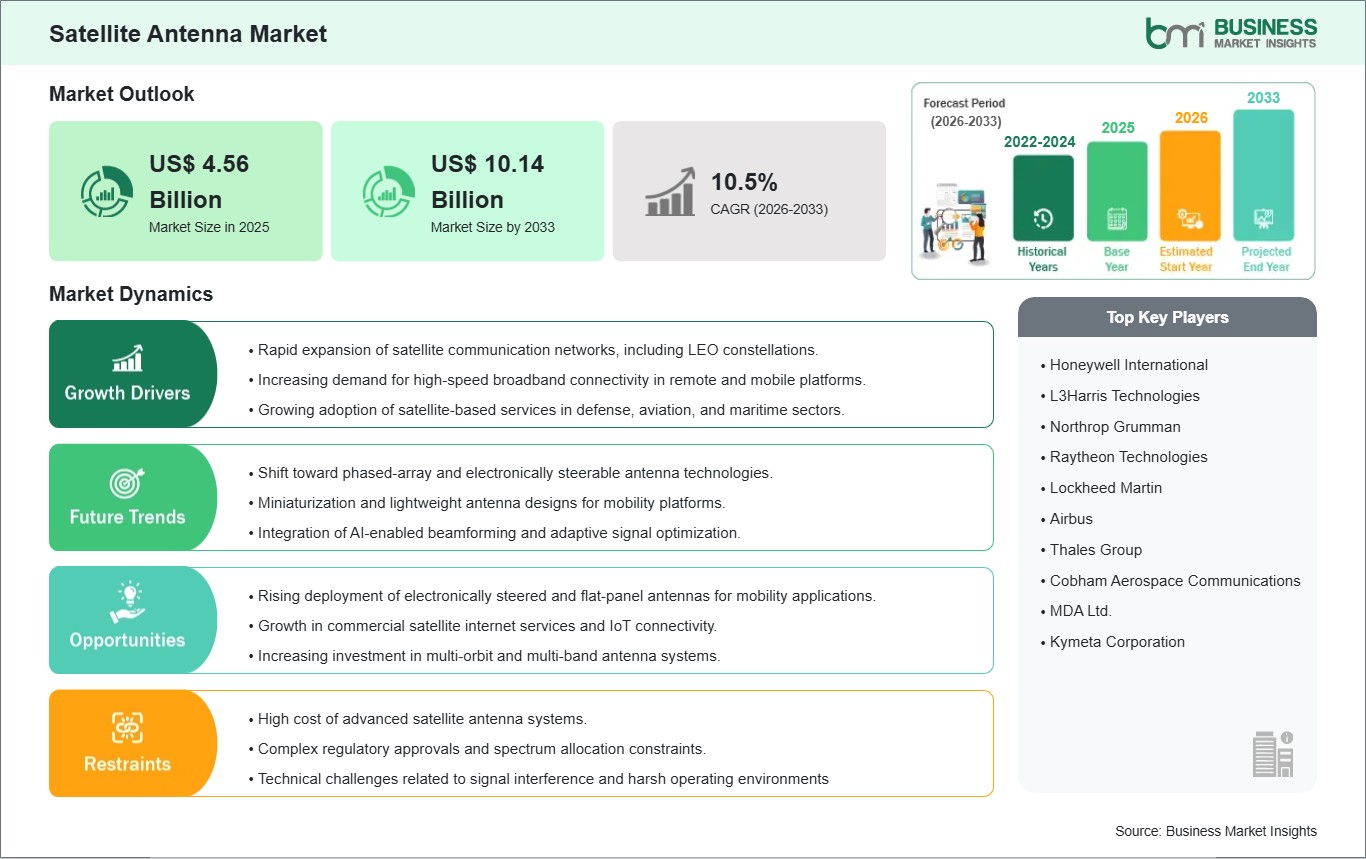

The satellite antenna market size is expected to reach US$ 10.14 billion by 2033 from US$ 4.56 billion in 2025. The market is estimated to record a CAGR of 10.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Satellite antennas are communication systems engineered to transmit and receive radio frequency signals between satellites and terrestrial or mobile platforms. These antennas support connectivity across broadcasting, military communications, navigation, broadband internet, and aerospace operations. Their configurations differ according to mobility requirements, operating frequency bands, tracking precision, and environmental endurance conditions.

