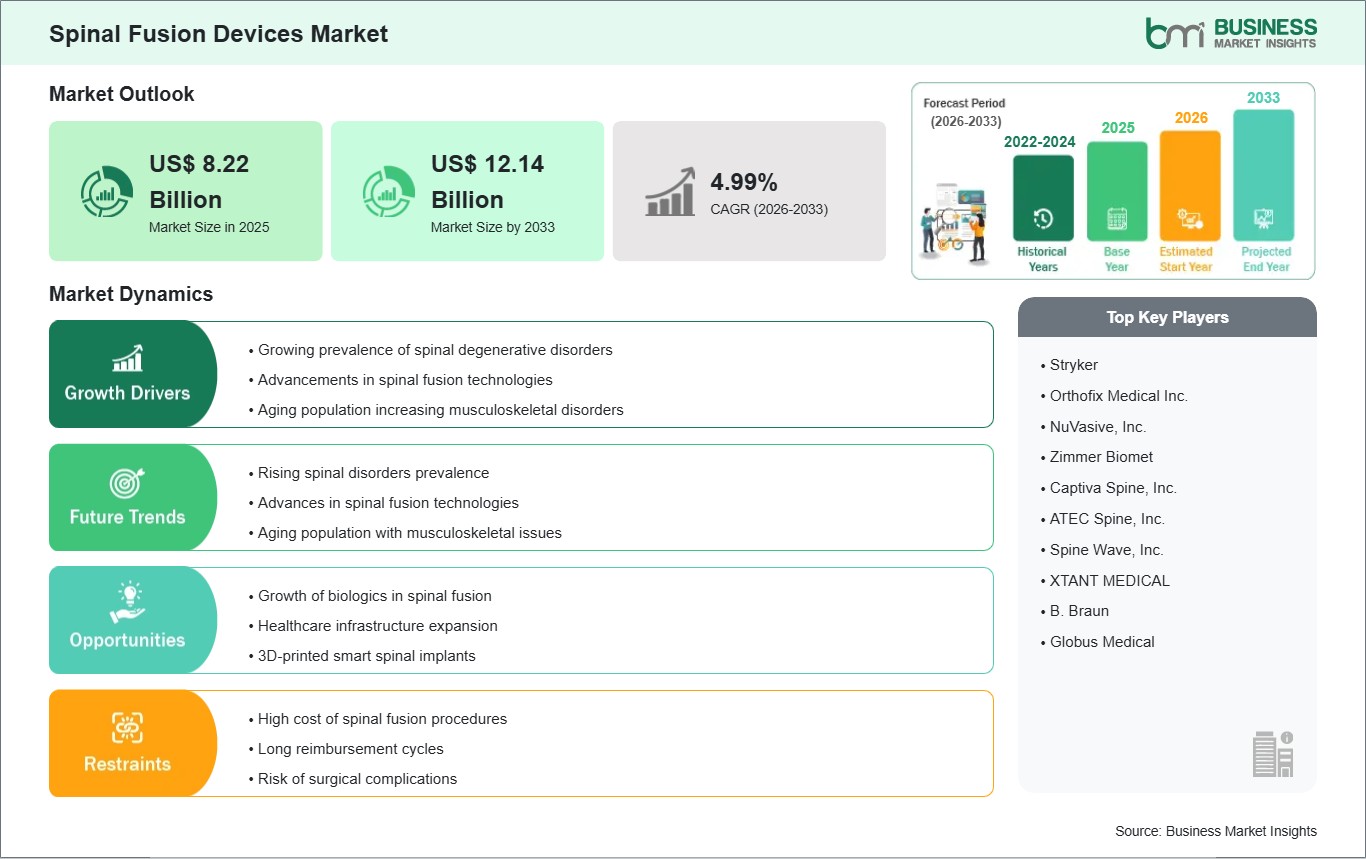

The Spinal Fusion Devices Market size is expected to reach US$ 12.14 Billion by 2033 from US$ 8.22 Billion in 2025. The market is estimated to record a CAGR of 4.99% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Spinal fusion surgery depends on spinal fusion devices which serve as medical implants and surgical instruments for enhancing vertebral stability through their capability to connect multiple vertebrae that treat spinal conditions which include degenerative disc disease and spinal stenosis and trauma and deformities. The system uses interbody cages together with pedicle screws and plates and rods and biologic bone graft substitutes which enable bone healing through their ability to create mechanical stability. Patients who fail to respond to noninvasive treatments still choose spinal fusion as their preferred surgical method which doctors now perform with safer techniques and modern materials that enhance treatment results while shortening patient recovery durations.

The spinal fusion devices market maintains its global growth momentum because of three main factors which include an increasing aging population and a growing number of spinal disorders and technological innovations which include 3D-printed implants and navigation-assisted systems and robotic surgery platforms. North America currently leads demand distribution because its advanced healthcare facilities enable doctors to perform procedures at high rates while Asia-Pacific markets show better growth potential because of their healthcare system improvements and increased public knowledge about medical procedures.

