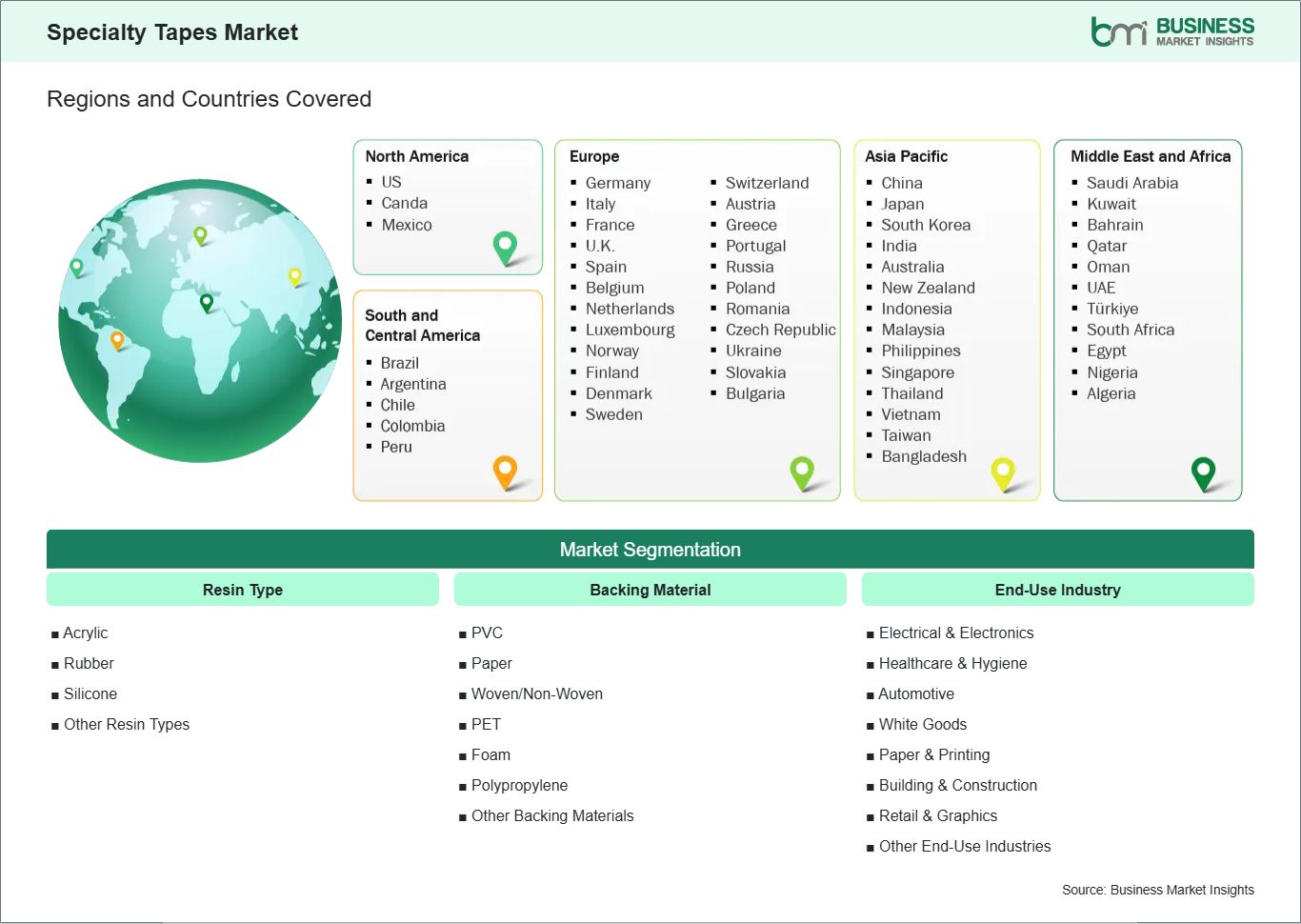

Resin Type (Acrylic, Rubber, Silicone, Other Resin Types)

Backing Material (PVC, Paper, Woven/Non-Woven, PET, Foam, Polypropylene (PP), Other Backing Materials)

End-Use Industry (Electrical & Electronics, Healthcare & Hygiene, Automotive, White Goods, Paper & Printing, Building & Construction, Retail & Graphics, Other End-Use Industries)

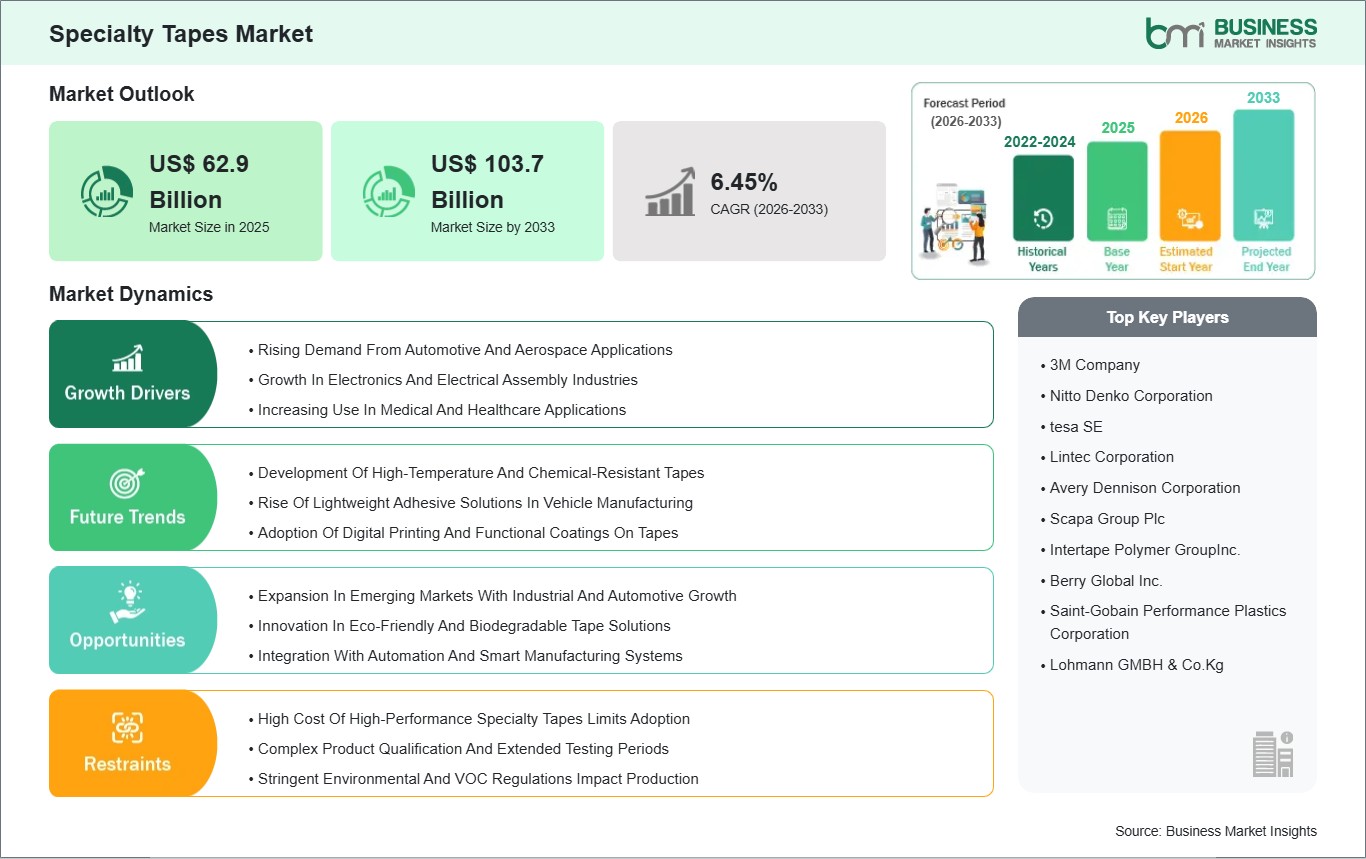

The Specialty Tapes Market size is expected to reach US$ 103.7 billion by 2033 from US$ 62.9 billion in 2025. The market is estimated to record a CAGR of 6.45% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The worldwide market for specialty tapes includes various adhesive tape products that manufacturers designed to meet different bonding needs, sealing requirements, masking needs and insulation needs and protection needs that occur in multiple industrial sectors. Specialty tapes — including acrylic, foam, double‑sided, filament, high‑temperature, and electrically conductive tapes — are designed for high performance under demanding conditions where traditional tapes fall short. The unique material formulations together with the adhesive technologies enable the products to maintain their adhesion on challenging substrates while they withstand extreme environmental conditions and provide their full range of functional properties, which include electrical insulation, impact damping and vibration control and surface protection. The characteristics make them essential for use in sectors which include automotive, aerospace and electronics, electrical, healthcare and industrial manufacturing. The global market experiences its major growth because companies develop new advanced manufacturing and assembly processes, which need strong bonding and sealing solutions. Automotive production uses specialty tapes instead of mechanical fasteners to attach interior trim and exterior trims and NVH (noise, vibration, and harshness) reduction systems, which leads to lighter assemblies and better manufacturing efficiency.

The electronics industry increasingly relies on specialty tapes for flexible circuit bonding, electromagnetic interference shielding, and display protection, which needs high precision and performance because these factors affect product reliability. The renewable energy sectors experience growth in wind and solar power, which leads to increased demand for high-durability tapes that can withstand both outdoor conditions and long-term usage. The market encounters its main restrictions because of strong customer demand, which exists in the market. High-performance specialty tapes cost more than standard pressure-sensitive tapes, which creates difficulties for businesses that need to use their products in applications that require cost control or in emerging markets that need to compete on pricing. The process of selecting specialty tapes requires testing procedures, which consume time during both design testing and production testing stages in manufacturing.

Environmental and regulatory considerations about volatile organic compound (VOC) emissions and end-of-life disposal methods determine both product formulations and customer choices, which make some market segments shift toward different bonding methods. The global specialty tapes market develops through three main factors, which include performance needs from advanced industrial sectors, new adhesive and backing technologies, and the search for lightweight assembly materials that deliver efficient and reliable performance.

Specialty Tapes Market - Strategic Insights:

Get more information on this report

Specialty Tapes Market Segmentation Analysis:

Key segments that contributed to the derivation of the specialty tapes market analysis are resin type, backing material, and end‑use industry.

By resin type, the specialty tapes market is segmented into acrylic, rubber, silicone, other resin types. The acrylic segment dominated the market in 2025.

Based on backing material, the specialty tapes market is categorized into PVC, paper, woven/non‑woven, PET, foam, polypropylene (PP), other backing materials. The woven/non‑woven segment dominated the market in 2025.

In terms of end‑use industry, the specialty tapes market is categorized into electrical & electronics, healthcare & hygiene, automotive, white goods, paper & printing, building & construction, retail & graphics, other end‑use industries. The healthcare & hygiene segment dominated the market in 2025.

Specialty Tapes Market Drivers and Opportunities:

Rising Demand From Automotive And Aerospace Applications

The specialty tapes market is experiencing significant growth driven by rising demand in automotive and aerospace applications worldwide. In the automotive industry, manufacturers are increasingly adopting specialty tapes for interior trim attachment, exterior moldings, and NVH (noise, vibration, and harshness) control solutions, replacing mechanical fasteners and liquid adhesives. These tapes offer lightweight bonding, design flexibility, and consistent performance, aligning with the industry`s broader push toward vehicle weight reduction and fuel efficiency. Leading production hubs in North America, Europe, and Asia Pacific are at the forefront of this trend, integrating double‑sided acrylics, foam tapes, and structural bonding tapes into next‑generation vehicle assemblies. This shift supports automation on assembly lines and enhances production throughput without compromising build quality.

