01

Market Summery

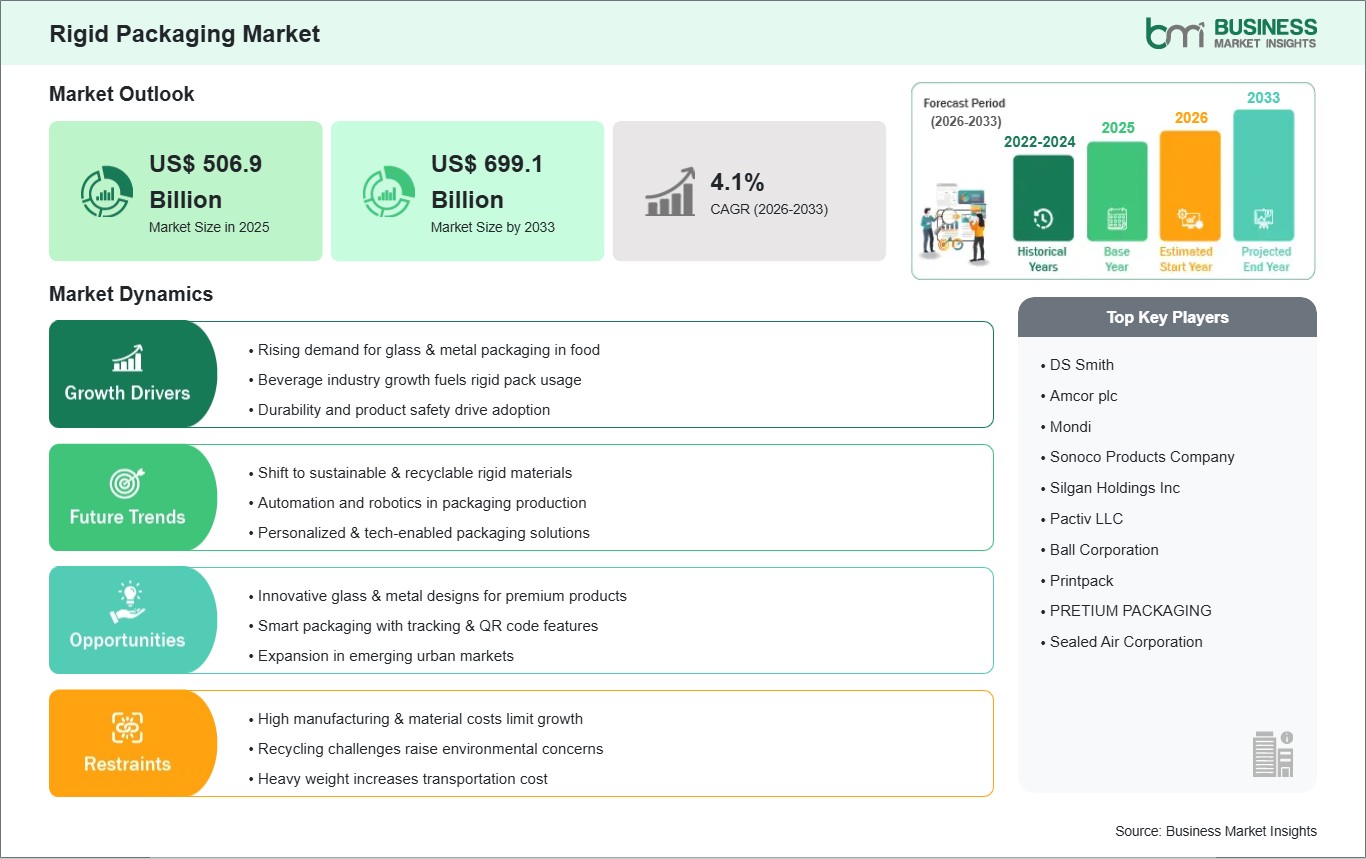

Executive Summary and Global Market Analysis

Rigid Packaging serves as the primary structural and protective framework for global product distribution, encompassing bottles, jars, cans, trays, and tubs. These formats offer distinct advantages, including high impact resistance, excellent barrier properties against oxygen and moisture, and the ability to support heavy stack loads in automated warehouses. Growth is fueled by the burgeoning demand for packaged food and beverages, the critical need for tamper-evident pharmaceutical packaging, and the rapid expansion of modern retail infrastructure in emerging economies. Additionally, the shift toward monomaterial designs (such as all-PET or all-PP containers) is fundamentally enhancing the recyclability of rigid formats to meet circular economy mandates.

