01

Market Summery

Executive Summary and Global Market Analysis

Robotic palletizers are automated material-handling systems designed to organize, stack, and transfer packaged goods onto pallets through programmable robotic mechanisms. These systems combine robotic arms, gripping tools, motion control technologies, and intelligent software to improve warehouse throughput and production consistency. Their deployment has expanded across manufacturing and distribution facilities seeking operational precision and reduced manual handling requirements.

Industrial facilities increasingly integrate robotic palletizers to streamline repetitive end-of-line operations under demanding production schedules. Rising pressure to minimize workplace injuries, maintain packaging accuracy, and support uninterrupted logistics activity continues to influence purchasing decisions. Automated palletizing solutions also support flexible production environments where packaging configurations frequently change across multiple product categories.

The market demonstrates broad applicability across food and beverages, pharmaceuticals, chemicals, and retail distribution environments. Traditional industrial robots maintain substantial deployment across high-volume operations due to their durability and payload capacity. Collaborative robots continue gaining commercial attention because compact facilities prioritize adaptable automation systems with easier integration requirements and simplified operator interaction.

Technology development within this sector increasingly emphasizes machine vision, AI-enabled motion planning, and intelligent gripper systems. Manufacturers are refining EOAT configurations to support mixed-package palletizing and irregular load handling. Software-driven monitoring tools additionally improve operational visibility by enabling predictive maintenance, real-time diagnostics, and centralized production management across automated packaging lines.

Competitive conditions remain shaped by product innovation, customization capability, and integration expertise. Market participants focus on scalable robotic platforms capable of supporting varied industrial layouts and packaging specifications. Strategic emphasis on warehouse automation, flexible manufacturing, and digital production infrastructure continues to reinforce long-term investment activity across the robotic palletizer market.

