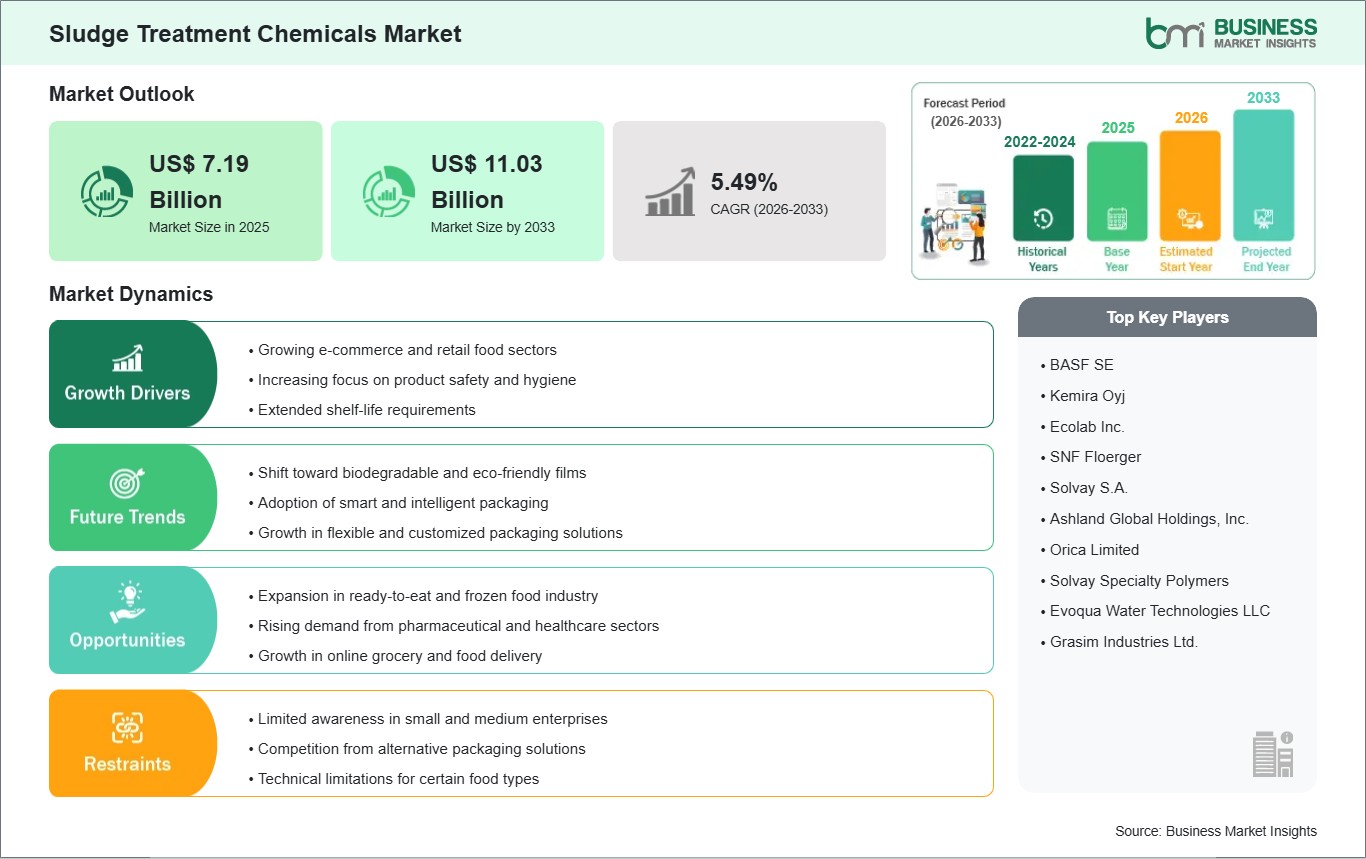

The Sludge Treatment Chemicals Market size is expected to reach US$ 11.03 billion by 2033 from US$ 7.19 billion in 2025. The market is estimated to record a CAGR of 5.49% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global sludge treatment chemicals market is witnessing steady growth, driven by increasing urbanization, industrialization, and stricter environmental regulations regarding wastewater management. Sludge treatment chemicals—including coagulants, flocculants, dewatering agents, and stabilizers—play a critical role in enhancing sludge handling efficiency, reducing volume, and minimizing environmental impact. Rising investments in wastewater treatment plants, coupled with the need to recover valuable by-products such as biogas and fertilizers, are fueling demand for advanced chemical solutions. Industries such as municipal wastewater, pulp and paper, food and beverage, and chemicals are increasingly prioritizing efficient sludge management to reduce operational costs and ensure compliance with environmental standards.

