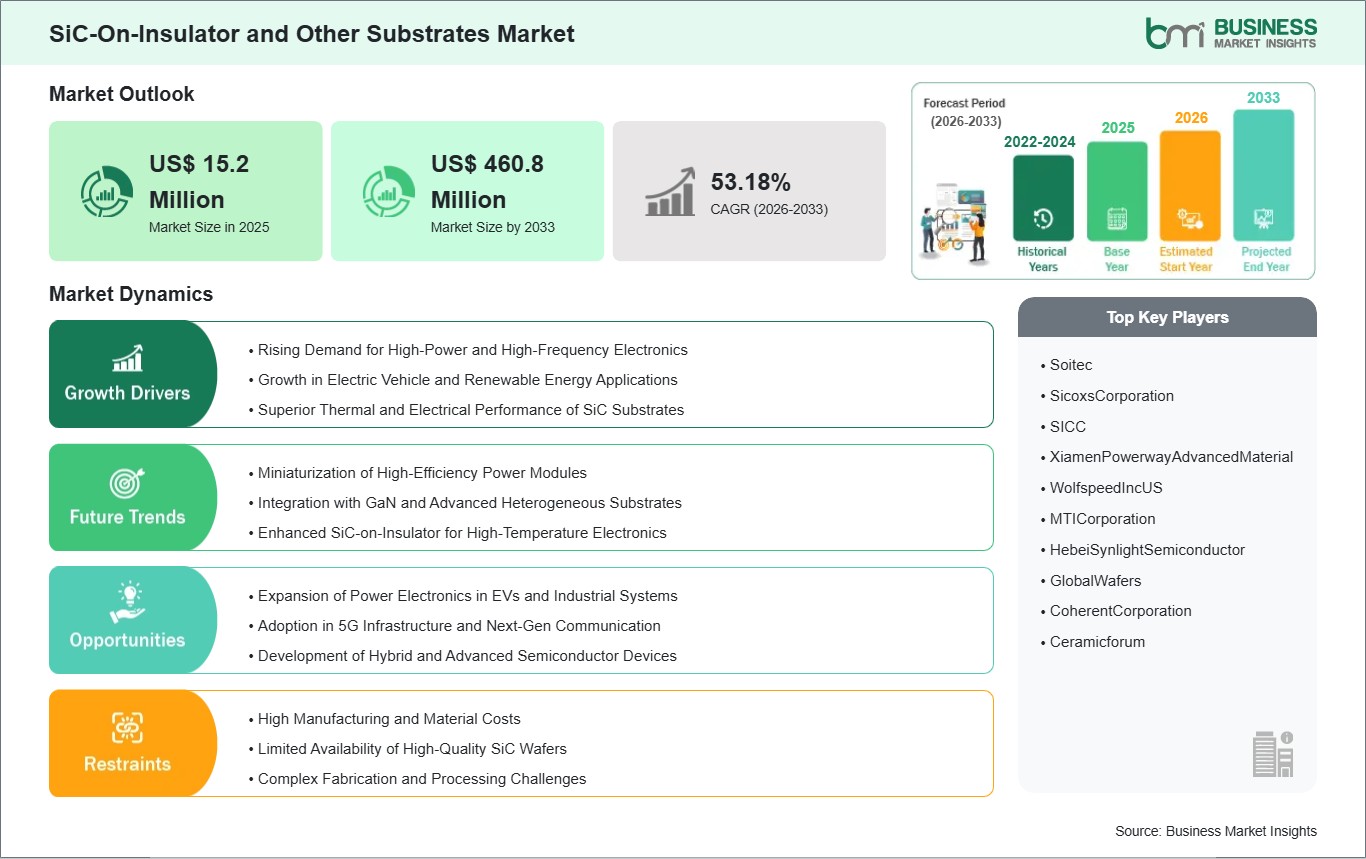

The SiC-On-Insulator and Other Substrates Market size is expected to reach US$ 460.8 million by 2033 from US$ 15.2 million in 2025. The market is estimated to record a CAGR of 53.18% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global market for SiC-On-Insulator (SiCOI) and other advanced semiconductor substrates is growing as demand rises for high-performance, energy-efficient electronics. SiCOI and similar materials are being used more often in power electronics, RF devices, and high-frequency uses because they let heat move away more easily, work with higher voltages, and waste less power than regular silicon substrates. The move toward electrification in cars, including electric and hybrid vehicles, and the growth of renewable energy are increasing interest in substrates that can handle high temperatures and tough conditions. The telecommunications and aerospace industries also need substrates that support fast, high-frequency signal processing and remain reliable in harsh environments. SiC-based substrates help devices perform better in power conversion, energy storage, and advanced semiconductors. However, the market still struggles with the high cost of producing SiC wafers and the challenges of large-scale processing. The limited supply of large-diameter wafers and the need for specialized manufacturing methods can slow down adoption, especially where cost is a concern.