Global communication infrastructure modernization and expanding satellite constellations continue reinforcing deployment activity across the sector. Enterprises and government agencies increasingly seek uninterrupted connectivity for remote operations, transportation systems, and mission-critical networks. Rising utilization of low Earth orbit satellite networks additionally supports antenna integration across mobility-focused communication applications.

Flat panel antennas are gaining commercial attention because compact architectures and electronically steered capabilities support high-speed communication on moving platforms. Parabolic reflector antennas maintain considerable industry relevance for fixed installations requiring stable long-distance signal transmission. Ku/Ka band systems continue witnessing broader integration due to expanding broadband communication requirements across commercial and defense sectors.

Technology evolution within the industry increasingly emphasizes phased-array architectures, lightweight materials, and software-controlled beam steering functionality. Manufacturers are refining antenna efficiency to improve signal tracking accuracy, lower latency, and optimize bandwidth performance across multi-orbit satellite networks. Advanced integration with maritime, airborne, and autonomous mobility systems is additionally shaping next-generation satellite communication infrastructure.

Competitive conditions remain influenced by satellite broadband expansion, defense communication modernization, and connected mobility initiatives. Market participants prioritize compact antenna engineering, thermal resilience, and interoperability across multiple frequency bands and orbital systems. Long-term strategic emphasis on global connectivity infrastructure and real-time communication capability continues supporting innovation across the satellite antenna market.

Satellite Antenna Market - Strategic Insights:

Get more information on this report

Satellite Antenna Market Segmentation Analysis:

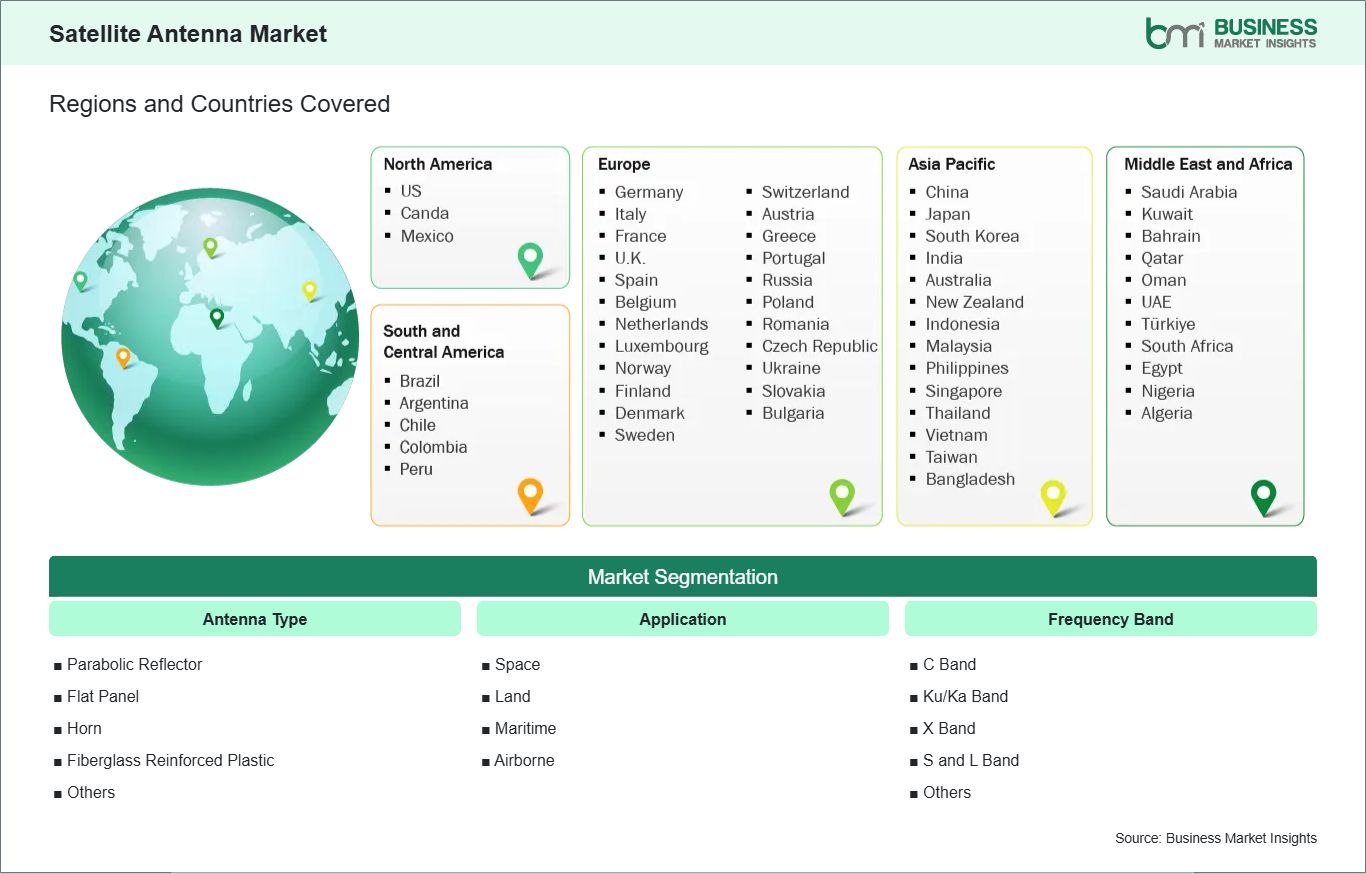

The satellite antenna market is segmented based on antenna type, application and frequency band.

By Antenna Type

Parabolic Reflector – Maintains strong signal concentration for long-range satellite communication systems.

Satellite Antenna Market Drivers and Opportunities:

Expansion of Satellite-Based Broadband and Mobility Communication

Telecommunication providers and aerospace operators continue strengthening satellite-based communication infrastructure to support uninterrupted global connectivity. Mobile platforms across aviation, shipping, and remote terrestrial operations increasingly require stable high-bandwidth communication systems capable of operating under dynamic environmental conditions. This requirement has accelerated deployment of advanced satellite antenna technologies with enhanced tracking precision and multi-band communication capability.

The operational impact extends into defense modernization, disaster response coordination, and broadband accessibility initiatives. Governments and commercial entities increasingly prioritize resilient communication architecture supporting remote operations and mission continuity. Satellite antennas therefore maintain heightened strategic relevance across connected transportation systems, intelligence operations, and next-generation communication ecosystems.

Development of Electronically Steered and Flat Panel Antenna Systems

Advancements in phased-array engineering and electronically steered communication technologies are reshaping antenna system capabilities. Flat panel antennas increasingly support mobility-oriented communication environments by reducing mechanical complexity and improving aerodynamic efficiency. Innovations in beamforming technologies and lightweight materials are also enabling more compact and energy-efficient antenna deployment across airborne and maritime platforms.

Future opportunities are associated with expanding low Earth orbit satellite constellations and integrated multi-orbit communication networks. Enterprises continue evaluating antenna systems capable of seamless broadband connectivity across terrestrial and mobile environments. Expanding deployment of autonomous transportation systems and connected defense platforms is anticipated to reinforce broader market progression.

Satellite Antenna Market Size and Share Analysis:

The Satellite Antenna Market was valued at USD 4.56 Billion in 2025 and is projected to reach USD 10.14 Billion by 2033, expanding at a CAGR of 10.50% during 2026–2033. Market progression reflects stronger investment in satellite communication infrastructure, connected mobility systems, and advanced broadband connectivity solutions across commercial and government sectors.

Flat panel antennas maintain rising industry prominence due to compact integration capability and electronically steered communication functionality. Ku/Ka band systems also account for considerable deployment because high-throughput communication networks increasingly require enhanced bandwidth efficiency and advanced signal performance.

Land-based applications represent a substantial market contribution owing to expanding satellite broadband infrastructure and remote communication requirements. Airborne and maritime applications additionally demonstrate notable deployment momentum as transportation systems prioritize uninterrupted connectivity and operational communication reliability.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Honeywell International

L3Harris Technologies

Northrop Grumman

Raytheon Technologies

Lockheed Martin

Airbus

Thales Group

Cobham Aerospace Communications

MDA Ltd.

Kymeta Corporation

Get more information on this report

Satellite Antenna Market Report Coverage and Deliverables:

The Satellite Antenna report provides a detailed analysis of the market covering the below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Satellite Antenna Market Geographic Insights:

The Satellite Antenna market shows diverse regional adoption patterns influenced by satellite broadband expansion, defense communication priorities, aerospace modernization programs, and connected mobility infrastructure development. Communication providers and government agencies worldwide continue strengthening satellite connectivity capabilities to support resilient broadband coverage and mission-critical communication systems.