The market is witnessing innovation with multifunctional chemicals that combine coagulation, flocculation, and odor control, improving operational efficiency and reducing chemical consumption. Sustainability trends are encouraging the development of bio-based and low-toxicity formulations, aligning with global environmental policies. However, the market faces challenges, including the high cost of specialty chemicals, variability in sludge characteristics, and strict regulatory approvals for chemical use in different regions. Additionally, handling and storage complexities for certain chemical types can limit adoption in smaller treatment facilities. Despite these restraints, growing environmental awareness, technological advancement, and the drive for resource recovery position the global sludge treatment chemicals market for consistent expansion.

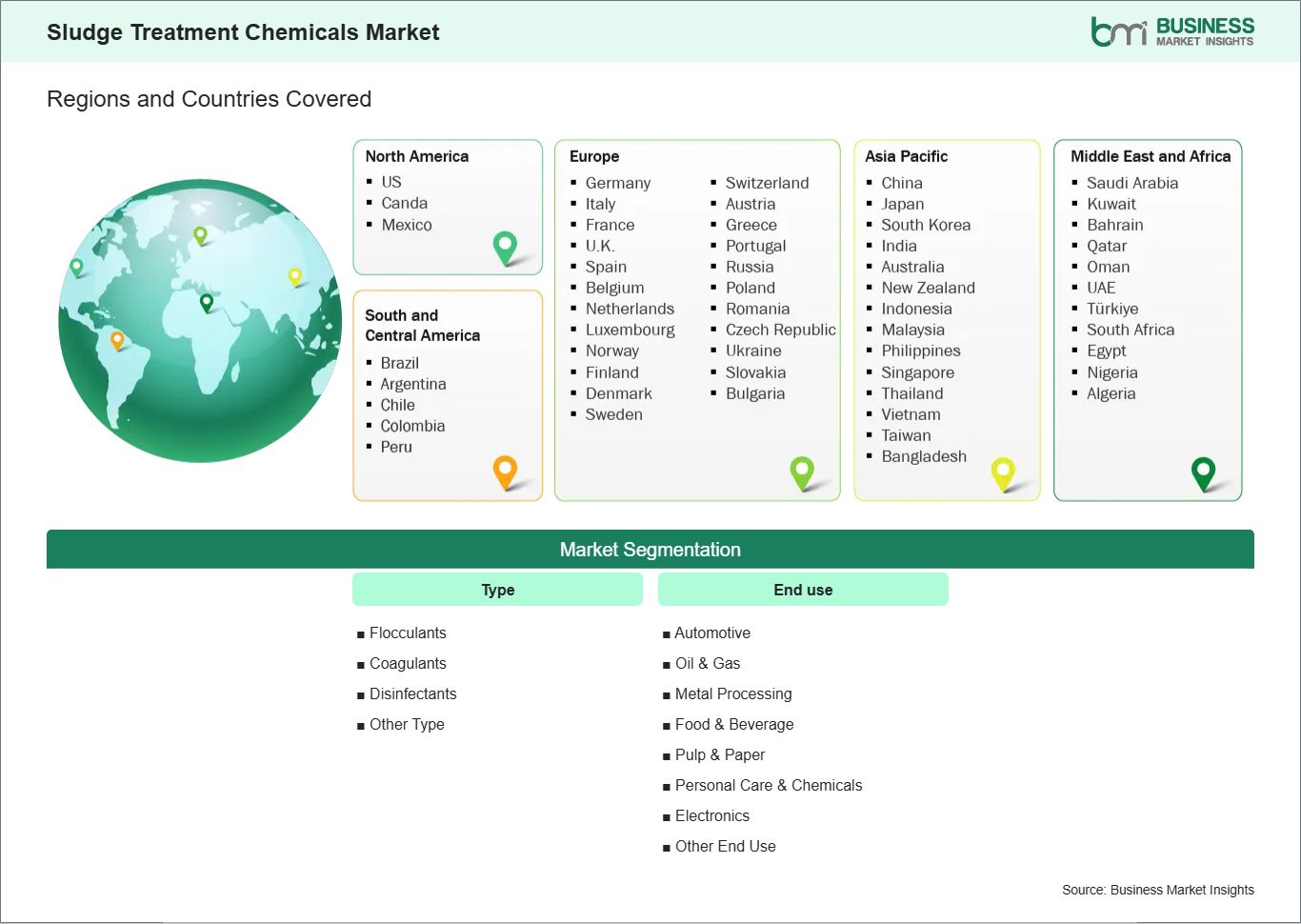

Key segments that contributed to the derivation of the sludge treatment chemicals market analysis are type and end use.