SiC-On-Insulator and Other Substrates Market - Strategic Insights:

Get more information on this report

SiC-On-Insulator and Other Substrates Market Segmentation Analysis:

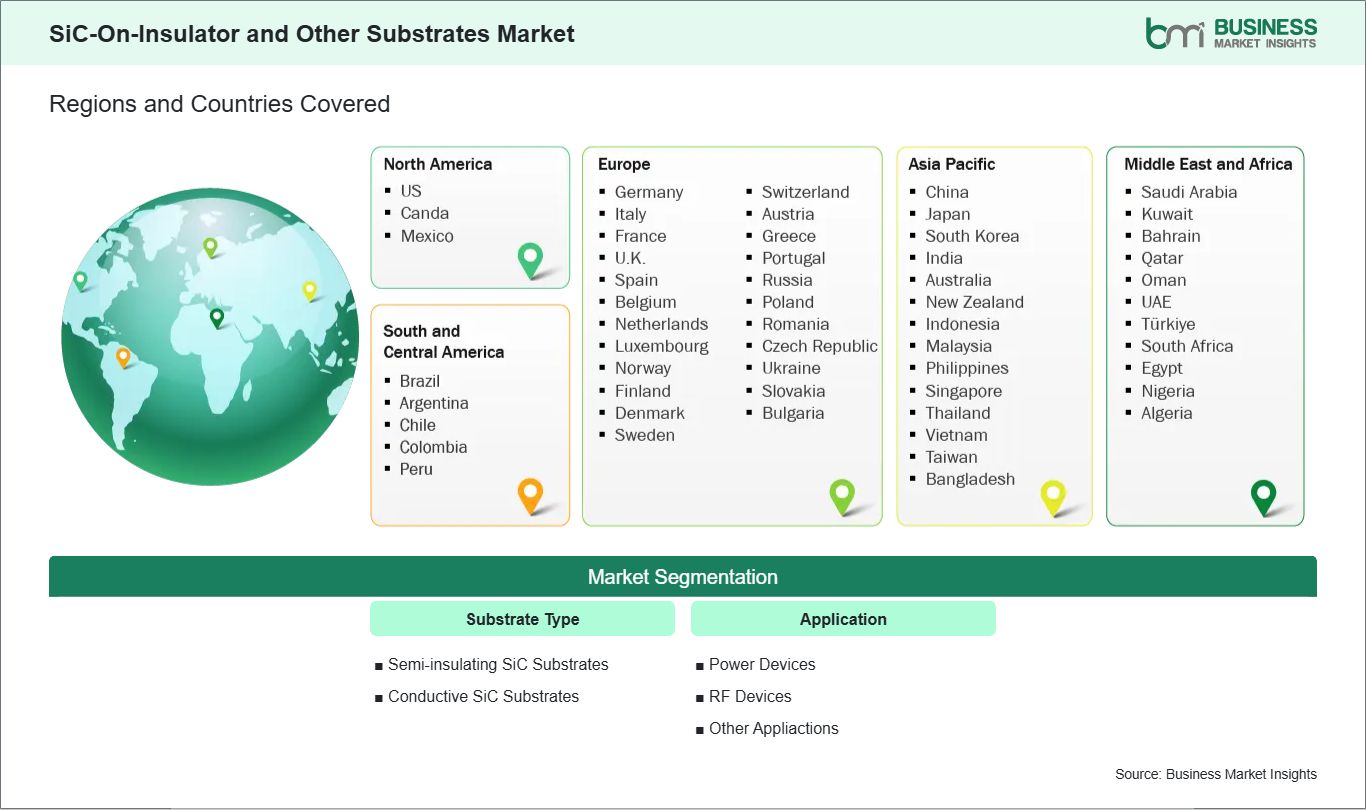

Key segments that contributed to the derivation of the sic-on-insulator and other substrates market analysis are substrate type and application.

By substrate type, the SiC-On-Insulator and Other Substrates market is segmented into semi-insulating sic substrates and conductive sic substrates. The conductive sic substrates segment dominated the market in 2025.

Based on application, the SiC-On-Insulator and Other Substrates market is classified into power devices, RF devices, and other applications. The power devices segment dominated the market in 2025.

