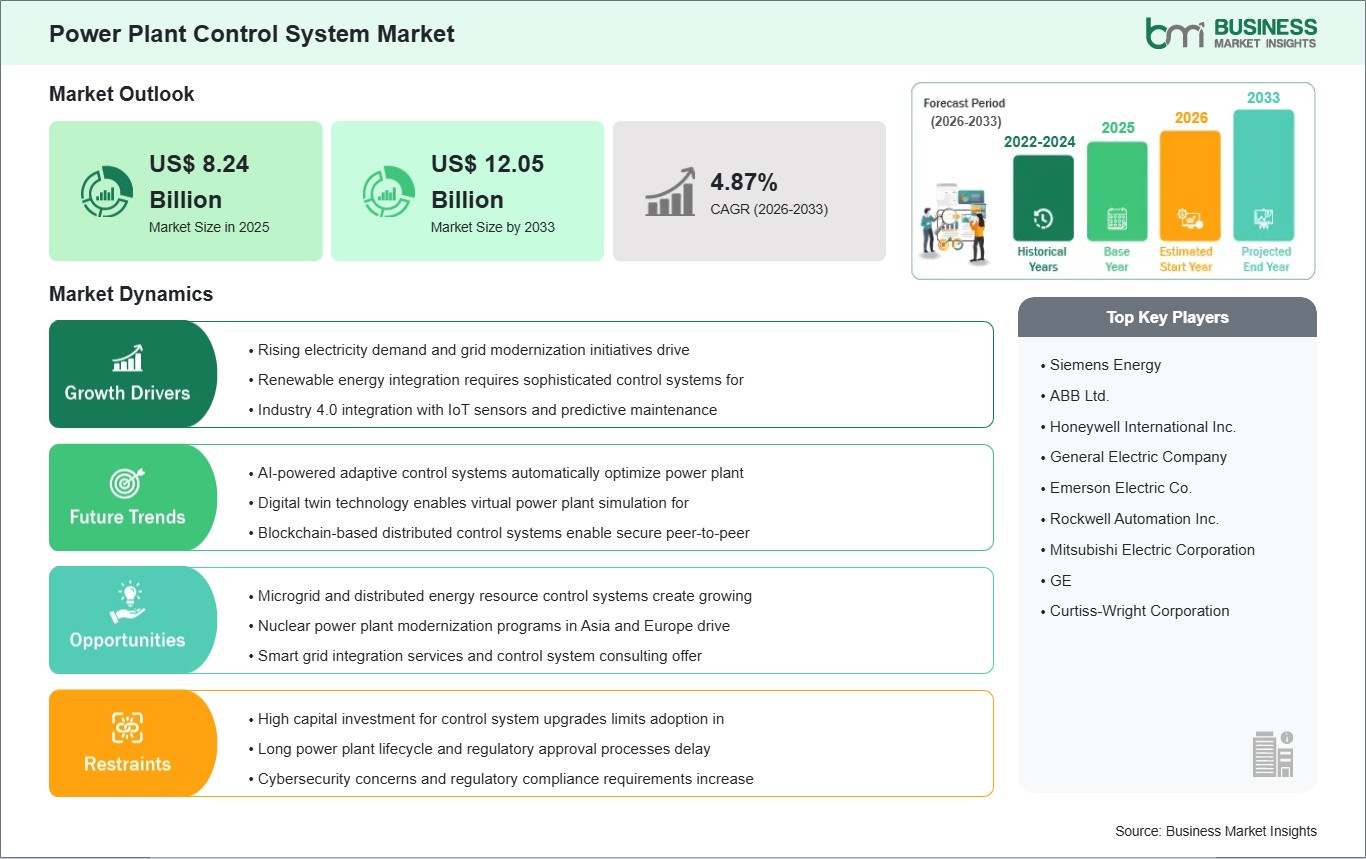

The Power Plant Control System Market size is expected to reach US$ 12.05 billion by 2033 from US$ 8.24 billion in 2025. The market is estimated to record a CAGR of 4.87% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Power plant control systems are integrated automation environments used to supervise, coordinate, and optimize generation processes across turbines, boilers, generators, auxiliaries, and grid-connected electrical equipment. These systems combine monitoring, control logic, operator interfaces, and data acquisition functions to maintain safe and efficient plant performance under changing operating conditions. Their technical role extends from load management and process stability to fault handling and operational visibility across complex assets. As utilities modernize generation fleets, control platforms are becoming more central to plant reliability and lifecycle management.