03

Segment Analysis

Robotic Palletizer Market Segmentation

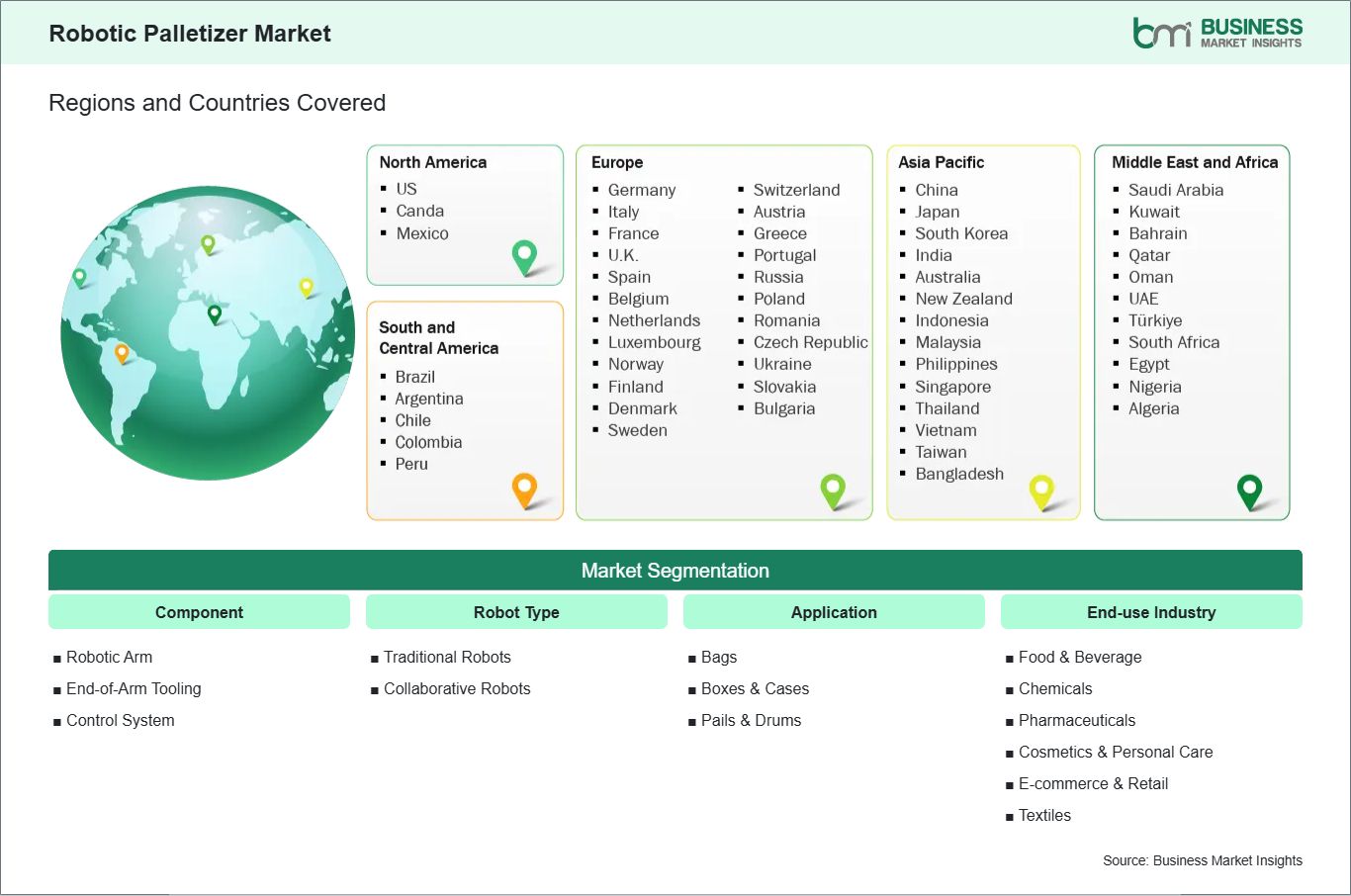

The robotic palletizer market is segmented based on component, robot type, payload capacity and end use industry.

By Component

- Robotic Arm: Enables high-speed handling with repeatable precision across palletizing cycles.

- End-of-Arm Tooling (EOAT): Supports adaptable gripping for cartons, bags, containers, and mixed loads.

- Control System: Coordinates motion accuracy, sensing functions, and operational synchronization.

By Robot Type

- Traditional Industrial Robots – Preferred for intensive production environments requiring continuous heavy-load movement.

- Collaborative Robots – Expanding deployment within compact facilities emphasizing operator interaction and flexibility.

By Payload Capacity

- Upto 1000 kg – Suitable for lightweight consumer goods and compact logistics operations.

- 1000 to 2000 kg – Balances operational efficiency with medium-scale industrial packaging demands.

- More than 2000 kg – Supports bulk material industries with extensive pallet handling requirements.

By End-use Industry

- Food and Beverages – Maintains consistent product stacking under hygiene-focused production conditions.

- Chemicals – Enhances handling safety for industrial containers and hazardous packaging materials.

- Pharmaceuticals – Improves accuracy in regulated packaging and warehouse distribution processes.

- Cosmetics and Personal Care – Facilitates organized pallet formation for diverse packaging formats.

- E-commerce and Retail – Accelerates order movement across fast-paced fulfillment operations.

- Others – Addresses customized palletizing requirements across specialized manufacturing sectors.

