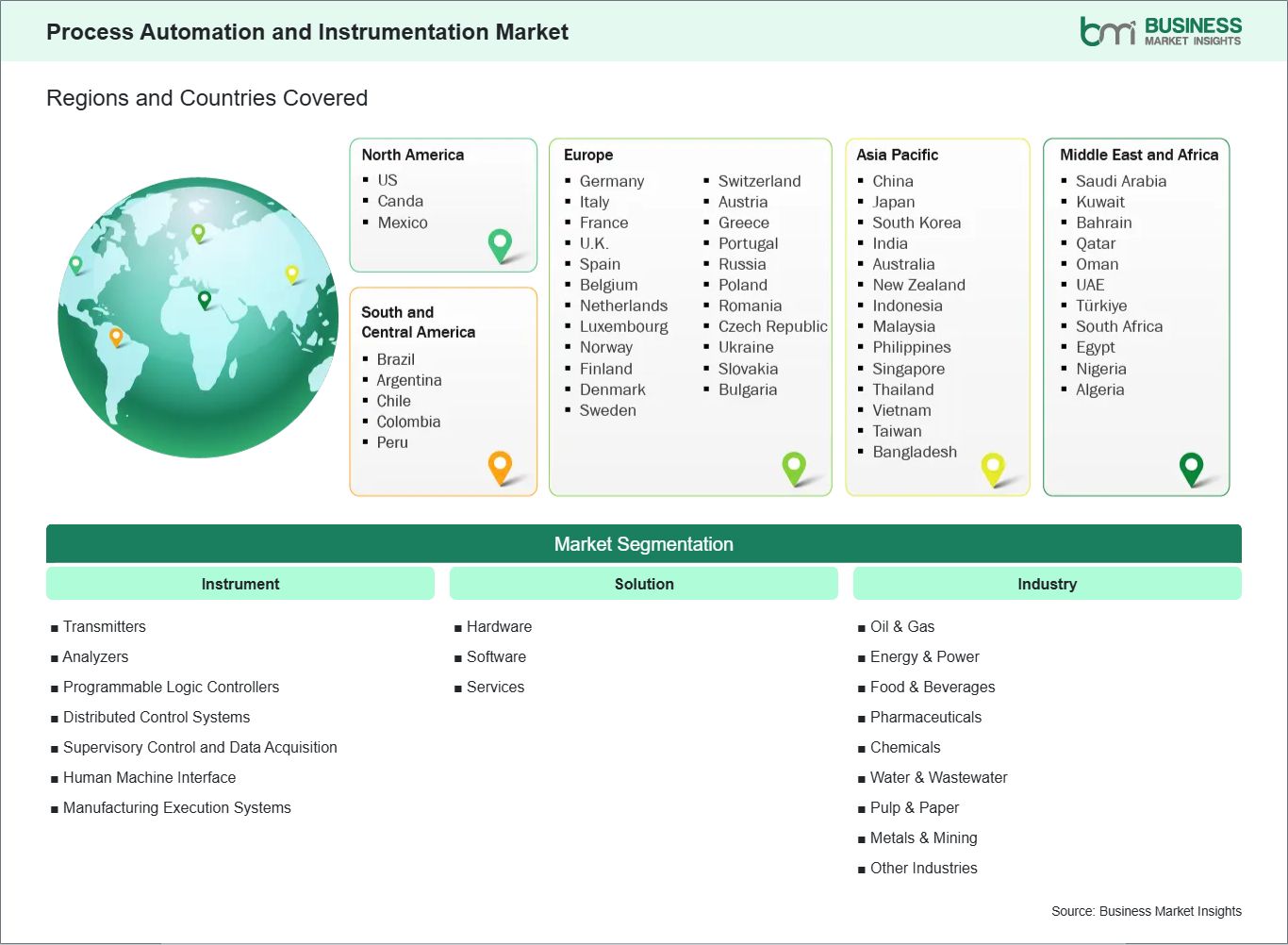

Instrument (Transmitters, Analyzers, Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA), Human Machine Interface (HMI), Manufacturing Execution Systems (MES))