North America demonstrates strong market advancement due to extensive aerospace innovation, defense communication investment, and commercial satellite deployment activity. Enterprises across the region increasingly integrate flat panel and phased-array antenna technologies into airborne, maritime, and terrestrial communication platforms. Expanding low Earth orbit satellite programs additionally contribute to higher deployment of next-generation antenna systems supporting high-throughput connectivity.

Asia Pacific reflects accelerating communication infrastructure development supported by expanding space programs and rising broadband accessibility initiatives. Governments and telecommunication operators throughout the region continue prioritizing satellite connectivity solutions for remote coverage expansion and transportation communication networks. Maritime trade activity and aviation modernization programs further strengthen utilization of advanced antenna systems across regional markets.

Europe maintains a technologically advanced communication ecosystem emphasizing secure connectivity, aerospace research, and integrated satellite communication capability. Regional organizations continue focusing on electronically steered antenna systems and multi-band communication platforms for defense and commercial environments. Emerging markets across the Middle East, Africa, and South and Central America are additionally strengthening satellite communication infrastructure to improve digital access, navigation efficiency, and remote connectivity coverage.

Get more information on this report

Satellite Antenna Market Research Report Guidance:

The Satellite Antenna market report encompasses both qualitative and quantitative data pertaining to the market, categorized by antenna type, application, frequency band and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on antenna type, application, frequency band, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Satellite Antenna Market News and Key Development:

The satellite antenna market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In Apri, 2026, Amazon Leo is preparing to provide fast, reliable internet connectivity to a wide variety of customers, using satellites in low Earth orbit to deliver high speeds and low latency across land, sea, and skies. The company is designing its own hardware to optimize performance across the network, and its newest antenna, the Amazon Leo Aviation Antenna, will allow commercial airline passengers and crew to enjoy high performance from their departure gate all the way to their arrival gate.

In November 2025, KYOCERA AVX launched a new LDS cap antenna and evaluation board optimized for Iridium® satellite IoT applications and designated as Iridium Qualified Antenna products for Iridium Certus 9704 modules. Developed to provide Iridium with an embedded antenna optimized for low Earth orbit (LEO) satellites used to provide seamless connectivity and data exchange for IoT devices anywhere in the world, the new KYOCERA AVX LDS cap antenna developed for Iridium outperforms the ceramic patch antennas traditionally used in these applications.

Key Sources Referred:

Satellite communication industry reportsGovernment aerospace and communication databasesAcademic journals related to RF and antenna engineeringCompany annual reports and communication filingsSpace communication and broadband research studiesDefense communication technology publicationsMaritime and airborne connectivity research papersSatellite mobility infrastructure and phased-array antenna studies

The List of Companies - Satellite Antenna Market

Honeywell International

L3Harris Technologies

Northrop Grumman

Raytheon Technologies

Lockheed Martin

Airbus

Thales Group

Cobham Aerospace Communications

MDA Ltd.

Kymeta Corporation

Frequently Asked Questions

How big is the Satellite Antenna Market?

The Satellite Antenna Market is valued at US$ 4.56 Billion in 2025, it is projected to reach US$ 10.14 Billion by 2033.

What is the CAGR for Satellite Antenna Market by (2026 - 2033)?

As per our report Satellite Antenna Market, the market size is valued at US$ 4.56 Billion in 2025, projecting it to reach US$ 10.14 Billion by 2033. This translates to a CAGR of approximately 10.5% during the forecast period.

What segments are covered in this report?

The Satellite Antenna Market report typically cover these key segments-

Frequency Band (C Band, Ku/Ka Band, X Band, S and L Band, Others)

What is the historic period, base year, and forecast period taken for Satellite Antenna Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Satellite Antenna Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Satellite Antenna Market?

The Satellite Antenna Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Honeywell International

L3Harris Technologies

Northrop Grumman

Raytheon Technologies

Lockheed Martin

Airbus

Thales Group

Cobham Aerospace Communications

MDA Ltd.

Kymeta Corporation

Who should buy this report?

The Satellite Antenna Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Satellite Antenna Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Satellite Antenna Market

Get Free Sample For Satellite Antenna Market