01

Market Summery

Executive Summary and Global Market Analysis

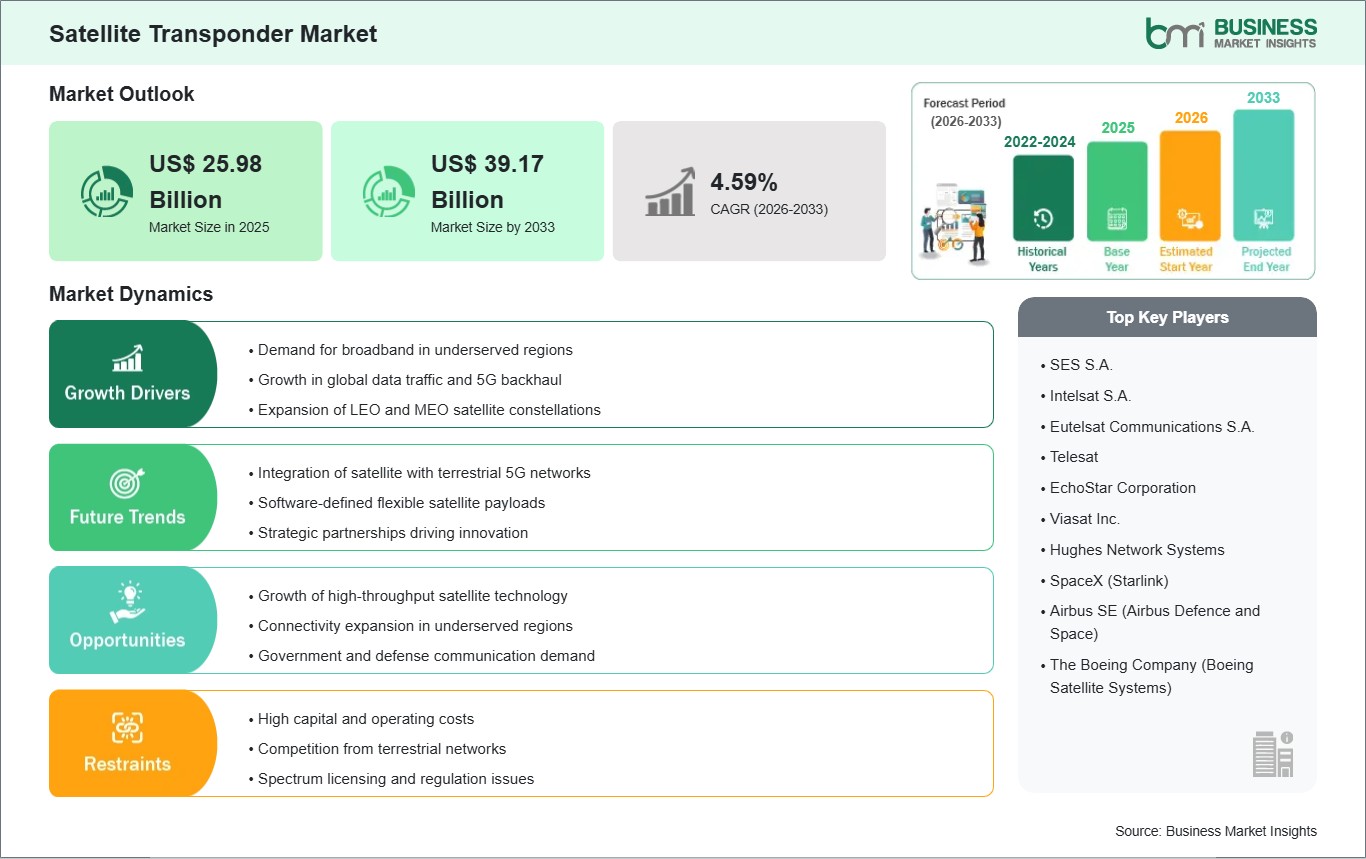

Satellite transponders are the foundational elements of the space segment in satellite communications, responsible for receiving upward signals from Earth, amplifying them, and retransmitting them to specific geographic footprints. These devices are indispensable for global connectivity, powering everything from high-definition television broadcasting and secure military data links to maritime navigation and remote sensing for environmental monitoring. The market is witnessing a significant shift toward High-Throughput Satellites (HTS) and the deployment of Low Earth Orbit (LEO) constellations, which offer lower latency and higher data speeds compared to traditional geostationary systems. This evolution is primarily driven by the exponential surge in data consumption for video streaming and the integration of satellite links with 5G backhaul services.