SiC-On-Insulator and Other Substrates Market Drivers and Opportunities:

Rising Demand for High-Power and High-Frequency Electronics

As electronics continue to advance, there is growing interest in new substrate technologies like silicon carbide-on-insulator (SiC-OI) and other specialized materials. Today’s devices run at higher power and switch faster, which puts more pressure on thermal management and electrical efficiency. Standard silicon substrates have some limitations, but SiC-OI provides higher breakdown voltage, faster switching, and better heat management. Because of these benefits, SiC-OI works well in high-frequency uses such as RF amplifiers, telecom systems, and new power conversion equipment.

As telecommunications networks are upgraded around the world, there is a growing need for substrates that can support high frequencies. In places like North America and East Asia, new mobile networks and early 6G projects need components that can manage more data and lower delays. SiC‑OI and similar substrates offer the stability and thermal performance needed to keep signals clear, even when conditions are tough. This makes advanced substrates essential for today’s communication technologies.

Outside of telecom, industries like aerospace and defense are also driving growth in the market for high-power, high-frequency substrates. These materials are used in radar, electronic warfare systems, and high-speed signal processors, all of which need to perform reliably in challenging environments. In the United States and European Union, ongoing investment in defense technology is leading manufacturers to choose SiC-based substrates to meet high standards for reliability and efficiency.

Expansion of Power Electronics in EVs and Industrial Systems

The growth of electric vehicles (EVs) is intensifying the need for efficient, durable power electronics, creating new opportunities for advanced substrates. Inverters, onboard chargers, and power conversion modules all require materials capable of managing high voltages and temperatures while ensuring efficient switching. SiC‑OI and other high-performance substrates are increasingly being used to improve energy efficiency, reduce component size and weight, and extend battery life. In rapidly growing EV markets such as China and the European Union, automakers are prioritizing these materials to enhance vehicle performance and reliability.

Industrial power applications are also fueling substrate demand. Renewable energy inverters, industrial motor drives, and smart grid components all operate under high-power conditions, where energy losses must be minimized and thermal management is critical. Regions investing heavily in renewable infrastructure, including Scandinavia and Australia, are seeing wider adoption of SiC‑based and other advanced substrates in these applications. This trend reflects a broader global shift toward electrification and energy-efficient industrial systems, extending substrate demand beyond consumer electronics.

Collaboration between substrate manufacturers and system developers is helping tailor solutions for regional needs. For example, in India, modernizing industrial facilities with energy-efficient motor drives has highlighted the value of advanced substrates in lowering operational costs and improving equipment lifespan. Globally, such partnerships are enabling optimized production and region-specific solutions that meet local performance and regulatory requirements. As the electrification of transportation and industrial systems continues, SiC‑OI and other high-performance substrates are expected to remain a key component in efficient, reliable power electronics.

SiC-On-Insulator and Other Substrates Market Size and Share Analysis:

The sic-on-insulator and other substrates market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within substrate type and application, highlighting their respective contributions to overall market performance.

By substrate type, the conductive SiC substrates segment dominated the Silicon-on-Insulator (SOI) and other substrates market in 2025. This is driven by the growing demand for high-performance substrates that offer superior thermal conductivity, high breakdown voltage, and enhanced efficiency in electronic devices. Conductive SiC substrates are critical for power electronics and high-frequency applications, making them a key revenue driver for manufacturers and ensuring consistent adoption across industries requiring reliable, high-performance semiconductor components.

Based on application, the power devices segment dominated the market in 2025. The leadership of power device applications is attributed to the increasing use of SOI and other advanced substrates in power conversion, energy-efficient electronics, and electric vehicle systems. Their ability to reduce energy loss, handle high voltages, and improve overall device performance makes these substrates highly preferred by manufacturers for developing next-generation power electronics and industrial solutions.

SiC-On-Insulator and Other Substrates Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Soitec

SicoxsCorporation

SICC

XiamenPowerwayAdvancedMaterial

WolfspeedIncUS

MTICorporation

HebeiSynlightSemiconductor

GlobalWafers

CoherentCorporation

Ceramicforum

Get more information on this report

SiC-On-Insulator and Other Substrates Market Report Coverage and Deliverables:

The "SiC-On-Insulator and Other Substrates Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

SiC-On-Insulator and Other Substrates market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

SiC-On-Insulator and Other Substrates market trends, as well as drivers, restraints, and opportunities

SiC-On-Insulator and Other Substrates market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the SiC-On-Insulator and Other Substrates market

Detailed company profiles, including SWOT analysis

SiC-On-Insulator and Other Substrates Market Geographic Insights:

The geographical scope of the SiC-On-Insulator and Other Substrates market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The SiC-On-Insulator and Other Substrates market in North America is expected to grow during the forecast period.

