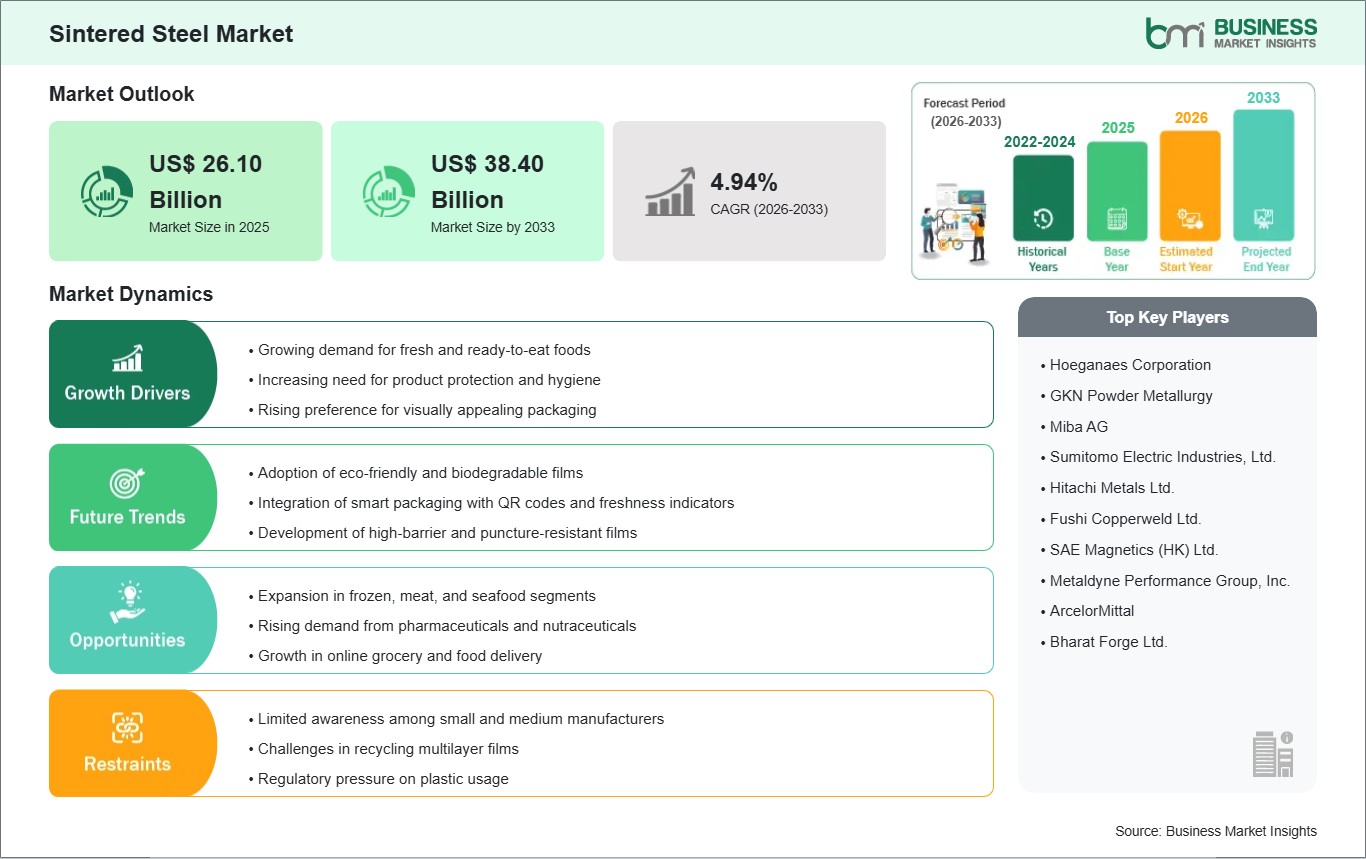

The Sintered Steel Market size is expected to reach US$ 38.4 billion by 2033 from US$ 26.1 billion in 2025. The market is estimated to record a CAGR of 4.94% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global market for sintered steels is experiencing a major transformation due to the increased demand for cost-effective products with high performance in various industries like automotive, industrial machinery, and aerospace. Sintered steels, manufactured using powder metallurgy technology, exhibit dimensional accuracy, efficient material utilization, and enhanced mechanical properties, making them suitable for various applications like gears, bearings, structural components, and engine components. The market is fueled by the global drive for lightweight, strong, and efficient products, especially in automotive and industrial machinery industries where weight reduction without compromising strength is critical.

