01

Market Summery

Executive Summary and Global Market Analysis

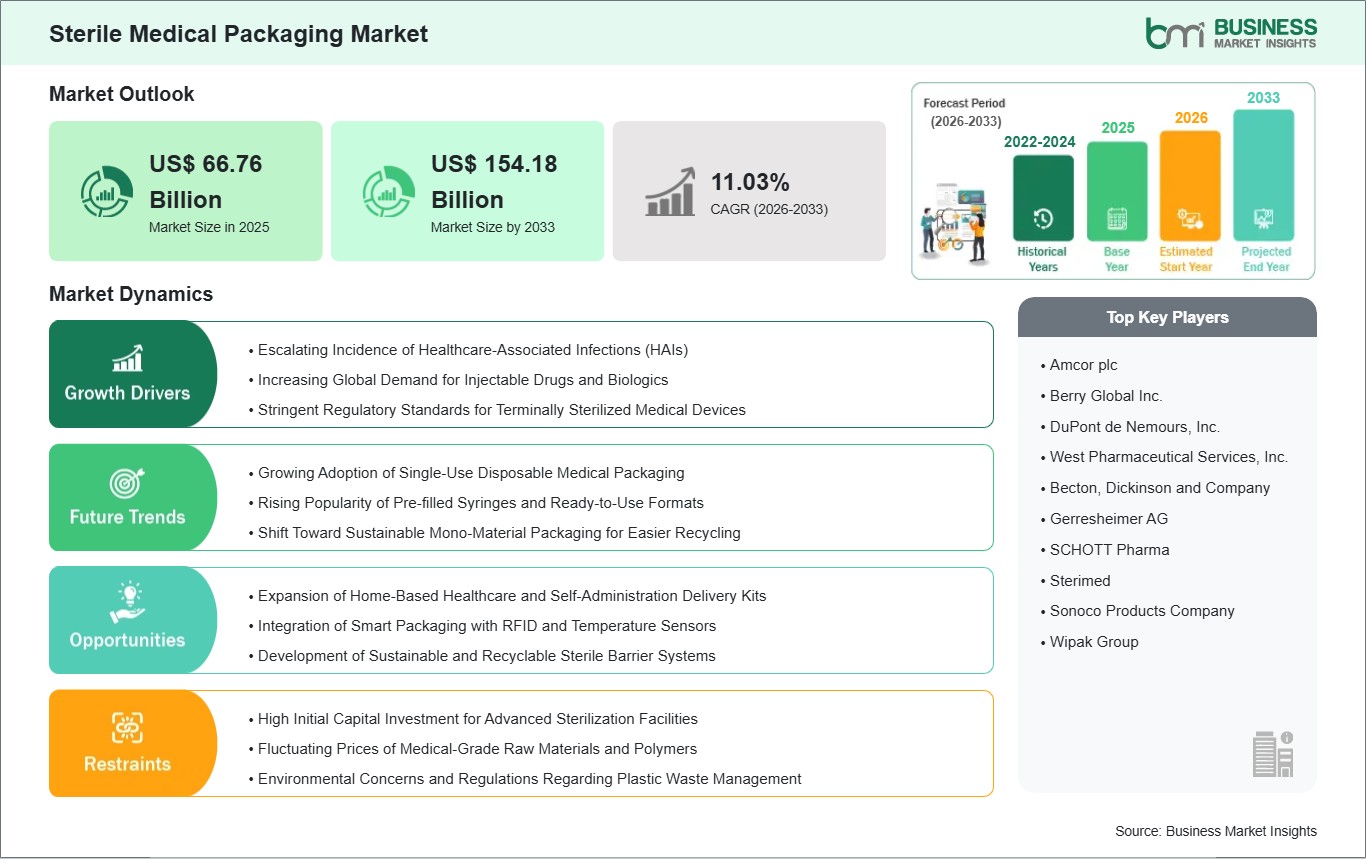

The global sterile medical packaging market is defined by its strong emphasis on material science; therefore, advanced polymers and rigid thermoforming solutions are used to create protective packaging for a variety of life-saving devices and pharmaceutical products. The rapid increase in the number of healthcare-associated infections has driven significant growth in this industry as it has led manufacturers to move towards terminally sterilizing their products and using single-use medical disposables (which can reduce the risk of cross-contamination). Additionally, as high-value biologics and more complicated injectable therapies enter the market, pharmaceutical manufacturers are using more sophisticated forms of primary packaging (e.g., pre-fillable syringes and vials) that are now the leading source of technological innovation and regulatory scrutiny. Strategic market movements in 2025 have centered on balancing the uncompromising requirements of sterility with a growing corporate responsibility toward environmental sustainability.

