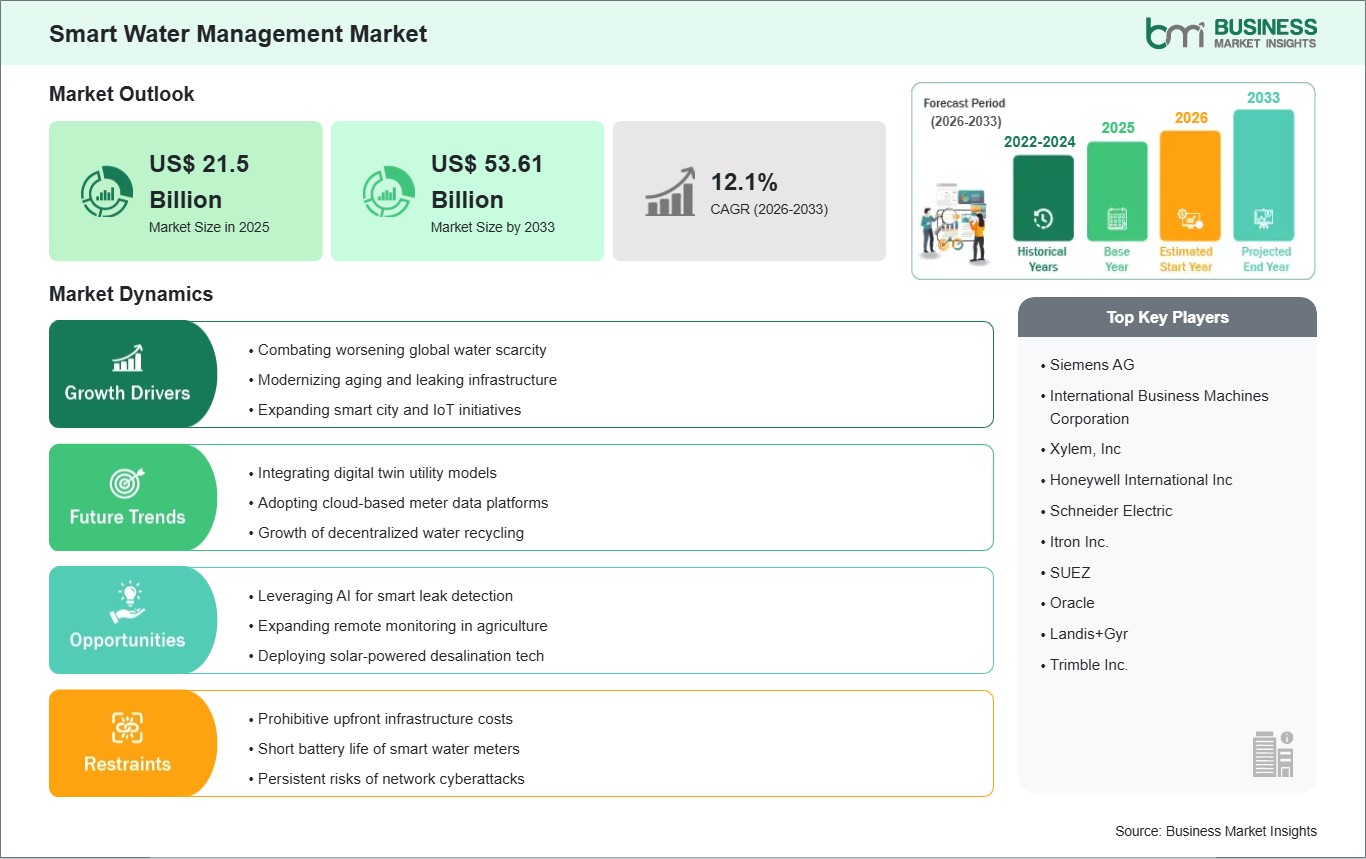

The Smart Water Management Market size is expected to reach US$ 53.61 Billion by 2033 from US$ 21.5 Billion in 2025. The market is estimated to record a CAGR of 12.10% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Smart Water Management plays a critical role in providing the digital intelligence and resilient infrastructure essential for addressing the global water crisis and modernizing aging utility networks. It encompasses key equipment and services: Advanced Metering Infrastructure (AMI), leak detection sensors, smart irrigation controllers, and cloud-based water analytics platforms. Smart water management offers advantages, including the drastic reduction of Non-Revenue Water (NRW) losses, the optimization of energy consumption in pumping stations, and the enhancement of public health through real-time water quality monitoring. The market is being fueled by the massive global pressure of urbanization and population growth, the exponential adoption of IoT and Digital Twin technologies for network simulation, and the urgent need to adapt to climate-induced droughts and flooding. Additionally, the shift toward integrated smart city ecosystems, where water data is synchronized with energy and waste management, is fundamentally enhancing urban resource efficiency and sustainability.

However, several challenges can restrain market growth. High initial capital costs and the complexity of replacing extensive legacy underground piping and deploying large-scale AMI networks can strain municipal budgets. Increasing cybersecurity threats, particularly the vulnerability of interconnected water OT networks to remote hacking and ransomware, present ongoing management and security concerns. The industry also faces persistent data silos between regional utilities and a significant talent gap in managing complex, software-defined hydraulic systems. Despite these challenges, the market offers significant opportunities due to the universal need for climate-resilient infrastructure, the rapid adoption of LPWAN and satellite connectivity for remote asset monitoring, and the growing use of AI and machine learning for predictive pipe-burst modeling and automated demand forecasting. The transition to Water-as-a-Service models, which allow utilities to access advanced technology through subscriptions rather than large upfront investments, is expected to create substantial opportunities for market expansion.

