By device type, the spine surgery devices market is categorized into spinal decompression devices, spinal fusion devices, arthroplasty / disc replacement devices, fracture repair devices, motion-preservation / non-fusion devices. The spinal fusion devices segment dominated the market in 2025. Spinal fusion devices dominance stems from their wide application in treating degenerative disc disease, spinal instability, deformities, and trauma. Fusion procedures are well established clinically with predictable long-term outcomes, driving physician preference and reimbursement support. Surgeons also rely on fusion implants (e.g., pedicle screws, interbody cages) for structural stability across diverse pathology severities.

By procedure type, the market is bifurcated into open spine surgery, minimally-invasive spine surgery. The open spine surgery segment held a larger share of the market in 2025. Open spine surgery leads because it remains the standard for complex, multi-level fusions, severe deformity corrections, and extensive neural decompressions. Its long clinical history, surgeon familiarity, and ability to directly visualize anatomy make it indispensable for challenging cases where minimally invasive access is limited or unsuitable. However, MIS is growing rapidly in simpler procedures due to lower trauma and quicker recovery.

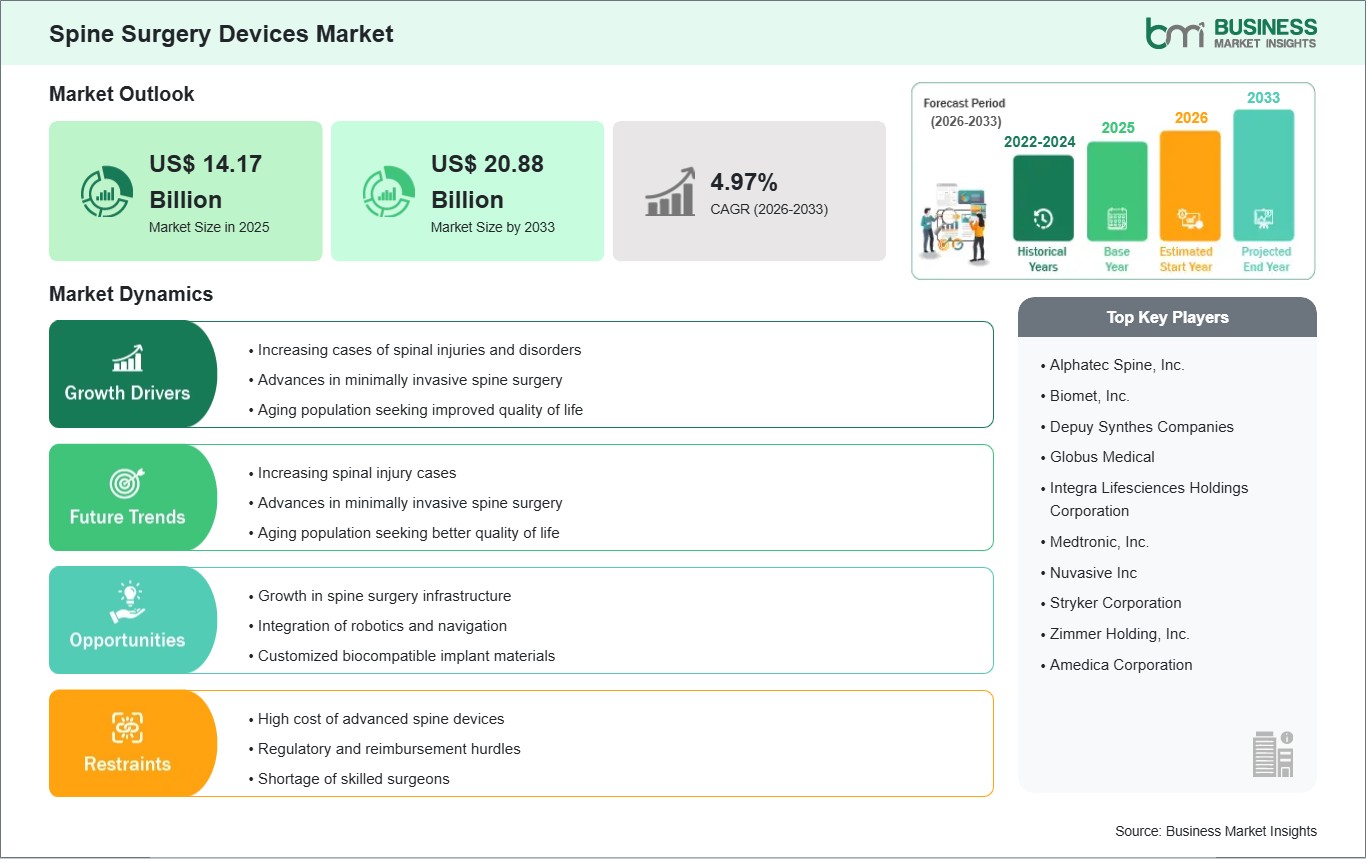

By surgical technology, the market is segmented into robotic-assisted systems, AR/VR-navigated systems, traditional navigation and imaging-guided. The traditional navigation and imaging-guided segment held the largest share of the market in 2025. Traditional navigation and imaging guided technologies generate the most revenue as they are widely adopted across spine procedures due to established accuracy, surgeon trust, and integration with existing operating room workflows. While newer technologies like robotic assistance and AR/VR navigation are expanding fast and improving precision, traditional systems remain foundational in many surgical centers because of lower complexity, broader clinical validation, and lower incremental cost.

By surgery setting, the spine surgery devices market is segmented into hospitals, ambulatory surgery centers, specialty clinics. The hospitals segment dominated the market in 2025. Hospitals lead as the primary setting for spine surgery devices, driven by their capacity to handle complex cases, invest in costly equipment, and support multidisciplinary care teams. They maintain high patient volume, advanced imaging/OR infrastructure, and specialist surgeons, making them the default for both traditional and advanced minimally invasive or robotic procedures. Ambulatory surgical centers are growing rapidly for less complex or same day surgeries, but hospitals remain the dominant venue.