01

Market Summery

Executive Summary and Global Market Analysis

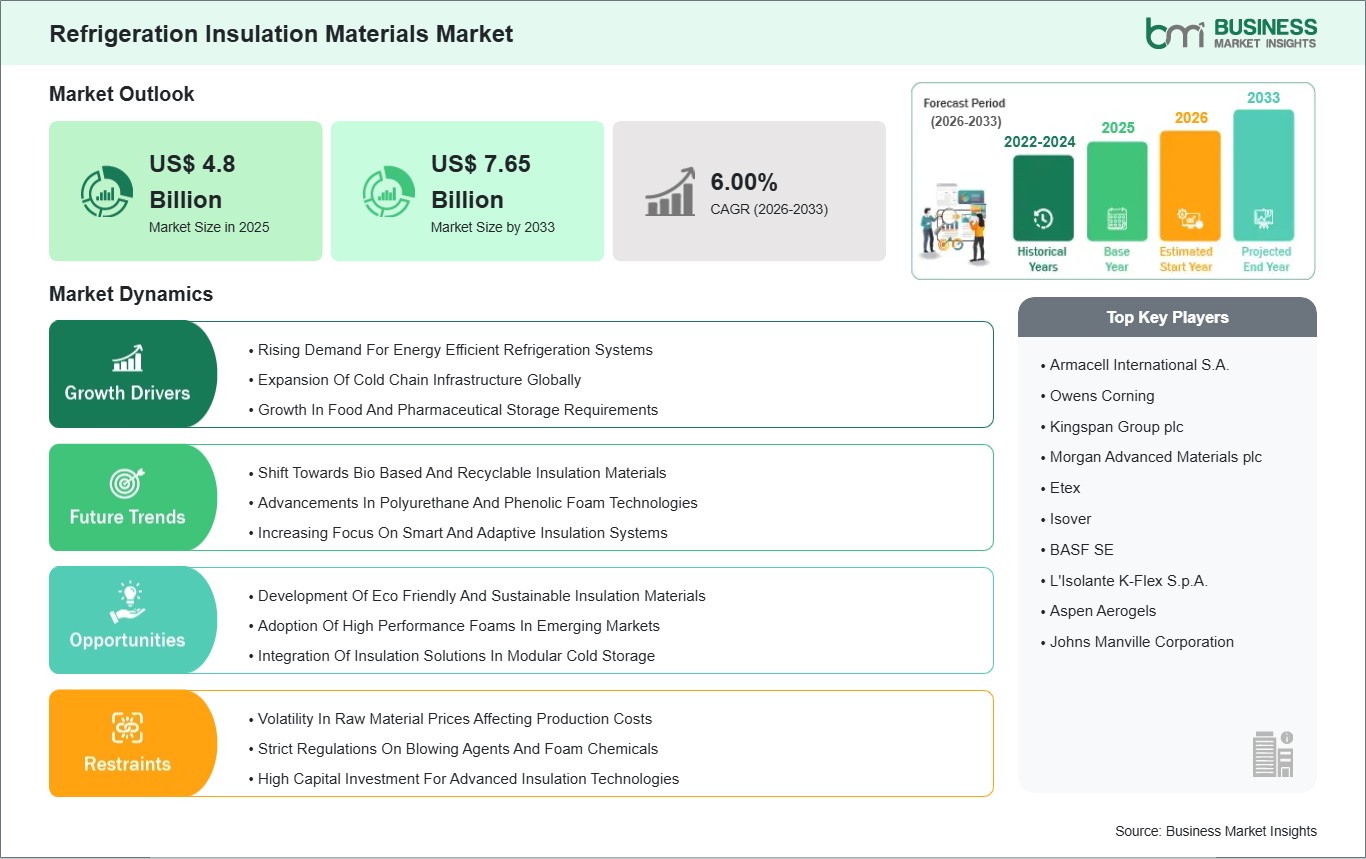

The global refrigeration insulation materials market is influenced by the growing requirement for energy-efficient thermal management products in a wide range of refrigeration applications. The role of insulation materials like polyurethane foam (PUR/PIR), extruded polystyrene (XPS), expanded polystyrene (EPS), and phenolic foam is vital in cold infrastructure, commercial refrigeration systems, industrial freezers, and domestic refrigeration products. Sustainability and energy saving are the new buzzwords in the regulatory and corporate world across the globe, and the need for energy-efficient insulation products is the need of the hour. The need for energy-efficient thermal management products is visible in the global market, especially in regions that have set energy-efficient standards and are committed to reducing greenhouse gas emissions and saving the environment.

