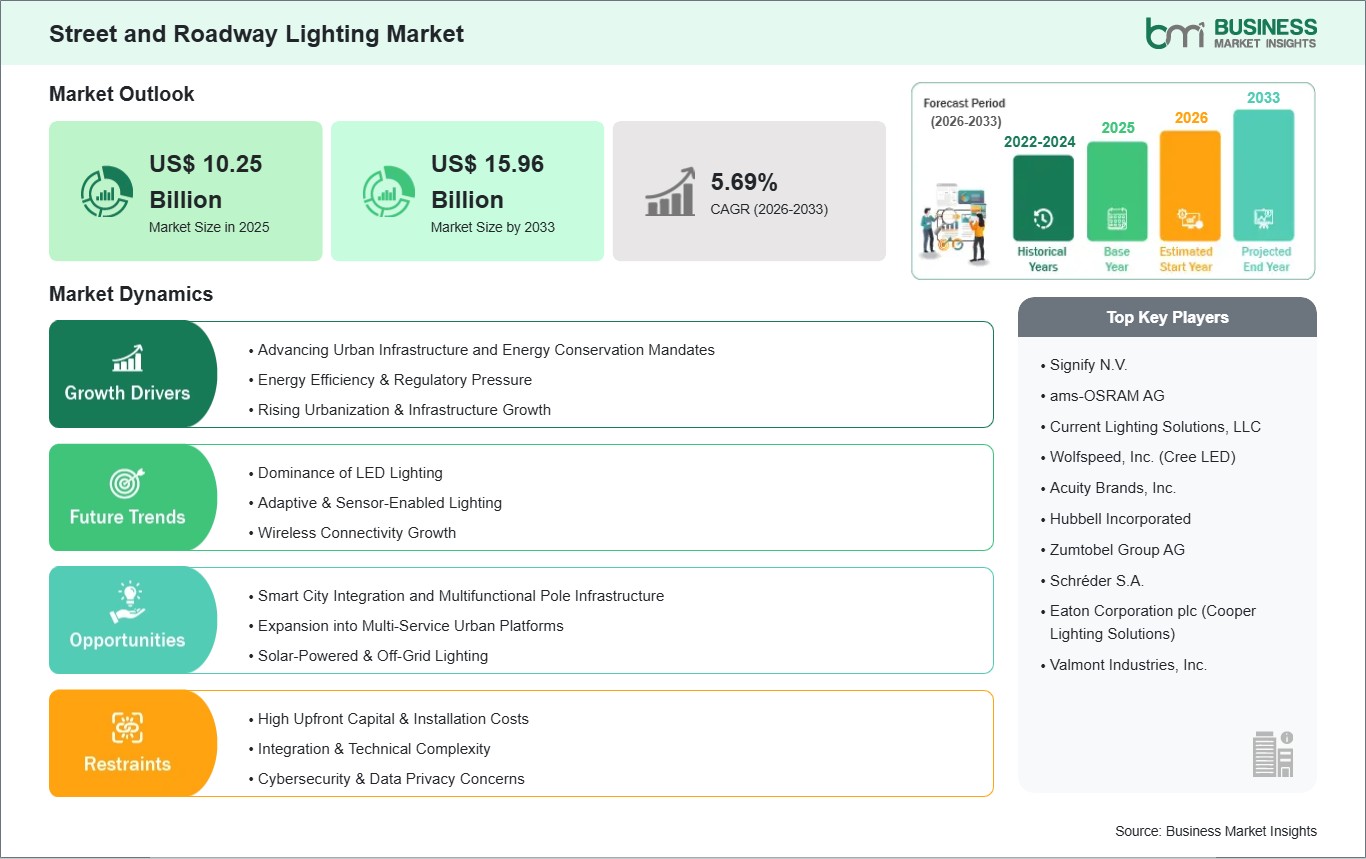

The Street and Roadway Lighting Market size is expected to reach US$ 15.96 billion by 2033 from US$ 10.25 billion in 2025. The market is estimated to record a CAGR of 5.69% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Street and roadway lighting refers to the specialized outdoor illumination systems designed to provide visibility and safety for motorists, pedestrians, and cyclists on public thoroughfares. These systems comprise luminaires (light fixtures), lamps (LED or conventional sources), poles, and control mechanisms. Modern roadway lighting is increasingly transitioning from "static" illumination to "intelligent" systems that can adjust brightness based on traffic density, weather conditions, or ambient light levels, serving as a critical pillar for both traffic safety and urban energy management. Market expansion is primarily attributed to the rising global demand for energy-efficient LED retrofitting, the rapid acceleration of Smart City initiatives, and the increasing integration of renewable energy (solar/wind) sources into public lighting networks.

