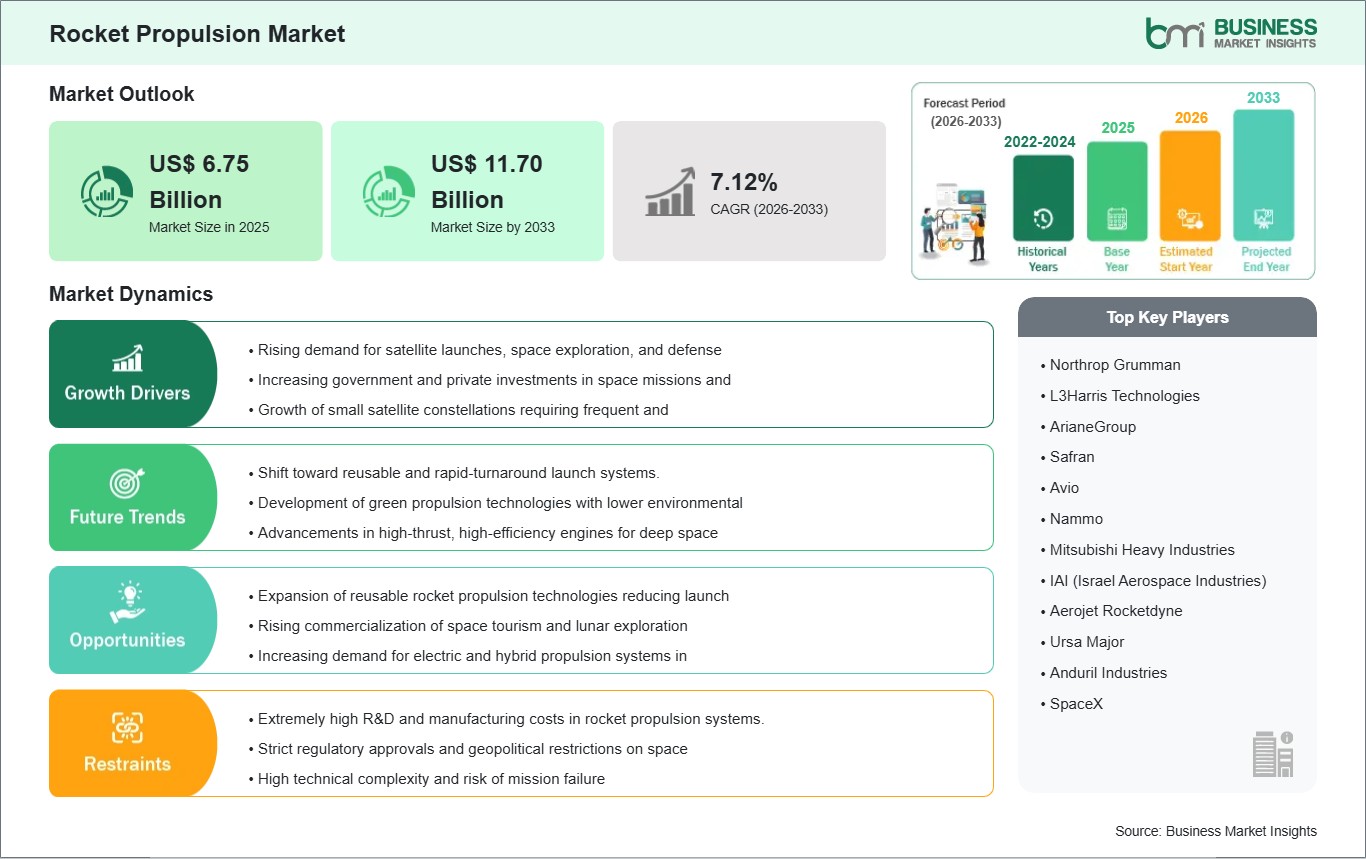

The rocket propulsion market size is expected to reach US$ 11.70 billion by 2033 from US$ 6.75 billion in 2025. The market is estimated to record a CAGR of 7.12% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Rocket propulsion systems generate thrust by expelling high-velocity gases through controlled combustion or propellant acceleration mechanisms. These systems form the operational foundation of launch vehicles, missile platforms, orbital missions, and deep-space transportation technologies. Propulsion architectures differ according to mission duration, payload requirements, maneuverability demands, and thermal performance conditions.

