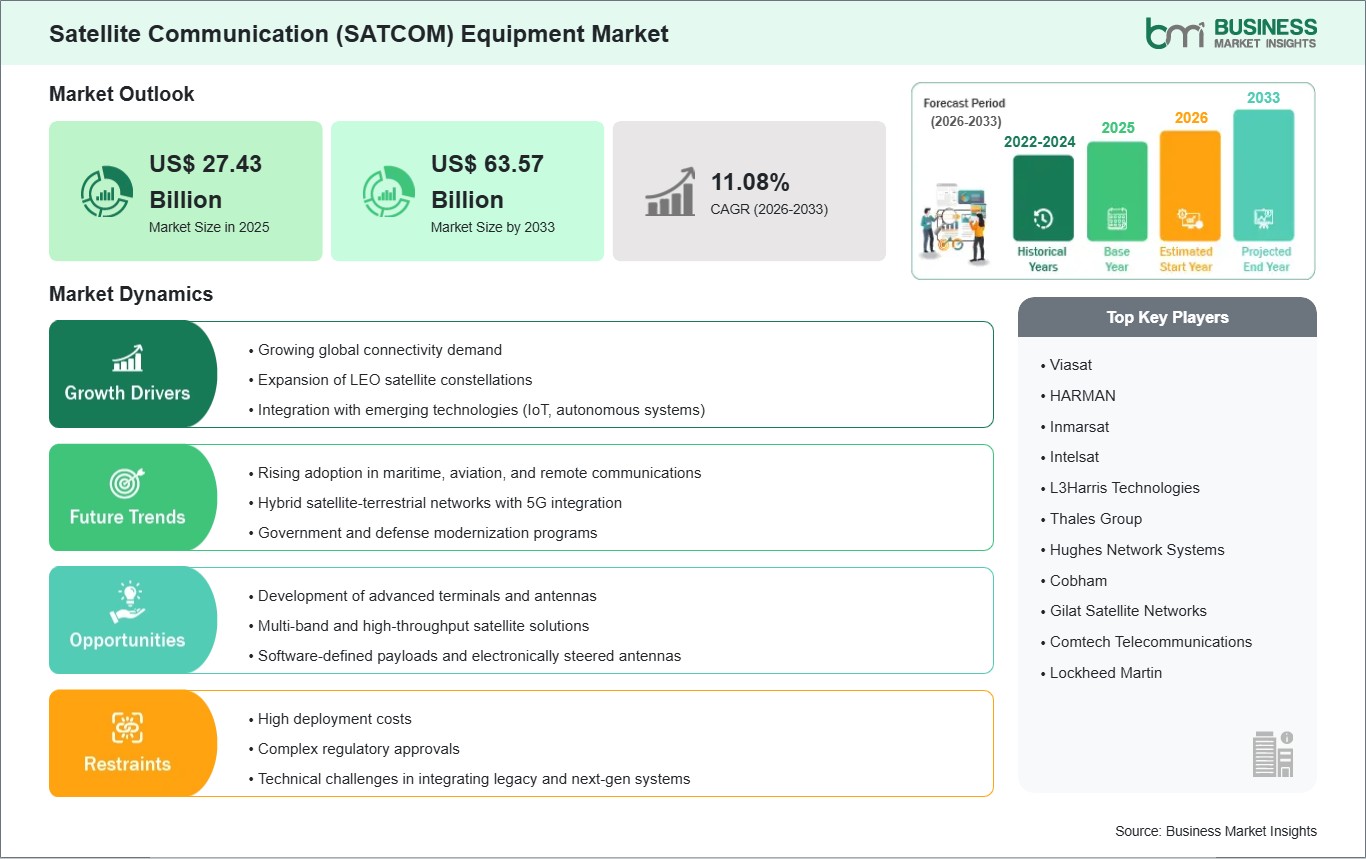

The Satellite Communication (SATCOM) Equipment Market size is expected to reach US$ 63.57 billion by 2033 from US$ 27.43 billion in 2025. The market is estimated to record a CAGR of 11.08% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global SATCOM equipment market is a critical component of modern communication infrastructure, enabling reliable data transmission across remote, maritime, airborne, and defense environments. SATCOM equipment includes antennas, transceivers, modems, and ground terminals that facilitate voice, video, and data communication via satellite networks.

Growth is driven by the need for broadband connectivity in underserved regions, advancements in LEO satellite constellations, high-throughput satellites (HTS), and multi-band communication systems, enhancing bandwidth and reducing latency. These developments support aviation, maritime, disaster response, and military communications.

Competitive dynamics focus on multi-band capability, compact terminal design, high data throughput, and interoperability with next-generation satellite networks. Integration with terrestrial networks, including 5G, supports hybrid communication models. SATCOM equipment is increasingly foundational for resilient, scalable, and secure connectivity across industries and geographies.

