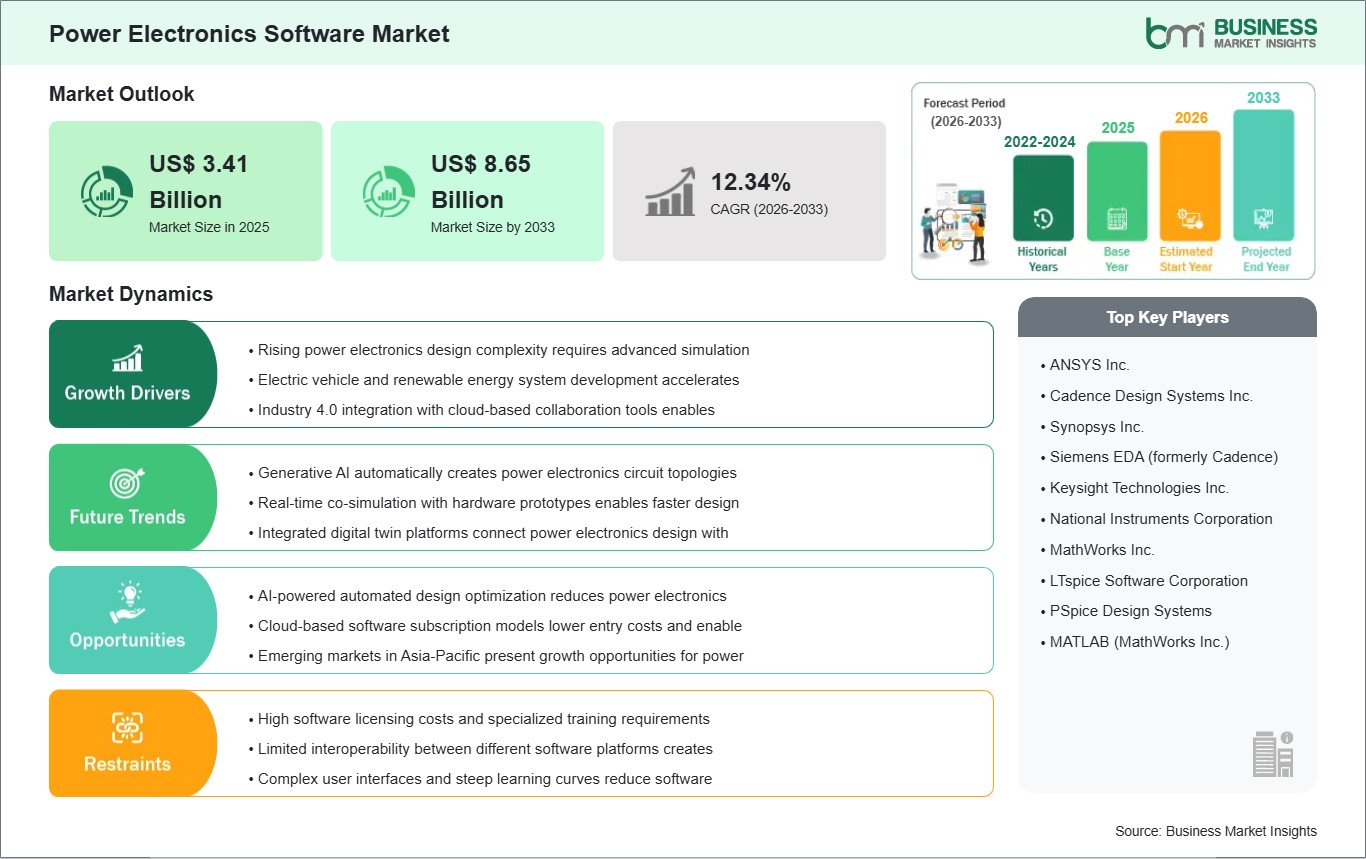

The Power Electronics Software Market size is expected to reach US$ 8.65 billion by 2033 from US$ 3.41 billion in 2025. The market is estimated to record a CAGR of 12.34% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Power electronics software comprises digital tools used to design, model, simulate, validate, and control power conversion systems before and during hardware deployment. These platforms support engineering workflows across converters, inverters, motor drives, battery systems, and grid-connected equipment where electrical behavior must be tested under demanding operating conditions. Their value lies in reducing development cycles, improving design confidence, and enabling earlier validation of control strategies. As electrical architectures become more software-defined, these tools are becoming more integrated into product development across power-intensive sectors.

The market is advancing because power systems are becoming more complex, while development timelines remain compressed. Engineers increasingly need software environments that can support faster controller tuning, fault testing, algorithm validation, and cross-domain coordination between electrical, control, and embedded design teams. This need is especially pronounced in automotive electrification, renewable energy systems, industrial drives, and aerospace applications where hardware failure is costly and verification requirements are stringent. As a result, software is taking a more central role in front-loading engineering decisions.