The driving force behind the global market is the growing cold infrastructure, particularly in the food and pharmaceutical industries. The need for effective insulation, which can ensure consistent temperatures during storage and transportation, has thus been heightened by the increasing global need for fresh and frozen food products, as well as the rise of pharmaceutical and vaccine products. As cold chain infrastructure continues to develop in the market, products with enhanced thermal resistance, structural strength, and moisture management capabilities are increasingly desired. On the other hand, the need for high-performance refrigeration systems with optimized insulation capabilities is also being felt in the residential and commercial sectors, driven by the need to provide end-users with lower energy bills and longer product lifetimes.

However, the market is currently being threatened by fluctuations in raw material prices and changes in regulations. The prices of fundamental polymeric materials, as well as changes in regulations with respect to blowing agents and foam chemistries, have forced manufacturers to develop new products or reformulate existing products without compromising their insulation capabilities. Furthermore, the need to balance cost competitiveness with performance considerations will remain a key driver for material selection, especially for price-sensitive markets. However, the ongoing drive for materials engineering and the development of bio-based and recyclable materials for insulation will provide end users with a wider range of options. Overall, the global refrigeration insulation materials market is driven by the need for energy efficiency, expansion of the industry, and the development of materials.

03

Segment Analysis

Refrigeration Insulation Materials Market Segmentation

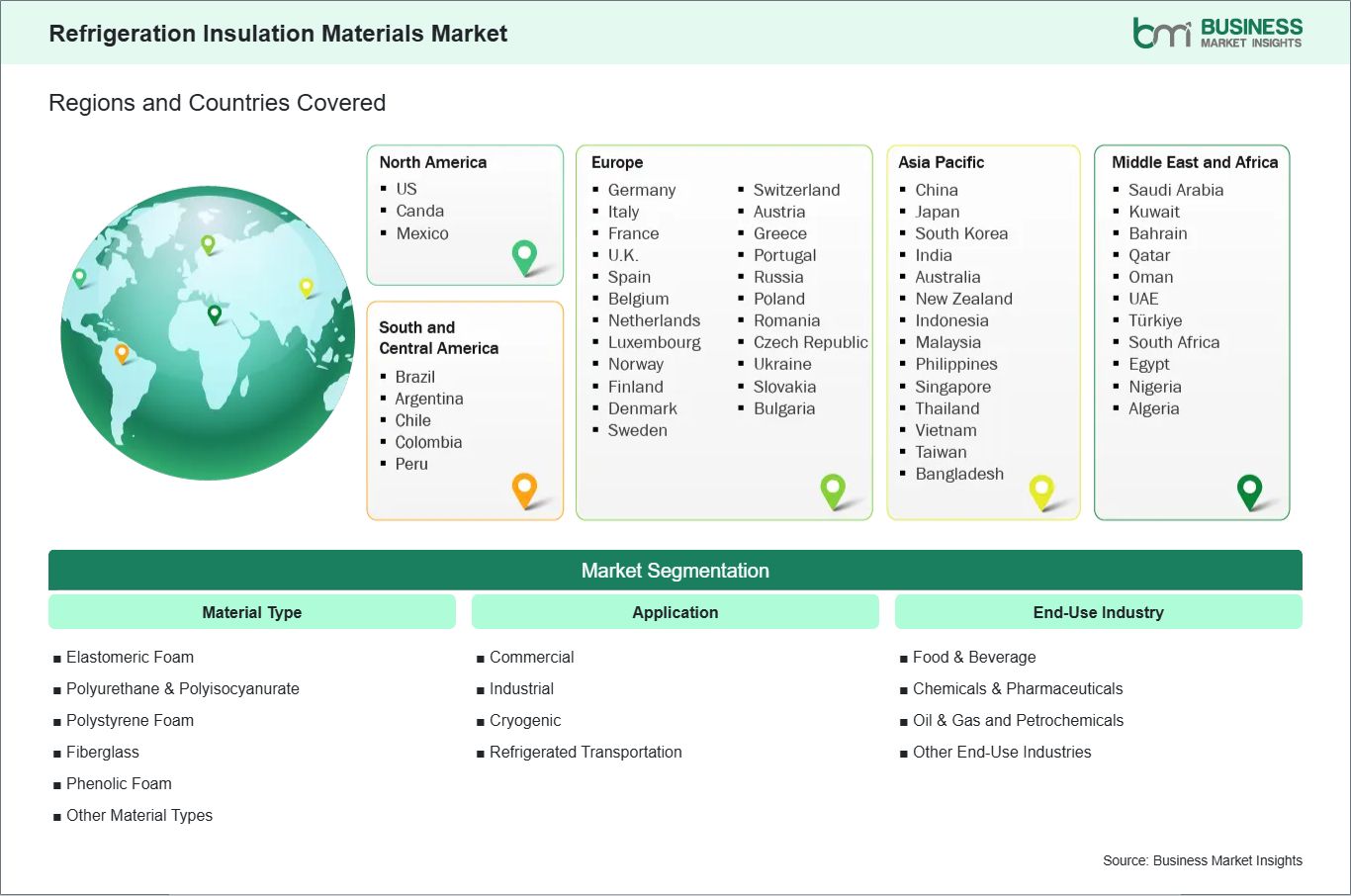

Key segments that contributed to the derivation of the refrigeration insulation materials market analysis are material type, application, and end‑use industry.

- By material type, the refrigeration insulation materials market is segmented into elastomeric foam, polyurethane & polyisocyanurate (PU & PIR), polystyrene foam, fiberglass, phenolic foam, other material types. The PU & PIR segment dominated the market in 2025.

- Based on application, the refrigeration insulation materials market is categorized into commercial, industrial, cryogenic, refrigerated transportation. The commercial segment dominated the market in 2025.

- In terms of end‑use industry, the refrigeration insulation materials market is categorized into food & beverage, chemicals & pharmaceuticals, oil & gas and petrochemicals, other end‑use industries. The food & beverage segment dominated the market in 2025.