Expanding satellite deployment activity and heightened defense modernization programs continue strengthening procurement across propulsion technologies. Governments and commercial launch providers increasingly emphasize reusable systems, mission reliability, and propulsion efficiency to support evolving aerospace objectives. Strategic investments in hypersonic technologies and orbital mobility programs also reinforce long-term development initiatives throughout the sector.

Liquid propulsion systems maintain substantial utilization because controlled thrust modulation supports advanced launch and spacecraft maneuvering operations. Solid propulsion technologies remain central within tactical missile systems due to structural simplicity and operational readiness advantages. Hybrid propulsion concepts are attracting engineering interest for balancing safety characteristics with performance adaptability across emerging aerospace applications.

Technological progress increasingly centers on additive manufacturing, lightweight thermal-resistant materials, and reusable propulsion mechanisms. Advanced nozzle configurations, improved propellant chemistry, and precision combustion management systems are enhancing operational performance while reducing manufacturing complexity. Engineering attention additionally focuses on modular engine platforms capable of supporting both commercial launch programs and national security applications.

Competitive conditions within the market continue evolving through long-term aerospace contracts, propulsion testing programs, and integration partnerships. Industry participants concentrate on scalable manufacturing capability, rapid prototype validation, and propulsion reliability under demanding mission environments. Expanding commercialization of space activities and defense-oriented propulsion development continues shaping innovation priorities across the global rocket propulsion market.

Rocket Propulsion Market - Strategic Insights:

Get more information on this report

Rocket Propulsion Market Segmentation Analysis:

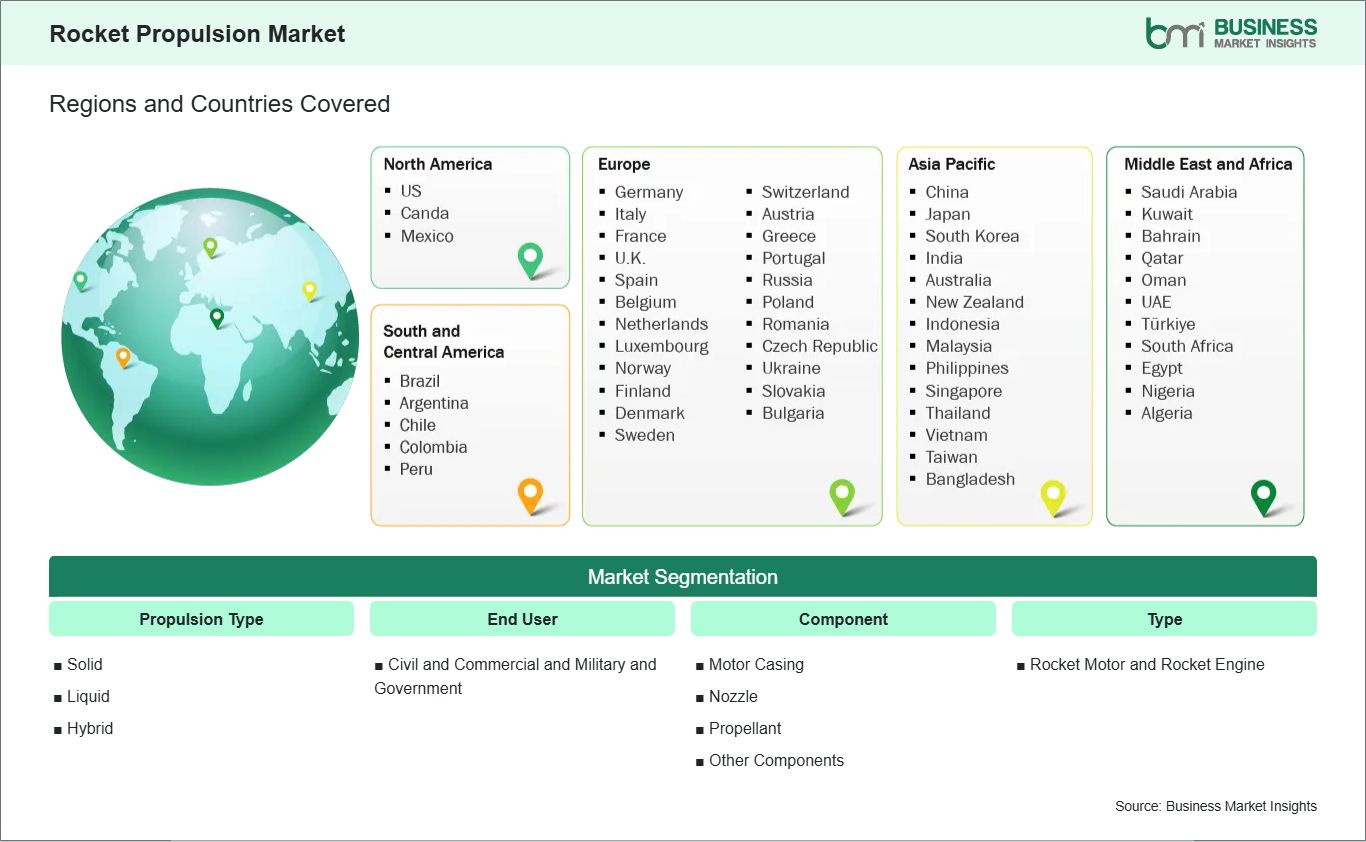

The rocket propulsion market is segmented based on propulsion type, end user, component and type-

By Propulsion Type

Solid – Supports rapid-launch military systems with simplified storage and operational durability.

Liquid – Enables controlled thrust regulation during orbital insertion and spacecraft maneuvering.

Other Components – Supports ignition, cooling, structural integration, and propulsion control functions.

By Type

Rocket Motor – Maintains suitability for tactical and short-duration propulsion applications.

Rocket Engine – Facilitates sustained propulsion control during complex aerospace missions.

Rocket Propulsion Market Drivers and Opportunities:

Expansion of Space Launch and Defense Programs

National space initiatives and orbital infrastructure projects continue accelerating propulsion system procurement worldwide. Launch providers and defense agencies require reliable propulsion technologies capable of supporting reusable vehicles, tactical missions, and satellite deployment operations. This requirement has increased engineering activity surrounding advanced rocket engines, improved propellant efficiency, and scalable propulsion manufacturing systems.

The broader impact extends across military modernization strategies and commercial aerospace investment planning. Governments increasingly prioritize propulsion independence and domestic manufacturing capability for strategic mission readiness. The relevance of high-performance propulsion systems has therefore intensified within national security programs, private launch services, and space exploration initiatives.

Emergence of Reusable and Advanced Propulsion Architectures

Propulsion innovation increasingly emphasizes reusable systems, additive manufacturing, and high-efficiency combustion technologies. Advanced engineering techniques are enabling lighter propulsion assemblies with improved thermal resilience and lower operational turnaround times. Hybrid configurations and electric-assisted propulsion concepts are additionally gaining technical attention for future orbital and interplanetary mission applications.

Future opportunities are linked with deep-space transportation, hypersonic systems, and responsive launch infrastructure. Aerospace organizations continue evaluating propulsion technologies capable of supporting frequent launches and long-duration missions with improved operational economics. Expanding commercial participation in lunar programs and satellite deployment activity is anticipated to strengthen industry potential over the forecast period

Rocket Propulsion Market Size and Share Analysis:

The Rocket Propulsion Market was valued at USD 6.75 Billion in 2025 and is projected to reach USD 11.70 Billion by 2033, expanding at a CAGR of 7.12% during 2026–2033. Market progression reflects sustained investment in launch vehicle technologies, missile propulsion systems, and advanced aerospace engineering infrastructure supporting commercial and defense-oriented missions.

Liquid propulsion technologies maintain notable industry presence because advanced aerospace missions require controlled thrust management and precision maneuverability. Rocket engines also hold considerable market positioning owing to their suitability for orbital transportation and reusable aerospace platforms.

Military and government applications represent a leading contribution area due to strategic demand for missile readiness and national defense modernization initiatives. Civil and commercial aerospace programs are also strengthening propulsion deployment through satellite launches, exploration missions, and private space transportation developments.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Northrop Grumman

L3Harris Technologies

ArianeGroup

Safran

Avio

Nammo

Mitsubishi Heavy Industries

IAI (Israel Aerospace Industries)

Aerojet Rocketdyne

Ursa Major

Anduril Industries

SpaceX

Blue Origin

Rocket Lab

Firefly Aerospace

Get more information on this report

Rocket Propulsion Market Report Coverage and Deliverables:

The Rocket Propulsion report provides a detailed analysis of the market covering the below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Rocket Propulsion Market Geographic Insights:

The Rocket Propulsion market shows diverse regional adoption patterns influenced by defense expenditure priorities, commercial launch activity, technological capabilities, and national space exploration agendas. Aerospace organizations worldwide continue allocating resources toward propulsion modernization programs supporting orbital transportation, missile readiness, and future deep-space mission capabilities.