Segment trends indicate that simulation, control, and design software are all commercially significant, but their roles differ across engineering stages. Model-based design is gaining strong relevance because it connects system architecture, control development, and validation within one coherent workflow. Hardware-in-the-loop simulation and rapid control prototyping are also becoming more important where teams need real-time testing before full hardware integration. Embedded system prototyping maintains relevance in deployment-oriented development environments that require early control implementation.

Technology evolution is moving toward real-time simulation, faster solver performance, improved communication support, and better alignment with e-mobility and grid modernization use cases. Software releases increasingly emphasize high-fidelity modeling, FPGA-oriented workflows, and more robust testing environments for complex switching behavior. These developments are improving the practicality of digital validation across advanced power conversion projects. The result is a market defined less by standalone design tools and more by integrated engineering ecosystems.

Competitive conditions are shaped by usability, real-time performance, workflow integration, and the ability to support both early design and later-stage validation. Suppliers are differentiating through HIL capability, model execution speed, embedded workflow support, and broader applicability across industrial and mobility segments. The sector therefore reflects a transition toward software platforms that serve as development infrastructure for modern power electronics engineering.

Power Electronics Software Market - Strategic Insights:

Get more information on this report

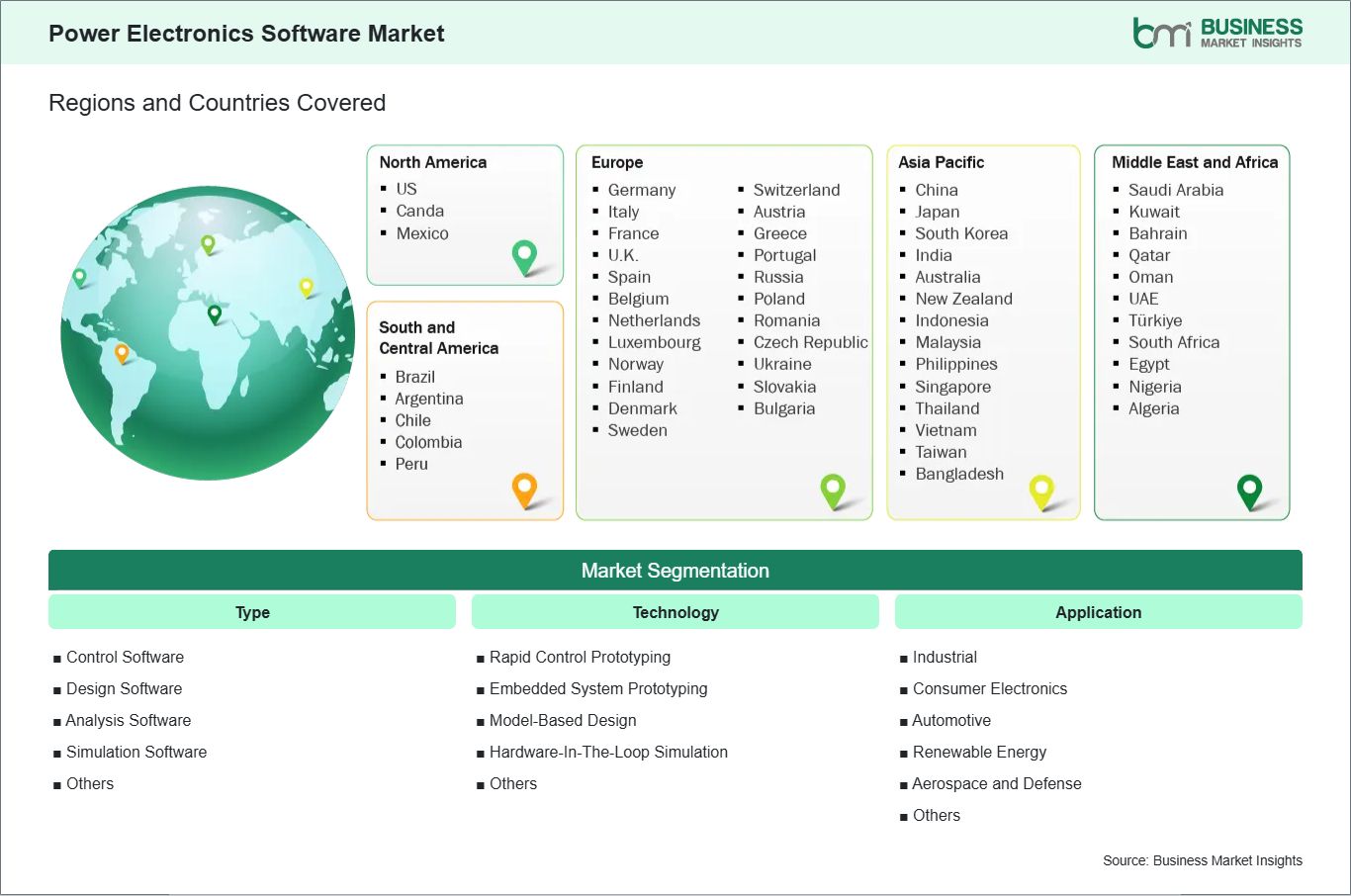

Power Electronics Software Market Segmentation Analysis:

The Power Electronics Software Market is segmented based on type, technology, application, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Type

Control Software: Enables controller development and operational logic refinement.

Design Software: Supports architecture planning and component-level engineering decisions.

Analysis Software: Examines electrical behavior, efficiency, and performance constraints.

Simulation Software: Replicates operating conditions before hardware commitment.

Others: Covers supporting tools for workflow integration and specialized tasks.

By Technology

Rapid Control Prototyping (RCP): Accelerates controller tuning before final embedded implementation.

Embedded System Prototyping: Bridges software logic with deployable hardware environments.

Model-Based Design (MBD): Connects system modeling, control logic, and validation workflows.

Hardware-In-The-Loop (HIL) Simulation: Tests controllers under real-time virtual operating conditions.

Others: Includes additional validation and software-assisted engineering approaches.

By Application

Industrial: Uses software to optimize drives, converters, and factory power systems.

Consumer Electronics: Supports compact and efficient product power architectures.

Automotive: Requires rigorous validation for electrified propulsion and onboard converters.

Renewable Energy: Applies simulation for inverters, storage interfaces, and grid interaction.

Aerospace and Defense: Prioritizes high-confidence verification in mission-critical electrical systems.

Others: Covers additional application fields with power conversion design needs.

Power Electronics Software Market Drivers and Opportunities:

Greater Engineering Complexity in Electrified and Software-Defined Systems

Power conversion systems are becoming more complex as industries integrate advanced control logic, faster switching devices, and stricter performance requirements into electrical architectures. Traditional development methods are less effective when teams must validate behavior across multiple scenarios before hardware commissioning. This creates a strong need for software tools that can simulate operating conditions, refine control strategies, and verify system response earlier in the design cycle. The requirement is especially strong in sectors where failure risk, regulatory pressure, and time-to-market constraints intersect.

The market impact is broad because software now supports both technical precision and development efficiency. Automotive, industrial, renewable energy, and aerospace teams increasingly rely on digital validation to reduce iteration time and detect issues before costly physical testing. This strengthens the value of simulation, control, and HIL environments as part of mainstream engineering infrastructure rather than optional support tools. The market is therefore expanding through deeper workflow integration across the product lifecycle.

Real-Time HIL, Model-Based Design, and Faster Simulation Workflows

A major opportunity lies in software platforms that unify design, testing, and controller validation within real-time engineering environments. HIL simulation, model-based design, and rapid control prototyping are becoming more relevant because they shorten validation cycles and improve confidence in complex control strategies. These technologies are particularly valuable in e-mobility, renewable energy, and industrial automation projects where system behavior must be evaluated under dynamic operating conditions before full deployment. Their ability to connect virtual design with practical controller testing gives them strong commercial relevance.

Future scope expands as software vendors improve solver speed, communication support, interface usability, and compatibility with emerging power applications. Real-time simulation environments are moving closer to full development platforms that support both early-stage concept evaluation and later-stage verification. As engineering teams seek faster iteration and more dependable digital validation, integrated software ecosystems can capture a larger share of development budgets across high-value power electronics programs.

Power Electronics Software Market Size and Share Analysis:

The Power Electronics Software Market is projected to grow from US$ 3.41 billion in 2025 to US$ 8.65 billion by 2033. The market is estimated to record a CAGR of 12.34% from 2026 to 2033.

This growth path indicates a market supported by the digitalization of engineering workflows, broader electrification, and stronger reliance on virtual validation before hardware deployment. It also reflects the expanding role of software in reducing design risk and development time.

By type and technology, simulation and control software hold strong strategic importance because they sit close to critical design and validation activities. Model-based design and HIL simulation also maintain a prominent position where teams require iterative testing, controller refinement, and system-level confidence. Other software categories remain relevant as enabling layers within integrated engineering workflows.

By application, industrial and automotive environments represent the strongest demand centers because they combine power complexity with strict performance validation requirements. Renewable energy also accounts for a substantial opportunity due to inverter and grid-interface design needs. Aerospace and defense and consumer electronics broaden the market through specialized and compact power conversion use cases.