04

Market Forces

Robotic Palletizer Market Drivers and Opportunities

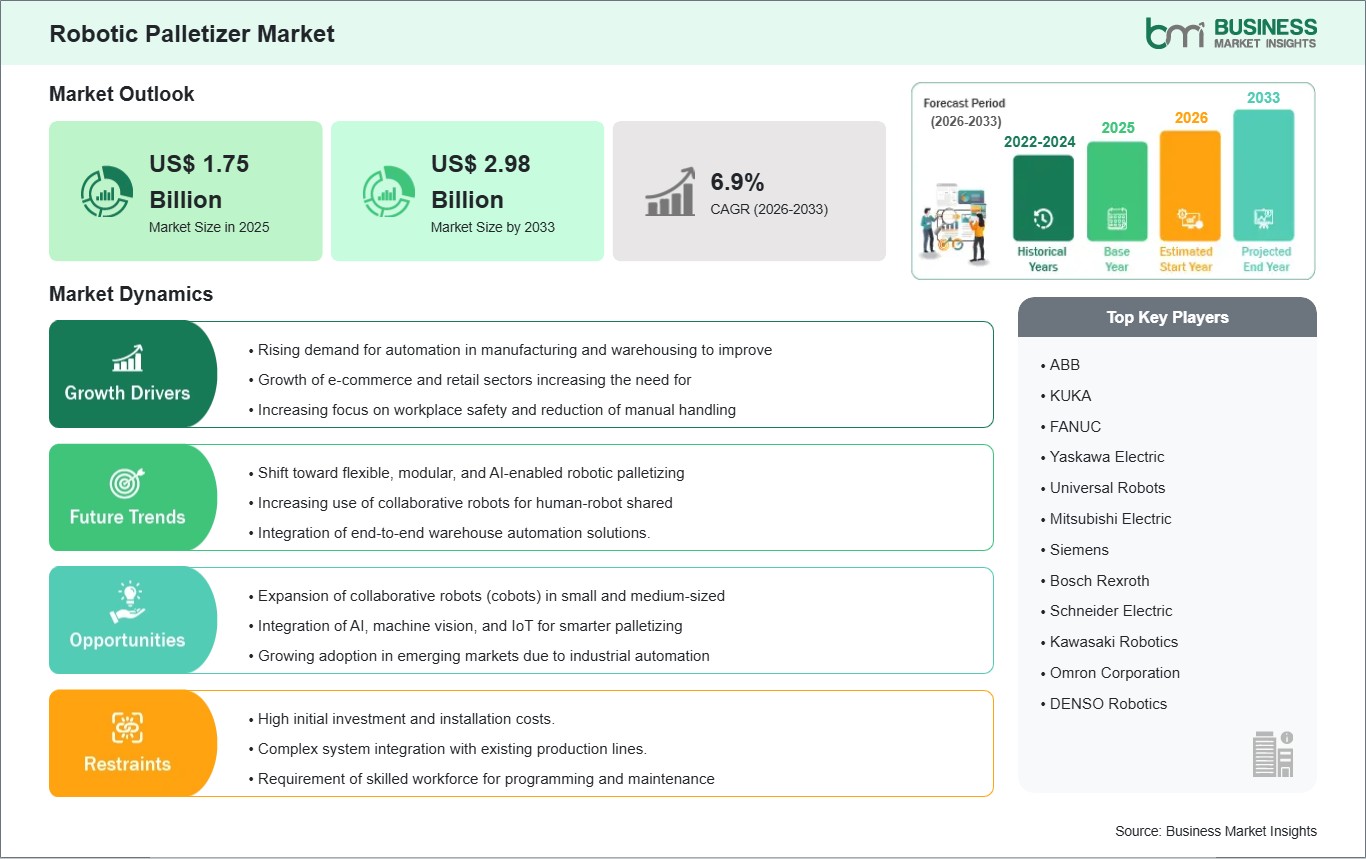

Rising Automation Across Warehousing and Manufacturing Operations

Manufacturing companies increasingly automate material-handling activities to improve throughput consistency and labor utilization efficiency. Manual palletizing operations often create workflow bottlenecks, ergonomic risks, and packaging inaccuracies during continuous production cycles. Robotic palletizers address these operational limitations through programmable handling precision, uninterrupted operation, and reduced dependency on labor-intensive packaging tasks.

The operational impact extends beyond productivity enhancement into logistics optimization and facility standardization. Enterprises managing multi-location manufacturing networks prioritize automated palletizing systems capable of maintaining uniform packaging output. This relevance has strengthened as industries seek scalable production infrastructure supporting evolving warehousing models and diversified distribution requirements.