In aerospace, the use of high‑performance specialty tapes has expanded beyond traditional masking and surface protection to structural bonding, insulation, and composite assembly. Airlines and OEMs in the U.S., Europe, and China are deploying advanced tape solutions that withstand extreme temperatures, vibration, and long service cycles. These tapes contribute to overall aircraft performance by reducing weight compared to rivets and welds, simplifying maintenance, and improving fuel efficiency.

Expansion In Emerging Markets With Industrial And Automotive Growth

Emerging markets are playing an increasingly critical role in the global specialty tapes landscape as industrialization and automotive production accelerate across Asia Pacific, Latin America, and parts of the Middle East & Africa. In Asia Pacific, rapid expansion of manufacturing hubs in countries such as India, Vietnam, and Indonesia is creating robust demand for specialty tapes in automotive assembly, consumer electronics, and industrial machinery. Local OEMs and global manufacturers establishing regional operations are specifying high‑performance tapes for bonding, sealing, and protection to enhance product quality while meeting international standards. This regional growth is reinforced by investments in infrastructure and export‑oriented manufacturing facilities that benefit from cost‑competitive production and expanding domestic markets.

In South America, countries like Brazil and Mexico are witnessing incremental uptake of specialty tapes in automotive interiors, packaging, and consumer goods, driven by urbanization and rising disposable incomes. Manufacturers in these regions are exploring advanced tape applications as alternatives to traditional fastening methods to improve assembly efficiency and reduce production costs. Although slower compared to more developed regions, this trend is gaining momentum as local converters and resin suppliers strengthen supply chains and technical support.

Specialty Tapes Market Size and Share Analysis:

The specialty tapes market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within resin type, backing material, and end‑use industry, offering insights into their contribution to overall market performance.

By resin type, the acrylic subsegment dominated the market in 2025, driven by its excellent adhesion, durability, and resistance to temperature and UV, making it ideal for industrial and healthcare applications.

Based on backing material, the woven/non‑woven subsegment dominated the market in 2025, driven by superior strength, flexibility, and conformability, which are critical for medical, hygiene, and industrial tapes.

In terms of end‑use industry, the healthcare & hygiene subsegment dominated the market in 2025, driven by growing demand for medical tapes, wound care products, and hygiene applications requiring reliable, high-performance adhesives.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

3M Company

Nitto Denko Corporation

tesa SE

Lintec Corporation

Avery Dennison Corporation

Scapa Group Plc

Intertape Polymer GroupInc.

Berry Global Inc.

Saint-Gobain Performance Plastics Corporation

Lohmann GMBH & Co.Kg

Get more information on this report

Specialty Tapes Market Report Coverage and Deliverables:

The "Specialty Tapes Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Specialty Tapes Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Specialty Tapes Market trends, as well as drivers, restraints, and opportunities

Specialty Tapes Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Specialty Tapes Market

Detailed company profiles, including SWOT analysis

Specialty Tapes Market Geographic Insights:

The geographical scope of the Specialty Tapes Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The Specialty Tapes Market demonstrates multiple regional markets, which identify North America as the primary market because the region possesses a strong industrial base, advanced manufacturing infrastructure, and high rates of technological adhesive solution adoption. The automotive industry and aerospace sector, electronics field and medical industry in the United States and Canada use specialty tapes for their essential high-performance bonding, sealing and surface protection needs. Automotive manufacturers in Michigan, Ohio and the southern U.S. use foam, acrylic and double-sided tapes as alternatives to mechanical fasteners because these materials enable them to achieve vehicle weight reduction and production efficiency improvements. The electronics and electrical OEMs in Silicon Valley and the Pacific Northwest use tapes for flexible circuits, EMI/RFI shielding and precise assembly operations.

Europe represents a mature market driven by high demand in automotive manufacturing, renewable energy installations, and industrial machinery sectors. Germany, France, and Italy use advanced specialty tape applications for electric vehicle assembly, wind turbine construction and industrial automation systems, which create energy-efficient, durable and safe products.