Market momentum reflects the need to improve operational continuity, modernization readiness, and process efficiency across aging and newly built plants. Utilities and independent power producers increasingly require control solutions that can unify plant subsystems, support faster decision-making, and maintain stable output amid grid variability and fuel-mix changes. This requirement applies across hydroelectric, natural gas, coal, and oil-based assets, particularly where refurbishment or performance optimization is commercially preferable to full asset replacement. The industry therefore benefits from both retrofit demand and automation expansion in newer facilities.

Segment structure shows a clear interplay between software-led solutions and service-led lifecycle support. Solutions hold the operational core because they govern plant logic, alarm handling, coordination functions, and operator visibility, while services remain essential for migration, commissioning, training, and long-term maintenance. By plant type, natural gas and coal facilities retain strong relevance due to the complexity of thermal process coordination, while hydroelectric plants create a distinct opportunity linked to digital control upgrades and pumped-storage development. Application demand is anchored in generator excitation, turbine control, and boiler-related process coordination.

Technology development is moving toward more integrated distributed control systems, improved supervisory functionality, predictive maintenance support, and stronger real-time plant coordination. Utilities are placing greater attention on unified control architectures that can reduce fragmentation across electrical and process domains. This transition is especially relevant where operators are modernizing legacy systems or connecting broader renewable and storage assets into centralized monitoring environments. As a result, platform flexibility and upgrade capability are becoming more commercially important.

Competitive conditions are shaped by modernization capability, installed-base migration expertise, and the ability to deliver plant-wide integration across multiple control domains. The market favors suppliers and service providers that can handle complex brownfield upgrades, support mixed plant portfolios, and maintain system continuity during transition phases. This creates a competitive environment defined less by standalone controls and more by integrated lifecycle execution.

Power Plant Control System Market - Strategic Insights:

Get more information on this report

Power Plant Control System Market Segmentation Analysis:

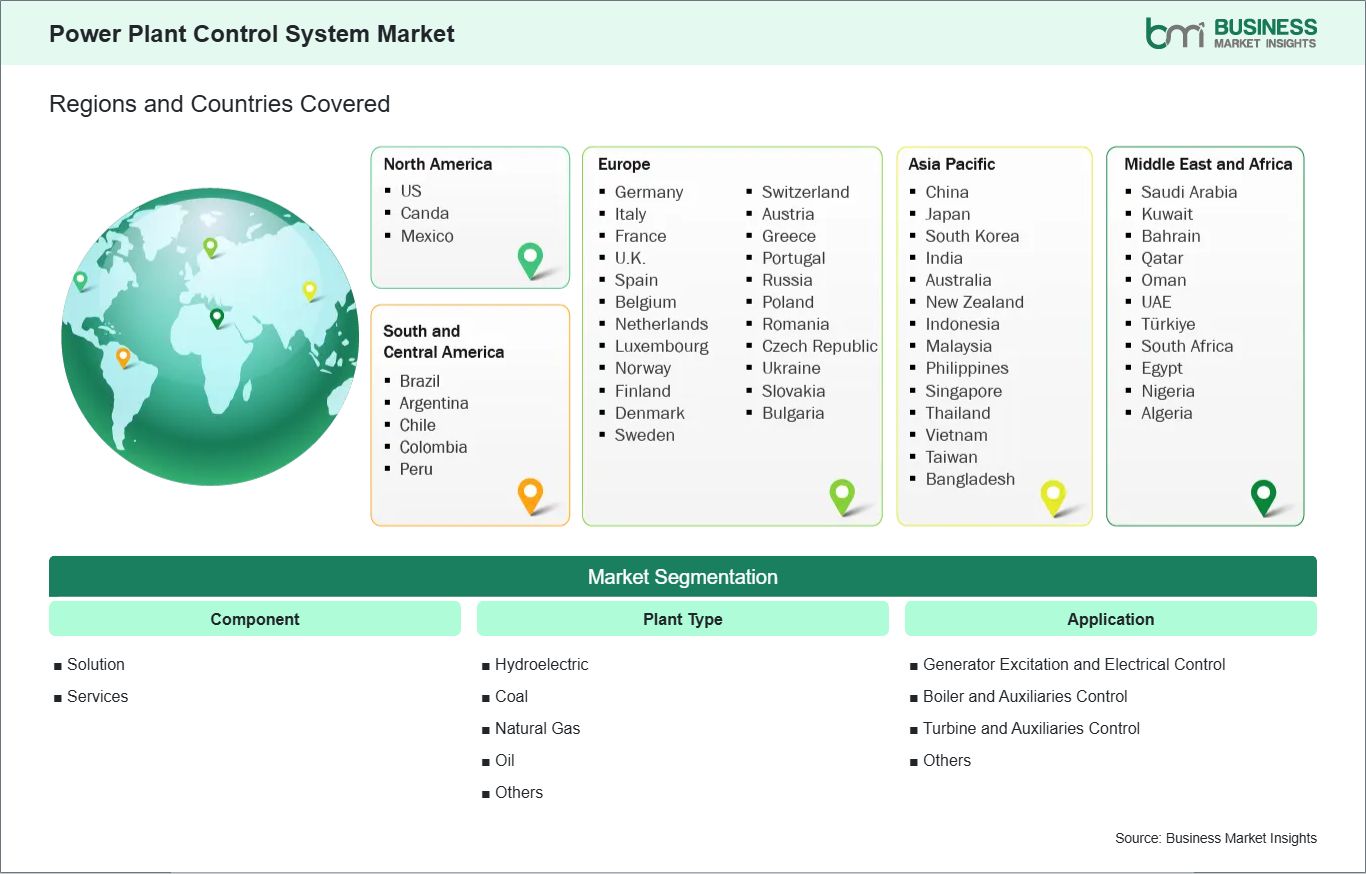

The Power Plant Control System Market is segmented based on component, plant type, application, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Component

Solution – Forms the central automation layer for plant-wide supervision and control.

Services – Supports migration, integration, commissioning, and long-term system upkeep.

By Plant Type

Hydroelectric – Requires coordinated control across turbines, water flow, and electrical assets.

Coal – Demands synchronized boiler, turbine, and emissions-related process control.

Natural Gas – Supports fast-response generation with integrated turbine and balance-of-plant oversight.

Oil – Relies on dependable monitoring for fuel handling and thermal process continuity.

Others – Includes additional generation formats with site-specific automation needs.

By Application

Generator Excitation and Electrical Control – Maintains output quality, voltage behavior, and electrical coordination.

Boiler and Auxiliaries Control – Regulates combustion-linked processes and support equipment.

Turbine and Auxiliaries Control – Oversees speed, efficiency, and mechanical operating stability.

Power Plant Control System Market Drivers and Opportunities:

Fleet Modernization and Operational Reliability

A large part of the market is shaped by the need to modernize aging power infrastructure without disrupting generation continuity. Many plants still operate with legacy automation architectures that limit visibility, complicate maintenance, and reduce integration across major subsystems. This creates demand for updated control environments that can improve process coordination, load response, and operator effectiveness across boilers, turbines, generators, and auxiliaries. The need becomes more pressing where utilities seek better asset utilization from existing plants.

The commercial effect extends beyond hardware replacement into long-cycle service and migration activity. Plant operators increasingly prefer phased upgrades that preserve system availability while improving control quality and data access. This strengthens the relevance of integrated solutions and engineering services in brownfield environments. The market therefore advances through modernization programs that tie automation investment directly to reliability and lifecycle extension.

Digital Upgrades Across Flexible and Renewable-Linked Generation

An important opportunity lies in digital upgrades that improve control precision across flexible thermal assets and digitally managed hydroelectric facilities. Modern control platforms can support unified monitoring, faster disturbance response, and better coordination between process and electrical layers. This is particularly relevant for gas-fired assets responding to variable grid conditions and for hydroelectric or pumped-storage projects requiring integrated supervision across multiple subsystems. These use cases expand the role of control platforms from routine automation toward strategic operating infrastructure.

Future scope improves as operators seek centralized oversight across mixed generation portfolios that increasingly include renewable and storage-linked assets. Control systems capable of interoperable monitoring, scalable architecture, and lifecycle support can capture stronger interest in both new and retrofit projects. This broadens opportunity across software solutions, migration services, and long-term operational support.

Power Plant Control System Market Size and Share Analysis:

The Power Plant Control System Market is projected to grow from US$ 8.24 billion in 2025 to US$ 12.05 billion by 2033. The market is estimated to record a CAGR of 4.87% from 2026 to 2033.

This growth trajectory indicates a market supported by automation renewal, operational efficiency targets, and the need for tighter coordination across plant systems. It also reflects broader digitalization within conventional and hydroelectric power operations.

By component, solutions account for the larger strategic share because they define the plant’s functional control architecture and real-time operating logic. Services remain indispensable because migrations, upgrades, maintenance, and engineering support are closely tied to long asset lives and complex plant environments. This pairing gives the market both recurring service depth and core platform value.

By application, generator excitation and electrical control together with turbine and auxiliaries control represent the strongest demand focus because they sit close to output stability and plant responsiveness. Boiler and auxiliaries control also holds strong relevance within thermal facilities where process balance directly affects efficiency and reliability. Application demand therefore, aligns closely with the need to coordinate generation-critical functions.

