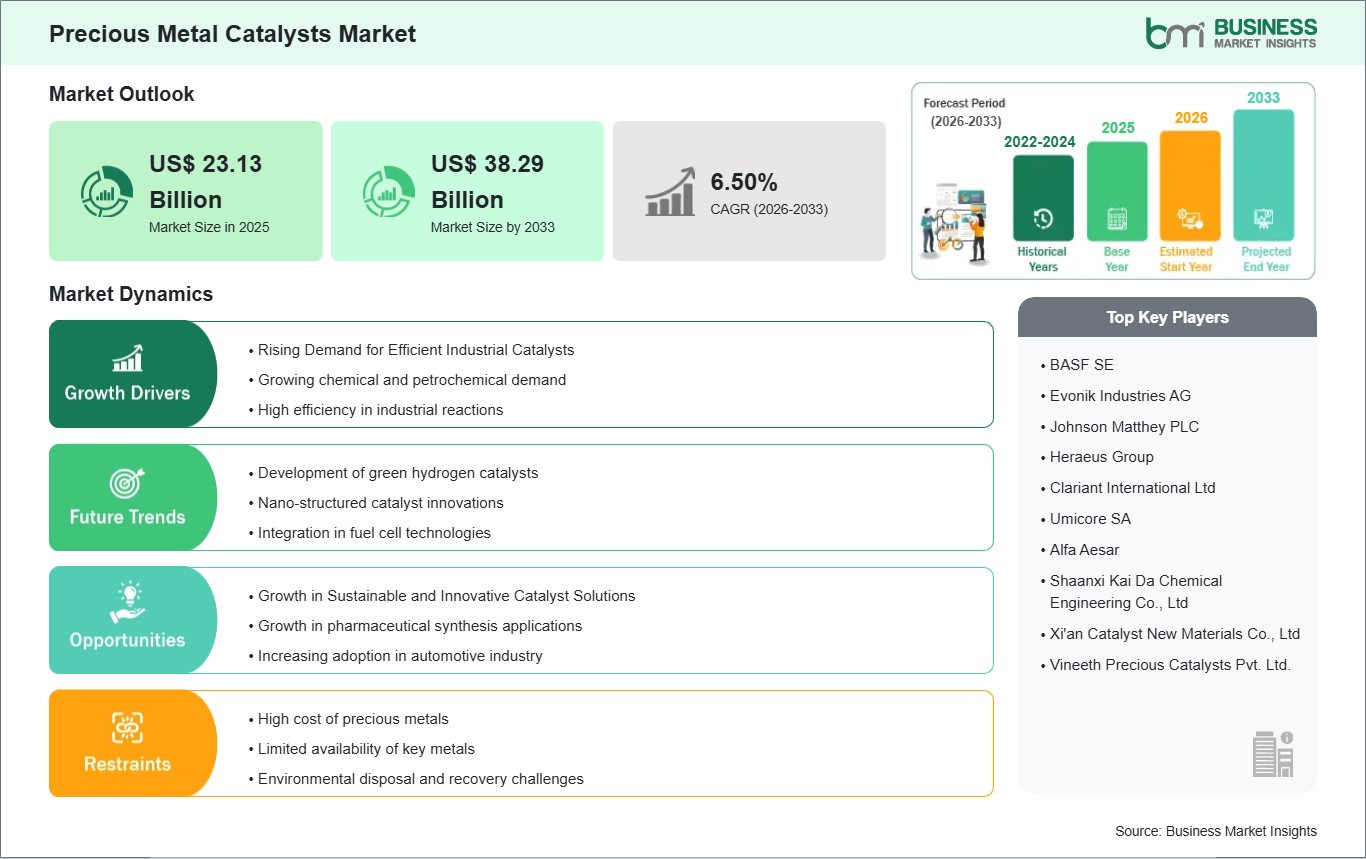

Rising Demand for Efficient Industrial Catalysts

The precious metal catalysts market is growing steadily because of the increasing demand for effective and high-performance catalysts in various industrial applications. Precious metal catalysts, which usually contain platinum, palladium, and rhodium, are vital for speeding up chemical reactions while staying stable under high temperature and pressure. Industries depend on these catalysts to improve process efficiency, lower energy use, and increase product yield. This makes them crucial in chemical manufacturing, petroleum refining, and environmental control technologies.

Besides improving efficiency, precious metal catalysts are appreciated for their durability and ability to work in tough operational settings. They are commonly used in automotive catalytic converters, fuel cells, and emission control systems to cut harmful emissions and meet strict environmental standards. The growing focus on cleaner technologies and energy-efficient operations has boosted the use of these catalysts. Industries look for materials that can maintain their performance over long periods while providing consistent and reliable results, which has further driven global demand.

Progress in industrial automation and chemical processing is also contributing to market growth. Manufacturers increasingly need catalysts that can provide predictable reaction rates, enhance selectivity, and minimize by-product formation. The unique chemical properties of precious metal catalysts allow them to meet these needs effectively. As companies prioritize efficiency, regulatory compliance, and sustainability, the demand for precious metal catalysts is expected to stay strong, leading to continued growth in the global industrial market.

Growth in Sustainable and Innovative Catalyst Solutions

The market for precious metal catalysts is gaining from new ideas aimed at sustainability, efficiency, and cost-effectiveness. Researchers and manufacturers are creating better catalyst formulations that optimize metal use, reduce waste, and extend product life. Innovations like supported catalysts, nanoparticle designs, and hybrid materials are helping to improve reaction efficiency and selectivity while lowering the environmental impact. These developments match the increasing focus on cleaner production methods and resource conservation in various industries.

There is growing interest in catalysts for renewable energy applications, such as fuel cells, hydrogen production, and biofuel processing. Precious metal catalysts play a vital role in driving chemical reactions in these new sectors, promoting both innovation and acceptance. New formulations that boost durability and lower the amount of precious metal needed are making broader applications and cost-effective scaling possible. Integrating advanced catalyst designs into industrial processes leads to better energy use and reduced emissions.

Sustainability is shaping production and application strategies. Companies are looking into recycling techniques, recovery methods, and better catalyst deployment to maximize efficiency and minimize environmental harm. The combination of performance, durability, and environmentally friendly design makes precious metal catalysts essential in today’s industrial operations. Continued emphasis on innovation and sustainability should create long-term growth opportunities, strengthening the market's position in global chemical, energy, and environmental sectors.