The Asia Pacific region experiences rapid industrialization while automotive and electronics manufacturing and infrastructure development advance in China Japan India, and South Korea. Specialty tapes are becoming more popular in packaging, electronics assembly and medical uses because domestic production expands and international tape manufacturers enter these markets.

The Middle East and Africa market is growing because construction and energy, oil, and gas sectors need tapes which provide sealing, insulation and protection in extreme weather conditions.

The South and Central American market shows slow development because the automotive, packaging, and industrial manufacturing industries in Brazil, Mexico and Argentina drive economic growth. The implementation process faces two main obstacles because organizations show price sensitivity, and there are existing problems with the necessary infrastructure.

North America proves to be the main market because the region has its own special market drivers and challenges, which create opportunities for growth through established industrial systems and widespread use of advanced specialty tapes and strong partnerships between production companies and their end users.

Get more information on this report

Specialty Tapes Market Research Report Guidance:

The report includes qualitative and quantitative data in the Specialty Tapes Market across resin type, backing material, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Specialty Tapes Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Specialty Tapes Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Specialty Tapes Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Specialty Tapes Market segments by resin type, backing material, end‑use industry and geography across North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Specialty Tapes Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Specialty Tapes Market News and Key Development:

The Specialty Tapes Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the specialty tapes market are:

In June 2024, Avery Dennison Performance Tapes announced that it had introduced new pressure‑sensitive adhesive tape solutions specifically engineered for electric vehicle (EV) battery cell wrapping applications, addressing electrical insulation and corrosion resistance challenges in advanced EV battery pack designs. These tapes enhance safety and performance in electric vehicle manufacturing.

In April 2025, Avery Dennison Performance Tapes announced that it had launched a new Flashing and Seaming Portfolio of high‑performance pressure‑sensitive tapes designed for building envelope applications such as window systems, roofing, and wall insulation, providing enhanced air and water resistance for construction industries worldwide. This new product line expands the company`s specialty tape offerings into infrastructure and energy‑efficient construction markets.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerThe LancetInternational Bar AssociationInternational Trade Administration

The List of Companies - Specialty Tapes Market

3M Company

Nitto Denko Corporation

tesa SE

Lintec Corporation

Avery Dennison Corporation

Scapa Group Plc

Intertape Polymer GroupInc.

Berry Global Inc.

Saint-Gobain Performance Plastics Corporation

Lohmann GMBH & Co.Kg

Frequently Asked Questions

How big is the Specialty Tapes Market?

The Specialty Tapes Market is valued at US$ 62.9 Billion in 2025, it is projected to reach US$ 103.7 Billion by 2033.

What is the CAGR for Specialty Tapes Market by (2026 - 2033)?

As per our report Specialty Tapes Market, the market size is valued at US$ 62.9 Billion in 2025, projecting it to reach US$ 103.7 Billion by 2033. This translates to a CAGR of approximately 6.45% during the forecast period.

What segments are covered in this report?

The Specialty Tapes Market report typically cover these key segments-

Resin Type (Acrylic, Rubber, Silicone, Other Resin Types)

Backing Material (PVC, Paper, Woven/Non-Woven, PET, Foam, Polypropylene (PP), Other Backing Materials)

End-Use Industry (Electrical & Electronics, Healthcare & Hygiene, Automotive, White Goods, Paper & Printing, Building & Construction, Retail & Graphics, Other End-Use Industries)

What is the historic period, base year, and forecast period taken for Specialty Tapes Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Specialty Tapes Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Specialty Tapes Market?

The Specialty Tapes Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

3M Company

Nitto Denko Corporation

tesa SE

Lintec Corporation

Avery Dennison Corporation

Scapa Group Plc

Intertape Polymer GroupInc.

Berry Global Inc.

Saint-Gobain Performance Plastics Corporation

Lohmann GMBH & Co.Kg

Who should buy this report?

The Specialty Tapes Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Specialty Tapes Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Specialty Tapes Market

Get Free Sample For Specialty Tapes Market