infrastructure and stringent environmental standards, while Asia-Pacific is gradually integrating bio-based cores in automotive and construction projects. The shift toward sustainable cores is set to redefine structural core material selection across global industries.

Structural Core Material Market Size and Share Analysis:

The structural core material market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type, outer skin type, and end‑use industry, offering insights into their contribution to overall market performance.

By type, the foam subsegment dominated the market in 2025, driven by its lightweight nature, cost-effectiveness, and versatility for use in various composite structural applications.

Based on outer skin type, the GFRP (Glass Fiber Reinforced Polymer) subsegment dominated the market in 2025, driven by its durability, low cost, and widespread adoption across multiple industries.

On the basis of end‑use industry, the aerospace subsegment dominated the market in 2025, driven by the high demand for lightweight, high-strength materials to improve fuel efficiency and performance in aircraft and spacecraft.

Structural Core Material Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Diab Group

Hexcel Corporation

Schweiter Technologies

Evonik Industries

Gurit Holding

Euro-Composites

The Gill Corporation

Changzhou Tiansheng New Materials Co. Ltd.

Plascore Incorporated

Armacell International

Get more information on this report

Structural Core Material Market Report Coverage and Deliverables:

The "Structural Core Material Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Structural Core Material Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Structural Core Material Market trends, as well as drivers, restraints, and opportunities

Structural Core Material Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Structural Core Material Market

Detailed company profiles, including SWOT analysis

Structural Core Material Market Geographic Insights:

The geographical scope of the Structural Core Material Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global structural core material market demonstrates distinct regional characteristics, with North America emerging as the dominant region due to its advanced aerospace, automotive, and renewable energy sectors, as well as its well-established R&D ecosystem for lightweight and high-performance composites. North American manufacturers lead in the adoption of honeycomb, foam, and hybrid core materials for aircraft interiors, automotive battery enclosures, wind turbine blades, and construction sandwich panels, benefiting from strong collaboration between industry, academia, and research institutes that drives innovation and rapid commercialization.

The market in Asia Pacific shows rapid expansion because large-scale industrialization, urbanization and infrastructure growth take place in China, Japan and South Korea. The aerospace, automotive, and renewable energy sectors in this region are increasingly adopting structural core materials in lightweight vehicles, wind turbine blades, and high-performance composites for railway and marine applications.

The European aerospace, automotive and building construction industries drive structural core material usage through established regulations and strict quality requirements and their commitment to sustainable practices especially in Germany and France and the Nordic countries, which are beginning to adopt energy-efficient building panels and lightweight vehicle components.

The Middle East and Africa region now shows increasing use of structural cores for renewable energy projects, aerospace maintenance operations and industrial construction work with United Arab Emirates and South Africa investing in infrastructure development and advanced manufacturing systems.

The South and Central American market develops through infrastructure development and construction industry adoption of sandwich panels and new automotive and marine technology projects in Brazil and Argentina.

The growth of all regions proceeds through lightweighting programs and industrial energy use, and fresh developments in advanced structural core material technology.

Get more information on this report

Structural Core Material Market Research Report Guidance:

The report includes qualitative and quantitative data in the Structural Core Material Market across type, outer skin type, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Structural Core Material Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Structural Core Material Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Structural Core Material Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Structural Core Material Market segments by type, outer skin type, end‑use industry and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Structural Core Material Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Structural Core Material Market News and Key Development:

The Structural Core Material Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the structural core material market are:

In March 2026, Hexcel announced that it would unveil breakthrough composite solutions for aerospace, defense, and automotive markets at JEC World 2026, showcasing its full range of advanced materials, including honeycomb cores, engineered core structures, and other composite solutions. This presentation reflects Hexcel`s continued commitment to expanding its structural material offerings for multiple high‑performance applications globally and strengthening industrial collaborations with partners such as FACC, Duqueine, and Arkema.

In September 2025, Gurit announced that it secured a multi‑year contract to supply its Corecell structural foam core to the subsea industry, enabling the company to expand its operations in the Asia‑Pacific region with a new facility near Brisbane, Australia in support of this long‑term agreement. Corecell is a high‑performing structural core material based on styrene acrylonitrile resin that continues to see global demand in demanding composite applications beyond traditional markets.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Structural Core Material Market

Diab Group

Hexcel Corporation

Schweiter Technologies

Evonik Industries

Gurit Holding

Euro-Composites

The Gill Corporation

Changzhou Tiansheng New Materials Co. Ltd.

Plascore Incorporated

Armacell International

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Structural Core Material Market?

The Structural Core Material Market is valued at US$ 2.9 Billion in 2025, it is projected to reach US$ 5.9 Billion by 2033.

What is the CAGR for Structural Core Material Market by (2026 - 2033)?

As per our report Structural Core Material Market, the market size is valued at US$ 2.9 Billion in 2025, projecting it to reach US$ 5.9 Billion by 2033. This translates to a CAGR of approximately 9.28% during the forecast period.

What segments are covered in this report?

The Structural Core Material Market report typically cover these key segments-

Type (Foam, Honeycomb, Balsa)

Outer Skin Type (GFRP, CFRP, NFRP, Other Outer Skin Types)

End-use Industry (Aerospace, Wind Energy, Marine, Transportation, Construction, Other End-use Industries)

What is the historic period, base year, and forecast period taken for Structural Core Material Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Structural Core Material Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Structural Core Material Market?

The Structural Core Material Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Diab Group

Hexcel Corporation

Schweiter Technologies

Evonik Industries

Gurit Holding

Euro-Composites

The Gill Corporation

Changzhou Tiansheng New Materials Co. Ltd.

Plascore Incorporated

Armacell International

Who should buy this report?

The Structural Core Material Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Structural Core Material Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Structural Core Material Market

Get Free Sample For Structural Core Material Market