With technological advancements, such as alloy development, sintering, and hybrid technologies, there has been an increasing possibility of developing sintered steel products with better wear resistance, fatigue strength, and corrosion protection. Environmental factors, including reduced waste and energy consumption, also contribute to increasing product demand. However, there are some factors that might act as barriers to the development of this product. These factors include high capital costs associated with powder metallurgy, production complexities, and difficulties in manufacturing large products. Fluctuating raw material prices will be one more factor affecting pricing strategy. Despite all these barriers, the product has been gaining popularity, thanks to advancements in material science, industrial automation, and increasing product use in critical applications.

Sintered Steel Market - Strategic Insights:

Get more information on this report

Sintered Steel Market Segmentation Analysis:

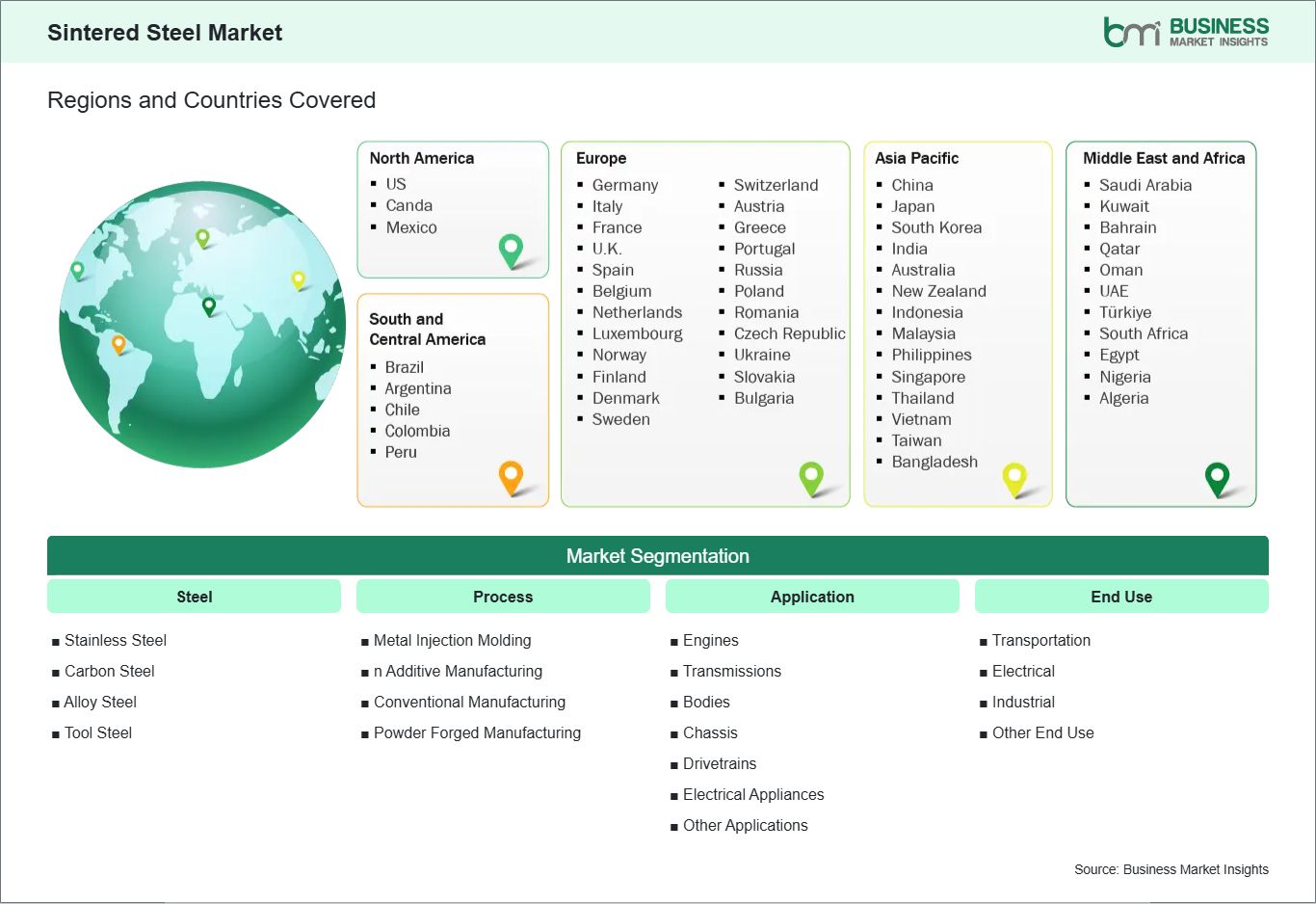

Key segments that contributed to the derivation of the sintered steel market analysis are steel, process, application, and end use.

By steel the sintered steel market is segmented into stainless steel, carbon steel, alloy steel, and tool steel. The alloy steel subsegment dominated the market in 2025.

Based on process, the sintered steel market is classified into additive manufacturing, conventional manufacturing, and powder forged manufacturing. The conventional manufacturing subsegment dominated the market in 2025.