The industry faces multiple growth challenges because of three main factors which include high expenses for devices and procedures and strict rules from regulators and worries about surgical results and inconsistent operating procedures. The market will experience its next growth phase through outcome-based procurement processes and customized patient implant solutions and digital planning tools which enable better accuracy and successful long-term fusion results.

Key segments that contributed to the derivation of the spinal fusion devices market analysis are product, disease¸ surgery, and end user.

By product, the spinal fusion devices market is categorized into thoracolumbar devices, cervical fixation devices, interbody fusion devices. The thoracolumbar devices segment held the largest share of the market in 2025.

By disease, the market is segmented into degenerative disc, complex deformity, trauma and fractures, other diseases. The degenerative disc segment held the largest share of the market in 2025.

By surgery, the market is categorized into open spine surgery, minimally invasive spine surgery. The minimally invasive spine surgery segment held the largest share of the market in 2025.

By end user, the spinal fusion devices market is bifurcated into hospitals, outpatient facilities. The hospitals segment dominated the market in 2025.

Spinal Fusion Devices Market Drivers and Opportunities:

Rising Prevalence of Degenerative Spinal Disorders and Aging Population

Degenerative spinal conditions which affect aging populations around the world are the main factor that drives spinal fusion devices market growth. Degenerative disc disease and spinal stenosis with their related disorders now account for more than half of all spinal cases which need surgical treatment because over 540 million people worldwide suffer from lower back pain and disc degeneration constitutes a major cause of their condition. The clinical need for treatment exists because between 22 and 27 percent of adults who reach 60 years of age will experience spinal instability which requires fusion or fixation procedures. The growth of surgical volumes results from the rising popularity of navigation-assisted spine surgery together with minimally invasive techniques. Technological enhancementssuch as 3D-printed patient-specific cages and robotic systems that improve placement accuracy (e.g., reported ~97 percent accuracy in screw placement)strengthen clinical adoption and drive device utilization across hospitals and surgical centers. The demand for spinal fusion devices will continue to grow throughout developed countries and developing nations because of rising demographic and clinical trends.

Technological Innovation and Advanced Materials

The spinal fusion devices market presents its primary opportunity through two main factors which include technological advancements that occur at fast speeds and the development of modern materials and digital surgical instruments. Recent years have seen the introduction of bioactive coatings in spinal implants which obtained approval from regulators because they enhance bone growth and osseointegration for approximately 34 percent of new products which manufacturers introduced to the market. Robotic navigation systems in spine surgery have demonstrated nearly 24 percent improvements in implant placement accuracy, encouraging broader adoption of precision technologies. The implementation of AI-based preoperative planning tools together with innovative regenerative bone grafts which experience growth above 27 percent shows that surgical centers are increasing their ability to provide distinctive clinical services. Device makers and research institutions work together to create new products, which have resulted in 19 new product approvals, that will lead to international market expansion while improving patient outcomes across the globe.

Spinal Fusion Devices Market Size and Share Analysis:

By product, the spinal fusion devices market is categorized into thoracolumbar devices, cervical fixation devices, interbody fusion devices. The thoracolumbar devices segment held the largest share of the market in 2025. The thoracolumbar devices segment leads because disorders of the thoracic and lumbar spine (especially lumbar degenerative diseases and trauma) are more prevalent and constitute the majority of fusion procedures globally. These devices (e.g., pedicle screw systems and rods) provide robust stabilization and correction needed in multi-level and high-load spinal regions, making them the most widely adopted among surgeons.

By disease, the market is segmented into degenerative disc, complex deformity, trauma and fractures, other diseases. The degenerative disc segment held the largest share of the market in 2025. The degenerative disc segment dominates as age-related disc deterioration is the most common cause of chronic back pain and spinal instability worldwide. With aging populations and increasing lifestyle-related spinal degeneration, this indication drives the highest volume of fusion surgeries, leading to greater demand for fusion devices.

By surgery, the market is categorized into open spine surgery, minimally invasive spine surgery. The minimally invasive spine surgery segment held the largest share of the market in 2025. Minimally invasive spine surgery leads due to strong surgeon and patient preference for procedures with smaller incisions, reduced tissue trauma, less pain, shorter hospital stays, and faster recovery. These advantages have increased adoption of MIS approaches and associated devices, outpacing traditional open surgery in many markets.

By end user, the spinal fusion devices market is bifurcated into hospitals, outpatient facilities. The hospitals segment dominated the market in 2025. Hospitals leads because they handle the largest volume of complex spinal fusions requiring advanced infrastructure, multidisciplinary surgical teams, imaging and postoperative care, and they account for the majority of fusion procedures globally.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Stryker

Orthofix Medical Inc.