Satellite Communication (SATCOM) Equipment Market - Strategic Insights:

Get more information on this report

Satellite Communication (SATCOM) Equipment Market Segmentation Analysis:

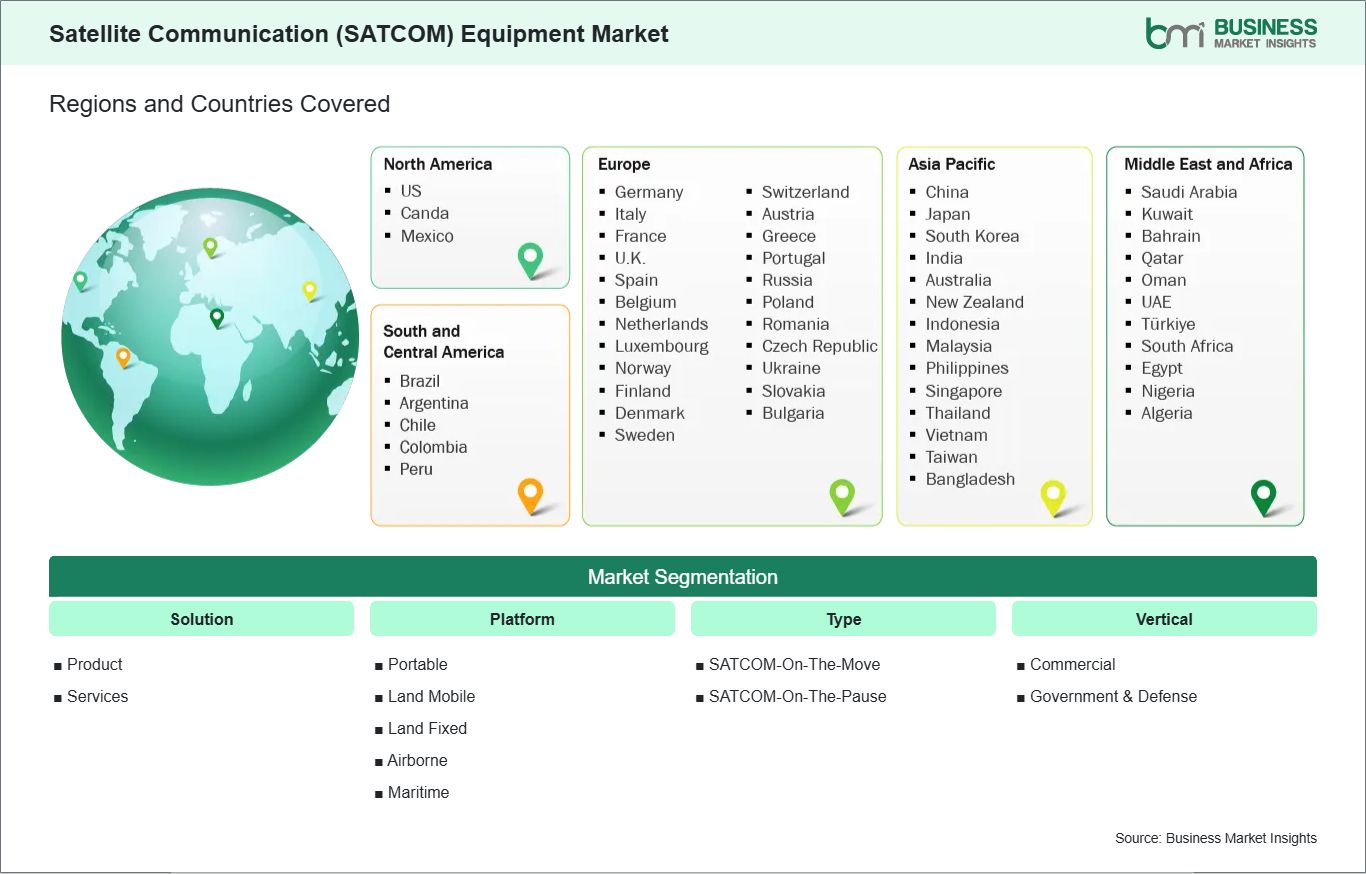

Key segments that contributed to the derivation of the satellite communication (SATCOM) equipment market analysis are solution, platform, type, vertical, frequency band, connectivity, technology, and terminal.

By solution, the satellite communication (SATCOM) equipment market is segmented into product and services. The services segment dominated the market in 2025.

Based on platform, the satellite communication (SATCOM) equipment market is categorized into portable, land mobile, land fixed, airborne, and maritime. The land-based segment (including land fixed and land mobile) dominated the market in 2025.