However, several challenges can restrain market growth, such as high satellite launch costs, spectral congestion, and the increasing prevalence of terrestrial fiber-optic networks in urban areas. The industry is also highly sensitive to international regulations regarding orbital slot allocations and spectrum licensing. Despite these hurdles, the market holds significant opportunities driven by the rise of the Internet of Things (IoT), the expansion of Direct-to-Home (DTH) services in emerging economies, and the demand for secure, anti-jamming communication channels for defense operations. Continued investments in multi-orbit hybrid networks and miniaturized satellite technology are expected to open new avenues for market expansion.

03

Segment Analysis

Satellite Transponder Market Segmentation

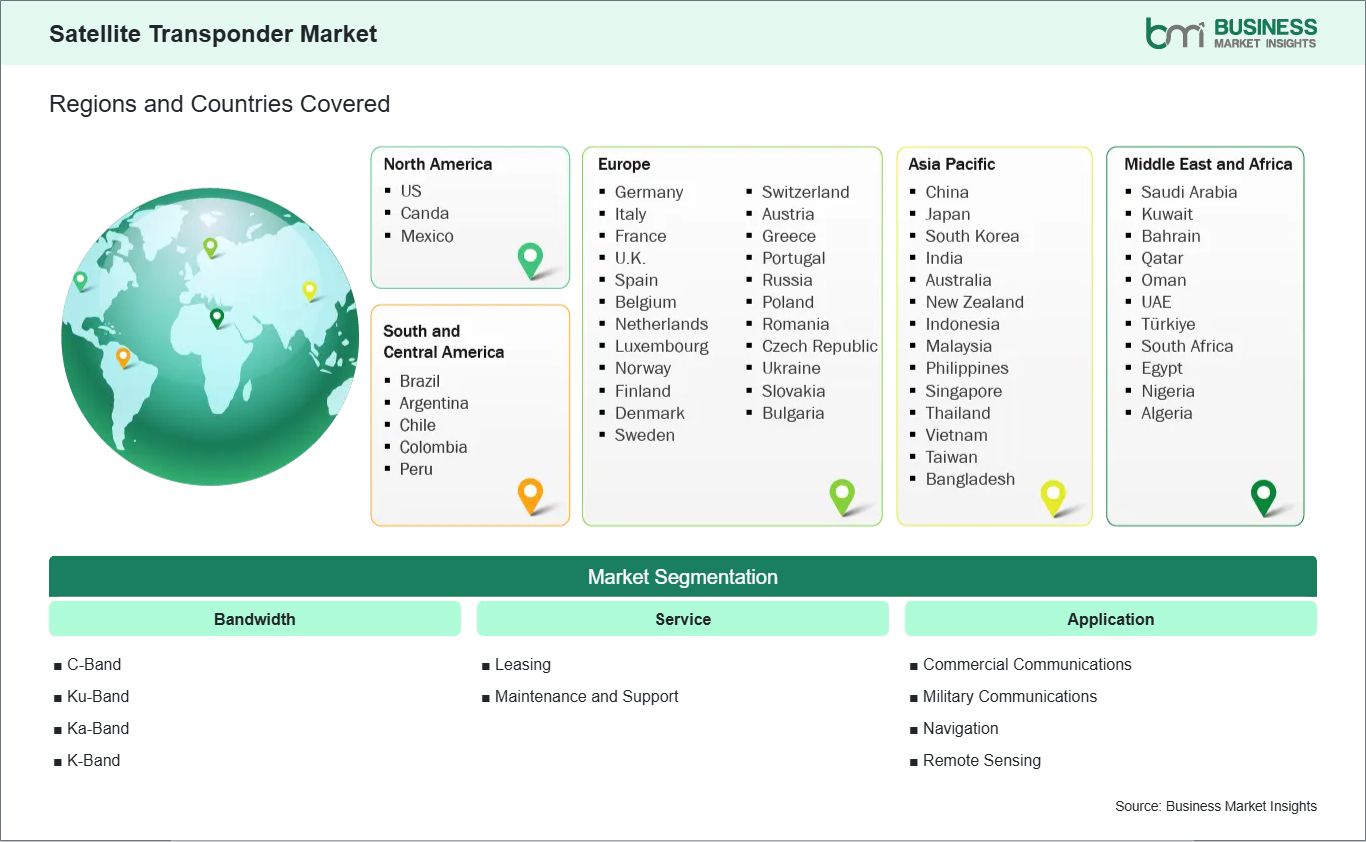

Key segments that contributed to the derivation of the Satellite Transponder market analysis are bandwidth, service, and application.

- By Bandwidth, the market is segmented into C-Band, Ku-Band, Ka-Band, and K-Band.

- By Service, the market is divided into Leasing and Maintenance and Support.

- By Application, the market is categorized into Commercial Communications, Military Communications, Navigation, and Remote Sensing.

