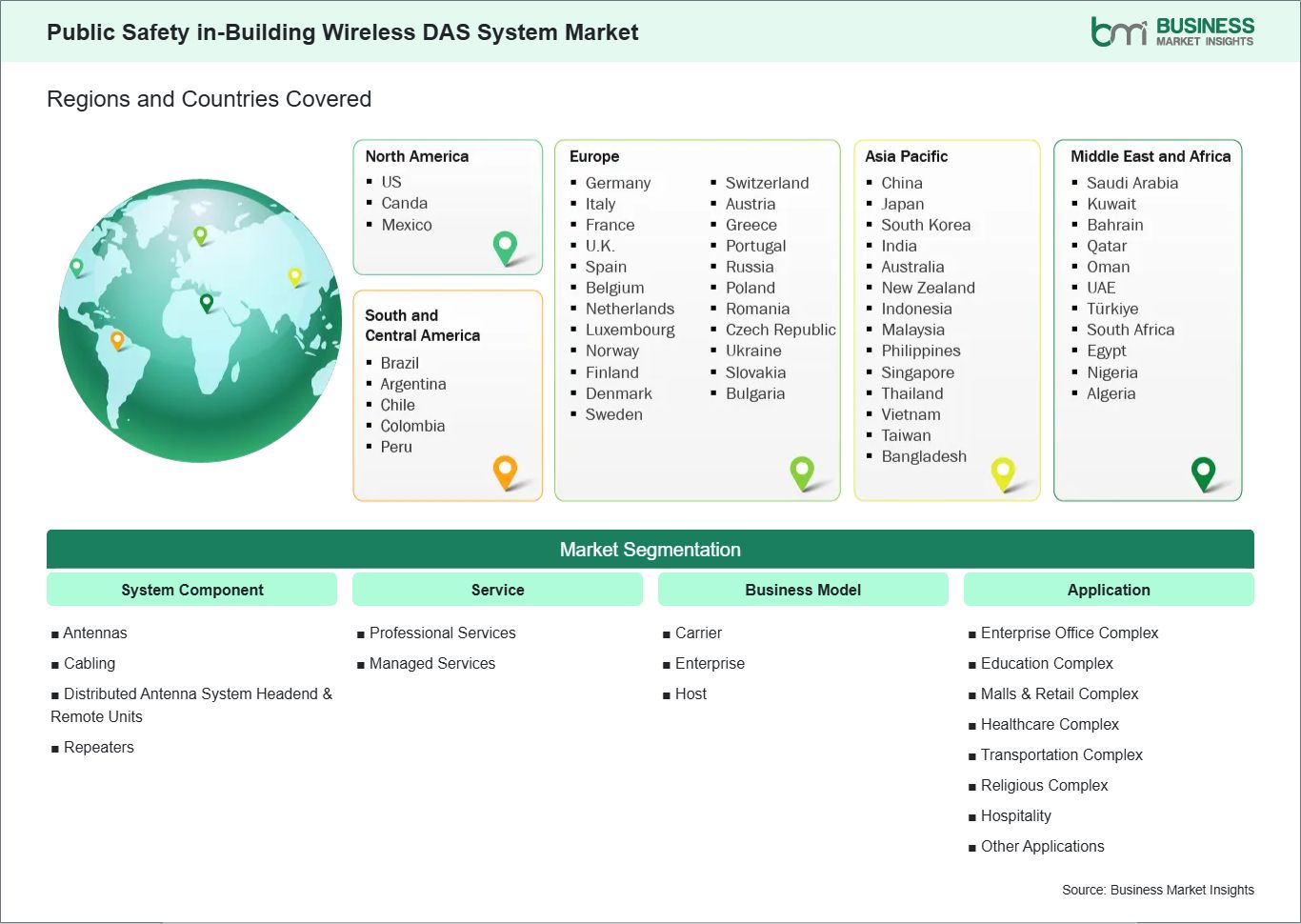

The geographical scope of the Public Safety in- Building Wireless DAS System Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America held the largest share in 2025 due to established regulatory frameworks, advanced infrastructure, and high adoption of safety‑critical communication systems across public and private sectors. The U.S. and Canada, with stringent building codes and public safety requirements, continue to lead in DAS deployments for transportation hubs, healthcare campuses, and commercial complexes.

In Europe, market growth is supported by harmonized safety standards and emphasis on life‑safety communication across densely built environments. Countries such as the UK, Germany, and France demonstrate strong adoption in major office environments, transit systems, and mixed‑use developments. Regulatory alignment across the EU enables wider deployment strategies and cross‑border vendor participation.

The Asia Pacific region is experiencing rapid expansion, driven by urbanization, modernization of transportation infrastructure, and increased safety investments in hospitality and retail complexes. Markets such as China, Japan, South Korea, and India are integrating public safety DAS as part of broader smart building initiatives, though adoption levels vary based on regulatory maturity and infrastructure spend.

In Middle East & Africa and South & Central America, early growth is concentrated in major urban centers and industrial corridors where stakeholder focus on first responder communication and large‑venue safety is rising. Public‑private partnerships and infrastructure modernization programs are facilitating initial DAS deployments, though pricing sensitivity and uneven regulatory enforcement remain challenges. Across regions, local safety codes, infrastructure priorities, and fiscal frameworks shape competitive strategies, with vendors customizing offerings to match regional needs and compliance landscapes.