In terms of type, the satellite communication (SATCOM) equipment market is divided into SATCOM-On-The-Move (SOTM) and SATCOM-On-The-Pause (SOTP). The SOTM segment dominated the market in 2025.

By vertical, the satellite communication (SATCOM) equipment market is segmented into commercial and government & defense. The commercial segment dominated the market in 2025.

Based on frequency band, the satellite communication (SATCOM) equipment market includes C-band, L & S-band, X-band, Ka-band, Ku-band, VHF/UHF-band, EHF/SHF-band, multi-band, and Q-band. The Ku-band segment dominated the market in 2025.

By connectivity, the satellite communication (SATCOM) equipment market is segmented into LEO, MEO, and GEO orbits. The LEO segment held the largest share in 2025.

Based on technology, the satellite communication (SATCOM) equipment market is categorized into next-generation and legacy systems. The legacy segment dominated in 2025.

By terminal, the satellite communication (SATCOM) equipment market includes LTE-based and non-LTE-based systems. The non-LTE-based segment dominated the market in 2025.

Satellite Communication (SATCOM) Equipment Market Drivers and Opportunities:

Growing Demand for Global Connectivity

Satellite systems provide reliable communications in remote and underserved areas where terrestrial networks are limited, expensive, or damaged. Over 100 million users rely on SATCOM services, bridging the digital divide. Industries like maritime, aviation, oil & gas, and defense demand real-time communication, navigation, and monitoring to enhance operational efficiency and safety.

Integration with IoT, autonomous systems, and smart infrastructure increases demand for SATCOM equipment. Government programs expanding or upgrading satellite infrastructure create additional growth opportunities for manufacturers.

Advancements in LEO Satellites

LEO satellite constellations provide lower latency, higher capacity, and improved global coverage. Applications include autonomous vehicles, remote monitoring, and high-speed internet services. Growth of LEO satellites drives demand for ground terminals, antennas, and tracking systems.

High-throughput satellites (HTS), multi-band communications, and electronically steered antennas improve SATCOM quality and efficiency. Integration with terrestrial networks, including 5G, supports hybrid models for applications like smart cities and connected mobility. Continuous technological innovation enables manufacturers to meet evolving client requirements.

Satellite Communication (SATCOM) Equipment Market Size and Share Analysis:

The Satellite Communication (SATCOM) Equipment Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within solution, platform, type, vertical, frequency band, connectivity, technology, and terminal, offering insights into their contribution to overall market performance.

By solution, the services segment dominated the market in 2025, driven by increasing reliance on satellite bandwidth services, managed communication networks, and recurring service-based revenue models.

Based on platform, the land-based segment dominated the market in 2025, driven by large-scale deployment of fixed ground stations, enterprise communication hubs, and defense communication systems.

In terms of type, the SATCOM-On-The-Move (SOTM) segment dominated the market in 2025, driven by the need for uninterrupted connectivity across mobile platforms such as aircraft, naval vessels, and military vehicles.

By vertical, the commercial segment dominated the market in 2025, driven by high demand for broadband connectivity, media broadcasting, and aviation communication services.

Based on frequency band, the Ku-band segment dominated the market in 2025, driven by its widespread use in satellite television, broadband internet, and VSAT networks.

By connectivity, the LEO orbit segment dominated the market in 2025, driven by the rapid deployment of low-earth orbit satellite constellations for high-speed, low-latency communication.

In terms of technology, the legacy systems segment dominated the market in 2025, driven by advancements in high-throughput satellites, software-defined payloads, and electronically steered antennas.

By terminal, the non-LTE-based segment dominated the market in 2025, driven by the extensive installed base of traditional SATCOM terminals, while LTE-based terminals are gradually gaining adoption with the integration of satellite and 5G networks.

Satellite Communication (SATCOM) Equipment Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Viasat

HARMAN

Inmarsat

Intelsat

L3Harris Technologies

Thales Group

Hughes Network Systems

Cobham

Gilat Satellite Networks

Comtech Telecommunications

Lockheed Martin

Get more information on this report

Satellite Communication (SATCOM) Equipment Market Report Coverage and Deliverables:

The "Satellite Communication (SATCOM) Equipment Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Satellite Communication (SATCOM) Equipment Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Satellite Communication (SATCOM) Equipment Market trends, as well as drivers, restraints, and opportunities

Satellite Communication (SATCOM) Equipment Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Satellite Communication (SATCOM) Equipment Market

Detailed company profiles, including SWOT analysis

Satellite Communication (SATCOM) Equipment Market Geographic Insights:

The geographical scope of the Satellite Communication (SATCOM) Equipment Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

The geographical scope of the Satellite Communication (SATCOM) Equipment Market report is divided into North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America. North America held the largest market share in 2025.