04

Market Forces

Satellite Transponder Market Drivers and Opportunities

Escalating Global Demand for High-Speed Data and 5G Backhaul Services

The exponential surge in data consumption for high-definition video streaming, cloud computing, and 5G backhaul has emerged as a pivotal factor driving the satellite transponder market. As terrestrial networks struggle to meet the bandwidth requirements of data-intensive applications in rural or isolated regions, satellite transponders have become a critical bridge in the global digital supply chain. Mobile network operators are increasingly leasing transponder capacity to support 5G deployment in areas where laying fiber-optic cable is geographically challenging or cost-prohibitive.

For instance, the high-definition content has led to a nearly increase in required bandwidth per channel, as 4K and 8K video consumption grows. This robust expansion directly supports the growth of the satellite transponder market, as the need for high-frequency bands like Ka-band and Ku-band continues to increase to meet consumer expectations for seamless, high-speed connectivity worldwide. Furthermore, the digitalization of enterprise operations across the globe ensures that satellite-based internet remains a non-negotiable component for international business continuity, especially in the maritime and aviation sectors, where terrestrial infrastructure is nonexistent.

Expansion of Secure Military and Government Communication Infrastructure

As modern warfare becomes increasingly centered on real-time intelligence, surveillance, and reconnaissance (ISR), government and defense agencies are more reliant than ever on secure, dedicated transponder capacity. High-value, time-sensitive data for defense is frequently transmitted via specialized transponders that offer anti-jamming and encrypted capabilities to ensure signal integrity in contested environments.

In recent years, global defense budgets have seen a marked increase in allocations for space-based assets, with a focus on resilient communication networks that can survive terrestrial disruptions. This shift often involves the need for advanced transponder solutions that can support complex, time-critical military networks spanning multiple continents. Moreover, the rise of unmanned aerial vehicles (UAVs) and autonomous naval fleets further accelerates the demand for dedicated transponder links, as these platforms require constant, high-bandwidth connectivity for remote operation and data relay. This steady governmental investment provides a stable long-term revenue stream for satellite operators, fostering innovation in regenerative transponder technologies and secure multi-band payloads.

05

Size and Share Analysis

Satellite Transponder Market Size and Share Analysis

The satellite transponder market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within bandwidth, service, and application, offering insights into their contribution to overall market performance.

Based on Bandwidth, Ku-Band sub-segments are used in the industry standard for DTH television and VSAT services due to their optimal balance of terminal size and data throughput.

In terms of application, the Commercial Communications remain the largest application segment, supported by the massive bandwidth requirements of internet service providers (ISPs) and telecom operators.

07

Report Coverage

Satellite Transponder Market Report Coverage and Deliverables

The "Satellite Transponder Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Satellite Transponder market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Satellite Transponder market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Satellite Transponder market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Satellite Transponder market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Satellite Transponder Market Geographic Insights

The geographical scope of the Satellite Transponder market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America remains the largest region in the satellite transponder market. This is attributed to the presence of major satellite operators, a highly advanced defense sector, and the rapid adoption of 4K-UHD and OTT services that drive Ka-band demand. The United States is a primary contributor, with significant government spending on secure military communications and NASA-led research programs.

Asia-Pacific is expected to be the fastest-growing region during the forecast period. This growth is fueled by the rapid expansion of digital infrastructure in China and India, alongside a surge in DTH subscriptions in Southeast Asia. Regional initiatives to bridge the digital divide in rural areas have led to increased leasing of transponder capacity for satellite broadband. Furthermore, the rise of domestic space programs and private satellite startups in the region is enhancing local capacity and reducing reliance on international providers.

Europe demonstrates steady growth, driven by a strong media and broadcasting industry and the increasing use of satellite-based navigation and aviation connectivity. The region benefits from well-established regulatory frameworks and a high concentration of telecommunications leaders. Meanwhile, the Middle East & Africa and South & Central America are witnessing growth through the expansion of government-led connectivity projects and the rising need for reliable communications in the mining, oil, and gas industries located in remote territories.

10

Industry Activity

Recent Developments

The Satellite Transponder market is evaluated by gathering qualitative and quantitative data post primary and secondary research. A few of the key developments in the satellite transponder market are:

- In December 2025, Telesat announced a strategic partnership agreement among the Government of Canada, Telesat Corporation, and MDA Space to develop and deliver a multi-frequency, Arctic military satellite communications (MILSATCOM) capability to the Canadian Armed Forces.

- In December 2025, SKY Perfect JSAT Holdings Inc. announced that SKY Perfect JSAT Corporation had selected SpaceX to launch its communications satellites “JSAT-31” and “JSAT-32.” The agreement has been finalized, and together with the previously contracted “Superbird-9,” a total of three satellites are scheduled for sequential launches. JSAT-31” and “Superbird-9” are fully flexible satellites equipped with a fully digitalized communications payload, enabling dynamic adjustments of coverage areas and transmission capacity even after launch in orbit.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations