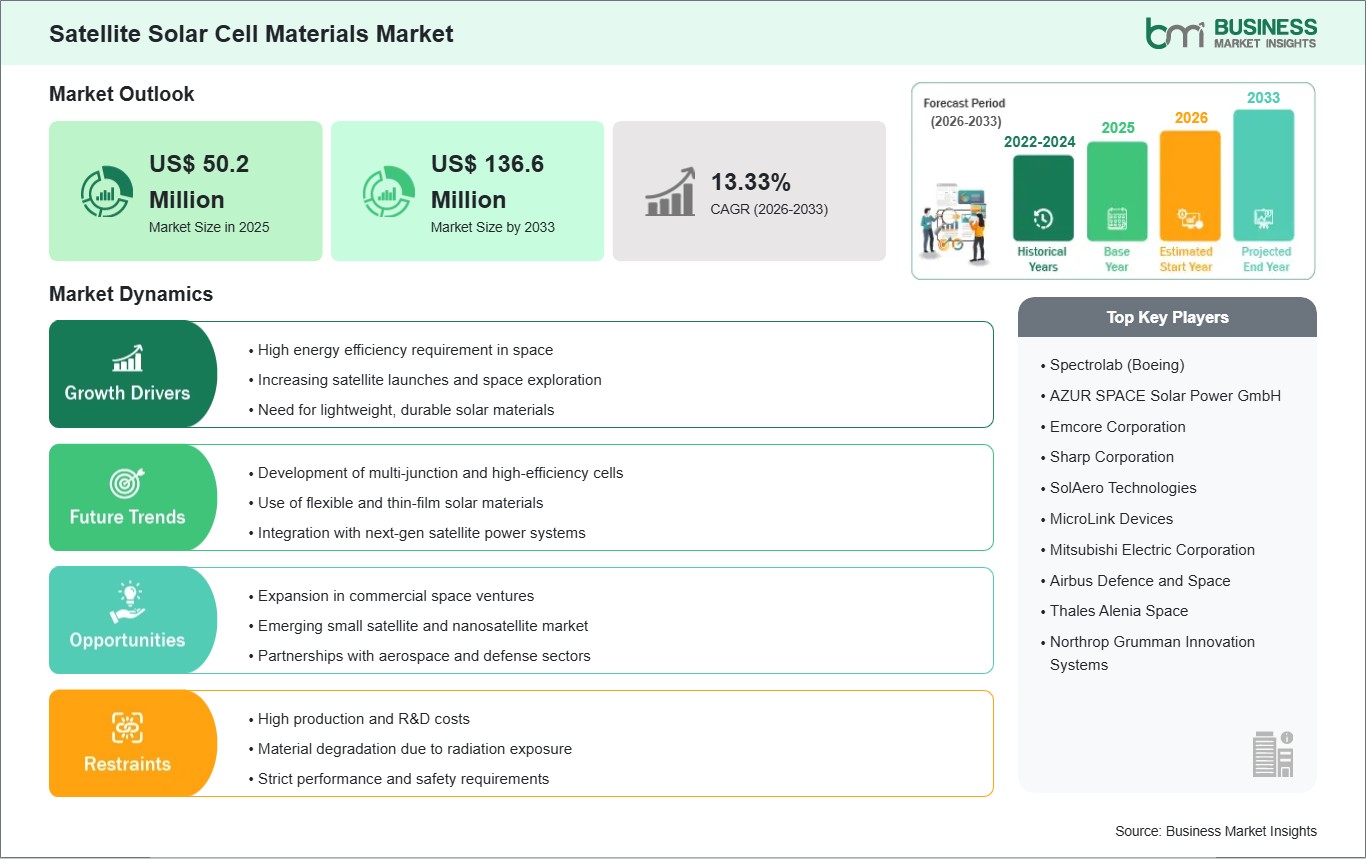

The Satellite Solar Cell Materials Outlook (2022-2033) size is expected to reach US$ 136.6 million by 2033 from US$ 50.2 million in 2025. The market is estimated to record a CAGR of 13.33% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global satellite solar cell materials market is witnessing significant growth, fueled by the rapid expansion of space exploration, satellite deployment, and advanced communication technologies. Satellite solar cells are critical for providing reliable, long-term energy in space, where durability, efficiency, and resistance to extreme temperatures and radiation are essential. Key drivers for this market include the growing demand for small satellites, including CubeSats and nanosatellites, which rely on lightweight, high-efficiency solar materials, and the increasing number of government and private space missions aimed at Earth observation, broadband internet, and scientific research.

Technological advancements in photovoltaic materials, such as multi-junction solar cells and flexible thin-film technologies, are enabling higher energy conversion rates while reducing weight, a critical factor for launch cost optimization. However, the market faces certain restraints. High production costs and stringent quality standards make the manufacturing process challenging. Additionally, long development cycles and the need for rigorous testing to ensure radiation resistance and thermal stability can delay commercialization. Supply chain limitations for specialized materials such as gallium arsenide and indium phosphide further complicate production. Despite these challenges, ongoing research into new lightweight, flexible, and radiation-hardened materials, along with growing investment in commercial and government satellite programs, is expected to drive innovation and long-term market expansion.

Satellite Solar Cell Materials Market - Strategic Insights:

Get more information on this report

Satellite Solar Cell Materials Market Segmentation Analysis:

Key segments that contributed to the derivation of the satellite solar cell materials analysis are material type, orbit, tracking, application, and component.

By material type, the satellite solar cell materials is segmented into silicon, CIGS, GAAS, and other material types. The silicon segment dominated the market in 2025.

By orbit, the satellite solar cell materials is segmented into LEO, MEO, GEO, HEO, and polar orbit. The low earth orbit (LEO) segment dominated the market in 2025.

By tracking, the satellite solar cell materials is segmented into fixed solar cells and tracking solar cells. The fixed solar cell segment dominated the market in 2025.

By application, the satellite solar cell materials is segmented into satellites, rovers, space station, and other applications. The satellites segment dominated the market in 2025.