Solution (Hardware, Software, Services)

Industry (Oil & Gas, Energy & Power, Food & Beverages, Pharmaceuticals, Chemicals, Water & Wastewater, Pulp & Paper, Metals & Mining, Other Industries)

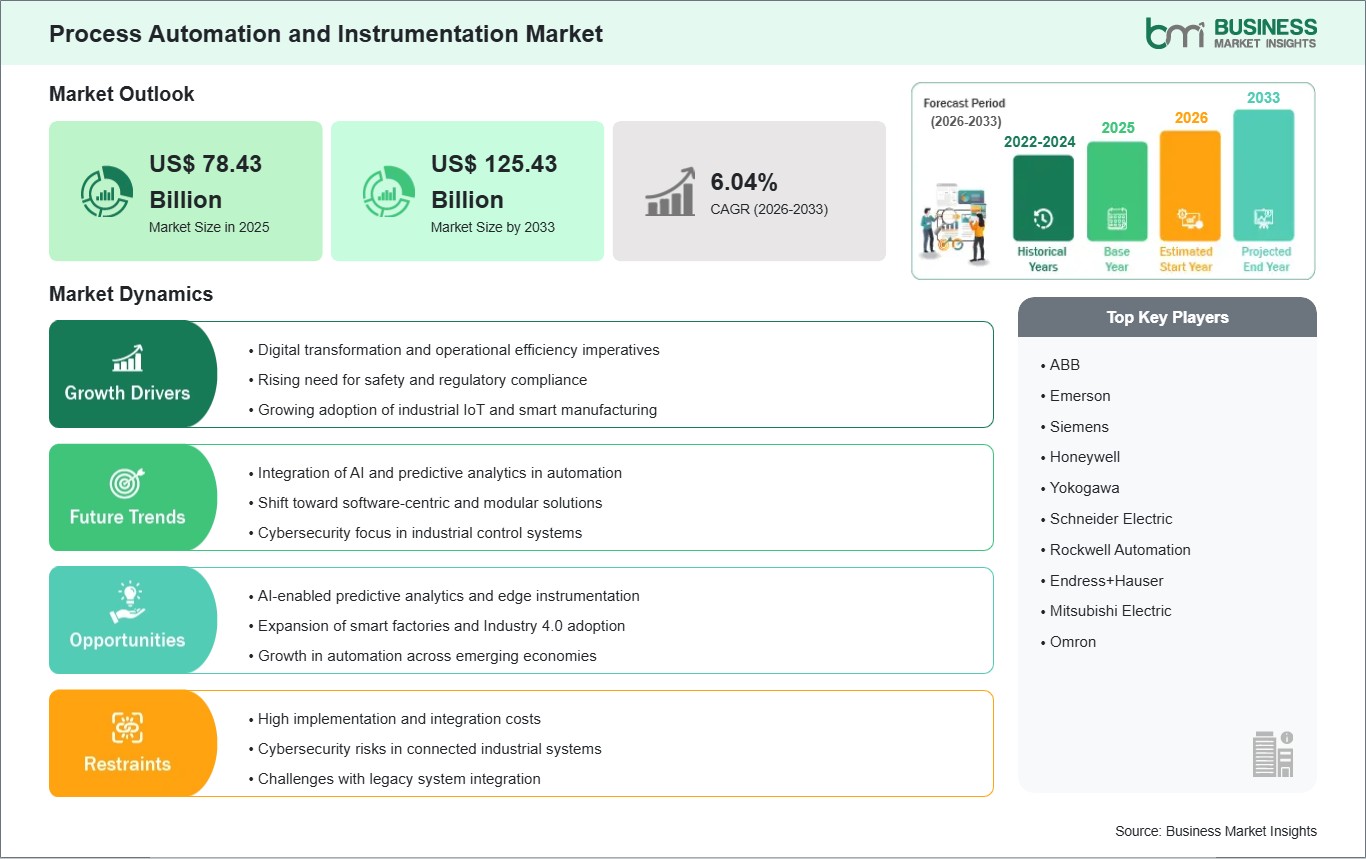

The Process Automation and Instrumentation Market size is expected to reach US$ 125.43 billion by 2033 from US$ 78.43 billion in 2025. The market is estimated to record a CAGR of 6.04% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global process automation and instrumentation market is propelled by rapid industrial digitization, stringent regulatory requirements, and the rising emphasis on safety, efficiency, and productivity across manufacturing and process‑centric industries. Automation and instrumentation technologies — including transmitters, analyzers, PLCs, DCS, SCADA, HMIs, and MES — form the backbone of industrial control systems that enhance operational visibility, reduce human error, and enable real‑time decision‑making.

With Industry 4.0 and smart manufacturing paradigms gaining traction globally, enterprises are accelerating investments in integrated automation solutions that combine hardware, software, and services.

Competitive dynamics focus on interoperability, scalability, and cybersecurity. Vendors are increasingly offering modular, software‑centric solutions that integrate with legacy systems while enabling digital transformation.

Geographically, North America and Europe currently lead in adoption due to advanced industrial infrastructure and high investments in digital transformation. However, emerging markets in Asia Pacific and the Middle East are witnessing accelerated demand driven by industrial expansion, infrastructure spend, and modernization of process industries.

Strategic initiatives that emphasize cost optimization, regulatory compliance, and digital integration position the process automation and instrumentation market at the forefront of industrial efficiency improvements and long‑term competitive advantage.

Process Automation and Instrumentation Market - Strategic Insights:

Get more information on this report

Process Automation and Instrumentation Market Segmentation Analysis:

Key segments that contributed to the derivation of the process automation and instrumentation market analysis are instrument, solution, and industry.

By instrument, the process automation and instrumentation market is segmented into transmitters, analyzers, programmable logic controllers (PLCs), distributed control systems (DCS), supervisory control and data acquisition (SCADA), human machine interface (HMI), and manufacturing execution systems (MES). The Distributed Control Systems (DCS) segment dominated the market in 2025.

By solution, the process automation and instrumentation market is segmented into hardware, software, and services. The hardware segment dominated in 2025.

By industry, the process automation and instrumentation market is segmented into oil & gas, energy & power, food & beverages, pharmaceuticals, chemicals, water & wastewater, pulp & paper, metals & mining, and other industries. The oil & gas segment dominated the market in 2025.

Process Automation and Instrumentation Market Drivers and Opportunities:

Digital Transformation and Operational Efficiency Imperatives

The primary driver for the process automation and instrumentation market is the accelerating shift toward digital transformation and operational efficiency across industrial sectors. Organizations are under increasing pressure to optimize production, improve quality, and lower operational costs — all while maintaining safety and regulatory compliance. Automation and instrumentation technologies fulfill these needs by providing real‑time monitoring, precise control, and advanced analytics capabilities.

Key technologies such as PLCs, DCS, SCADA, and HMIs enable seamless control and visualization of complex industrial processes, reducing reliance on manual intervention and minimizing errors. Additionally, the integration of industrial IoT (IIoT) devices, smart sensors, and analytics platforms enhances predictive maintenance and asset performance management. This integration allows companies to pre‑empt equipment failures, reduce unplanned downtime, and extend the lifecycle of critical assets — leading to significant cost savings and improved throughput.

Furthermore, digital transformation initiatives are supported by advanced software solutions that provide data aggregation, remote access, and scalable architectures. Cloud connectivity and edge computing improve responsiveness and allow distributed operations teams to monitor processes from anywhere. The result is a connected ecosystem where automation output directly informs strategic decision‑making and continuous improvement.

