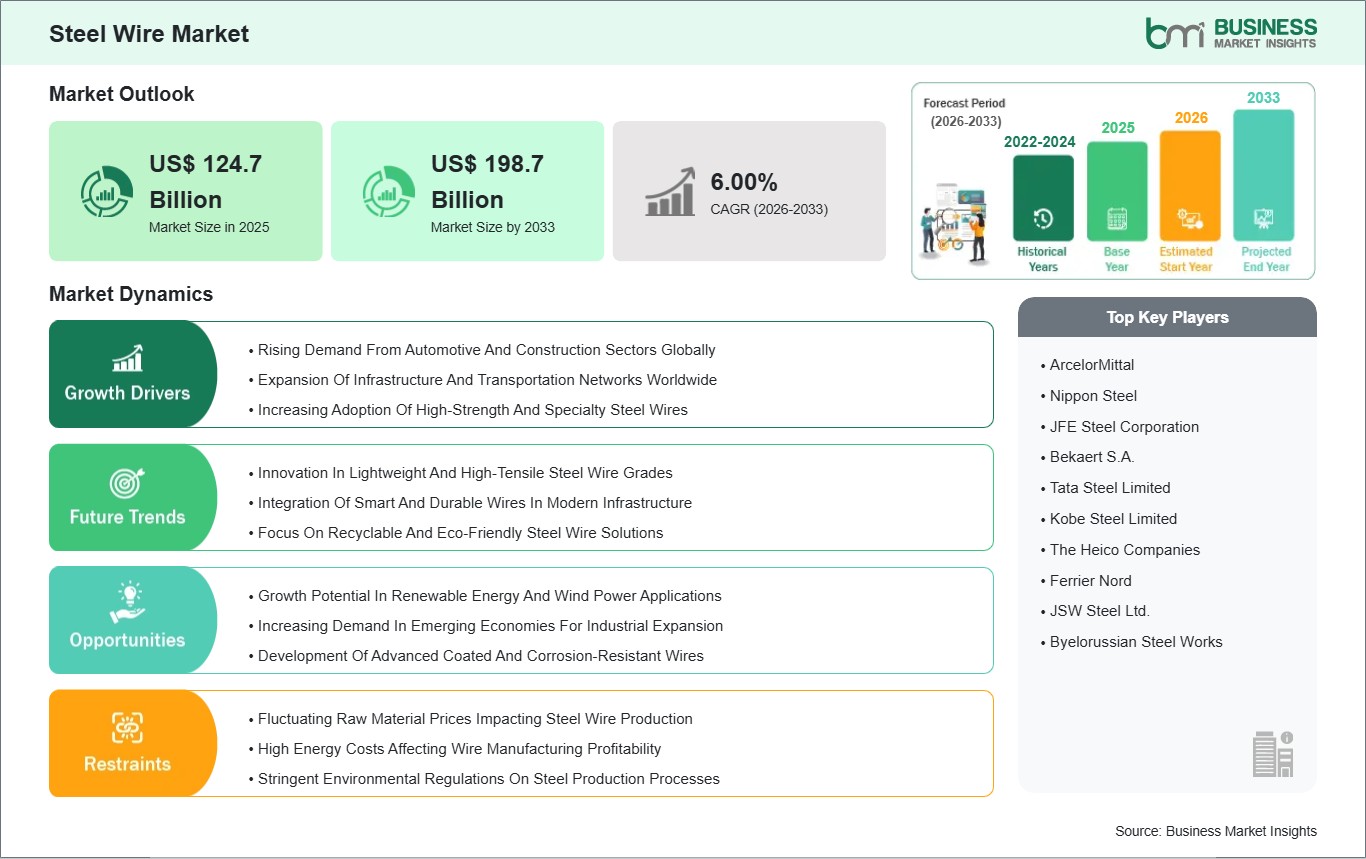

The Steel Wire Market size is expected to reach US$ 198.7 billion by 2033 from US$ 124.7 billion in 2025. The market is estimated to record a CAGR of 6.00% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global steel wire market serves as an essential part of the entire steel and metals industry because it provides vital basic materials used in infrastructure construction and automotive manufacturing, industrial machinery production and consumer durable goods creation, and energy production work. The tensile strength of steel wires combined with their flexibility, fatigue resistance and economical production costs makes them vital for various uses, which include concrete reinforcement, fencing, power transmission and tire cord production. The worldwide demand for steel wire products depends on the progress made in major construction work, the automotive manufacturing process and the implementation of modern industrial systems. The market growth proceeds through the development of specialized wire products, which emerge from technological progress in wire drawing and surface treatment methods that create wires with advanced performance features for particular market needs. Infrastructure development functions as the main factor that drives the global steel wire market.

The construction of transportation networks, high-rise buildings and utility systems requires steel wires for structural reinforcement, which authorities in different regions have identified as an essential infrastructure need. The automotive industry uses steel wire materials to manufacture various components, which include tire reinforcement materials, springs and fasteners. Vehicle manufacturers implement high-performance steel wire grades to develop vehicle components that require both lightweight and high-strength and durable attributes. The oil and gas industry, the mining sector and heavy machinery operations create a major demand for wire products that need to provide dependable and durable performance to survive extreme working conditions. The global steel wire market encounters obstacles, even though strong demand fundamentals exist.

The production of wire faces ongoing profitability dangers, which arise from budget constraints that result from raw material price changes, including variations in scrap prices, iron ore costs and alloying element expenses. The market experiences disturbances through trade policy changes and tariff shifts, which create supply chain disruptions that impact the competitiveness of exporting and importing nations. The steelmaking industry faces increasing operational pressure because environmental regulations and sustainability targets require manufacturers to implement cleaner production methods and efficient resource utilization techniques. The ongoing development of infrastructure projects together with the advancement of automotive technologies and the expansion of industrial activities will create continuous worldwide demand for steel wire products in both emerging and established markets.

Steel Wire Market - Strategic Insights:

Get more information on this report

Steel Wire Market Segmentation Analysis:

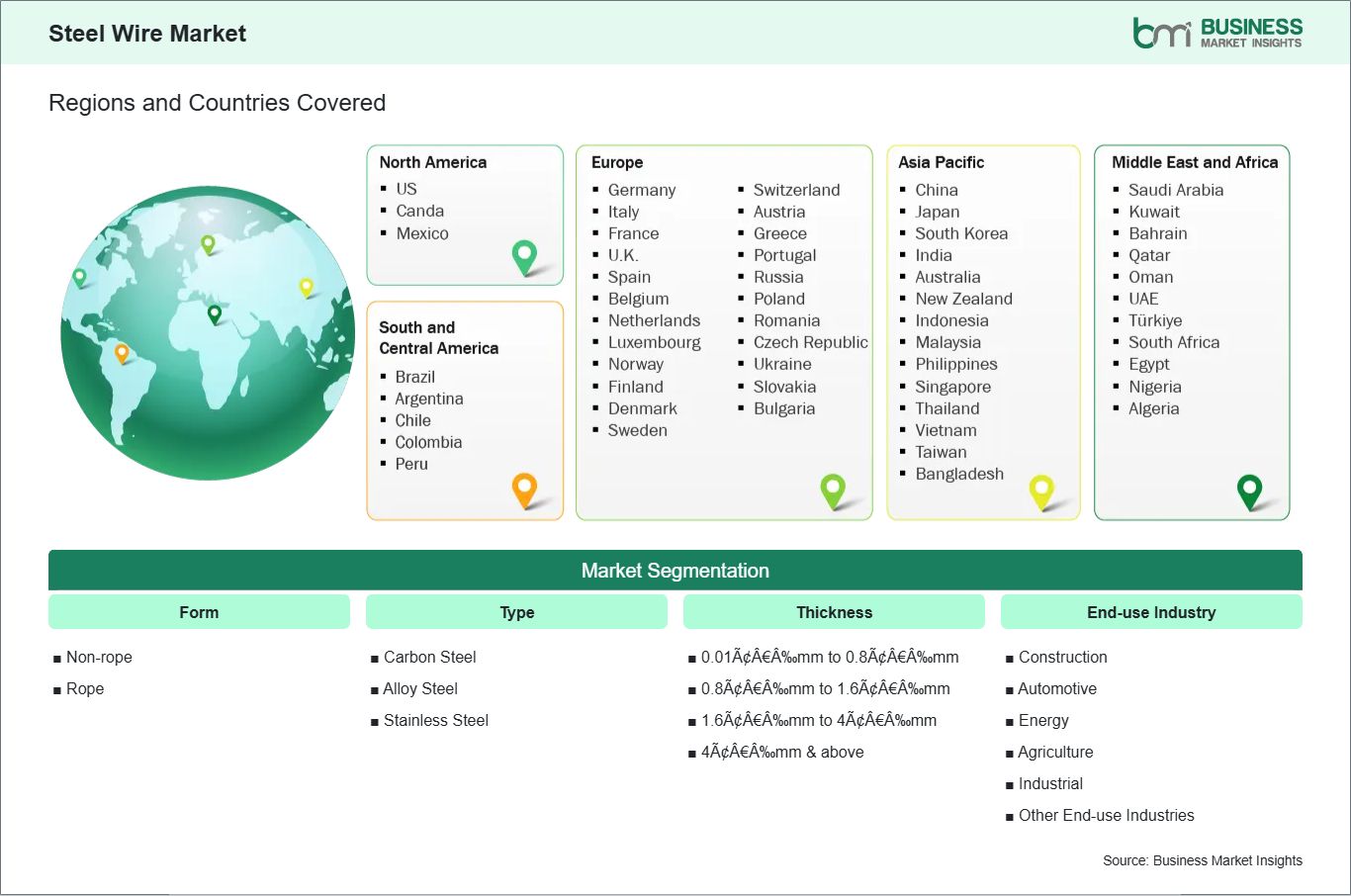

Key segments that contributed to the derivation of the steel wire market analysis are form, type, thickness, and end‑use industry.

By form, the steel wire market is segmented into non‑rope, rope. The non‑rope segment dominated the market in 2025.

Based on type, the steel wire market is categorized into carbon steel, alloy steel, stainless steel. The carbon steel segment dominated the market in 2025.

On the basis of thickness, the steel wire market is categorized into 0.01 mm to 0.8 mm, 0.8 mm to 1.6 mm, 1.6 mm to 4 mm, 4 mm & above. The 1.6 mm to 4 mm segment dominated the market in 2025.

In terms of end‑use industry, the steel wire market is categorized into construction, automotive, energy, agriculture, industrial, other end‑use industries. The construction segment dominated the market in 2025.

Steel Wire Market Drivers and Opportunities:

Rising Demand From Automotive And Construction Sectors Globally

The global steel wire market is heavily influenced by the growth of the automotive and construction sectors, which together account for a substantial portion of steel wire consumption. In the automotive industry, steel wires are essential in tire reinforcement, suspension systems, fasteners, and springs. Manufacturers are increasingly adopting high-tensile strength wires to enhance vehicle safety, reduce weight, and improve overall performance. The global push for more durable and lightweight components has led to the development of specialized wire grades that meet strict automotive standards, driving demand worldwide.

In construction, steel wire is widely used in reinforced concrete, pre-stressed structures, bridges, and cable systems. Rapid urbanization and infrastructure development in emerging economies, coupled with modernization projects in developed regions, have elevated the requirement for high-quality steel wire. Architects and engineers prioritize materials that can deliver long-term stability, resist environmental stress, and support innovative designs. Pre-stressed concrete and high-strength cable systems are increasingly favored, directly benefiting steel wire consumption.