In terms of components, the satellite solar cell materials is segmented into solar cells, solar panel, and electrical connection and interface. The solar panel segment dominated the market in 2025.

Satellite Solar Cell Materials Market Drivers and Opportunities:

Increasing Satellite Launches and Space Exploration

Western Europe has experienced a surge in satellite launches and space exploration activities, and this has a significant influence on the satellite solar cell material industry. The space agencies of various Western European countries, such as the French Centre National d’Études Spatiales (CNES) and the German DLR Space Administration, are focusing on small satellite missions for Earth observation, climate, and scientific research. The need for efficient and light solar cells that can provide long-lasting power in space has led Western European manufacturers to innovate in efficient photovoltaic materials.

The European Union’s emphasis on the development of independent space technologies has led to the establishment of joint launches with European launch companies in France and Sweden. This has seen the expansion of the regional satellite fleet, creating new demand for robust solar cell materials that meet the needs of these satellites in terms of resistance to radiation, temperature extremes, and long mission lifetimes. Suppliers in Western Europe are working on the development of the next generation of multi-junction solar cells and flexible substrate materials to meet these needs. The region is at the center of the development and utilization of solar cell materials for the needs of regional and international space exploratory endeavors.

Further, research institutions in Western Europe, including the UK and the Netherlands, have seen an increase in the development of solar cell materials with the aim of improving the efficiency and robustness of these materials. This has been made possible through the development of joint projects with industry that have reduced the time taken to develop these materials. The region is at the center of the development and utilization of solar cell materials for the needs of regional and international space exploratory endeavors.

Expansion In Commercial Space Ventures

The Western European satellite solar cell materials industry is also benefiting from the rapid growth in the number of commercial space operations. Several business organizations in the UK, France, and Germany are launching several small satellites for telecommunications, earth observation, and data services. The operations of these small satellites are carried out on tighter margins in terms of costs and performance. Therefore, there is an increasing demand for cost-effective and long-lasting solar cell materials that can be produced in large quantities.