Although the market is dealing with challenges related to plastic waste, the increasing use of recyclable medical grade materials and technological advancements (i.e., smart tracking systems) will allow the world`s healthcare supply chain to be more efficient and achieve a closed loop (circular) system. Looking ahead, the expansion of home-based healthcare and the continuous modernization of hospital infrastructure in emerging economies will remain the dominant themes, ensuring that sterile packaging remains an indispensable and growing sector of the broader medical technology industry.

03

Segment Analysis

Sterile Medical Packaging Market Segmentation

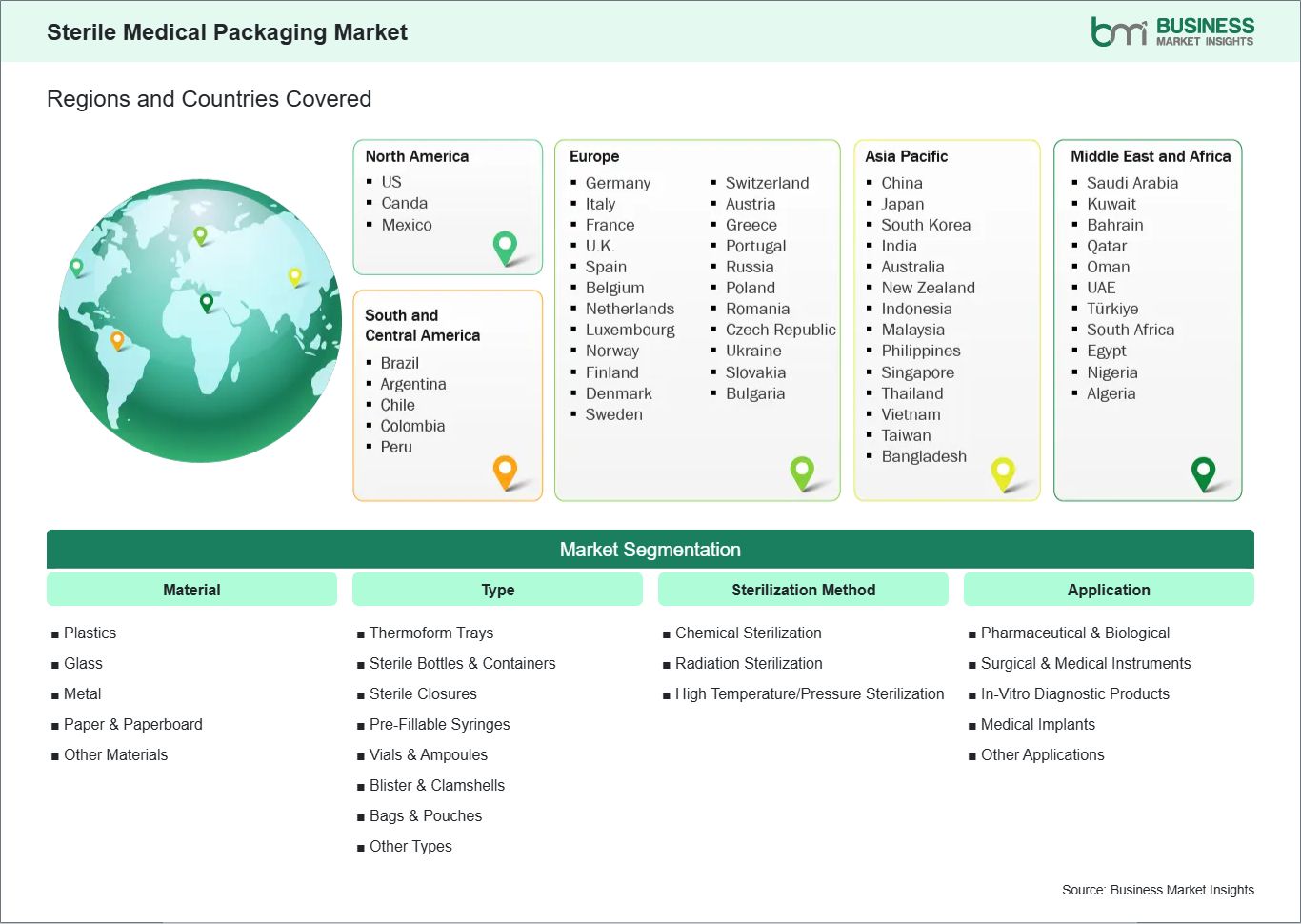

Key segments that contributed to the derivation of the Sterile Medical Packaging market analysis are material, type, sterilization method, and application.

- By material, the market is segmented into Plastics, Glass, Metal, Paper & Paperboard, and Others. The Plastics segment dominated the market in 2025.

- By type, the market is segmented into Thermoform Trays, Sterile Bottles & Containers, Sterile Closures, Pre-Fillable Syringes, Vials & Ampoules, Blister & Clamshells, Bags & Pouches, and Others. The Thermoform Trays segment dominated the market in 2025.

- By sterilization method, the market is segmented into Chemical Sterilization, Radiation Sterilization, and High Temperature/Pressure Sterilization. The Chemical Sterilization segment dominated the market in 2025.

- By application, the market is segmented into Pharmaceutical & Biological, Surgical & Medical Instruments, In-Vitro Diagnostic Products, Medical Implants, and Others. The Pharmaceutical & Biological segment dominated the market in 2025.

04

Market Forces

Sterile Medical Packaging Market Drivers and Opportunities

Escalating Incidence of Healthcare-Associated Infections

The growing prevalence of Healthcare-Associated Infections (HAIs) presents a major challenge to the global healthcare system by impacting patient recovery times and contributing to increased overall hospital mortality rates. The majority of HAIs occur when the microbial barrier of a medical device or instrument becomes compromised through improper or damaged packaging. Therefore, there is an increasing emphasis on developing advanced sterile barrier systems capable of providing complete protection from the time they leave manufacturing facilities until the time they are used in the clinical environment. As a result, sterile packaging has moved from being seen as merely a logistical requirement to being considered an important aspect of infection control procedures.

Regulatory bodies and healthcare providers are increasingly prioritizing terminally sterilized products that minimize human intervention. The shift toward single-use sterile kits for surgical procedures is a primary example of this trend. By using pre-packaged, pre-sterilized instruments, hospitals can significantly reduce the risks associated with on-site sterilization errors. This systemic change in hospital procurement is driving manufacturers to innovate with high-performance materials that offer visible tamper-evidence, ensuring that the aseptic field is maintained during the opening process in a high-pressure operating environment.

Moreover, the financial burden of treating HAIs has encouraged healthcare institutions to invest in more reliable packaging solutions. Extended patient stays and the high cost of additional antibiotic treatments make the use of premium sterile packaging a cost-effective preventative strategy. As surgical volumes return to high levels and the complexity of minimally invasive procedures increases, the demand for specialized packaging that can protect delicate robotic and laparoscopic tools continues to grow, cementing the role of high-integrity sterile packaging as an essential driver of patient safety in modern medicine.

Expansion of Home-Based Healthcare

More patients are handling their treatments at home instead of in hospitals. That change comes because people are living longer and getting more chronic illnesses like diabetes and rheumatoid arthritis. As a result, packaging must protect medical supplies well and still be easy to use for people who aren’t trained in medicine. Companies can build packages with simple ways to open them and built-in safety for throwing away needles. The demand for this kind of packaging is growing fast. This trend gives manufacturers a clear chance to innovate in the field. Packaging needs to work well with daily life, not just in clinics. Designing it that way improves how people follow treatment plans.