04

Market Forces

Refrigeration Insulation Materials Market Drivers and Opportunities

Rising Demand For Energy Efficient Refrigeration Systems

The drive toward energy efficiency is one of the most influential forces shaping the global refrigeration insulation materials market. As governments and industry stakeholders intensify efforts to reduce carbon footprints and operational energy costs, the demand for superior insulation in refrigeration equipment has grown substantially. Energy‑efficient systems depend on advanced insulation materials that minimize thermal transfer, improve system performance, and reduce power consumption over the product lifecycle. In developed markets like North America and Europe, stringent energy regulations and building codes have accelerated the uptake of high‑performance insulations such as polyurethane and phenolic foams, which offer excellent thermal resistance.

Utilities and commercial operators also prefer these materials to achieve long‑term savings and compliance with evolving legislative requirements. In emerging economies across Asia Pacific and Latin America, rapid expansion of the cold chain — driven by food retail modernization and expanding pharmaceutical logistics has similarly boosted demand for energy‑efficient refrigeration. Insulation plays a crucial role in maintaining optimal temperatures in cold storage warehouses, refrigerated transport, and retail display units. Manufacturers in these regions are balancing cost considerations with performance expectations, leading to rising adoption of materials such as extruded polystyrene and advanced polymer blends that offer improved insulation without excessive cost increases.

Development Of Eco Friendly And Sustainable Insulation Materials

Sustainability has emerged as a key trend within the global refrigeration insulation materials market, as manufacturers, regulators, and end users seek alternatives that reduce environmental impact without compromising performance. Traditional foam insulations have relied on blowing agents and chemical processes with high global warming potential, prompting industry focus on greener formulations. Bio‑based polyols, recyclable foams, and materials with reduced emissions profiles are gaining traction, particularly in regions with ambitious emissions reduction targets such as the European Union and parts of North America. These eco‑friendly alternatives are being integrated into commercial and industrial refrigeration systems to align product lifecycles with broader sustainability goals, including circular economy principles.

The development of sustainable insulation materials also reflects evolving consumer preferences, especially in residential and commercial applications where energy labels and eco‑certifications influence purchasing decisions. End users increasingly demand refrigeration units that not only consume less energy but also use construction materials with lower environmental footprints. Manufacturers that pioneer recyclable and low‑impact insulation solutions are better positioned to capture market share, as sustainability becomes a competitive differentiator in global markets. Overall, the shift toward eco‑friendly insulation materials is expanding the technological horizon of the refrigeration industry while contributing to global energy and environmental objectives.

05

Size and Share Analysis

Refrigeration Insulation Materials Market Size and Share Analysis

The refrigeration insulation materials market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within material type, application, and end‑use industry, offering insights into their contribution to overall market performance.

By material type, the PU & PIR subsegment dominated the market in 2025, driven by their excellent thermal insulation properties and widespread use in refrigeration systems.

Based on application, the commercial subsegment dominated the market in 2025, driven by high demand from retail refrigeration and cold-storage facilities.

In terms of end‑use industry, the food & beverage subsegment dominated the market in 2025, driven by the need for effective cold-chain storage and preservation of perishable products.

07

Report Coverage

Refrigeration Insulation Materials Market Report Coverage and Deliverables

The "Refrigeration Insulation Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Refrigeration Insulation Materials Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Refrigeration Insulation Materials Market trends, as well as drivers, restraints, and opportunities

- Refrigeration Insulation Materials Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Refrigeration Insulation Materials Market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Refrigeration Insulation Materials Market Geographic Insights

The geographical scope of the Refrigeration Insulation Materials Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America has become the primary region in the global refrigeration insulation materials market because it possesses advanced cold chain infrastructure and enforces strict energy efficiency standards and operates multiple end-use industries. The United States and Canada use refrigeration insulation materials like high-density polyurethane foam and phenolic foam to meet regulatory requirements and sustainability goals which decrease energy expenses in commercial refrigeration systems and industrial cold storage warehouses and transport refrigeration units. The food retail sector maintains strong growth while pharmaceutical and biotech distribution networks expand thus creating a need for insulation systems that maintain temperature control during both storage and transportation.

The Asia Pacific market experiences rapid growth because industrialization and urbanization together with cold chain logistics development drive economic progress in major countries such as China India Japan and South Korea. The increasing demand for fresh and frozen food products together with rising grocery retail infrastructure investments and government storage facility modernization initiatives drive insulation material consumption which includes extruded polystyrene and advanced polymer foams. Europe remains strong in this segment, backed by stringent thermal performance standards, sustainability drives, and high penetration rates for energy-efficient refrigeration equipment in Germany, France, the UK, and Nordic countries. European insulation material suppliers also focus on providing eco-friendly insulation materials that are in sync with the concept of circular economy. Middle East & Africa: Market growth is emerging in this region, backed by investments in industrial refrigeration equipment for petrochemical, food processing, and logistics industries.

However, reliance on imported insulation compounds is also seen in this region. South & Central America: Demand for insulation materials is steady in this region, backed by strong demand from Brazil and Mexico. The growth in food retail and cold storage facilities in these countries is driving demand for efficient insulation materials, along with rising awareness about energy-saving refrigeration equipment.

10

Industry Activity

Recent Developments

The Refrigeration Insulation Materials Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the refrigeration insulation materials market are:

- In June 2025, Armacell announced that it had opened a new aerogel insulation production plant in Pune, India, where it will manufacture its ArmaGel XG product line. This expansion significantly increases Armacell`s manufacturing capacity for high‑performance insulation materials suited for cryogenic and dual‑temperature applications, reinforcing its ability to serve global refrigeration and industrial markets with advanced insulation solutions.

- In October 2024, BASF SE announced the expansion of production capacity for its Neopor® expandable polystyrene (EPS) insulation material at its Ludwigshafen site, increasing annual output by 50,000 metric tons to better meet demand for energy‑efficient insulation applications. While Neopor® primarily targets building insulation, the expanded production reflects BASF`s broader commitment to supplying advanced insulation materials — including those relevant to energy‑efficient refrigeration systems.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Health Organization (WHO) Organisation for Economic Cooperation and Development (OECD) The World Bank Group Worldometer The Lancet International Bar Association International Trade Administration