By type, the sludge treatment chemicals market is segmented into flocculants, coagulants, disinfectants, and other type. The flocculants subsegment dominated the market in 2025.

Based on end use, the sludge treatment chemicals market is classified into automotive, oil & gas, metal processing, food & beverage, pulp & paper, personal care & chemicals, electronics, other end use. The oil & gas subsegment dominated the market in 2025.

Sludge Treatment Chemicals Market Drivers and Opportunities:

Technological Advancements in Packaging Machinery

Improvements in packaging machinery in Western Europe are significantly changing the profile of wastewater streams and creating a greater need for specific chemicals to treat the sludges produced during treatment of these wastewaters. New packaging machinery in Germany, France, and the Netherlands now operates at ultrahigh speeds and includes washing and rinsing stages in the process. This has created a wastewater stream with high concentrations of solids, lubricating materials, and leftover packaging materials such as starch and adhesives. To deal with these increased demands before they enter the public treatment systems, food and consumer product manufacturers are looking to highly active coagulants and flocculants to quickly combine finely divided solids in these difficult-to-treat wastewater streams.

In the industrial centers of Germany, including Bavaria and Baden-Württemberg, the move to servo-drive, automated packaging machines has led to a decrease in human interaction but an increase in rinse water volumes, thereby creating a situation of high sludge generation. To address these issues, wastewater treatment plants in the region are increasingly turning to specialized polymeric conditioners to improve dewaterability, thereby decreasing drying costs. In the French dairy and beverage industry, including those in the Lyon and Paris areas, bio-enzyme blends are being utilized to improve the degradation of residues from cleaning-in-place operations associated with high-speed filling equipment.

In addition, the Benelux region is witnessing the adoption of innovations in packaging machinery, including sensors and automated dosing systems, which are designed to provide an effective dosing system of sludge treatment chemicals in line with changing turbidity and conductivity patterns in the wastewater stream. As Western European manufacturers continue to drive the adoption of smarter, faster equipment to support sustainability and productivity objectives, sludge treatment chemicals are being innovated to match the changing wastewater landscape in the region.

Expansion in Ready‑To‑Eat and Frozen Food Industry

The growth of the ready-to-eat (RTE) and frozen food production sector in Western Europe is one major factor driving the sludge treatment chemical market. The increasing urban population, changing eating patterns, and desire for convenience foods have fueled production in France, Spain, and the UK, where massive production facilities operate around the clock, manufacturing RTE products and frozen meals. These facilities have high-fat, protein, and starch concentrations in their wastewater, especially after blanching, cooling, and IQF treatment. The treatment plants use specific sludge treatment chemicals, including grease-specific coagulants and polymeric flocculants, to treat such high-strength wastewater.

In the French food processing centers in Lille and Nantes, the rising production levels of RTE salads, marinated proteins, and frozen bakery products have resulted in an increase in the cost of handling sludge. To address this issue, operators have turned to multi-stage conditioning chemicals to pre-treat the varying levels of influent. This has reduced the need to frequently desludge the wastewater treatment plants. Similarly, in the Valencia and Barcelona regions of Spain, frozen seafood processing centers have turned to enzymatic sludge breakers to address the seasonal peaks in wastewater treatment plant influent due to export cycles.

In the UK, the increasing number of frozen meal brands, especially those being promoted through retail and internet campaigns, is also having an impact on wastewater treatment. Operators in North West England and Scotland have turned to acid-base balancing agents to address the pH level fluctuations due to intermittent production peaks. With the rising levels of RTE and frozen food production, the need for high-performance sludge treatment chemicals to address the varying levels of influent will continue to rise.

Sludge Treatment Chemicals Market Size and Share Analysis:

The sludge treatment chemicals market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type and end use, highlighting their respective contributions to overall market performance.

By type, the flocculant subsegment dominated the Sludge treatment chemicals market in 2025 because because they are essential in nearly every sludge treatment process sthey help particles aggregate so water can be separated efficiently. Across industries like wastewater, industrial effluents, and municipal treatment, flocculants reduce processing time and improve dewatering outcomes.

Based on end use, the oil & gas subsegment dominated the sludge treatment chemicals market in 2025 because because operations produce large volumes of oily sludges and wastewater that require extensive chemical treatment before disposal or reuse. Drilling, refining, and pipeline maintenance generate persistent waste streams that must be conditioned, dewatered, and stabilized.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Kemira Oyj

Ecolab Inc.

SNF Floerger

Solvay S.A.

Ashland Global Holdings, Inc.

Orica Limited

Solvay Specialty Polymers

Evoqua Water Technologies LLC

Grasim Industries Ltd.

