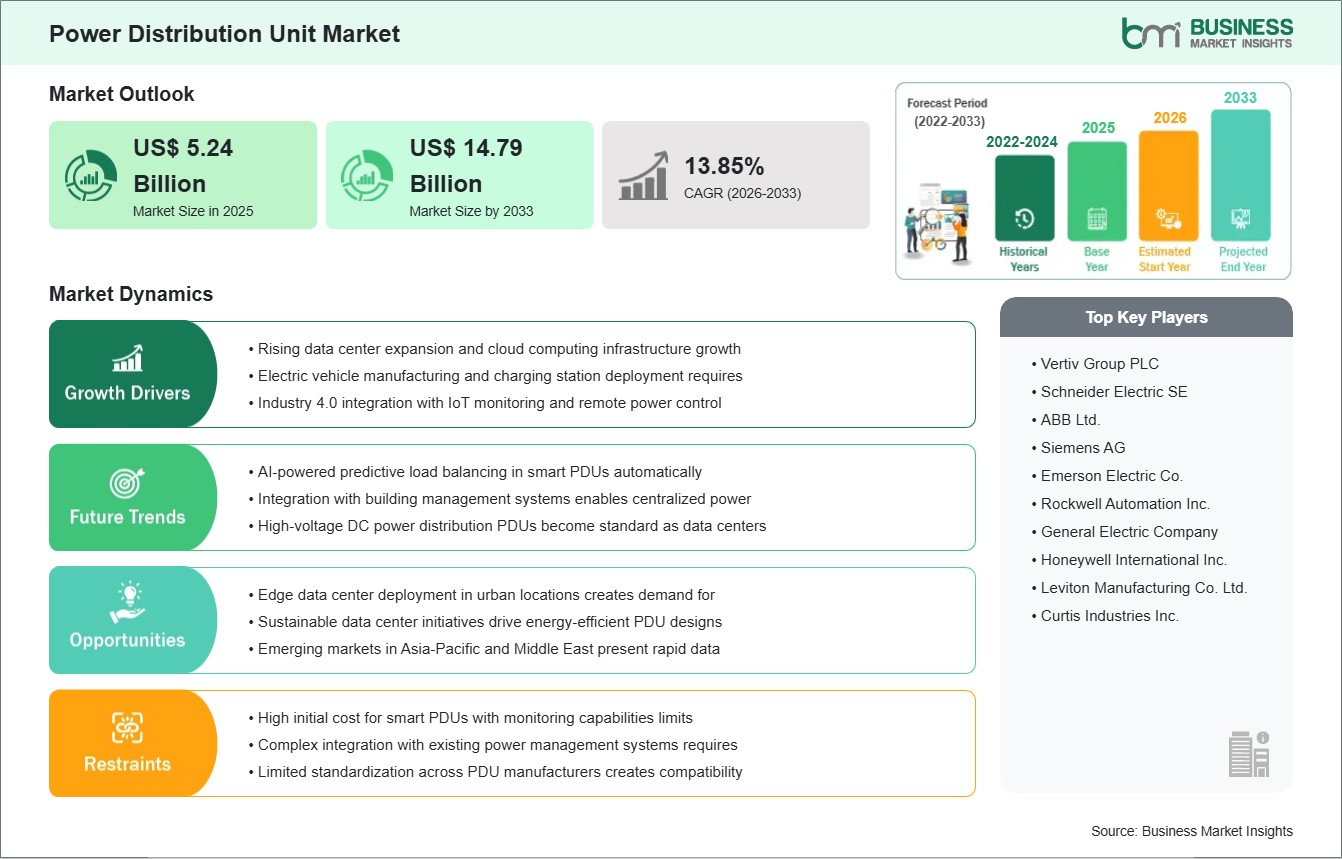

The Power Distribution Unit Market size is expected to reach US$ 14.79 billion by 2033 from US$ 5.24 billion in 2025. The market is estimated to record a CAGR of 13.85% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Power distribution units are electrical devices that distribute, monitor, and manage power delivery from a primary source to multiple downstream loads within controlled environments. They are widely used where equipment density, uptime expectations, and power visibility require more structured distribution architecture than standard outlets or panels can provide. Their function now extends beyond basic delivery, especially in environments where monitoring, switching, and energy oversight influence operational reliability. This makes the category increasingly relevant across digital infrastructure and power-sensitive enterprise facilities.