Power Electronics Software Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

ANSYS Inc.

Cadence Design Systems Inc.

Synopsys Inc.

Siemens EDA (formerly Cadence)

Keysight Technologies Inc.

National Instruments Corporation

MathWorks Inc.

LTspice Software Corporation

PSpice Design Systems

MATLAB (MathWorks Inc.)

Get more information on this report

Power Electronics Software Market Report Coverage and Deliverables:

The "Power Electronics Software Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Power Electronics Software Market Geographic Insights:

The Power Electronics Software market shows diverse regional adoption patterns influenced by engineering maturity, electrification priorities, digital validation practices, and advanced manufacturing capability. Across the global industry, market activity is expanding as power conversion systems become more software-intensive and development teams require earlier, faster, and safer verification methods. Regional differences largely reflect industrial specialization, R&D infrastructure, and the pace of adoption for real-time testing tools.

North America holds a strong position because the region combines advanced automotive, aerospace, industrial, and energy technology ecosystems with high engineering software intensity. Demand is reinforced by the use of HIL, real-time simulation, and controller development platforms in sectors where validation depth and time efficiency are especially important. This makes the region a major center for high-value software deployment across complex power electronics programs.

Asia Pacific presents a broad opportunity due to its concentration of electronics production, automotive development, and renewable energy system deployment. Engineering teams in the region increasingly require software that supports scalable design, embedded development, and faster verification of converters, drives, and power control systems. This gives the market a strong foundation across both high-volume industrial applications and emerging advanced mobility projects.

Europe shows strong alignment with model-based design, industrial automation, and electrified mobility engineering, making software-intensive development workflows increasingly relevant. Regional demand is also shaped by emphasis on simulation-backed validation and efficient system integration in automotive, renewable, and industrial applications. Beyond these major regions, emerging markets offer selective opportunity as engineering capabilities strengthen and electrified infrastructure programs expand.

Get more information on this report

Power Electronics Software Market Research Report Guidance:

The Power Electronics Software market report includes qualitative and quantitative data in the Power Electronics Software Market across type, technology, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Power Electronics Software Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Power Electronics Software Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Power Electronics Software Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Power Electronics Software Market segments by type, technology, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Power Electronics Software Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Power Electronics Software Market News and Key Development:

The Power Electronics Software Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In May 2026, ROHM has released the ROHM PLECS Simulator on ROHM’s official website. This simulation tool enables designers of power electronics circuits and system designers to rapidly simulate the operation of ROHM’s power devices online. The tool is based on the PLECS® simulation software.

In May 2026, L&T Semiconductor Technologies Ltd (LTSCT), a leading Indian fabless semiconductor company and a wholly-owned subsidiary of Larsen and Toubro, today announced a multiyear license agreement with Synopsys Inc., a leader in engineering solutions from silicon to systems, to strengthen its advanced power electronics design capabilities and support India’s growing semiconductor ecosystem.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Power Electronics Software Market

ANSYS Inc.

Cadence Design Systems Inc.

Synopsys Inc.

Siemens EDA (formerly Cadence)

Keysight Technologies Inc.

National Instruments Corporation

MathWorks Inc.

LTspice Software Corporation

PSpice Design Systems

MATLAB (MathWorks Inc.)

Frequently Asked Questions

How big is the Power Electronics Software Market?

The Power Electronics Software Market is valued at US$ 3.41 Billion in 2025, it is projected to reach US$ 8.65 Billion by 2033.

What is the CAGR for Power Electronics Software Market by (2026 - 2033)?

As per our report Power Electronics Software Market, the market size is valued at US$ 3.41 Billion in 2025, projecting it to reach US$ 8.65 Billion by 2033. This translates to a CAGR of approximately 12.34% during the forecast period.

What segments are covered in this report?

The Power Electronics Software Market report typically cover these key segments-

Type (Control Software, Design Software, Analysis Software, Simulation Software, Others)

Technology (Rapid Control Prototyping (RCP), Embedded System Prototyping, Model-Based Design (MBD), Hardware-In-The-Loop (HIL) Simulation, Others)

What is the historic period, base year, and forecast period taken for Power Electronics Software Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Power Electronics Software Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Power Electronics Software Market?

The Power Electronics Software Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ANSYS Inc.

Cadence Design Systems Inc.

Synopsys Inc.

Siemens EDA (formerly Cadence)

Keysight Technologies Inc.

National Instruments Corporation

MathWorks Inc.

LTspice Software Corporation

PSpice Design Systems

MATLAB (MathWorks Inc.)

Who should buy this report?

The Power Electronics Software Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Power Electronics Software Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Power Electronics Software Market

Get Free Sample For Power Electronics Software Market