On a basis of application, the sintered steel market is classified into engines, transmissions, bodies, chassis, drivetrains, electrical appliances, and others application. The transmission subsegment dominated the market in 2025.

In terms of end use, the sintered steel market is classified into transportation, electrical, industrial, and other end use. The transportation subsegment dominated the market in 2025.

Sintered Steel Market Drivers and Opportunities:

Growing Demand For Fresh And Ready-To-Eat Foods

Emerging urban and semi-urban markets across Western Europe are providing new opportunities for sintered steel manufacturers. As population centers in cities like Lisbon, Milan, and Lyon expand, there is rising investment in automated manufacturing and infrastructure, which requires durable metal components. Sintered steel, known for its wear resistance and strength-to-weight ratio, is increasingly used in compact industrial machinery, precision engineering, and transportation systems in these growing urban hubs. In Italy’s Lombardy region, small and medium-sized factories are modernizing equipment for local food, automotive, and packaging industries, driving incremental demand for sintered steel parts such as powder metallurgy gears, bushings, and bearings.

In Spain, semi-urban processing clusters near Valencia and Zaragoza are upgrading machinery in food and beverage production lines to meet rising domestic and European export demand. Sintered steel components are favored due to their ability to reduce assembly costs, improve energy efficiency in motors, and extend service life under continuous operation. Manufacturers report that integrating sintered steel has lowered machine downtime and maintenance frequency, making production more resilient and competitive.

Additionally, the expansion of cold-chain logistics across Western Europe has indirectly increased demand for sintered steel. Machines handling packaging, sealing, and labeling in refrigerated environments require components that can withstand temperature variations and moisture exposure. As the fresh and ready-to-eat food market grows, manufacturers are expected to prioritize machinery longevity and operational reliability, supporting continuous adoption of sintered steel components throughout the region’s food processing sector.

Emerging Urban And Semi-Urban Markets

Emerging urban and semi-urban markets across Western Europe are providing new opportunities for sintered steel manufacturers. As population centers in cities like Lisbon, Milan, and Lyon expand, there is rising investment in automated manufacturing and infrastructure, which requires durable metal components. Sintered steel, known for its wear resistance and strength-to-weight ratio, is increasingly used in compact industrial machinery, precision engineering, and transportation systems in these growing urban hubs. In Italy’s Lombardy region, small and medium-sized factories are modernizing equipment for local food, automotive, and packaging industries, driving incremental demand for sintered steel parts such as powder metallurgy gears, bushings, and bearings.

In Spain, semi-urban processing clusters near Valencia and Zaragoza are upgrading machinery in food and beverage production lines to meet rising domestic and European export demand. Sintered steel components are favored due to their ability to reduce assembly costs, improve energy efficiency in motors, and extend service life under continuous operation. Manufacturers report that integrating sintered steel has lowered machine downtime and maintenance frequency, making production more resilient and competitive.

Furthermore, the expansion of urban logistics networks and automation in semi-urban industrial zones is contributing to demand for high-precision sintered steel components in conveyor systems, robotic arms, and handling equipment. Countries like Belgium and France are deploying automated warehouse and distribution systems for groceries and fresh products, where sintered steel is essential for reliable performance under continuous mechanical stress. Overall, as Western Europe’s urban and semi-urban markets continue to grow, sintered steel is expected to see sustained demand across multiple industrial applications beyond traditional manufacturing hubs.

Sintered Steel Market Size and Share Analysis:

The sintered steel market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within steel, process, application, and end use highlighting their respective contributions to overall market performance.

By steel, the alloy steel subsegment dominated the Sintered steel market in 2025 because they offer the best combination of strength, toughness, and wear resistance once sintered and heat‑treated. Their alloying elements (like nickel, molybdenum, chromium) allow engineers to tailor mechanical properties for demanding parts without excessive machining.

Based on process, the conventional manufacturing subsegment dominated the sintered steel market in 2025 because it balances high throughput, low cost per part, and consistent quality. Most industrial users choose this method over more specialized routes because it’s proven, easily scalable, and suitable for large runs of complex shapes.

On a basis of application, the glass manufacturing subsegment dominated the sintered steel market in 2025 because hey contain a high number of precision, load‑bearing sintered components like gears, synchronizers, and shift forks. The performance requirements for torque transmission and wear resistance make sintered steel an efficient choice versus machined forged parts, especially in modern automatic and dual‑clutch transmissions where compact, tightly toleranced parts are essential.

In terms of end use, the transportation subsegment dominated the sintered steel market in 2025 due to the sheer volume of components used in engines, drivetrains, and transmissions. Sintered steel’s ability to deliver precise geometry with minimal post‑machining makes it ideal for cost‑sensitive, high‑volume vehicle production. Growth in electric and hybrid vehicles also supports this dominance, as more transmission and motor components are adapted to powder metallurgy.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Hoeganaes Corporation

GKN Powder Metallurgy

Miba AG

Sumitomo Electric Industries, Ltd.