Additionally, integration between wire producers and end-use industries has facilitated customized solutions that cater to regional construction and automotive needs. North America, for instance, focuses on advanced wire products for automotive safety, while Asia-Pacific emphasizes large-scale infrastructure projects. Europe leverages specialty wires for engineered construction applications. This cross-industry collaboration ensures that steel wire manufacturers can respond to evolving specifications, enhancing product adoption globally and reinforcing the market`s steady growth trajectory

Growth Potential In Renewable Energy And Wind Power Applications

Renewable energy infrastructure, particularly wind power, presents a growing opportunity for the global steel wire market. Steel wires are integral to the manufacturing of wind turbine cables, support structures, and tension systems, requiring high tensile strength and fatigue resistance to withstand dynamic operational conditions. With governments worldwide investing heavily in sustainable energy, the demand for specialized steel wires that meet these rigorous standards is increasing. Advanced wire technologies provide the durability and flexibility needed for turbine blades, nacelle reinforcements, and tower cables.

In addition to wind energy, solar power and other renewable projects are also driving demand for durable wire products. Transmission lines, anchor cables, and structural support systems rely on steel wires that can endure environmental stressors such as wind, snow, and UV exposure. This has encouraged manufacturers to develop coated, corrosion-resistant, and pre-stressed steel wire variants suitable for long-term performance in renewable infrastructure projects across regions such as Europe, North America, and Asia-Pacific.The ongoing transition toward cleaner energy sources creates opportunities for innovation in wire production. Companies are investing in R&D to produce high-performance, lightweight, and fatigue-resistant steel wires, which can extend the lifespan of renewable installations while reducing maintenance costs. As renewable energy adoption accelerates globally, the steel wire market is expected to benefit from sustained demand, positioning renewable energy infrastructure as a critical driver of long-term growth in the sector.

Steel Wire Market Size and Share Analysis:

The steel wire market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within form, type, thickness, and end‑use industry, offering insights into their contribution to overall market performance.

By form, the non‑rope subsegment dominated the market in 2025, driven by its widespread use in general industrial applications and easier manufacturability compared to rope steel wires.

Based on type, the carbon steel subsegment dominated the market in 2025, driven by its cost-effectiveness, high tensile strength, and versatility across multiple industries.

In terms of thickness, the 1.6 mm to 4 mm subsegment dominated the market in 2025, driven by its suitability for most construction and industrial applications, balancing strength and flexibility requirements.

On the basis of end‑use industry, the construction subsegment dominated the market in 2025, driven by the growing global infrastructure and real estate development, which heavily relies on steel wire for reinforcement and structural purposes.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

ArcelorMittal

Nippon Steel

JFE Steel Corporation

Bekaert S.A.

Tata Steel Limited

Kobe Steel Limited

The Heico Companies

Ferrier Nord

JSW Steel Ltd.

Byelorussian Steel Works

Get more information on this report

Steel Wire Market Report Coverage and Deliverables:

The "Steel Wire Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Steel Wire Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Steel Wire Market trends, as well as drivers, restraints, and opportunities

Steel Wire Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Steel Wire Market

Detailed company profiles, including SWOT analysis

Steel Wire Market Geographic Insights:

The geographical scope of the Steel Wire Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The North American steel wire market dominates because its industrial framework, automotive industry and infrastructure development initiatives have reached advanced stages. North America uses its integrated steelmaking and wire-drawing facilities to create specialized steel wires that meet critical needs in tire reinforcement and suspension systems, pre-stressed concrete and bridge cables and energy infrastructure. The region maintains constant demand because urban modernization projects, transportation network development and renewable energy projects require strong steel wires, which offer durability and superior performance. North America maintains its market leadership through its automotive sector, which promotes the use of advanced wire products that fulfill stringent safety standards and performance needs and weight reduction targets.