Several business organizations and startups in the aerospace industry are investing in modular solar materials and solutions that can be used for various satellite operations. For instance, several business organizations in London and Toulouse are working with material scientists to design lightweight and foldable solar materials that can be used in small satellites. The emphasis on flexibility and customization is in line with the overall technology industry in Western Europe. Several innovation centers in the region are promoting interdisciplinary collaboration in the fields of electronics engineering and materials science.

Commercial satellite business also receives funding support from various regional funding programs that aim to enhance technological competitiveness. Such funding support from innovation funds in the EU helps in developing prototypes and production of innovative solar cell materials. This helps businesses scale up their innovations and attract further funding for commercialization. With commercial satellite businesses increasingly developing different applications for their satellites, Western Europe’s market for solar cell materials is expected to continue growing through both entrepreneurial and strategic support for space industry development.

Satellite Solar Cell Materials Market Size and Share Analysis:

The global Satellite solar cell materials is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material type, orbit, tracking, application, and component highlighting their respective contributions to overall market performance.

By material type, the silicon subsegment dominated the market in 2025 because it is cost-effective, reliable, and has well-established manufacturing processes. While newer materials like CIGS and GaAs offer higher efficiency, silicon provides a strong balance of performance, durability, and availability, making it the preferred choice for most satellites.

By orbit, the low earth orbit (LEO) segment subsegment dominated the market in 2025 dominates because most commercial, scientific, and communication satellites are being deployed in low earth orbit. The shorter orbital distance reduces radiation exposure and allows solar cells to operate efficiently with less degradation over time.

By tracking, the fixed solar cell subsegment dominated the market in 2025 because they are simpler, lighter, and require less maintenance than tracking systems. In space applications, reliability and minimal moving parts are crucial, making fixed cells more practical for long-term satellite missions

By application, the satellites subsegment dominated the market in 2025 because demand for communication, earth observation, and navigation satellites continues to rise. Solar cells are essential for powering these space craft reliably in orbit, driving consistent market demand.

By component, the solar panel subsegment dominated because they integrate multiple solar cells into a single, efficient, and durable unit ready for satellite deployment. They provide structural support, protect the cells from space conditions, and simplify installation and maintenance, making them more critical than individual cells or electrical interfaces.

Satellite Solar Cell Materials Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Spectrolab (Boeing)

AZUR SPACE Solar Power GmbH

Emcore Corporation

Sharp Corporation

SolAero Technologies

MicroLink Devices

Mitsubishi Electric Corporation

Airbus Defence and Space

Thales Alenia Space

Northrop Grumman Innovation Systems

Get more information on this report

Satellite Solar Cell Materials Market Report Coverage and Deliverables:

The "Satellite Solar Cell Materials Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Satellite solar cell materials size and forecast at the regional and country levels for segments covered under the scope

Satellite solar cell materials trends, as well as drivers, restraints, and opportunities

Satellite solar cell materials analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the satellite solar cell materials.

Detailed company profiles, including SWOT analysis

Satellite Solar Cell Materials Market Geographic Insights:

The geographical scope of the Satellite solar cell materials report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America dominates the satellite solar cell materials market, largely due to its leadership in space technology, advanced research infrastructure, and strong presence of private and government satellite programs. The United States, in particular, leads in the deployment of geostationary, low-earth orbit, and small satellite missions, driving demand for high-efficiency and reliable solar cell materials. The region benefits from significant investment in space R&D from agencies such as NASA and private aerospace companies, fostering innovation in multi-junction solar cells, flexible thin films, and lightweight photovoltaic materials.