Smart Water Management Market - Strategic Insights:

Get more information on this report

Smart Water Management Market Segmentation Analysis:

Key segments that contributed to the derivation of the Smart Water Management market analysis are offering and end use.

By Offering, the market is segmented into Solutions, Services, and Water Meters.

By End Use, the market is segmented into Residential, Commercial, and Industrial.

Smart Water Management Market Drivers and Opportunities:

Escalating Water Crisis Globally

With a significant portion of treated water lost to leaks, often referred to as Non-Revenue Water (NRW), before it even reaches the consumer, municipalities are under immense pressure to adopt digital oversight. Smart management systems utilize a network of IoT sensors and acoustic leak detectors to provide real-time visibility into pipe integrity and flow dynamics. This transition from reactive repairs to proactive maintenance is fueled by the dual necessity of conserving a finite natural resource and reducing the massive financial losses incurred by inefficient distribution networks in rapidly growing urban centers.

Growing Adoption of Digital Twins and AI-Driven Predictive Analytics

Combining Digital Twin technology with Artificial Intelligence helps in developing fully autonomous, self-healing water networks. Virtual models of city water systems allow utilities to simulate scenarios such as water main breaks or sudden demand spikes during droughts. This approach improves energy efficiency in pumping stations and enables automatic pressure adjustments to prevent pipe damage. As ESG (Environmental, Social, and Governance) reporting requirements become more stringent, there is increasing demand for advanced, cloud-based analytics platforms. These tools enable large water users to monitor consumption, quickly identify issues, and maintain compliance with environmental regulations. Consequently, smart water solutions are becoming essential to the global circular economy.

Smart Water Management Market Size and Share Analysis:

The Smart Water Management market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within offering and end use, offering insights into their contribution to overall market performance.

For instance, the Solutions subsegment represents a significant portion of the market, driven by the integration of advanced technologies such as IoT and AI for real-time monitoring and leak detection. These solutions are widely adopted in the Industrial sector, where water-intensive industries such as food and beverage and chemical processing utilize them to ensure regulatory compliance and optimize operational efficiency. The shift toward predictive maintenance and automated control systems within this segment helps industrial operators reduce non-revenue water loss and energy consumption.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Siemens AG

International Business Machines Corporation

Xylem, Inc

Honeywell International Inc

Schneider Electric

Itron Inc.

SUEZ

Oracle

Landis+Gyr

Trimble Inc.

Get more information on this report

Smart Water Management Market Report Coverage and Deliverables:

The "Smart Water Management Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Smart Water Management market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Smart Water Management market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Smart Water Management market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Smart Water Management market

Detailed company profiles, including SWOT analysis

Smart Water Management Market Geographic Insights:

The geographical scope of the Smart Water Management market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Smart Water Management Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by rapid urbanization and the urgent need to curb Non-Revenue Water (NRW) losses.

Growth is further accelerated by the integration of IoT-enabled sensors and AI-driven analytics for real-time leak detection and water quality monitoring. The rising adoption of Advanced Metering Infrastructure (AMI) and the shift toward sustainable irrigation in agriculture solidify Asia-Pacific as the critical global driver for smart water technology and resource conservation.

Get more information on this report

Smart Water Management Market Research Report Guidance:

The report includes qualitative and quantitative data in the Smart Water Management market across offering, end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Smart Water Management market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Smart Water Management market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Smart Water Management market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Smart Water Management market segments by offering, end use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Smart Water Management market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Smart Water Management Market News and Key Development:

The Smart Water Management market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Smart Water Management market are:

In November 2025, Commission launches dialogues with Member States to ensure sustainable water management across Europe. As part of the implementation of the EU Water Resilience Strategy, the Commission is launching a series of Structured Water Dialogues with Member States, to jointly accelerate action to achieve the environmental objectives of EU water legislation.

In May 2025, Xylem announced that Manchester City Football Club is teaming up with Xylem to bring smart water management to City Football Academy. With the help of Xylem Vue, the Club is capturing and reusing rainwater more efficiently through data and analytics. At City Football Academy, Xylem Vue – a digital water platform – uses connected sensors and smart meters to deliver live insights into how water moves across the training facility. Showing exactly when and where water is being used or lost across the 16.5-pitch campus, the system helps the Club make smarter decisions to optimize irrigation and reduce reliance on public water sources.

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Smart Water Management Market

Siemens AG

International Business Machines Corporation

Xylem, Inc

Honeywell International Inc

Schneider Electric

Itron Inc.

SUEZ

Oracle

Landis+Gyr

Trimble Inc.

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Smart Water Management Market?

The Smart Water Management Market is valued at US$ 21.5 Billion in 2025, it is projected to reach US$ 53.61 Billion by 2033.

What is the CAGR for Smart Water Management Market by (2026 - 2033)?

As per our report Smart Water Management Market, the market size is valued at US$ 21.5 Billion in 2025, projecting it to reach US$ 53.61 Billion by 2033. This translates to a CAGR of approximately 12.10% during the forecast period.

What segments are covered in this report?

The Smart Water Management Market report typically cover these key segments-

Offering (Solutions, Services, Water Meters)

End Use (Residential, Commercial, Industrial)

What is the historic period, base year, and forecast period taken for Smart Water Management Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Smart Water Management Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Smart Water Management Market?

The Smart Water Management Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens AG

International Business Machines Corporation

Xylem, Inc

Honeywell International Inc

Schneider Electric

Itron Inc.

SUEZ

Oracle

Landis+Gyr

Trimble Inc.

Who should buy this report?

The Smart Water Management Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Smart Water Management Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Smart Water Management Market

Get Free Sample For Smart Water Management Market