Power Plant Control System Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Siemens Energy

ABB Ltd.

Honeywell International Inc.

General Electric Company

Emerson Electric Co.

Rockwell Automation Inc.

Mitsubishi Electric Corporation

GE

Curtiss-Wright Corporation

Get more information on this report

Power Plant Control System Market Report Coverage and Deliverables:

The "Power Plant Control System Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Power Plant Control System Market Geographic Insights:

The Power Plant Control System market shows diverse regional adoption patterns influenced by installed generation mix, modernization priorities, grid operating requirements, and automation maturity. Global demand reflects a common need to improve power plant reliability, supervisory visibility, and coordination across electrical and process systems. Regional trajectories differ according to fleet age, renewable integration pressure, and the pace of capital investment in plant upgrades.

North America remains an important market because many facilities operate with long-lived generation assets that periodically require control modernization and subsystem integration. The region also places high emphasis on reliable output, lifecycle extension, and automation-led improvement of operational efficiency across thermal fleets. This supports continued interest in plant-wide control migrations and unified digital environments.

Asia Pacific presents a broader expansion profile shaped by ongoing power demand, infrastructure development, and the need to upgrade older units while supporting newer capacity additions. Utilities in the region are increasingly attentive to automation systems that improve plant responsiveness, centralize monitoring, and reduce operational disruption. These conditions make the region highly relevant for both new deployments and retrofit-oriented services.

Europe combines strong relevance in hydropower, flexible generation, and digital modernization of power infrastructure. Pumped-storage projects, decarbonization-linked grid balancing needs, and stronger interest in centralized control architectures support market activity across the region. Emerging markets in the Middle East, Africa, and South America also present selective opportunity where utility modernization and generation reliability remain priority investment themes.

Get more information on this report

Power Plant Control System Market Research Report Guidance:

The Power Plant Control System market report includes qualitative and quantitative data in the Power Plant Control System Market across component, plant type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Power Plant Control System Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Power Plant Control System Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Power Plant Control System Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Power Plant Control System Market segments by component, plant type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Power Plant Control System Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Power Plant Control System Market News and Key Development:

The Power Plant Control System Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In March 2026, In line with ABB‘s position as one of the market leaders in hydropower process control systems in Austria, Tiroler Wasserkraft (TIWAG) has awarded ABB the distributed control system ABB Ability™ System 800xA® (DCS) contract for its Kuhtai 2 project. TIWAG is an Austrian energy company specialized in generating electricity from hydropower.

In November 2025, Ansaldo Energia has completed the project to modernize Unit 1 of the Modugno combined cycle power plant owned by Sorgenia. The plant, located near the city of Bari in Southern Italy, has a nominal power rate of 810 MW. As part of this project, ABB has evolved the plant’s existing gas turbine control systems to the latest ABB Ability™ System 800xA® technology. The project helps to extend the lifetime of the gas turbine control systems by approximately 20 years.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Power Plant Control System Market

Siemens Energy

ABB Ltd.

Honeywell International Inc.

General Electric Company

Emerson Electric Co.

Rockwell Automation Inc.

Mitsubishi Electric Corporation

GE

Curtiss-Wright Corporation

Frequently Asked Questions

How big is the Power Plant Control System Market?

The Power Plant Control System Market is valued at US$ 8.24 Billion in 2025, it is projected to reach US$ 12.05 Billion by 2033.

What is the CAGR for Power Plant Control System Market by (2026 - 2033)?

As per our report Power Plant Control System Market, the market size is valued at US$ 8.24 Billion in 2025, projecting it to reach US$ 12.05 Billion by 2033. This translates to a CAGR of approximately 4.87% during the forecast period.

What segments are covered in this report?

The Power Plant Control System Market report typically cover these key segments-

Component (Solution, Services)

Plant Type (Hydroelectric, Coal, Natural Gas, Oil, Others)

Application (Generator Excitation and Electrical Control, Boiler and Auxiliaries Control, Turbine and Auxiliaries Control, Others)

What is the historic period, base year, and forecast period taken for Power Plant Control System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Power Plant Control System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Power Plant Control System Market?

The Power Plant Control System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens Energy

ABB Ltd.

Honeywell International Inc.

General Electric Company

Emerson Electric Co.

Rockwell Automation Inc.

Mitsubishi Electric Corporation

GE

Curtiss-Wright Corporation

Who should buy this report?

The Power Plant Control System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Power Plant Control System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Power Plant Control System Market

Get Free Sample For Power Plant Control System Market