However, several challenges can restrain market growth: high initial procurement and installation costs for smart, connected systems can strain the capital improvement budgets of smaller municipalities, despite the promise of long-term savings. Stringent regulatory hurdles regarding light pollution (Dark Sky compliance) and evolving cybersecurity standards for connected infrastructure lengthen the time-to-market and increase administrative overhead. Additionally, the industry faces constraints due to interoperability issues between different lighting management software and supply chain volatility in the LED driver and semiconductor sectors, which can delay large-scale infrastructure projects by several months.

Despite these hurdles, the market holds immense opportunities in the universal mandate for carbon neutrality and the accelerating deployment of AI-driven adaptive dimming, which optimizes light levels in real-time to protect local wildlife and reduce energy waste. The expansion of Public-Private Partnerships (PPPs) and Energy Service Company (ESCO) models, allowing cities to pay for upgrades through energy savings, and the development of off-grid solar lighting for rural roadway expansion are expected to create significant opportunities for market growth.

Street and Roadway Lighting Market - Strategic Insights:

Get more information on this report

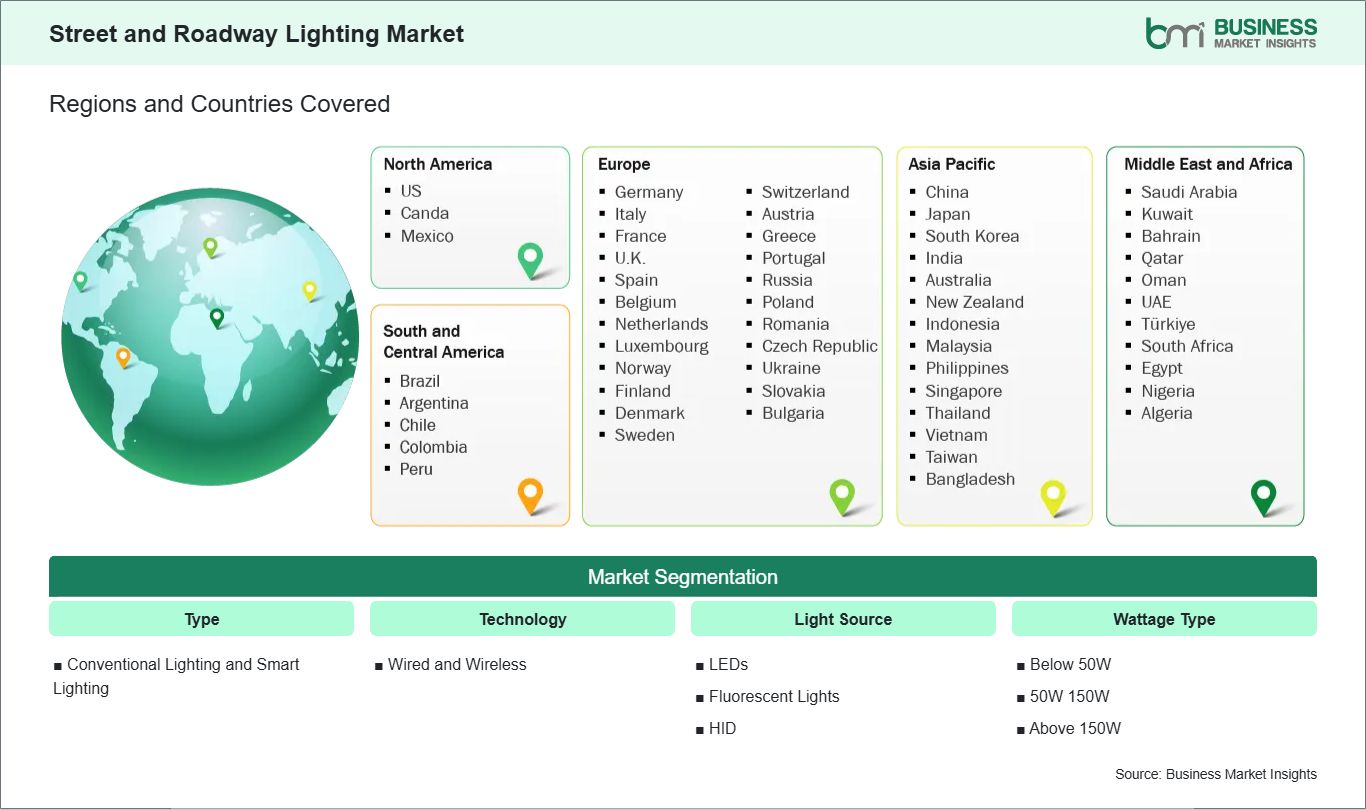

Street and Roadway Lighting Market Segmentation Analysis:

Key segments that contributed to the derivation of the Street and Roadway Lighting market analysis are type, technology, light source, and wattage type.

By Type, the market is segmented into Conventional Lighting and Smart Lighting.

By Technology, the market is divided into Wired and Wireless.

By Light Source, the market is categorized into LEDs, Fluorescent Lights, and HID.

By Wattage Type, the market is segmented into Below 50W, 50W‑150W, and Above 150W.

Street and Roadway Lighting Market Drivers and Opportunities:

Advancing Urban Infrastructure and Energy Conservation Mandates

The primary driver for the Street and Roadway Lighting Market is the intensifying global push for energy-efficient urban infrastructure and the implementation of stringent environmental regulations. As of 2026, municipalities are aggressively transitioning from legacy high-pressure sodium (HPS) and fluorescent systems to advanced LED technology, which can reduce energy consumption by up to 50%, a critical factor given that street lighting can account for nearly 40% of a city`s total energy expenditure. This momentum is further fueled by rapid urbanization and large-scale roadway expansion projects, particularly in emerging economies across the Asia-Pacific region. Furthermore, the global mandate for "net-zero" cities has turned public lighting into a non-discretionary focus for carbon reduction strategies. Governments are increasingly providing financial incentives and "Green City" grants to accelerate the adoption of adaptive lighting solutions that improve nighttime visibility and public safety while simultaneously lowering operational costs and light pollution. Together, these factors ensure that modern roadway lighting is now a foundational pillar of sustainable, high-velocity urban development.

Smart City Integration and Multifunctional Pole Infrastructure

A significant high-value opportunity lies in the convergence of Street Lighting with IoT-enabled Smart City ecosystems and 5G connectivity. Modern lighting poles are increasingly being viewed as "vertical real estate" capable of hosting a wide array of smart sensors for traffic management, environmental monitoring, and public Wi-Fi. There is also a major growth frontier in the deployment of Integrated Electric Vehicle (EV) Charging Poles, which utilize existing electrical infrastructure to provide accessible charging points in dense urban environments where space is at a premium. Furthermore, the rise of AI-driven Adaptive Lighting and Predictive Maintenance presents an opportunity for "connected" systems that automatically adjust brightness based on real-time traffic flow or weather conditions, drastically extending luminaire lifespans and reducing maintenance visits. Manufacturers who focus on solar-powered hybrid lighting for off-grid rural connectivity and those pioneering "lighting-as-a-service" (LaaS) business models, allowing cities to upgrade infrastructure with zero upfront capital, are positioned to lead the most innovative and high-margin segments of the global outdoor lighting market.

Street and Roadway Lighting Market Size and Share Analysis:

Based on type, the Smart Lighting subsegment is experiencing the fastest growth, although Conventional Lighting still maintains a considerable presence in regions with legacy infrastructure. Smart lighting systems are indispensable for modern "connected cities" because they integrate sensors and networking to facilitate autonomous brightness adjustment based on traffic density and ambient light. A notable trend in 2026 is the adoption of "Edge-AI" within these systems, allowing light poles to double as environmental monitoring stations and EV charging points. These innovations are particularly vital for municipalities looking to maximize their return on investment, providing a multi-functional utility that extends far beyond simple illumination.

Street and Roadway Lighting Market Report Highlights:

Street and Roadway Lighting Market Report Coverage and Deliverables:

The "Street and Roadway Lighting Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Street and Roadway Lighting market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Street and Roadway Lighting market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Street and Roadway Lighting market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Street and Roadway Lighting market

Detailed company profiles, including SWOT analysis

Street and Roadway Lighting Market Geographic Insights:

The geographical scope of the Street and Roadway Lighting market report is divided into five regions: North America, Asia Pacific, Europe, Middle East and Africa, and South and Central America.

The Asia-Pacific Street and Roadway Lighting Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. This region is emerging as the fastest-growing market globally, with China and India leading the regional expansion. The growth is primarily fueled by extensive roadway electrification and the proliferation of "Smart City" missions that integrate cloud-based lighting controls with urban utility networks. Japan and South Korea further bolster the region's position through early adoption of advanced IoT-enabled luminaires and high-efficiency solar lighting solutions in rural and off-grid areas.

Growth is further bolstered by a significant shift toward subscription-based "Light-as-a-Service" (LaaS) models among municipalities looking to modernize their infrastructure without high upfront capital expenditure. The integration of adaptive dimming sensors and AI-assisted traffic monitoring into lighting poles, alongside the rising demand for sustainable, solar-powered fixtures in the post-pandemic recovery era, solidifies Asia-Pacific as a critical hub for innovation and the future scaling of the street and roadway lighting industry.

Get more information on this report

Street and Roadway Lighting Market Research Report Guidance:

The report includes qualitative and quantitative data in the Street and Roadway Lighting market across type, technology, light source, wattage type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Street and Roadway Lighting market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Street and Roadway Lighting market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Street and Roadway Lighting market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Street and Roadway Lighting market segments by type, technology, light source, and wattage type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Street and Roadway Lighting market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Street and Roadway Lighting Market News and Key Development:

The Street and Roadway Lighting market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Street and Roadway Lighting market are:

In January 2025, TRT introduced the Aspect Gen2 product range, the next-generation upgrade to its successful Aspect Gen1 series. The new range features models with 32, 64, 96, and 128 LEDs, with the larger models optimized for highway illumination. Incorporating innovations such as the patent-granted MountSet universal mounting system, Tool-Less Access for easy maintenance, and PowerSet NFC for programmable power output and dimming, the launch enhances efficiency, adaptability, and reliability in street and roadway lighting. This development strengthens market offerings and supports sustainable infrastructure upgrades.

In September 2025, Signify expanded its professional lighting portfolio with the launch of four new products: SunStay Pro gen2, SunStay Pro gen2 mini, GreenVision Xceed Pro, and ActiStar. The SunStay Pro series offers modular, connected solar streetlighting for bike paths, campuses, and pedestrian areas, featuring sustainable designs with up to 80% recycled materials. The GreenVision Xceed Pro provides flexible, energy-efficient street lighting adaptable to urban and rural applications, while the ActiStar delivers advanced LED floodlighting for sports and outdoor facilities. These innovations enhance energy efficiency, sustainability, and connectivity in street, roadway, and sports lighting markets worldwide.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Street and Roadway Lighting Market

Signify N.V.

ams-OSRAM AG

Current Lighting Solutions, LLC

Wolfspeed, Inc. (Cree LED)

Acuity Brands, Inc.

Hubbell Incorporated

Zumtobel Group AG

Schréder S.A.

Eaton Corporation plc (Cooper Lighting Solutions)

Valmont Industries, Inc.

Frequently Asked Questions

How big is the Street and Roadway Lighting Market?

The Street and Roadway Lighting Market is valued at US$ 10.25 Billion in 2025, it is projected to reach US$ 15.96 Billion by 2033.

What is the CAGR for Street and Roadway Lighting Market by (2026 - 2033)?

As per our report Street and Roadway Lighting Market, the market size is valued at US$ 10.25 Billion in 2025, projecting it to reach US$ 15.96 Billion by 2033. This translates to a CAGR of approximately 5.69% during the forecast period.

What segments are covered in this report?

The Street and Roadway Lighting Market report typically cover these key segments-

Type (Conventional Lighting and Smart Lighting)

Technology (Wired and Wireless)

Light Source (LEDs, Fluorescent Lights, and HID)

Wattage Type (Below 50W, 50W 150W, and Above 150W)

What is the historic period, base year, and forecast period taken for Street and Roadway Lighting Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Street and Roadway Lighting Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Street and Roadway Lighting Market?

The Street and Roadway Lighting Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Street and Roadway Lighting Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Street and Roadway Lighting Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Street and Roadway Lighting Market

Get Free Sample For Street and Roadway Lighting Market