Get more information on this report

Sludge Treatment Chemicals Market Report Coverage and Deliverables:

The "Sludge Treatment Chemicals Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Sludge treatment chemicals market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Sludge treatment chemicals market trends, as well as drivers, restraints, and opportunities

Sludge treatment chemicals market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Sludge treatment chemicals market

Detailed company profiles, including SWOT analysis

The geographical scope of the Sludge treatment chemicals market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Sludge treatment chemicals market in North America is expected to grow during the forecast period.

Geographically, the global sludge treatment chemicals market is dominated by North America, considering its developed wastewater management infrastructure, regulatory framework, and industrial base. The United States, in particular, plays a vital role in contributing to regional demand, considering its focus on developing and upgrading its wastewater management and industrial effluent management practices. For instance, the United States Environmental Protection Agency has implemented stricter regulations concerning wastewater disposal, pollutant removal, and nutrient recovery, thereby encouraging the use of superior quality chemicals for coagulation, flocculation, and dewatering processes.

Canada also plays a vital role in contributing to regional demand, considering its investments in developing sustainable wastewater management and industrial effluent management practices. The dominance of the North American market can also be attributed to technological innovation, considering the development and use of tailored chemicals for treating different types and compositions of sludge, dewatering processes, and minimizing chemical consumption.

The market also focuses on sustainable practices, such as using biodegradable and low-toxicity chemicals, to comply with stricter environmental regulations, thereby ensuring a sustainable environment. Thus, the dominance of the North American market can be attributed to its regulatory framework, industrial practices, and focus on sustainability, thereby playing a vital role in developing and adoption of sludge treatment chemical solutions globally.

Get more information on this report

Sludge Treatment Chemicals Market Research Report Guidance:

The report includes qualitative and quantitative data in the sludge treatment chemicals market across type, end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Sludge treatment chemicals market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Sludge treatment chemicals market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Sludge treatment chemicals market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the Sludge treatment chemicals market segments by type, end use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 10 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Sludge treatment chemicals market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Sludge Treatment Chemicals Market News and Key Development:

The sludge treatment chemicals market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the sludge treatment chemicals market are:

In November 2022, Kemira Oyj announced that it had expanded its production and blending capacity for sludge conditioning and dewatering chemicals at its facility in Poland, enabling faster delivery and stronger technical support for municipal and industrial wastewater treatment customers across Eastern Europe.

In June 2024, Ecolab Inc. announced a new partnership with a leading wastewater services provider in Romania to supply advanced polymer‑based sludge treatment chemicals and on‑site optimization services aimed at improving plant efficiency and reducing disposal costs for regional industrial clients.

In February 2025, SNF Group announced that it had opened a dedicated sales and technical support hub in Hungary focused on its latest generation of sludge flocculants and coagulants, with targeted engagement across Eastern European municipal wastewater utilities and industrial processors.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA)European Chemicals Agency (ECHA)American Chemistry Council (ACC)European Chemical Industry Council (Cefic)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Sludge Treatment Chemicals Market

BASF SE

Kemira Oyj

Ecolab Inc.

SNF Floerger

Solvay S.A.

Ashland Global Holdings, Inc.

Orica Limited

Solvay Specialty Polymers

Evoqua Water Technologies LLC

Grasim Industries Ltd.

Frequently Asked Questions

How big is the Sludge Treatment Chemicals Market?

The Sludge Treatment Chemicals Market is valued at US$ 7.19 Billion in 2025, it is projected to reach US$ 11.03 Billion by 2033.

What is the CAGR for Sludge Treatment Chemicals Market by (2026 - 2033)?

As per our report Sludge Treatment Chemicals Market, the market size is valued at US$ 7.19 Billion in 2025, projecting it to reach US$ 11.03 Billion by 2033. This translates to a CAGR of approximately 5.49% during the forecast period.

What segments are covered in this report?

The Sludge Treatment Chemicals Market report typically cover these key segments-

Type (Flocculants, Coagulants, Disinfectants, Other Type)

End use (Automotive, Oil & Gas, Metal Processing, Food & Beverage, Pulp & Paper, Personal Care & Chemicals, Electronics, Other End Use)

What is the historic period, base year, and forecast period taken for Sludge Treatment Chemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Sludge Treatment Chemicals Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Sludge Treatment Chemicals Market?

The Sludge Treatment Chemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Kemira Oyj

Ecolab Inc.

SNF Floerger

Solvay S.A.

Ashland Global Holdings, Inc.

Orica Limited

Solvay Specialty Polymers

Evoqua Water Technologies LLC

Grasim Industries Ltd.

Who should buy this report?

The Sludge Treatment Chemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Sludge Treatment Chemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Sludge Treatment Chemicals Market

Get Free Sample For Sludge Treatment Chemicals Market