Hitachi Metals Ltd.

Fushi Copperweld Ltd.

SAE Magnetics (HK) Ltd.

Metaldyne Performance Group, Inc.

ArcelorMittal

Bharat Forge Ltd.

Get more information on this report

Sintered Steel Market Report Coverage and Deliverables:

The "Sintered steel market Size And Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Sintered steel market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Sintered steel market trends, as well as drivers, restraints, and opportunities

Sintered steel market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Sintered steel market

Detailed company profiles, including SWOT analysis

Sintered Steel Market Geographic Insights:

The geographical scope of the Sintered steel market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Sintered steel market in North America is expected to grow during the forecast period.

North America is the leader in the global sintered steel market, and this is mainly because of the advanced manufacturing facilities, the automotive and industrial industries, and the emphasis on innovation and technology. The region is also home to major automotive and industrial companies, and they need high-quality, lightweight, and durable components, and sintered steel is the best solution for them, especially for gears, bearings, and engine components. The United States and Canada are the major players in the global market, and they are the pioneers in the production of advanced sintered steel alloys, especially through the powder metallurgy method, and the region is also embracing the concept of automation and smart manufacturing, and this is helping the production of high-precision and high-volume sintered steel components.

In addition, the region is also focused on sustainable and energy-efficient technologies, and industries are also shifting to sintered steel because the production process is energy-efficient and less wastage of raw materials compared to steel components. Although the region is facing challenges, especially because the production cost is high and the complexity is also an issue, the region is still the leader in the global market because of the advanced R&D facilities and the strong industrial demand.

Get more information on this report

Sintered Steel Market Research Report Guidance:

The report includes qualitative and quantitative data in the sintered steel market steel, process, application, end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Sintered steel market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Sintered steel market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Sintered steel market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover the Sintered steel market segments by steel, process, application, end use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 12 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Sintered steel market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Sintered Steel Market News and Key Development:

The sintered steel market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the sintered steel market are:

In October 2022, GKN Powder Metallurgy announced that it had expanded its sintered steel components production capacity at its facility in Poland, aiming to better serve automotive and industrial customers in Eastern Europe with high‑precision gears and structural parts.

In April 2024, BASF Forward AM (additive manufacturing division) announced a collaboration with a major Czech OEM to develop advanced sintered steel materials and powder metallurgy solutions for lightweight automotive and machinery applications, with pilot production expected later in 2024.

In September 2025, Metal Powder Industries (MPI) announced the opening of a new regional distribution and technical support center in Hungary, focused on supplying sintered steel powders and related metallurgical services to manufacturers across Eastern Europe, along with localized training programs for material engineers.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)S. Geological Survey (USGS)Environmental Protection Agency (EPA)European Chemicals Agency (ECHA)American Chemistry Council (ACC)European Chemical Industry Council (Cefic)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Sintered Steel Market

Hoeganaes Corporation

GKN Powder Metallurgy

Miba AG

Sumitomo Electric Industries, Ltd.

Hitachi Metals Ltd.

Fushi Copperweld Ltd.

SAE Magnetics (HK) Ltd.

Metaldyne Performance Group, Inc.

ArcelorMittal

Bharat Forge Ltd.

Frequently Asked Questions

How big is the Sintered Steel Market?

The Sintered Steel Market is valued at US$ 26.10 Billion in 2025, it is projected to reach US$ 38.40 Billion by 2033.

What is the CAGR for Sintered Steel Market by (2026 - 2033)?

As per our report Sintered Steel Market, the market size is valued at US$ 26.10 Billion in 2025, projecting it to reach US$ 38.40 Billion by 2033. This translates to a CAGR of approximately 4.94% during the forecast period.

What segments are covered in this report?

The Sintered Steel Market report typically cover these key segments-

Application (Engines, Transmissions, Bodies, Chassis, Drivetrains, Electrical Appliances, Other Applications)

End Use (Transportation, Electrical, Industrial, Other End Use)

What is the historic period, base year, and forecast period taken for Sintered Steel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Sintered Steel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Sintered Steel Market?

The Sintered Steel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Hoeganaes Corporation

GKN Powder Metallurgy

Miba AG

Sumitomo Electric Industries, Ltd.

Hitachi Metals Ltd.

Fushi Copperweld Ltd.

SAE Magnetics (HK) Ltd.

Metaldyne Performance Group, Inc.

ArcelorMittal

Bharat Forge Ltd.

Who should buy this report?

The Sintered Steel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Sintered Steel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Sintered Steel Market

Get Free Sample For Sintered Steel Market