NuVasive, Inc.

Zimmer Biomet

Captiva Spine, Inc.

ATEC Spine, Inc.

Spine Wave, Inc.

XTANT MEDICAL

B. Braun

Globus Medical

Get more information on this report

Spinal Fusion Devices Market Report Coverage and Deliverables:

The " Spinal Fusion Devices Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Spinal fusion devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Spinal fusion devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Spinal fusion devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the spinal fusion devices market

Detailed company profiles, including SWOT analysis

Spinal Fusion Devices Market Geographic Insights:

The geographical scope of the spinal fusion devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East and Africa, and South and Central America. The spinal fusion devices market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific spinal fusion devices market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific spinal fusion devices market is experiencing robust growth, due to a combination of demographic, economic, and healthcare system factors. The rising aging demographic in Japan, China, and South Korea leads to increased cases of degenerative spinal disorders which include degenerative disc disease and spinal stenosis and this creates greater need for fusion procedures. The combination of rising urbanization and sedentary lifestyles in India and Southeast Asia leads to increased cases of chronic back pain and spinal injuries. The development of healthcare facilities in China and India has resulted in better access to advanced surgical procedures through the establishment of new orthopedic and spine specialty centers in urban and tier-2 locations. The regional governments increase their healthcare financial support while they promote the use of medical technologies which leads hospitals to purchase systems for minimally invasive spine surgery and advanced implant technologies. The expansion of medical tourism in Thailand, India, and Malaysia attracts international patients who want affordable spine surgeries. The global device manufacturers develop distribution networks which they use to partner with regional hospitals and this process increases product accessibility while driving market growth in the area.

Get more information on this report

Spinal Fusion Devices Market Research Report Guidance:

The report includes qualitative and quantitative data in the spinal fusion devices market across product, disease¸ surgery, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the spinal fusion devices market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the spinal fusion devices market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the spinal fusion devices market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover spinal fusion devices market segments by product, disease¸ surgery, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the spinal fusion devices market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Spinal Fusion Devices Market News and Key Development:

The spinal fusion devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the spinal fusion devices market are:

In October 2023, Silony Medical International AG, a growing challenger to "big medtech" in the global spinal fusion market, has completed the acquisition of Centinel Spine's Global Fusion Business. This combines Silony's Verticale posterior screw and rod fusion Platform, its Roccia, and Favo Interbody Fusion (IBF) Systems with the STALIF Technology Platform to create a first in class occiput to sacrum, posterior, lateral, and anterior Spinal Fusion Portfolio for open and minimally invasive spinal fusion cases.

In August 2024, NanoHive Medical, a leader in 3D-printed titanium spinal interbody fusion devices, announced a US$7M Series C Financing to capitalize the company`s rapid growth and a priority on company-building to profitability. The primary use-of-proceeds include: expanding the US commercial organization; expanding the company`s innovative Hive portfolio of Soft Titanium spinal interbody fusion devices by way of product line-extensions, product launches, and “smart” sensor implant delivery research and development, entering select international markets; and expanding strategic partnerships.

Key Sources Referred:

World Health Organization (WHO)Institute for Health Metrics and EvaluationCenters for Disease Control and PreventionUnited Nations Population DivisionOrganisation for Economic Co-operation and Development Health DataWorld Bank Health DataCompany websitesCompany annual reportsCompany investor presentations

The List of Companies - Spinal Fusion Devices Market

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Spinal Fusion Devices Market?

The Spinal Fusion Devices Market is valued at US$ 8.22 Billion in 2025, it is projected to reach US$ 12.14 Billion by 2033.

What is the CAGR for Spinal Fusion Devices Market by (2026 - 2033)?

As per our report Spinal Fusion Devices Market, the market size is valued at US$ 8.22 Billion in 2025, projecting it to reach US$ 12.14 Billion by 2033. This translates to a CAGR of approximately 4.99% during the forecast period.

What segments are covered in this report?

The Spinal Fusion Devices Market report typically cover these key segments-

Disease (Degenerative Disc, Complex Deformity, Trauma and Fractures, Other Diseases)

Surgery (Open Spine Surgery, Minimally Invasive Spine Surgery)

End User (Hospitals, Outpatient Facilities)

What is the historic period, base year, and forecast period taken for Spinal Fusion Devices Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Spinal Fusion Devices Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Spinal Fusion Devices Market?

The Spinal Fusion Devices Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Stryker

Orthofix Medical Inc.

NuVasive, Inc.

Zimmer Biomet

Captiva Spine, Inc.

ATEC Spine, Inc.

Spine Wave, Inc.

XTANT MEDICAL

B. Braun

Globus Medical

Who should buy this report?

The Spinal Fusion Devices Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Spinal Fusion Devices Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Spinal Fusion Devices Market

Get Free Sample For Spinal Fusion Devices Market