North America’s dominance is primarily attributed to strong investments in satellite communication infrastructure, presence of major satellite operators, and extensive adoption across defense, aviation, and commercial sectors. The region benefits from advanced technological capabilities and early adoption of next-generation satellite systems, including LEO constellations and high-throughput satellites. According to market data, North America accounted for over 40% share of the SATCOM equipment market, highlighting its leadership position.

Europe represents a significant market driven by increasing investments in secure communication systems, aerospace innovation, and cross-border connectivity initiatives. The region is actively advancing satellite programs to support defense, navigation, and environmental monitoring applications.

The Asia Pacific region is expected to witness the fastest growth during the forecast period, supported by rising demand for broadband connectivity, expanding telecommunications infrastructure, and increasing government initiatives for digital inclusion. Countries such as China and India are investing heavily in satellite communication to enhance connectivity in rural and remote areas, contributing to market expansion.

Meanwhile, the Middle East & Africa and South & Central America are experiencing gradual growth driven by infrastructure development, increasing adoption of satellite-based communication services, and rising demand for connectivity in remote and underserved regions.

Across all regions, the growing need for reliable communication, increasing investments in satellite technology, and expansion of commercial and defense applications are shaping the adoption of SATCOM equipment globally.

Get more information on this report

Satellite Communication (SATCOM) Equipment Market Research Report Guidance:

The report includes qualitative and quantitative data in the Satellite Communication (SATCOM) Equipment Market across type, application, industry, and geography.

The report starts with key takeaways (chapter 2), highlighting key trends and outlook of the Satellite Communication (SATCOM) Equipment Market.

Chapter 3 focuses on research methodology.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights major industry dynamics, including drivers, restraints, and opportunities.

Chapter 6 discusses historical revenues and forecast till 2033.

Chapters 7 to 11 cover segment analysis across regions.

Chapter 12 describes competitive analysis.

Chapter 13 describes industry landscape analysis.

Chapter 14 provides company profiles.

Chapter 15 includes appendix and disclaimer.

Satellite Communication (SATCOM) Equipment Market News and Key Development:

The Satellite Communication (SATCOM) Equipment Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the satellite communication (SATCOM) equipment market are:

In March 2026, Automotive and connectivity provider HARMAN announced a collaboration with Viasat to enable satellite voice calling capabilities within HARMAN Ready Connect connected car products, enhancing reliable voice communication via satellite in areas without cellular coverage.

In January 2026, Viasat partnered with Bharat Sanchar Nigam Limited (BSNL) to upgrade the Indian Navy’s satellite communication infrastructure using advanced Ka‑Band systems, enhancing maritime connectivity, bandwidth capability, and secure data links for naval operations. The deployment reflects ongoing defense sector modernization and demand for sophisticated SATCOM equipment.

Key Sources Referred:

World Health Organization (WHO)Organisation for Economic Cooperation and Development (OECD)The World Bank GroupWorldometerInternational Telecommunication Union (ITU)

The List of Companies - Satellite Communication (SATCOM) Equipment Market

Viasat

HARMAN

Inmarsat

Intelsat

L3Harris Technologies

Thales Group

Hughes Network Systems

Cobham

Gilat Satellite Networks

Comtech Telecommunications

Lockheed Martin

Frequently Asked Questions

How big is the Satellite Communication (SATCOM) Equipment Market?

The Satellite Communication (SATCOM) Equipment Market is valued at US$ 27.43 Billion in 2025, it is projected to reach US$ 63.57 Billion by 2033.

What is the CAGR for Satellite Communication (SATCOM) Equipment Market by (2026 - 2033)?

As per our report Satellite Communication (SATCOM) Equipment Market, the market size is valued at US$ 27.43 Billion in 2025, projecting it to reach US$ 63.57 Billion by 2033. This translates to a CAGR of approximately 11.08% during the forecast period.

What segments are covered in this report?

The Satellite Communication (SATCOM) Equipment Market report typically cover these key segments-

Solution (Product, Services)

Platform (Portable, Land Mobile, Land Fixed, Airborne, Maritime)

Type (SATCOM-On-The-Move (SOTM), SATCOM-On-The-Pause (SOTP))

Vertical (Commercial, Government & Defense)

What is the historic period, base year, and forecast period taken for Satellite Communication (SATCOM) Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Satellite Communication (SATCOM) Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Satellite Communication (SATCOM) Equipment Market?

The Satellite Communication (SATCOM) Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Viasat

HARMAN

Inmarsat

Intelsat

L3Harris Technologies

Thales Group

Hughes Network Systems

Cobham

Gilat Satellite Networks

Comtech Telecommunications

Lockheed Martin

Who should buy this report?

The Satellite Communication (SATCOM) Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Satellite Communication (SATCOM) Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Satellite Communication (SATCOM) Equipment Market

Get Free Sample For Satellite Communication (SATCOM) Equipment Market