In particular, the rise of biologics and specialty medicines has fueled the demand for self-injection systems, such as autoinjectors and pre-filled syringes. These devices require primary packaging that ensures the long-term stability and sterility of sensitive drug formulations while being stored in domestic settings. The expansion of e-pharmacies and direct-to-patient delivery models further complicates the logistics of maintaining sterility. Packaging for this sector must be engineered to survive the "last mile" of delivery, which often involves multiple handling stages and exposure to uncontrolled environments. This requires secondary and tertiary packaging innovations that provide robust physical protection for the primary sterile barrier. By focusing on these specialized home-care needs, packaging companies can tap into a rapidly evolving market that prioritizes convenience, safety, and long-term compliance for patients managing their health outside of clinical facilities.

05

Size and Share Analysis

Sterile Medical Packaging Market Size and Share Analysis

The global Sterile Medical Packaging market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material, type, sterilization method, and application, highlighting their respective contributions to overall market performance.

By material, the Plastics subsegment dominated the market in 2025 because its high versatility allows for the engineering of multi-layered barrier films that are compatible with diverse sterilization techniques while remaining the most cost-effective solution for mass-produced medical disposables.

By type, the Thermoform Trays subsegment dominated the market in 2025 due to its ability to provide a customized, secure fit for heavy orthopedic and cardiovascular implants, preventing movement within the package that could cause punctures or compromise the sterile seal.

By sterilization method, the Chemical Sterilization subsegment dominated the market in 2025 because it provides deep penetration for complex device geometries and is uniquely suited for the large-scale industrial sterilization of pre-packaged, ready-to-use medical kits.

By application, the Pharmaceutical & Biological subsegment dominated the market in 2025 driven by the rigorous regulatory standards governing injectable medications, which mandate the highest levels of sterility assurance to prevent life-threatening microbial contamination in patients.

07

Report Coverage

Sterile Medical Packaging Market Report Coverage and Deliverables

The "Sterile Medical Packaging Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Sterile Medical Packaging market size and forecast at the regional and country levels for segments covered under the scope

- Sterile Medical Packaging market trends, as well as drivers, restraints, and opportunities

- Sterile Medical Packaging market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Sterile Medical Packaging market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Sterile Medical Packaging Market Geographic Insights

The geographical scope of the Sterile Medical Packaging market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintained its position as the leading regional market in 2025, supported by a highly advanced healthcare infrastructure and a stringent regulatory framework that mandates the highest levels of sterility assurance. The United States, as a global hub for medical device innovation and pharmaceutical research, accounts for a significant portion of the demand, driven by a vast number of surgical procedures and a rapid shift toward outpatient care. The region`s market dominance is further reinforced by the presence of major industry players and a well-established supply chain for medical-grade polymers. These factors, combined with high healthcare expenditure per capita, create a fertile environment for the adoption of premium sterile packaging solutions. The regional market is also characterized by a swift uptake of Smart Packaging technologies, as U.S. based hospitals increasingly integrate digital inventory management systems to track the shelf-life and sterility of medical supplies.

While the Asia-Pacific region is experiencing the fastest growth due to expanding hospital networks and a booming pharmaceutical manufacturing sector, North America remains the primary driver of value and technical standards. Federal initiatives aimed at reducing hospital-acquired infections have forced a systemic move toward ready-to-use sterile kits, which has significantly benefited manufacturers of thermoform trays and flexible pouches. This concentration of innovation and high-volume demand ensures that North America will continue to set the global trajectory for sterile packaging trends through the end of the decade.

10

Industry Activity

Recent Developments

The Sterile Medical Packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Sterile Medical Packaging market are:

- In April 2023, DuPont announced that it had introduced Tyvek® 40L, a new sterile medical packaging material engineered to improve durability and sustainability, targeting applications in surgical instruments and implant packaging.

- In September 2023, West Pharmaceutical Services announced that it had expanded its sterile packaging operations in North America, adding new capacity to meet rising demand for injectable drug packaging and biologics.

- In June 2024, Sonoco announced that it had launched a new line of eco-friendly sterile medical packaging solutions, including recyclable paper-based systems, aligning with global sustainability and regulatory requirements in healthcare.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

ASTM International - Committee on Medical Packaging Healthcare Packaging Consortium (HPC) Sterile Barrier Association (SBA, Europe) Institute of Packaging Professionals (IoPP) Company Websites Company Annual Reports Company Investor Presentations