However, several challenges can restrain market growth: high production costs and energy intensity, particularly for glass and metal manufacturing, remain a significant barrier compared to flexible alternatives. Stringent global regulations on plastic waste and the phasing out of non-recyclable multi-layer rigid structures pose constant compliance hurdles for manufacturers. Furthermore, the industry faces constraints due to volatile raw material prices for petroleum-based resins and the increasing consumer preference for lightweight, lower-carbon footprint packaging solutions. Despite these hurdles, the market holds immense opportunities as a result of the universal mandate for sustainable materials, the accelerating deployment of Refill-at-Home and returnable packaging systems, and the increasing reliance on Smart Packaging with integrated RFID/IoT for real-time supply chain tracking. The transition toward chemically recycled resins and bio-based rigid polymers (such as PEF) is expected to create significant opportunities for market growth.

03

Segment Analysis

Rigid Packaging Market Segmentation

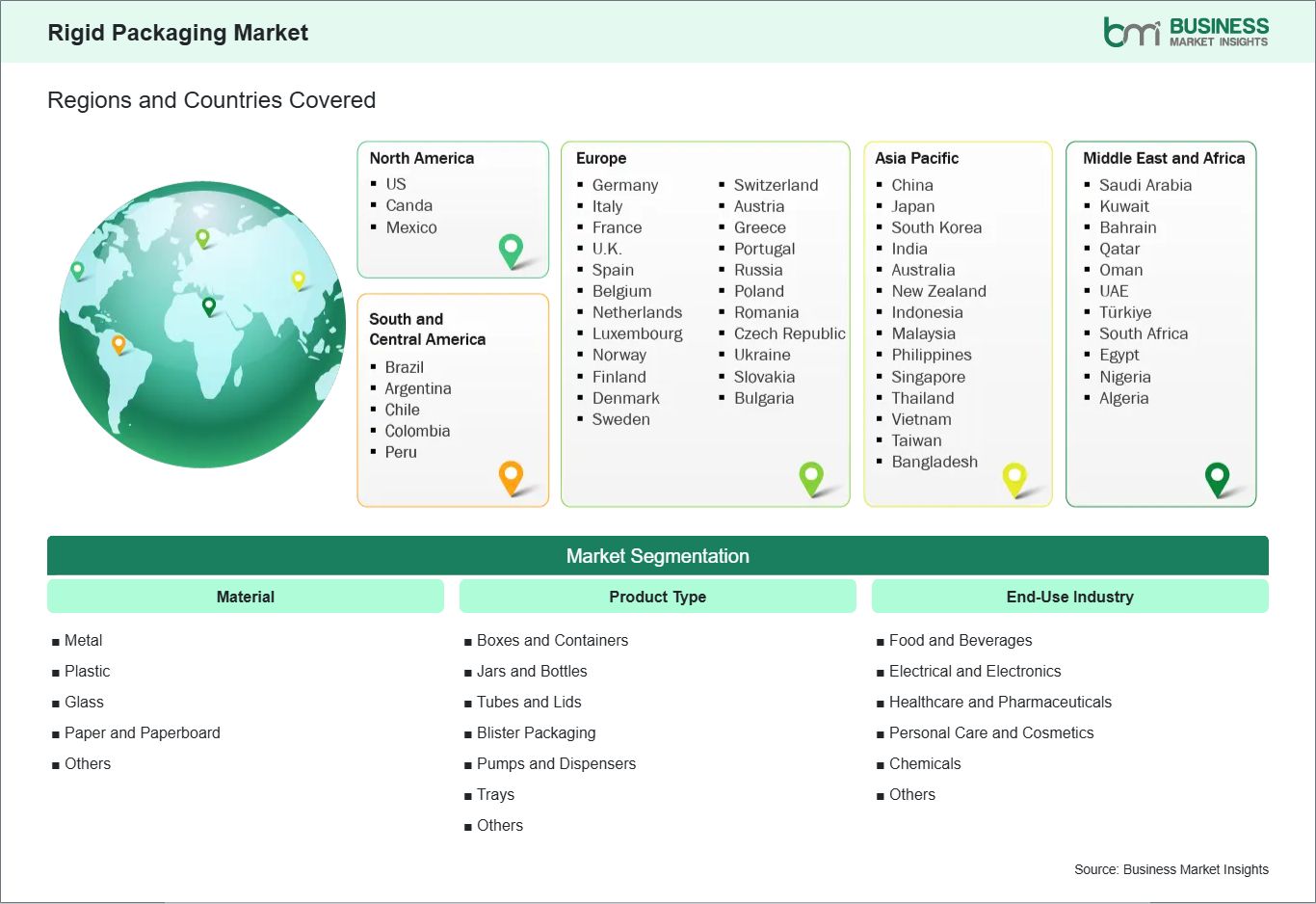

Key segments that contributed to the derivation of the Rigid Packaging market analysis are material, product type, and end-use industry.

- By Material, the market is segmented into Metal, Plastic, Glass, Paper, Paperboard, and Others.