Regulatory frameworks in sectors such as energy, pharmaceuticals, and chemicals also mandate rigorous safety and environmental standards. Compliance requirements drive investments in reliable instrumentation for monitoring pressures, temperatures, flow rates, and emissions, ensuring operational integrity and reducing risk.

AI‑Enabled Predictive Analytics and Edge‑Integrated Instrumentation

A significant opportunity in the process automation and instrumentation market is the integration of AI‑enabled predictive analytics and edge computing with instrumentation systems. Traditional automation architectures primarily focus on process control and historical data logging. However, the advent of AI, machine learning, and cloud‑edge orchestration is reshaping how industrial data is consumed and applied.

Smart instrumentation equipped with edge analytics can process data locally, identify anomalies, and trigger corrective actions without latency associated with cloud dependency. This capability enhances responsiveness for critical operations — such as detecting equipment degradation, predicting failures before they occur, and enabling automated corrective workflows. The combination of predictive insights with real‑time control improves uptime and optimizes maintenance schedules, significantly reducing operational expenditures.

AI analytics also help uncover hidden patterns across multiple process parameters, enabling operators to fine‑tune settings for peak efficiency. For example, in chemical processing or energy generation, AI algorithms can identify optimal setpoints that maximize yield while minimizing energy use and waste. The result is a smarter instrumentation ecosystem that actively contributes to operational decision‑making rather than merely reporting data.

Moreover, as industries adopt hybrid cloud strategies, instrumentation platforms that seamlessly integrate edge processing with centralized analytics and visualization tools present a compelling value proposition. Vendors that offer modular solutions combining smart sensors, edge hardware, AI analytics, and secure connectivity stand to capture market share by enabling digital transformation at scale. This trend creates opportunities for cross‑industry application — from improving water treatment plant efficiencies to optimizing throughput in food & beverage manufacturing — solidifying smart automation and AI‑augmented instrumentation as a cornerstone of next‑generation industrial operations.

Process Automation and Instrumentation Market Size and Share Analysis:

The Process Automation and Instrumentation Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within instrument, solution, and industry, offering insights into their contribution to overall market performance.

By instrument, the distributed control systems (DCS) subsegment dominated the market in 2025, driven by its ability to centralize control, facilitate complex process coordination, and provide scalability for large industrial environments.

By solution, the hardware subsegment dominated the market in 2025, driven by demand for field instrumentation, controllers, and control hardware in new installations and modernization projects.

By industry, the oil & gas subsegment dominated the market in 2025, driven by extensive automation requirements to improve safety, compliance, and production efficiency across exploration, drilling, refining, and distribution operations.

Process Automation and Instrumentation Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

ABB

Emerson

Siemens

Honeywell

Yokogawa

Schneider Electric

Rockwell Automation

Endress+Hauser

Mitsubishi Electric

Omron

Get more information on this report

Process Automation and Instrumentation Market Report Coverage and Deliverables:

The "Process Automation and Instrumentation Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Process Automation and Instrumentation Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Process Automation and Instrumentation Market trends, as well as drivers, restraints, and opportunities

Process Automation and Instrumentation Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Process Automation and Instrumentation Market

Detailed company profiles, including SWOT analysis

Process Automation and Instrumentation Market Geographic Insights:

The geographical scope of the Process Automation and Instrumentation Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America held a significant share in 2025 due to advanced industrial automation adoption, strong presence of key vendors, and robust modernization initiatives across manufacturing, energy, and chemical sectors. The U.S. particularly drives high investment in digital transformation, predictive maintenance, and integrated control systems.

Europe remains a major market, supported by stringent safety and environmental standards, particularly in oil & gas, chemical, and pharmaceutical industries. Automation and instrumentation solutions are increasingly adopted for compliance with European emissions regulations and Industry 4.0 initiatives emphasizing connectivity and data integration.

