01

Market Summery

Executive Summary and Global Market Analysis

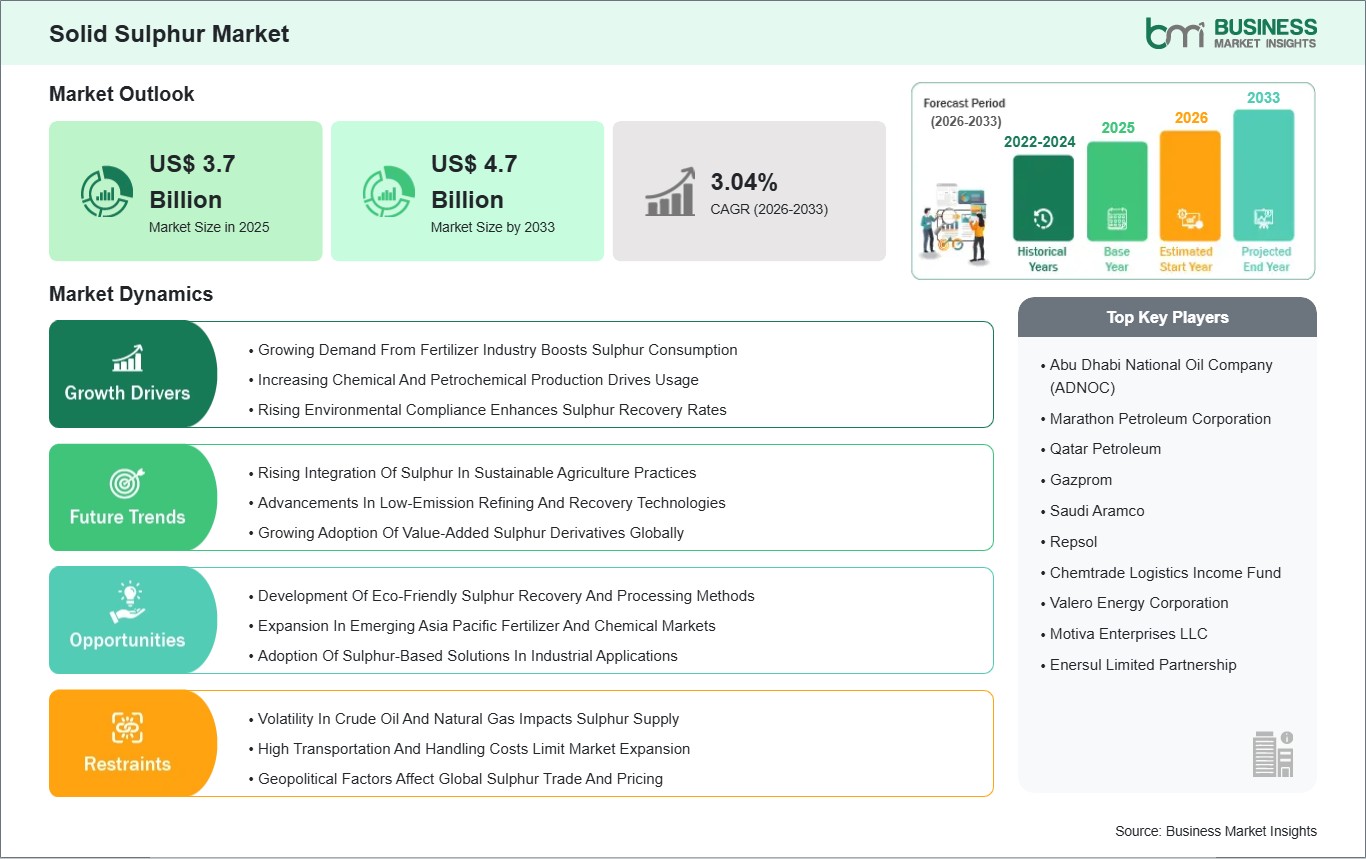

The global solid sulphur market plays a pivotal role across diverse industrial and agricultural ecosystems because it provides essential raw materials for fertilizer production and chemical manufacturing and energy supply chains. The production of sulfuric acid which ranks among the most commonly used industrial chemicals throughout the world relies on solid sulphur which comes from the extraction of elemental sulphur during petroleum refining and natural gas processing. Solid sulphur functions as a crucial element for phosphate fertilizer production and metal processing and mining operations and chemical synthesis because it enables essential activities that maintain global food security and industrial development. Companies now view sulphur recovery and reuse as necessary practices which refineries and gas processing plants should implement to convert waste by-products into valuable business assets because of the rising demand for environmental protection.

Agriculture sustains its persistent demand for sulfate-based fertilizers because phosphate-based fertilizers require sulfur as a vital nutrient which farmers need to grow their crops. Farmers and agribusinesses are placing greater emphasis on balanced nutrient application because they want to use sulfur as a fertilizer component which will enhance soil quality and increase crop production. The chemical industry maintains its high demand for solid sulphur because solid sulphur serves as a primary material for producing sulfuric acid which chemical manufacturers use to create detergents and pharmaceuticals and synthetic fibers. The establishment of efficient sulfur recovery systems has resulted from environmental rules which aim to reduce sulfur emissions from fuels and industrial operations thereby increasing the supply of solid sulfur for use in subsequent processes.

The market encounters important barriers which exist despite these growth driving factors. The production of sulphur experiences direct effects from crude oil and natural gas refining throughput which operates with unpredictable patterns. Geopolitical factors which affect hydrocarbon processing facilities in major oil producing nations result in supply chain disruptions. The existence of different regional regulatory systems together with varying sulphur market prices creates trade obstacles which affect international trade and purchasing decisions. The industrial demand which drives steady growth will remain the foundation of future outlooks. The transformation of sulphur from waste by-product to essential industrial material drives permanent industrial growth.

03

Segment Analysis

Solid Sulphur Market Segmentation

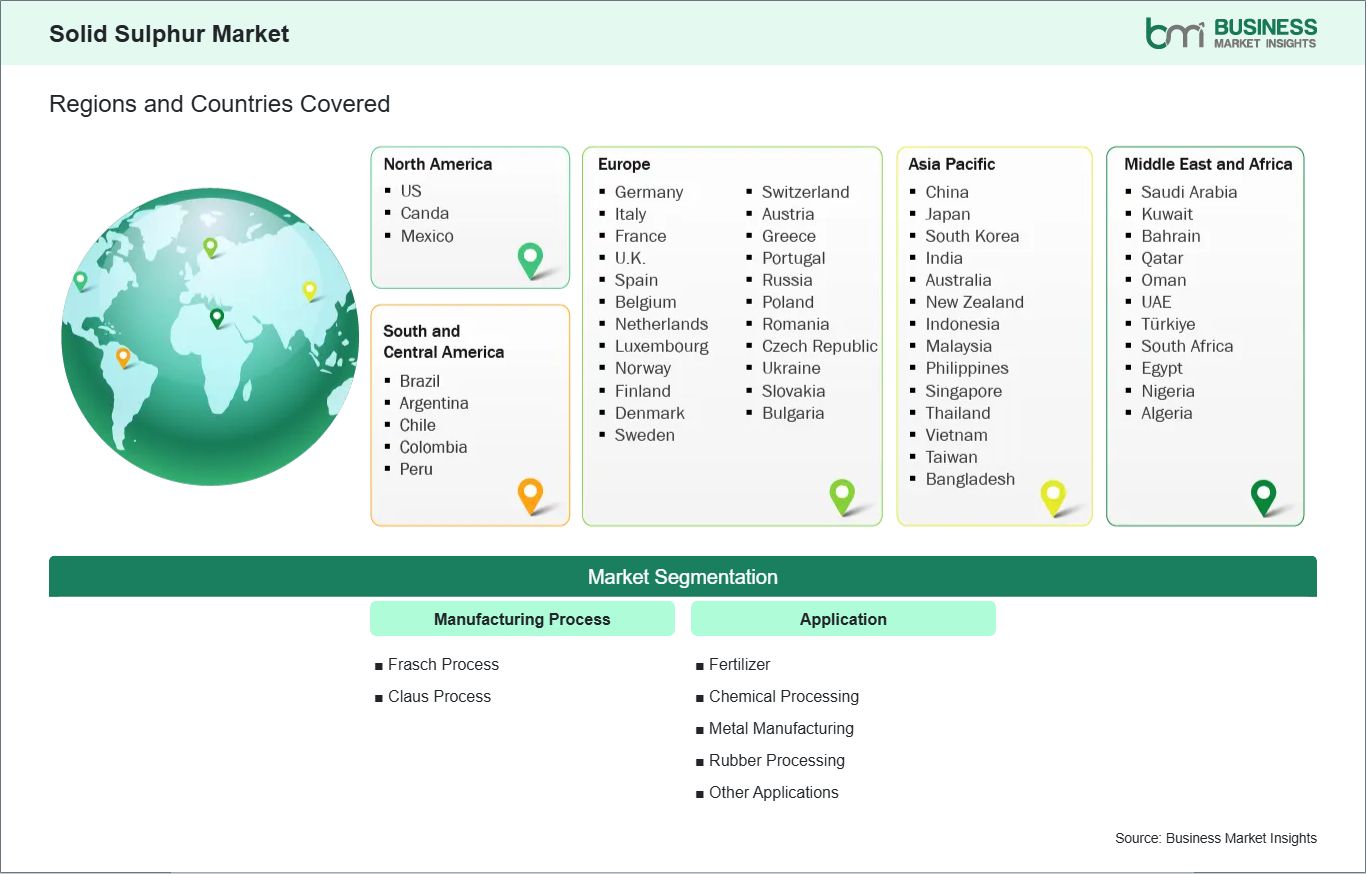

Key segments that contributed to the derivation of the solid sulphur market analysis are manufacturing process and application.

- By manufacturing process, the solid sulphur market is segmented into Frasch Process, Claus Process. The Claus Process segment dominated the market in 2025.

- Based on application, the solid sulphur market is categorized into fertilizer, chemical processing, metal manufacturing, rubber processing, other applications. The fertilizer segment dominated the market in 2025.

04

Market Forces

Solid Sulphur Market Drivers and Opportunities

Growing Demand From Fertilizer Industry Boosts Sulphur Consumption

Global demand for solid sulfur establishes a strong connection to fertilizer sector requirements because sulfur serves as an essential crop nutrient. North American fertilizer manufacturers now utilize sulfur together with phosphate and nitrogen compounds to create products that fulfill the nutritional needs of premium crops while improving agricultural results. Agricultural growth and high-intensity farming methods in Asia Pacific nations such as India and China and Indonesia lead to ongoing usage of sulfur-based fertilizers which help farmers maintain their local crops and grow their international markets. Phosphate fertilizer production, in particular, relies heavily on sulfuric acid, which in turn depends on elemental sulphur as a key feedstock. Manufacturing plants that produce fertilizers on a large scale benefit from accessing solid sulfur, which they obtain through natural gas and petroleum processing operations. Fertilizer companies now create nutrient formulas that include sulfur to meet environmental demands. Sulfur-containing fertilizers improve crop resistance and decrease chemical runoff, which helps establish sustainable agricultural practices.

The fertilizer industry maintains its role as the primary solid sulfur consumer because governments promote nutrient usage efficiency through various programs, which helps sustain global market operations and creates permanent demand for the product.

Development Of Eco-Friendly Sulphur Recovery And Processing Methods

Environmental sustainability has emerged as the main objective which drives research into sustainable recovery methods and processing techniques for the global solid sulphur market. The hydrocarbon refining process requires traditional sulphur recovery methods to consume excessive energy while releasing harmful chemicals which leads refiners to develop better Claus process methods and tail gas treatment systems and technology that reduces emissions. North America and Europe implement strict regulations which promote companies to use environmentally friendly technologies that produce recovered sulfur which complies with both industrial requirements and environmental regulations. The field of conventional recovery methods now operates through the development of both bio-based and catalytic recovery approaches.