- By Product Type, the market is segmented into Boxes and Containers, Jars and Bottles, Tubes and Lids, Blister Packaging, Pumps and Dispensers, Trays, and Others.

- By End-Use Industry, the market is segmented into Food and Beverages, Electrical and Electronics, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Chemicals, and Others.

04

Market Forces

Rigid Packaging Market Drivers and Opportunities

Product Protection and Consumer Convenience

Rigid packaging formats—such as bottles, jars, and cans—offer a sturdy and dependable physical barrier that safeguards sensitive products from impact, pressure fluctuations, and environmental contamination during long-distance transportation. This durability has become increasingly important as the e-commerce sector grows, exposing goods to numerous handling stages, automated sorting systems, and varied shipping conditions before they reach the end consumer. Beyond protection, evolving consumer lifestyles are driving a substantial rise in the demand for convenient, easy-to-use, and portion-controlled packaging solutions. Features like resealable lids, stackable geometries, ergonomic grips, and tamper-evident closures appeal to today’s busy, mobile population, particularly as ready-to-eat meals, meal kits, and single-serve products gain popularity. In addition, rapid urbanization and rising disposable incomes in emerging markets are strengthening the preference for premium, durable, and aesthetically appealing packaging that enhances product value and fits easily into compact living spaces. These combined factors ensure that rigid packaging formats continue to maintain a strong competitive edge and remain a dominant force within the global retail and distribution landscape.

Sustainability Transitions and Smart Integration

A significant high-value opportunity lies in the dual evolution of material circularity and intelligent packaging technology. With global regulatory frameworks increasingly penalizing single-use waste, there is a burgeoning market for rigid solutions made from 100% post-consumer recycled (PCR) content, bio-plastics, and "infinite" materials like glass and aluminum. Manufacturers can gain a competitive edge by developing "refill-at-home" systems, where a durable, rigid container is reused multiple times with concentrated refills. Furthermore, the integration of Smart Packaging features, such as NFC chips and time-temperature indicators, offers a major opportunity in the pharmaceutical and luxury goods segments. These technologies allow for real-time tracking, anti-counterfeiting verification, and digital consumer engagement. By investing in advanced molding techniques that allow for "light-weighting" without sacrificing strength, companies can meet environmental goals while reducing material costs. The shift toward a more circular and connected ecosystem positions rigid packaging as a key enabler of modern, sustainable brand experiences.

05

Size and Share Analysis

Rigid Packaging Market Size and Share Analysis

The Rigid Packaging market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within material, product type, and end-use industry, offering insights into their contribution to overall market performance.

For instance, the Plastic subsegment is a significant focus for development, particularly when utilized for Jars and Bottles. This combination is essential for the Food and Beverages sector, where durability and moisture resistance are paramount. A major trend in this area is the increased use of high-density polyethylene (HDPE) and recycled PET (rPET) to satisfy corporate sustainability mandates. By using rigid plastic containers, beverage manufacturers can maintain structural integrity during high-speed filling and long-distance transport.

07

Report Coverage

Rigid Packaging Market Report Coverage and Deliverables

The "Rigid Packaging Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Rigid Packaging market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Rigid Packaging market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Rigid Packaging market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Rigid Packaging market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Rigid Packaging Market Geographic Insights

The geographical scope of the Rigid Packaging market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Rigid Packaging Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by the region's massive food and beverage sector and a booming pharmaceutical industry. Growth is further bolstered by the rapid expansion of e-commerce and the rising demand for rigid plastic bottles, cans, and jars that ensure product safety during long-distance transit. The shift toward a circular economy, marked by the adoption of recycled PET (rPET) and bioplastics to meet evolving environmental regulations in Japan and Australia, ensures that Asia Pacific remains at the forefront of rigid packaging innovation.

10

Industry Activity

Recent Developments

The Rigid Packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Rigid Packaging market are:

- In March 2025, LyondellBasell, a leader in the global chemical industry, announced the launch of Pro-fax EP649U, a new polypropylene impact copolymer designed for the rigid packaging market. This innovative product is specifically formulated for thin-walled injection molding, making it ideal for food packaging applications.

- In April 2024, Amcor, a global leader in developing and producing responsible packaging solutions, announced of launching a one-liter polyethylene terephthalate (PET) bottle for carbonated soft drink (CSD) use that is made from 100% post-consumer recycled (PCR) content. This first-of-its-kind stock option will support customers as they strive to meet sustainability commitments and requirements. As the industry leader in packaging innovation, Amcor Rigid Packaging (ARP) is adding this one-litre CSD 100% PCR bottle to an expanding stock portfolio of responsible packaging made from recycled content.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade Indicators

World Trade Organization (WTO)

International Monetary Fund (IMF)

International Trade Administration (ITA)

Company Websites

Company Annual Reports

Company Investor Presentations