The Asia Pacific region is poised for rapid growth, driven by expanding manufacturing capacity, infrastructure projects, and increased automation in sectors such as food & beverage, power generation, and water treatment. Countries like China, India, Japan, and South Korea are major hubs for both production and deployment of automation systems.

Middle East & Africa and South & Central America show emerging opportunities aligned with investments in energy projects, mining operations, and utility modernization. However, slower infrastructure build‑outs and economic constraints temper near‑term adoption relative to more developed regions.

Across regions, the push toward smart, connected industrial ecosystems supported by IoT, AI, and improved instrumentation underpins long‑term market expansion and value creation.

Get more information on this report

Process Automation and Instrumentation Market Research Report Guidance:

The report includes qualitative and quantitative data in the Process Automation and Instrumentation Market across type, application, industry, and geography.

The report starts with key takeaways (chapter 2), highlighting key trends and outlook of the Process Automation and Instrumentation Market.

Chapter 3 focuses on research methodology.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights major industry dynamics, including drivers, restraints, and opportunities.

Chapter 6 discusses historical revenues and forecast till 2033.

Chapters 7 to 10 cover segment analysis across regions.

Chapter 11 describes competitive analysis.

Chapter 12 describes industry landscape analysis.

Chapter 13 provides company profiles.

Chapter 14 includes appendix and disclaimer.

Process Automation and Instrumentation Market News and Key Development:

The Process Automation and Instrumentation Market is evaluated by gathering qualitative and quantitative data post primary and secondary research. A few of the key developments in the process automation and instrumentation market are,

In June 2025, ABB launched a next‑generation distributed control system (DCS) platform with integrated AI‑based diagnostics to improve process visibility and reduce downtime.

In March 2025, Emerson expanded its PLC portfolio with enhanced cybersecurity features and modular scalability targeting energy, chemical, and manufacturing sectors.

Key Sources Referred:

International Society of Automation (ISA)International Electrotechnical Commission (IEC)U.S. National Institute of Standards and Technology (NIST)European Committee for Standardization (CEN) / European Committee for Electrotechnical Standardization (CENELEC)International Organization for Standardization (ISO)

The List of Companies - Process Automation and Instrumentation Market

ABB

Emerson

Siemens

Honeywell

Yokogawa

Schneider Electric

Rockwell Automation

Endress+Hauser

Mitsubishi Electric

Omron

Frequently Asked Questions

How big is the Process Automation and Instrumentation Market?

The Process Automation and Instrumentation Market is valued at US$ 78.43 Billion in 2025, it is projected to reach US$ 125.43 Billion by 2033.

What is the CAGR for Process Automation and Instrumentation Market by (2026 - 2033)?

As per our report Process Automation and Instrumentation Market, the market size is valued at US$ 78.43 Billion in 2025, projecting it to reach US$ 125.43 Billion by 2033. This translates to a CAGR of approximately 6.04% during the forecast period.

What segments are covered in this report?

The Process Automation and Instrumentation Market report typically cover these key segments-

Instrument (Transmitters, Analyzers, Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA), Human Machine Interface (HMI), Manufacturing Execution Systems (MES))

Solution (Hardware, Software, Services)

Industry (Oil & Gas, Energy & Power, Food & Beverages, Pharmaceuticals, Chemicals, Water & Wastewater, Pulp & Paper, Metals & Mining, Other Industries)

What is the historic period, base year, and forecast period taken for Process Automation and Instrumentation Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Process Automation and Instrumentation Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Process Automation and Instrumentation Market?

The Process Automation and Instrumentation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB

Emerson

Siemens

Honeywell

Yokogawa

Schneider Electric

Rockwell Automation

Endress+Hauser

Mitsubishi Electric

Omron

Who should buy this report?

The Process Automation and Instrumentation Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Process Automation and Instrumentation Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Process Automation and Instrumentation Market

Get Free Sample For Process Automation and Instrumentation Market