The aerospace industry, as well as the defense industry, are some of the key contributors to this market, with the need for solar materials to endure harsh space environment conditions such as high levels of radiation, extreme temperature changes, and micrometeoroid strikes. Cost optimization strategies are also emphasized in the North American region, with a focus on reusable, modular satellite structures that use strong, lightweight solar materials. Despite the high production costs of solar cell materials, as well as the strict regulations in place, the technological prowess of the region, coupled with the strong relationships between industry players, guarantees that this region remains at the forefront of solar cell material innovation.

Get more information on this report

Satellite Solar Cell Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the satellite solar cell materials across material type, orbit, tracking. Application, component, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Satellite solar cell materials.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the satellite solar cell materials, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Satellite solar cell materials scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 12 cover the satellite solar cell materials segments material type, orbit, tracking, application, component and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 13 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 14 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 15 provides detailed profiles of the major companies operating in the satellite solar cell materials. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 16, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Satellite Solar Cell Materials Market News and Key Development:

The satellite solar cell materials is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Satellite solar cell materials are:

In November 2025, SCHOTT AG announced that it launched its SCHOTT® Solar Glass exos, a high‑performance space‑qualified solar cell cover glass developed in collaboration with Heilbronn‑based AZUR SPACE Solar Power GmbH and supported by the European Space Agency (ESA) and the German Aerospace Center (DLR). This material is designed for next‑generation satellite solar cells and strengthens a European supply chain for advanced space photovoltaic materials.

In December 2025, SCHOTT and AZUR SPACE Solar Power announced that they completed joint development and testing of the new space solar cell cover glass (exos), engineered for compatibility with both silicon and III‑V multijunction solar cells used on satellites, helping drive material innovation and resilience for European space missions.

In 2024 - 2025, AZUR SPACE Solar Power GmbH expanded its role as a key European manufacturer of multi‑junction space solar cells and assemblies (e.g., 3G30‑Advanced and 4G32‑Advanced cells), supplying high‑efficiency photovoltaic materials critical to satellite solar arrays, thereby supporting satellite programs serving European and global markets.

Key Sources Referred:

EU REACH Regulation

National Aeronautics and Space Administration (NASA)

European Space Agency (ESA)

Company Websites

Company Annual Reports

Company Investor Presentations

The List of Companies - Satellite Solar Cell Materials Market

Spectrolab (Boeing)

AZUR SPACE Solar Power GmbH

Emcore Corporation

Sharp Corporation

SolAero Technologies

MicroLink Devices

Mitsubishi Electric Corporation

Airbus Defence and Space

Thales Alenia Space

Northrop Grumman Innovation Systems

Frequently Asked Questions

How big is the Satellite Solar Cell Materials Market?

The Satellite Solar Cell Materials Market is valued at US$ 50.2 Million in 2025, it is projected to reach US$ 136.6 Million by 2033.

What is the CAGR for Satellite Solar Cell Materials Market by (2026 - 2033)?

As per our report Satellite Solar Cell Materials Market, the market size is valued at US$ 50.2 Million in 2025, projecting it to reach US$ 136.6 Million by 2033. This translates to a CAGR of approximately 13.33% during the forecast period.

What segments are covered in this report?

The Satellite Solar Cell Materials Market report typically cover these key segments-

Material Type (Silicon, CIGS, GAAS, Other Material Types)

Orbit (LEO, MEO, GEO, HEO, Polar Orbit)

Tracking (Fixed Solar Cell, Tracking Solar Cell)

Application (Satellites, Rovers, Space Station, Other Applications)

What is the historic period, base year, and forecast period taken for Satellite Solar Cell Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Satellite Solar Cell Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Satellite Solar Cell Materials Market?

The Satellite Solar Cell Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Spectrolab (Boeing)

AZUR SPACE Solar Power GmbH

Emcore Corporation

Sharp Corporation

SolAero Technologies

MicroLink Devices

Mitsubishi Electric Corporation

Airbus Defence and Space

Thales Alenia Space

Northrop Grumman Innovation Systems

Who should buy this report?

The Satellite Solar Cell Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Satellite Solar Cell Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Satellite Solar Cell Materials Market

Get Free Sample For Satellite Solar Cell Materials Market