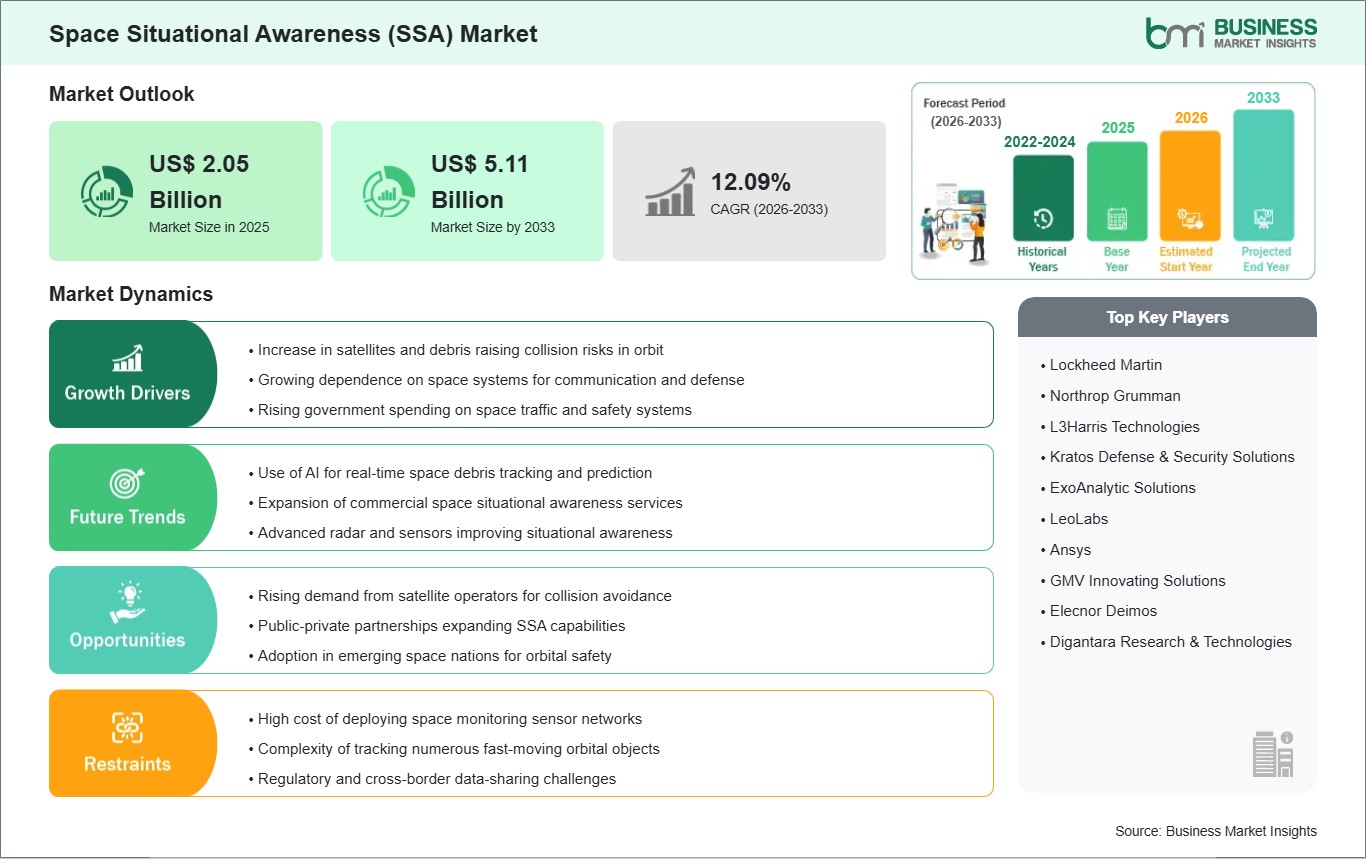

The Space Situational Awareness (SSA) Market size is expected to reach US$ 5.11 billion by 2033 from US$ 2.05 billion in 2025. The market is estimated to record a CAGR of 12.09% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Space Situational Awareness (SSA) is the comprehensive knowledge and characterization of the space environment, encompassing the detection, tracking, and identification of all objects in Earth`s orbit. This includes active and inactive satellites, spent rocket stages, and fragmentation debris. SSA leverages a global network of ground-based radars, optical telescopes, and space-based sensors to predict orbital trajectories, assess collision risks (conjunction analysis), and monitor "space weather" (solar activity) that could disrupt satellite electronics or communication signals. Market expansion is primarily attributed to the explosive growth of Low Earth Orbit (LEO) mega-constellations (e.g., Starlink, Kuiper), a rising volume of lethal non-trackable space debris, and increasing geopolitical tensions driving the need for "Space Domain Awareness" to detect hostile orbital maneuvers.