North America demonstrates strong propulsion sector maturity supported by advanced aerospace manufacturing infrastructure and extensive government-backed space initiatives. Commercial launch providers and defense contractors across the region continue advancing reusable propulsion systems, hypersonic technologies, and strategic missile development programs. Research collaboration between public agencies and private aerospace enterprises also contributes to continuous propulsion technology refinement.

Asia Pacific reflects expanding propulsion development activity due to accelerating satellite deployment initiatives and indigenous aerospace manufacturing expansion. Regional governments continue strengthening launch vehicle programs and tactical missile capabilities to enhance strategic autonomy within aerospace operations. Commercial space ventures and state-backed propulsion research institutions are further contributing to broader technological advancement throughout the region.

Europe maintains a technologically specialized propulsion ecosystem emphasizing sustainable launch systems, precision engineering, and collaborative aerospace projects. Research institutions and aerospace manufacturers within the region continue focusing on advanced cryogenic engines and next-generation propulsion architectures for scientific and orbital applications. Emerging markets across the Middle East, Africa, and South and Central America are additionally exploring propulsion investments through defense partnerships and expanding space technology ambitions.

Get more information on this report

Rocket Propulsion Market Research Report Guidance:

The Rocket Propulsion market report encompasses both qualitative and quantitative data pertaining to the market, categorized by propulsion type, end user, component, type and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 11 analyze market segments based on propulsion type, end user, component, type, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 12 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 13 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 14, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 15, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Rocket Propulsion Market News and Key Development:

The Rocket Propulsion market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In June 2026, Private equity firm EQT acquired Exolaunch, a major satellite launch integrator supporting SpaceX rideshare missions.

In March2026, GE Aerospace announced a $1 billion investment in US manufacturing, including propulsion engine components for aerospace and defense applications.

Key Sources Referred:

Aerospace propulsion industry reportsGovernment aerospace and defense databasesSpace technology academic journalsAerospace engineering research publicationsCompany annual reports and technical filingsDefense modernization policy documentsSatellite launch and propulsion development studiesAdvanced manufacturing and propulsion materials research papers

The List of Companies - Rocket Propulsion Market

Northrop Grumman

L3Harris Technologies

ArianeGroup

Safran

Avio

Nammo

Mitsubishi Heavy Industries

IAI (Israel Aerospace Industries)

Aerojet Rocketdyne

Ursa Major

Anduril Industries

SpaceX

Blue Origin

Rocket Lab

Firefly Aerospace

Agnikul Cosmos

Skyroot Aerospace

Bharat Dynamics Limited (BDL)

Hanwha Aerospace

China Aerospace Science and Technology Corporation (CASC)

Frequently Asked Questions

How big is the Rocket Propulsion Market?

The Rocket Propulsion Market is valued at US$ 6.75 Billion in 2025, it is projected to reach US$ 11.70 Billion by 2033.

What is the CAGR for Rocket Propulsion Market by (2026 - 2033)?

As per our report Rocket Propulsion Market, the market size is valued at US$ 6.75 Billion in 2025, projecting it to reach US$ 11.70 Billion by 2033. This translates to a CAGR of approximately 7.12% during the forecast period.

What segments are covered in this report?

The Rocket Propulsion Market report typically cover these key segments-

Propulsion Type (Solid, Liquid, and Hybrid)

End User (Civil and Commercial and Military and Government)

Component (Motor Casing, Nozzle, Propellant, and Other Components)

Type (Rocket Motor and Rocket Engine)

What is the historic period, base year, and forecast period taken for Rocket Propulsion Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Rocket Propulsion Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Rocket Propulsion Market?

The Rocket Propulsion Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Northrop Grumman

L3Harris Technologies

ArianeGroup

Safran

Avio

Nammo

Mitsubishi Heavy Industries

IAI (Israel Aerospace Industries)

Aerojet Rocketdyne

Ursa Major

Anduril Industries

SpaceX

Blue Origin

Rocket Lab

Firefly Aerospace

Agnikul Cosmos

Skyroot Aerospace

Bharat Dynamics Limited (BDL)

Hanwha Aerospace

China Aerospace Science and Technology Corporation (CASC)

Who should buy this report?

The Rocket Propulsion Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Rocket Propulsion Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Rocket Propulsion Market

Get Free Sample For Rocket Propulsion Market