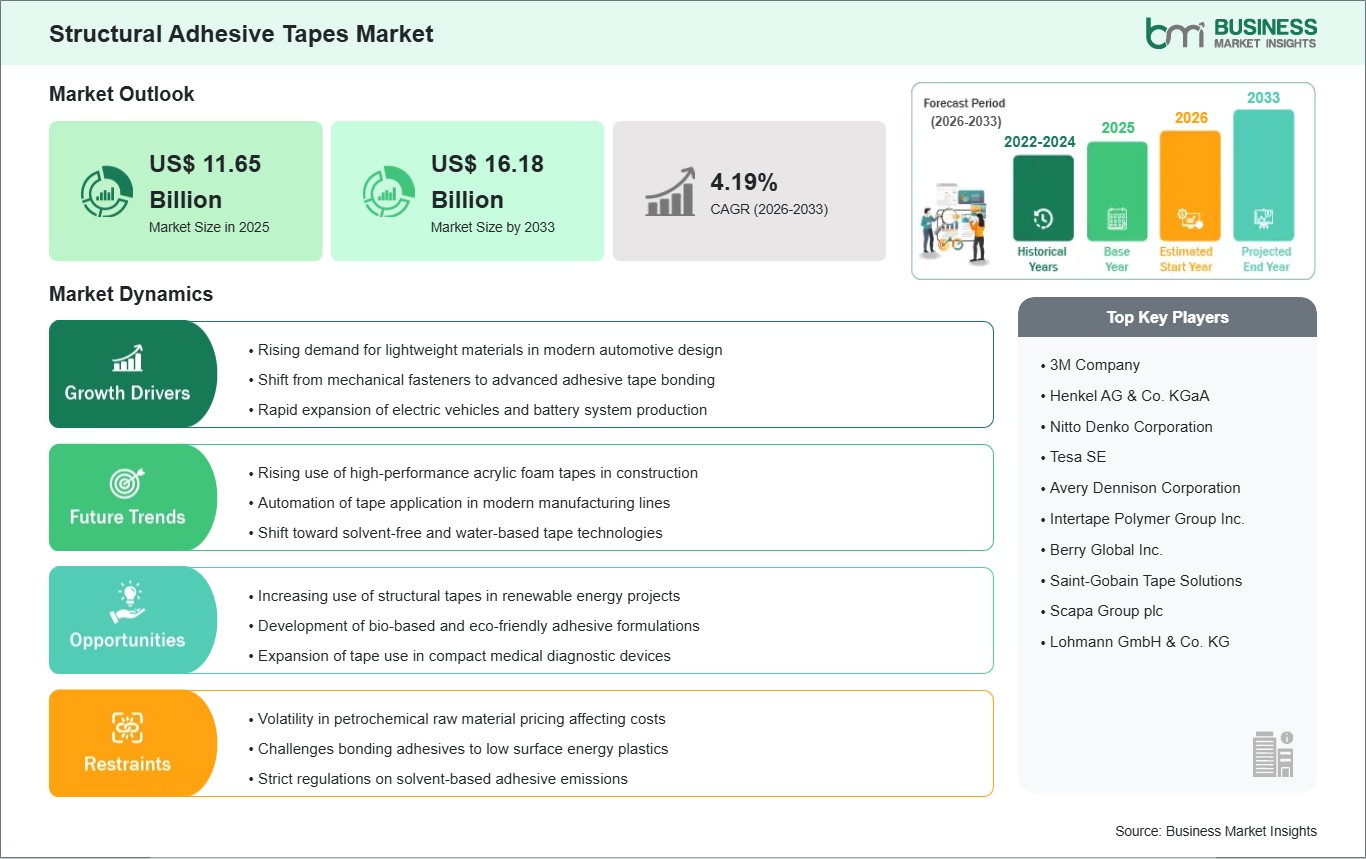

Escalating Demand for Lightweight Materials

The most important driver in the structural adhesive tapes industry is the global trend towards "light weighting," which is particularly prevalent in the transportation industry. As fuel efficiency regulations become increasingly stringent and the move towards electric vehicles (EVs) gathers pace, the importance of reducing the overall weight of the vehicle's body and internal components has become paramount. In this respect, traditional fastening materials like bolts, screws, and rivets are extremely detrimental to the fuel efficiency of vehicles, since they tend to add substantial weight to the overall structure, while the drilling of holes to accommodate these fasteners compromises the integrity of thin-gauge materials. Structural adhesive tapes, on the other hand, offer an extremely sophisticated solution to this problem, since they enable the joining of thin-gauge materials like aluminum, carbon fiber, and high-strength composites.

Unlike traditional fastening materials, which impose point loads on the materials being joined, structural adhesive tapes impose even stress across the entire surface area, thus preventing stress concentrations that often cause cracks and failure in materials like aluminum and carbon fiber. The use of high-strength adhesive tapes enables manufacturers to employ materials with reduced gauges without compromising the integrity or stiffness of the overall structure. This weight reduction is especially critical in EVs, where every gram saved directly contributes to extending the driving range of the vehicle, making adhesive tapes an essential technology for the next generation of mobility.

Furthermore, the move toward light weighting is also driven by the aesthetic and aerodynamic requirements of modern industrial design. Adhesive tapes allow for completely smooth exterior surfaces, which reduces air drag and improves the visual appeal of consumer products and vehicles alike. The ability of these tapes to bond dissimilar materials—such as a plastic trim to a metal door—without the risk of galvanic corrosion or thermal expansion mismatch makes them the preferred choice for engineers. As industries continue to prioritize material efficiency, the role of structural tapes as a primary joining method will only continue to expand.

Increasing Adoption in Renewable Energy Projects

The transition to a sustainable energy grid presents a massive opportunity for the structural adhesive tapes market, specifically in the wind and solar power sectors. Solar panel manufacturing requires robust bonding solutions that can withstand 25 years of exposure to harsh UV radiation, rain, and extreme temperature cycles. Structural tapes are increasingly used to bond solar cells to their frames and to attach junction boxes, providing a permanent seal that prevents moisture ingress and electrical failure. Compared to traditional liquid adhesives, tapes offer faster processing times and no "cure-time" bottlenecks, significantly increasing factory throughput.

In the wind energy sector, structural tapes are finding critical use in the assembly of massive turbine blades and internal nacelle components. As wind turbines increase in size to capture more power, the mechanical loads on the blade structures become immense. Tapes are used for leading-edge protection and to bond internal stiffeners, where their ability to absorb vibrations and resist fatigue is vital for long-term reliability. The lightweight nature of adhesive tapes also helps in maintaining the balance and efficiency of the blades, which is a key factor in lowering the levelized cost of energy for wind farm operators.

Beyond the energy generation stage, the expansion of green energy infrastructure—including large-scale battery storage systems (BESS)—creates further demand. These storage units require high-strength bonding for thermal management components and structural housing. As government subsidies for renewable energy continue to rise in North America and Europe, the demand for high-performance, weather-resistant structural tapes is poised for substantial growth. Tape manufacturers who can provide specialized products with documented long-term durability in outdoor environments will have a significant competitive advantage in this high-value infrastructure segment.