Asia Pacific industrial growth together with expanding urban centers and rising investments in building construction and vehicle manufacturing create essential market development opportunities. China India, and Japan together function as both major steel wire consumers and major steel wire manufacturing nations. The demand for steel wire products arises from the construction of major infrastructure projects, which include high-rise buildings, metro rail systems and bridges and from the growth of automotive production and consumer goods manufacturing. The region also witnesses rising adoption of high-strength and corrosion-resistant wire grades to address environmental and operational challenges.

Europe maintains a significant presence because it has an established automotive manufacturing base, advanced construction and energy infrastructure, and it produces high-strength and specialty wires that engineers use in their work. The wire manufacturing processes have developed new technologies because companies need to meet stricter environmental and quality requirements.

The Middle East and Africa market expands because cities grow, infrastructure develops, and energy projects increase particularly in the United Arab Emirates and South Africa, which use steel wires for construction and power transmission and industrial applications.

The South and Central America region experiences ongoing economic development because countries like Brazil and Argentina invest in infrastructure projects, industrial growth and automotive manufacturing expansion. The industrial sector faces two main obstacles, which are cost sensitivity and supply chain variations, but steel wire products are becoming more popular because of rising industrialization and urban development.

The demand for products across different regions depends on three factors, which include infrastructure development and the current state of industries, automotive production rates and advancements in wire manufacturing technology.

Get more information on this report

Steel Wire Market Research Report Guidance:

The report includes qualitative and quantitative data in the Steel Wire Market across form, type, thickness, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Steel Wire Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Steel Wire Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Steel Wire Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Steel Wire Market segments by form, type, thickness, end‑use industry and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Steel Wire Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Steel Wire Market News and Key Development:

The Steel Wire Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the steel wire market are:

In February 2025, SeAH Besteel announced that it developed a new special steel wire rod material tailored for energy and oil‑gas applications, enhancing cleanliness and resistance to hydrogen‑induced cracking for challenging service environments. This product expansion broadens the company`s wire portfolio beyond traditional bars and rods, signaling a strategic push into specialized industrial segments.

In May 2025, Bansal Wire Industries highlighted strategic investments near Tata Nagar for a new steel wire manufacturing plant, aimed at strengthening backward integration and supporting its wire production capabilities. While details are part of a regulatory filing, this development underscores the company`s commitment to expanding global supply capacity to meet growing demand.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Steel Wire Market

ArcelorMittal

Nippon Steel

JFE Steel Corporation

Bekaert S.A.

Tata Steel Limited

Kobe Steel Limited

The Heico Companies

Ferrier Nord

JSW Steel Ltd.

Byelorussian Steel Works

Frequently Asked Questions

How big is the Steel Wire Market?

The Steel Wire Market is valued at US$ 124.7 Billion in 2025, it is projected to reach US$ 198.7 Billion by 2033.

What is the CAGR for Steel Wire Market by (2026 - 2033)?

As per our report Steel Wire Market, the market size is valued at US$ 124.7 Billion in 2025, projecting it to reach US$ 198.7 Billion by 2033. This translates to a CAGR of approximately 6.00% during the forecast period.

What segments are covered in this report?

The Steel Wire Market report typically cover these key segments-

Form (Non-rope, Rope)

Type (Carbon Steel, Alloy Steel, Stainless Steel)

Thickness (0.01âmm to 0.8âmm, 0.8âmm to 1.6âmm, 1.6âmm to 4âmm, 4âmm & above)

End-use Industry (Construction, Automotive, Energy, Agriculture, Industrial, Other End-use Industries)

What is the historic period, base year, and forecast period taken for Steel Wire Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Steel Wire Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Steel Wire Market?

The Steel Wire Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ArcelorMittal

Nippon Steel

JFE Steel Corporation

Bekaert S.A.

Tata Steel Limited

Kobe Steel Limited

The Heico Companies

Ferrier Nord

JSW Steel Ltd.

Byelorussian Steel Works

Who should buy this report?

The Steel Wire Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Steel Wire Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Steel Wire Market

Get Free Sample For Steel Wire Market