Market progression is closely connected to the expansion of data-intensive environments and the need for more resilient internal power architecture. Telecom and IT sites, financial institutions, healthcare facilities, manufacturing operations, and public-sector installations are all increasing their attention to uninterrupted power distribution and better load management. As computing density rises and operational continuity becomes more critical, procurement is shifting toward PDUs that offer stronger visibility, control, and adaptability. This transition is reinforcing the value of both conventional and intelligent unit configurations.

Segmentation trends reveal a market shaped by installation format, monitoring capability, and load environment. Basic units continue to serve essential distribution needs, while metered and intelligent configurations are gaining stronger relevance where operators need granular power insight and remote management. Three-phase systems remain especially important in larger commercial and industrial settings because they suit higher-capacity electrical loads and scalable deployment requirements. Rack-mounted designs also occupy a prominent role due to their fit with data center and equipment room infrastructure.

Technology development is moving toward networked monitoring, compact high-density outlet design, and more flexible deployment options. Vendors are increasingly emphasizing remote visibility, environmental monitoring, outlet-level intelligence, and scalable form factors that support changing rack and facility layouts. These advances improve both operational control and energy management in complex installations. The sector is therefore evolving from passive distribution hardware into more connected infrastructure for digital power oversight.

Competitive dynamics are being shaped by intelligent product portfolios, energy-aware features, and solutions tailored to mission-critical environments. Suppliers are competing through outlet innovation, improved interoperability, and greater flexibility in how units are configured and expanded. The market consequently reflects a broader shift toward smarter, more adaptable power distribution ecosystems rather than standardized hardware-only offerings.

Power Distribution Unit Market - Strategic Insights:

Get more information on this report

Power Distribution Unit Market Segmentation Analysis:

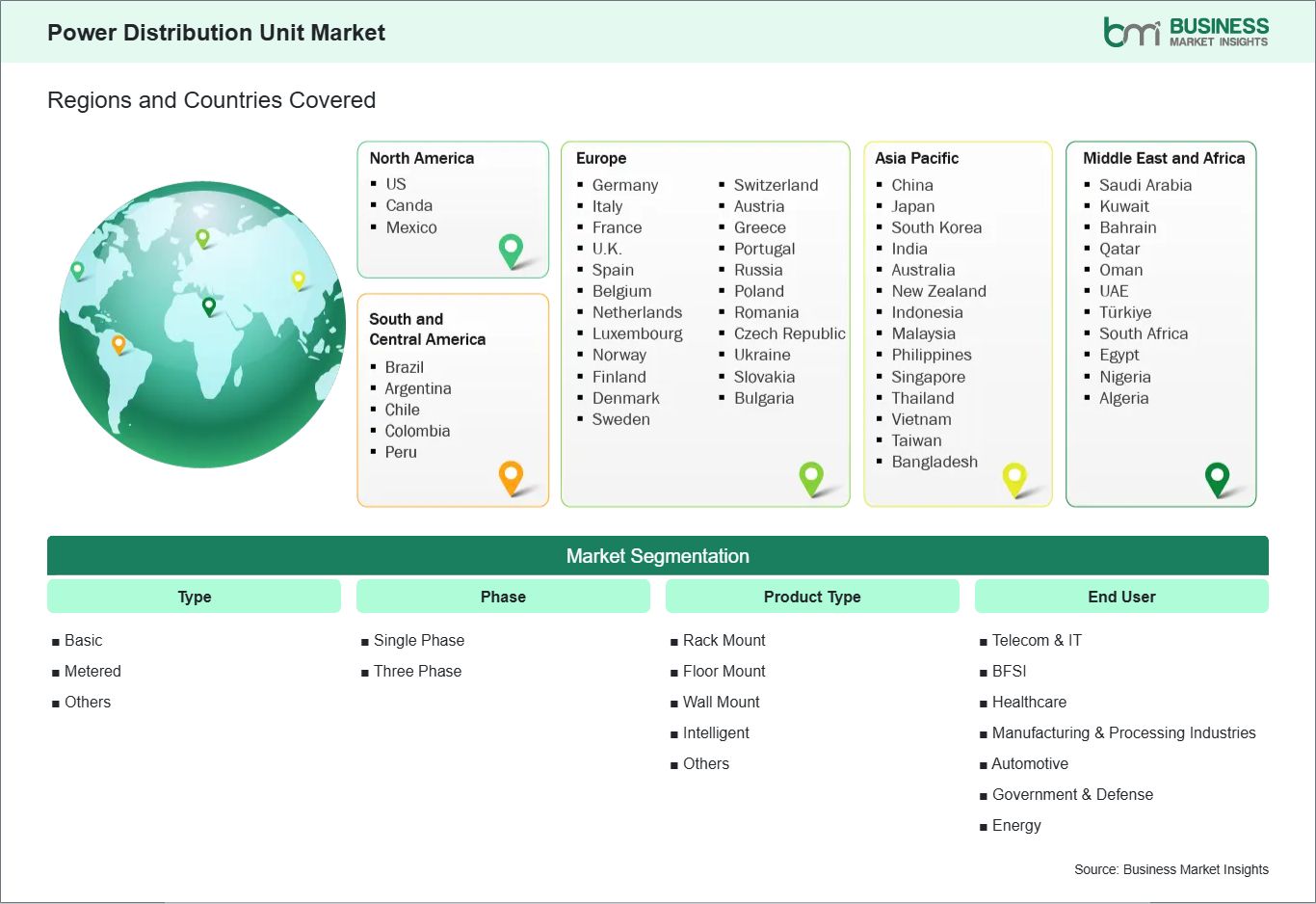

The Power Distribution Unit Market is segmented based on type, phase, product type, end user, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Type

Basic: Delivers straightforward power distribution for stable operational environments.

Metered: Adds load visibility for better energy tracking and capacity planning.

Others: Includes monitored, switched, and advanced configurable unit variants.

By Phase

Single Phase: Fits lighter-duty installations with moderate power requirements.

Three Phase: Supports dense infrastructure and higher-capacity load environments.

By Product Type

Rack Mount: Aligns with server, network, and equipment rack deployments.

Floor Mount: Serves larger installations requiring standalone power distribution placement.

Wall Mount: Conserves floor space in constrained technical environments.

Intelligent: Enables remote monitoring, switching, and operational insight.

Others: Covers specialized product formats for site-specific deployment needs.

By End User

Telecom & IT: Requires structured power distribution for uptime-sensitive digital infrastructure.

BFSI: Prioritizes continuity and monitored power for critical transaction systems.

Healthcare: Supports medical and facility equipment needing stable power access.

Manufacturing & Processing Industries: Protects production systems through managed internal distribution.

Automotive: Uses PDUs within automation-heavy industrial and testing environments.

Government & Defense: Demands reliable and secure power management infrastructure.

Energy: Applies PDUs in operational and control-intensive power environments.

Power Distribution Unit Market Drivers and Opportunities:

Expansion of Power-Dense Digital and Enterprise Infrastructure

Organizations are operating more equipment within limited physical space while placing greater importance on uptime, visibility, and controlled power allocation. This is especially relevant in telecom, IT, BFSI, healthcare, and government environments where internal power distribution must support concentrated loads without compromising reliability. Traditional distribution approaches offer less insight into load balance and downstream consumption patterns, creating a stronger need for purpose-built PDU solutions. As facilities become more power-dense, structured and monitored distribution becomes a more important operational requirement.

The business impact of this shift is evident in procurement preferences across both new and upgraded sites. Operators are increasingly selecting units that improve load monitoring, reduce operational blind spots, and support more efficient infrastructure planning. Rack-mounted, metered, and intelligent PDUs are becoming more relevant because they help facilities manage complexity while maintaining continuity. This strengthens the market’s role in supporting resilient and measurable internal power architecture.

Intelligent and Networked PDUs for Remote Visibility and Flexible Deployment

A major opportunity is emerging through the transition from basic power delivery toward intelligent, connected distribution platforms. Enterprises increasingly want PDUs that provide outlet-level monitoring, remote management, flexible input options, and compatibility with broader environmental or infrastructure oversight systems. This need is especially pronounced in data centers and high-availability enterprise environments where operators must optimize capacity, energy use, and service response. Intelligent and interoperable PDUs therefore offer a stronger value proposition than fixed-function distribution hardware.