However, several challenges can restrain market growth: high initial procurement and operational costs for global sensor networks, particularly high-power radars and cryogenic telescopes, can limit the participation of emerging space nations. Stringent regulatory hurdles and the lack of a unified international legal framework for "Space Traffic Management" (STM) create inconsistencies in data sharing and liability. Additionally, the industry faces constraints due to data silos and interoperability gaps, where fragmented information from different national and private catalogs can lead to conflicting collision warnings, complicating the decision-making process for satellite operators.

Despite these hurdles, the market holds immense opportunities in the universal mandate for orbital sustainability and the accelerating deployment of active debris removal (ADR) missions. The expansion of commercial SSA data marketplaces and the development of onboard autonomous collision-avoidance software, allowing satellites to maneuver without human intervention, are expected to create significant opportunities for market growth.

Space Situational Awareness (SSA) Market - Strategic Insights:

Get more information on this report

Space Situational Awareness (SSA) Market Segmentation Analysis:

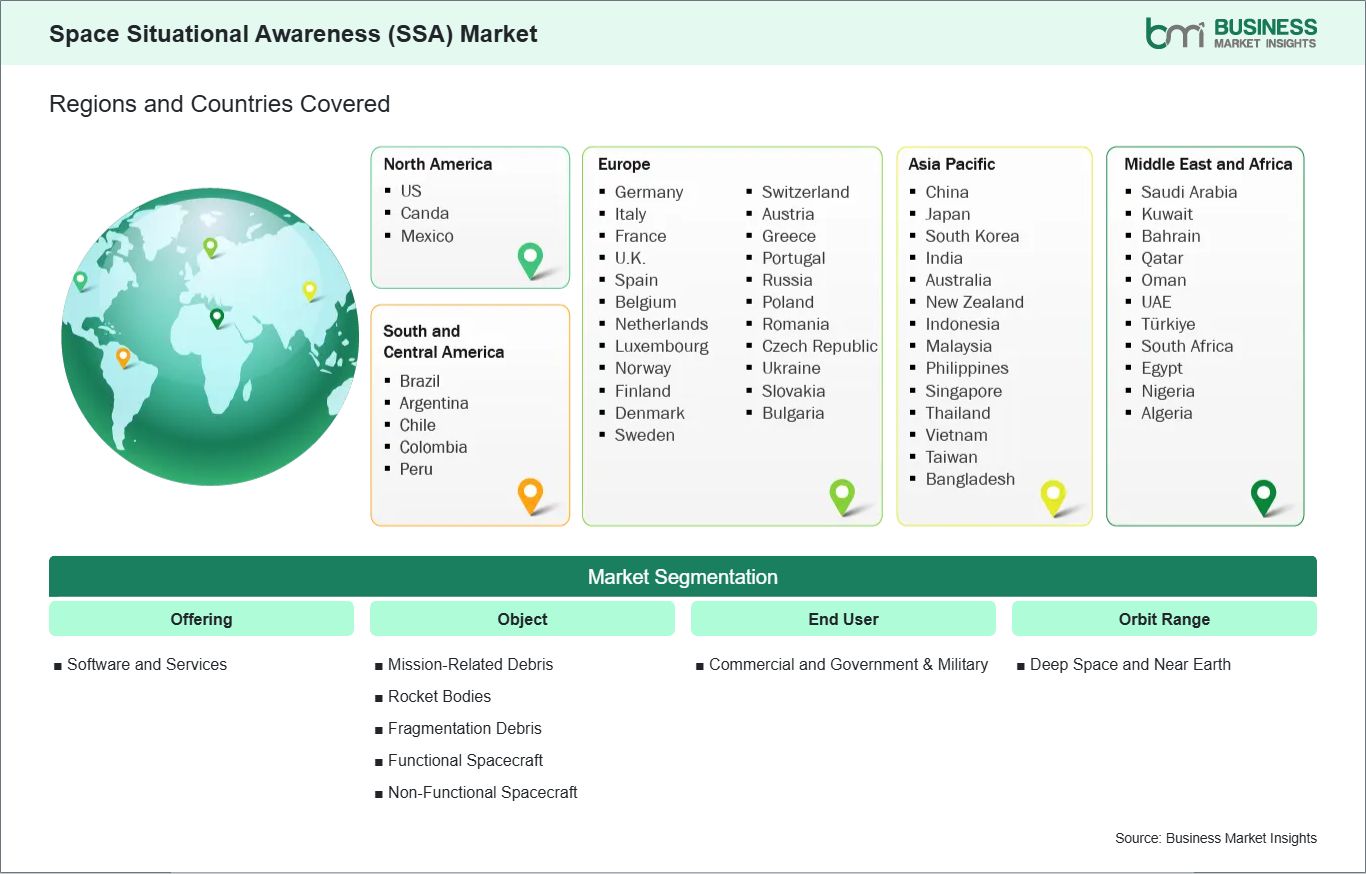

Key segments that contributed to the derivation of the Space Situational Awareness (SSA) market analysis are offering, object, end user, and orbit range.

By Offering, the market is segmented into Software and Services.

By Object, the market is divided into Mission-Related Debris, Rocket Bodies, Fragmentation Debris, Functional Spacecraft, and Non-Functional Spacecraft.

By End User, the market is categorized into Commercial and Government & Military.

By Orbit Range, the market is segmented into Deep Space and Near Earth.

Space Situational Awareness (SSA) Market Drivers and Opportunities:

Advancing Orbital Sustainability and Global Space Traffic Management

The primary driver for the Space Situational Awareness (SSA) Market is the accelerating congestion of Earth's orbits caused by the rapid deployment of mega-constellations and the proliferation of space debris. As of 2026, the launch of thousands of small satellites by commercial entities like SpaceX and Amazon has turned Low Earth Orbit (LEO) into a high-risk environment, necessitating real-time tracking to prevent catastrophic collisions. This momentum is further amplified by the urgent need for Space Traffic Management (STM) as the population of trackable debris exceeds. Governments worldwide are prioritizing SSA as a non-discretionary component of national security, investing heavily in ground-based radars and optical sensors to protect critical assets from both accidental conjunctions and intentional counterspace threats. Furthermore, the rising reliance on space-based services for global telecommunications, navigation, and environmental monitoring ensures that maintaining a transparent and safe orbital environment is no longer just a scientific goal but a vital economic and strategic imperative.

AI-Driven Predictive Analytics and Active Debris Removal

A significant high-value opportunity lies in the convergence of Space Situational Awareness with Artificial Intelligence (AI) and Machine Learning. By integrating AI into SSA software, operators can automate the processing of massive datasets to identify anomalous satellite behaviors and predict potential "collision cascades" with unprecedented accuracy. There is also a major growth frontier in the burgeoning Active Debris Removal (ADR) and In-Orbit Servicing sectors. As international regulations begin to mandate the de-orbiting of non-functional spacecraft, a lucrative market is emerging for "cleanup" missions that utilize tethered nets, robotic arms, and harpoons to remove hazardous debris. Furthermore, the rise of Space-Based SSA sensor networks, deploying dedicated monitoring satellites, presents an opportunity to eliminate the weather and atmospheric limitations of ground-based tracking. Manufacturers who focus on modular, interoperable data platforms that facilitate international data sharing and those pioneering commercial collision-avoidance-as-a-service are positioned to lead the most innovative and high-margin segments of the global space economy.

Space Situational Awareness (SSA) Market Size and Share Analysis:

The Space Situational Awareness (SSA) market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within offering, object, end user, and orbit range, offering insights into their contribution to overall market performance.

Based on offering, the Services subsegment holds the dominant market share. SSA services, including conjunction assessment, collision avoidance, and space weather monitoring, are indispensable for both Government & Military and Commercial sectors to protect high-value assets from orbital hazards. A notable trend in 2026 is the surge in the Software subsegment, which is fueled by the development of intelligent space awareness platforms that provide real-time command and control. This expansion is driven by the "automation of safety," where satellite operators utilize cloud-based software to process massive datasets from global sensor networks, allowing for faster and more accurate maneuver planning without manual intervention.