The development of low-energy catalytic processes enables more effective sulphur extraction from hydrogen sulfide and other industrial waste products. These methods produce lower carbon emissions and less environmental pollution while generating high-purity sulphur which meets the requirements of sensitive applications that include pharmaceuticals and food-grade chemicals and advanced fertilizers. The market changes through technological innovation and environmental responsibility because sustainable production methods now match the rising worldwide need for sulfur-based products.

05

Size and Share Analysis

Solid Sulphur Market Size and Share Analysis

The solid sulphur market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within manufacturing process and application, offering insights into their contribution to overall market performance.

By manufacturing process, the Claus Process subsegment dominated the market in 2025, driven by its high efficiency and cost-effectiveness in producing large volumes of sulfur from natural gas and petroleum refining.

Based on application, the fertilizer subsegment dominated the market in 2025, driven by strong global demand for sulfur-containing fertilizers to support crop yield and soil nutrient management.

07

Report Coverage

Solid Sulphur Market Report Coverage and Deliverables

The "Solid Sulphur Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Solid Sulphur Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Solid Sulphur Market trends, as well as drivers, restraints, and opportunities

- Solid Sulphur Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Solid Sulphur Market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Solid Sulphur Market Geographic Insights

The geographical scope of the Solid Sulphur Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The global solid sulphur market showcases different regional market characteristics because North America has become the leading region through its developed hydrocarbon refining facilities, gas processing systems, and extensive sulfur recovery operations which control emissions. The United States and Canada depend on recovered sulphur from oil refineries and natural gas plants to provide a dependable feedstock which supports sulfuric acid production and fertilizer manufacturing and chemical applications and solidifies the region's industrial dominance.

The Asia Pacific region functions as a dynamically expanding market because agricultural development and industrial growth and infrastructure projects are expanding across China India and Indonesia. The region experiences high solid sulphur consumption because farmers demand phosphate and nitrogen-based fertilizers while chemical and petrochemical production facilities increase their needs.

Europe sustains continuous demand because its established chemical sector and strong environmental regulations support the production of sulfuric acid and fertilizers which require sulfur, with particular demand from Germany, France, and Eastern European nations that practice sustainable agriculture to meet their regulatory obligations.

The Middle East and Africa market maintains a specialized yet important market position because Saudi Arabia and UAE and South Africa possess major oil and gas processing facilities which produce recovered sulfur that companies use for domestic supply and international sales to fulfill fertilizer and industrial requirements.

The South & Central American region experiences moderate market operations because Brazil, Argentina, and Chile utilize their abundant solid sulphur resources to produce phosphate fertilizers for their expansive agricultural territories while supply chain problems and pricing sensitivity prevent fast expansion of their operations.

The market across different regions develops through the interaction between hydrocarbon extraction activities and agricultural requirements and industrial chemical consumption and changing ecological legal standards while North America maintains its position as the primary region for infrastructure development and technological progress and complete sulphur recovery systems which establish worldwide standards for solid sulphur production and consumption.

10

Industry Activity

Recent Developments

The Solid Sulphur Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the solid sulphur market are:

- In November 2025, Sultech Global Innovation Corp. announced that it had signed a Memorandum of Understanding (MoU) with ADNOC Sour Gas to bring next‑generation micronized elemental sulphur technology to the United Arab Emirates, aiming to establish the UAE`s first commercial micronized sulphur manufacturing facility.

- In January 2023, Shell`s Thiogro sulphur technology was licensed by RNZ International to produce improved sulphur‑enhanced fertilizers for farmers in Canada and globally, highlighting the application of sulphur derivatives in agriculture through a collaboration approach.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Health Organization (WHO) Organisation for Economic Cooperation and Development (OECD) The World Bank Group Worldometer The Lancet International Bar Association International Trade Administration