North America dominates the SiC-On-Insulator and other substrate market due to its strong technological infrastructure, early adoption of advanced semiconductor materials, and concentration of high-tech industries. The United States serves as the primary hub, driven by a robust presence of semiconductor manufacturers, research institutions, and technology start-ups focused on next-generation electronics and power devices. Key sectors such as electric vehicles, renewable energy systems, aerospace, and defense are heavily investing in SiC-based substrates to enhance efficiency, thermal management, and overall device performance.

The region benefits from substantial research and development initiatives aimed at improving SiC wafer quality, reducing defects, and increasing production yields. Collaborations between industry and academia have accelerated innovation in SiC-On-Insulator technologies, enabling manufacturers to integrate these substrates into high-performance electronic and power systems.

Furthermore, North America’s focus on clean energy adoption and electrification strategies reinforces the market for high-efficiency substrates, as industries seek materials capable of supporting high-voltage applications and energy-dense components. The combination of strong industrial demand, technological expertise, and supportive innovation ecosystems positions North America as the leading market for SiC-On-Insulator and other advanced semiconductor substrates.

Get more information on this report

SiC-On-Insulator and Other Substrates Market Research Report Guidance:

The report includes qualitative and quantitative data in the SiC-On-Insulator and Other Substrates market across substrate type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the SiC-On-Insulator and Other Substrates market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the SiC-On-Insulator and Other Substrates market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the SiC-On-Insulator and Other Substrates market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the SiC-On-Insulator and Other Substrates market segments by substrate type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the SiC-On-Insulator and Other Substrates market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

SiC-On-Insulator and Other Substrates Market News and Key Development:

The sic-on-insulator and other substrates market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the sic-on-insulator and other substrates market are:

In February 2025, Infineon Technologies AG announced that it had released the first products to customers based on its advanced 200 mm SiC wafer manufacturing technology, strengthening its SiC production roadmap and enabling higher‑efficiency power semiconductor devices for renewable energy, EVs, and industrial applications.

In December 2024, Soitec announced that it had formally committed to deliver 300 mm RF‑SOI substrates to GlobalFoundries to support production of the company’s advanced RF‑SOI technology platforms used in 5G, Wi‑Fi, and other wireless radio‑frequency front‑end applications. This expansion of their long‑term supply relationship is aimed at ensuring a stable substrate supply for next‑generation connectivity chips.

Key Sources Referred:

International Electrotechnical CommissionInstitute of Electrical and Electronics EngineersInternational Organization for StandardizationBureau of Indian StandardsCentral Electricity AuthorityMinistry of PowerIndian Electrical and Electronics Manufacturers' AssociationEuropean Committee for Electrotechnical StandardizationVDE Association for Electrical Electronic & Information TechnologiesCompany WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - SiC-On-Insulator and Other Substrates Market

Soitec

SicoxsCorporation

SICC

XiamenPowerwayAdvancedMaterial

WolfspeedIncUS

MTICorporation

HebeiSynlightSemiconductor

GlobalWafers

CoherentCorporation

Ceramicforum

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the SiC-On-Insulator and Other Substrates Market?

The SiC-On-Insulator and Other Substrates Market is valued at US$ 15.2 Million in 2025, it is projected to reach US$ 460.8 Million by 2033.

What is the CAGR for SiC-On-Insulator and Other Substrates Market by (2026 - 2033)?

As per our report SiC-On-Insulator and Other Substrates Market, the market size is valued at US$ 15.2 Million in 2025, projecting it to reach US$ 460.8 Million by 2033. This translates to a CAGR of approximately 53.18% during the forecast period.

What segments are covered in this report?

The SiC-On-Insulator and Other Substrates Market report typically cover these key segments-

Substrate Type (Semi-insulating SiC Substrates, Conductive SiC Substrates)

Application (Power Devices, RF Devices, Other Appliactions)

What is the historic period, base year, and forecast period taken for SiC-On-Insulator and Other Substrates Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the SiC-On-Insulator and Other Substrates Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in SiC-On-Insulator and Other Substrates Market?

The SiC-On-Insulator and Other Substrates Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Soitec

SicoxsCorporation

SICC

XiamenPowerwayAdvancedMaterial

WolfspeedIncUS

MTICorporation

HebeiSynlightSemiconductor

GlobalWafers

CoherentCorporation

Ceramicforum

Who should buy this report?

The SiC-On-Insulator and Other Substrates Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the SiC-On-Insulator and Other Substrates Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For SiC-On-Insulator and Other Substrates Market

Get Free Sample For SiC-On-Insulator and Other Substrates Market