Space Situational Awareness (SSA) Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Lockheed Martin

Northrop Grumman

L3Harris Technologies

Kratos Defense & Security Solutions

ExoAnalytic Solutions

LeoLabs

Ansys

GMV Innovating Solutions

Elecnor Deimos

Digantara Research & Technologies

Get more information on this report

Space Situational Awareness (SSA) Market Report Coverage and Deliverables:

The "Space Situational Awareness (SSA) Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Space Situational Awareness (SSA) market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Space Situational Awareness (SSA) market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Space Situational Awareness (SSA) market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Space Situational Awareness (SSA) market

Detailed company profiles, including SWOT analysis

Space Situational Awareness (SSA) Market Geographic Insights:

The geographical scope of the Space Situational Awareness (SSA) market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Space Situational Awareness Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. This region is emerging as the fastest-growing market globally. The expansion is primarily fueled by rapid advancements in domestic space programs and the proliferation of satellite constellations that necessitate robust tracking and monitoring systems. China and Japan lead the regional growth, supported by the establishment of advanced optical satellite observation systems and a burgeoning commercial space sector. Furthermore, rising partnerships, such as those between India and the U.S. or Australia and South Korea, aimed at information sharing and joint missions, are accelerating the adoption of SSA technologies across the region.

Growth is further bolstered by a significant shift toward automated collision-avoidance software among satellite operators looking to navigate increasingly congested orbital environments. The integration of artificial intelligence and machine learning into data fusion tasks, alongside the rising demand for real-time threat assessment to protect critical national assets, solidifies Asia-Pacific as a critical hub for innovation and the future scaling of the SSA industry.

Get more information on this report

Space Situational Awareness (SSA) Market Research Report Guidance:

The report includes qualitative and quantitative data in the Space Situational Awareness (SSA) market across offering, object, end user, orbit range, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Space Situational Awareness (SSA) market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Space Situational Awareness (SSA) market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Space Situational Awareness (SSA) market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Space Situational Awareness (SSA) market segments by offering, object, end user, orbit range, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Space Situational Awareness (SSA) market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Space Situational Awareness (SSA) Market News and Key Development:

The Space Situational Awareness (SSA) market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Space Situational Awareness (SSA) market are:

In July 2025, Dragonfly Aerospace successfully demonstrated Non-Earth Imaging (NEI) with its EOSSAT-1 satellite, capturing high-precision lunar images using dual DragonEye imagers. The mission validates advanced satellite attitude control and imaging capabilities, supporting space situational awareness (SSA) by monitoring space assets, tracking debris, and calibrating sensors. This achievement highlights the growing role of small satellites in SSA, space traffic management, and technology validation for lunar and planetary missions.

In August 2024, Slingshot Aerospace acquired Numerica`s Space Domain Awareness division and UK-based Seradata, adding a global optical sensor network and the SpaceTrak database. This strengthens Slingshot`s space situational awareness (SSA) and space traffic management capabilities, expanding its footprint in the US and Europe. The move effectively launches new capabilities and products into the market.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Space Situational Awareness (SSA) Market

Lockheed Martin

Northrop Grumman

L3Harris Technologies

Kratos Defense & Security Solutions

ExoAnalytic Solutions

LeoLabs

Ansys

GMV Innovating Solutions

Elecnor Deimos

Digantara Research & Technologies

Frequently Asked Questions

How big is the Space Situational Awareness (SSA) Market?

The Space Situational Awareness (SSA) Market is valued at US$ 2.05 Billion in 2025, it is projected to reach US$ 5.11 Billion by 2033.

What is the CAGR for Space Situational Awareness (SSA) Market by (2026 - 2033)?

As per our report Space Situational Awareness (SSA) Market, the market size is valued at US$ 2.05 Billion in 2025, projecting it to reach US$ 5.11 Billion by 2033. This translates to a CAGR of approximately 12.09% during the forecast period.

What segments are covered in this report?

The Space Situational Awareness (SSA) Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Space Situational Awareness (SSA) Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Space Situational Awareness (SSA) Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Space Situational Awareness (SSA) Market?

The Space Situational Awareness (SSA) Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin

Northrop Grumman

L3Harris Technologies

Kratos Defense & Security Solutions

ExoAnalytic Solutions

LeoLabs

Ansys

GMV Innovating Solutions

Elecnor Deimos

Digantara Research & Technologies

Who should buy this report?

The Space Situational Awareness (SSA) Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Space Situational Awareness (SSA) Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Space Situational Awareness (SSA) Market

Get Free Sample For Space Situational Awareness (SSA) Market