Expansion of Intelligent and Collaborative Palletizing Systems

Developments in collaborative robotics, machine vision, and smart sensing technologies are reshaping palletizing system capabilities. Compact collaborative systems now support flexible installation within facilities handling multiple packaging formats and frequent product changeovers. Intelligent EOAT solutions additionally improve gripping adaptability across mixed products, enabling broader industrial implementation beyond high-volume applications.

Future opportunities are emerging through integrated warehouse automation and connected manufacturing ecosystems. Businesses increasingly evaluate robotic palletizers as part of broader digital transformation initiatives incorporating analytics, predictive maintenance, and centralized production monitoring. Expanding deployment within e-commerce distribution centers and mid-scale industrial facilities is expected to reinforce long-term sector expansion.

05

Size and Share Analysis

Robotic Palletizer Market Size and Share Analysis

The Robotic Palletizer Market was valued at USD 1.75 Billion in 2025 and is projected to reach USD 2.98 Billion by 2033, expanding at a CAGR of 6.90% during 2026–2033. Market progression reflects stronger industrial preference for automated material-handling systems capable of supporting continuous production efficiency and packaging consistency across large-scale operational environments.

Traditional industrial robots maintain a prominent market position due to their reliability in repetitive heavy-duty applications. Robotic arms and advanced control systems continue attracting investment because industrial operators prioritize precision handling, operational durability, and compatibility with integrated production infrastructure.

Food and beverages represent a leading application area owing to extensive packaging volume and strict operational efficiency requirements. E-commerce and retail facilities also demonstrate expanding deployment as distribution centers modernize pallet handling activities to support faster inventory movement and organized warehouse workflows.

07

Report Coverage

Robotic Palletizer Market Report Coverage and Deliverables

The Robotic Palletizer report provides a detailed analysis of the market covering the below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Robotic Palletizer Market Geographic Insights

The Robotic Palletizer market shows diverse regional adoption patterns influenced by industrial automation priorities, manufacturing intensity, labor structures, and logistics modernization strategies. Global implementation activity continues advancing as enterprises seek efficient pallet handling systems capable of supporting high-output production environments and digitally connected warehouse operations.

North America demonstrates strong commercialization potential due to extensive warehouse automation investment and established industrial robotics infrastructure. Food processing, pharmaceutical manufacturing, and retail distribution facilities across the region increasingly utilize robotic palletizers to improve operational continuity and packaging precision. Demand for collaborative palletizing systems also remains notable among medium-sized manufacturers pursuing flexible automation strategies.

Asia Pacific reflects broad industrial momentum supported by expanding manufacturing activity and accelerating logistics development. Industrial operators across regional production hubs continue incorporating robotic palletizers into packaging lines to strengthen throughput efficiency and reduce labor-intensive handling practices. E-commerce expansion and factory modernization initiatives further reinforce automation deployment within regional warehousing and fulfillment facilities.

Europe maintains steady market progression through emphasis on industrial efficiency, worker safety, and advanced production engineering capabilities. Manufacturers throughout the region prioritize intelligent palletizing systems integrated with smart factory environments and digital process management tools. Emerging markets across the Middle East, Africa, and South and Central America are additionally witnessing gradual deployment growth as industrial facilities modernize operational infrastructure and warehouse automation capabilities.

10

Industry Activity

Recent Developments

The Robotic Palletizer market market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- In September 2025, Sidel Cermex strengthened its end-of-line automation portfolio with upgraded robotic palletizing systems and integrated case-handling solutions.

- In December 2025, KUKA expanded its industrial robotics lineup used in palletizing applications across food, beverage, and building materials industries.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Industry automation and robotics reports Government manufacturing and industrial production databases Warehouse automation and logistics publications Academic journals related to industrial robotics Company annual reports and regulatory filings Packaging technology and smart manufacturing studies Trade association publications on material handling systems Industrial engineering and production optimization research papers