Future scope expands as distributed computing, edge deployments, and high-density racks reshape electrical requirements inside facilities. Networked PDUs that support scalable installation, remote diagnostics, and flexible outlet utilization are well-positioned to meet these demands. As organizations modernize digital infrastructure and seek tighter operational control, intelligent products can capture a larger share of spending across both centralized and distributed sites. This creates attractive opportunity across telecom, IT, BFSI, healthcare, and industrial control environments.

Power Distribution Unit Market Size and Share Analysis:

The Power Distribution Unit Market is projected to grow from US$ 5.24 billion in 2025 to US$ 14.79 billion by 2033. The market is estimated to record a CAGR of 13.85% from 2026 to 2033.

This growth path indicates a market supported by the spread of power-sensitive digital infrastructure, stronger interest in monitored distribution, and broader demand for resilient internal electrical architecture. It also reflects the shift toward more intelligent and adaptable unit configurations.

By type, phase, and product format, metered and intelligent solutions hold increasing strategic importance because operators want better visibility and control over distributed loads. Three-phase and rack-mount configurations also maintain strong commercial relevance in dense and technically demanding environments. Basic and single-phase units continue to serve practical needs where complexity and monitoring requirements are lower.

By end user, Telecom & IT represents the strongest demand center due to its concentration of uptime-sensitive and rack-based equipment. BFSI, healthcare, and government environments also maintain strong relevance because of their dependence on continuity and monitored electrical infrastructure. Manufacturing, automotive, and energy applications broaden the market through industrial and control-oriented use cases.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Vertiv Group PLC

Schneider Electric SE

ABB Ltd.

Siemens AG

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Leviton Manufacturing Co. Ltd.

Curtis Industries Inc.

Get more information on this report

Power Distribution Unit Market Report Coverage and Deliverables:

The "Power Distribution Unit Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Power Distribution Unit Market Geographic Insights:

The Power Distribution Unit market shows diverse regional adoption patterns influenced by data infrastructure density, power reliability needs, digital transformation, and enterprise facility modernization. Across the global landscape, market development is shaped by the need for safer and more controllable internal power distribution in rack-based, equipment-dense, and uptime-sensitive environments. Regional differences largely reflect digital infrastructure maturity and the pace of intelligent electrical system deployment.

North America remains a leading market because operators in the region continue upgrading data center, enterprise, and institutional infrastructure with monitored and intelligent distribution equipment. Strong demand is supported by the concentration of telecom, IT, BFSI, and healthcare environments that require reliable rack-level and facility-level power management. The region also shows stronger alignment with advanced PDUs that offer remote visibility and higher operational flexibility.

Asia Pacific presents a robust expansion environment as cloud adoption, digital services growth, and enterprise infrastructure investment continue to broaden. Demand is reinforced by data center development, telecom expansion, and industrial digitalization across major economies in the region. This creates strong relevance for scalable rack-mounted, three-phase, and intelligent PDU solutions across both centralized and distributed facilities.

Europe reflects a more efficiency- and compliance-led pattern, with emphasis on energy-aware infrastructure, operational resilience, and structured electrical management within advanced facilities. Enterprises in the region are increasingly attentive to intelligent distribution systems that support monitoring, optimization, and adaptable deployment. Beyond these major regions, emerging markets offer additional opportunity as digital infrastructure expands and organizations strengthen internal power management across critical sectors.

Get more information on this report

Power Distribution Unit Market Research Report Guidance:

The Power Distribution Unit market report includes qualitative and quantitative data in the Power Distribution Unit Market across type, phase, product type, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Power Distribution Unit Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Power Distribution Unit Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Power Distribution Unit Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover Power Distribution Unit Market segments by type, phase, product type, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the Power Distribution Unit Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Power Distribution Unit Market News and Key Development:

The Power Distribution Unit Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In June 2026, Vision Marine has improved the manufacturability of its E-Motion Power Distribution Unit and engaged a contract manufacturer to support production planning for a key high-voltage component. The work strengthens E-Motion manufacturing readiness and supports the platform's roadmap toward future compatibility with fast-charging infrastructure for higher-use applications, including commercial operators, boat clubs, rental fleets and marina environments.

In September 2025, Vertiv, a global leader in critical digital infrastructure, today announced the new Vertiv™ PowerIT rack power distribution units (PDU), an extension of the Vertiv PowerIT product line. These models are designed to address the rising power needs of data-intensive workloads, including AI and high-performance computing (HPC). They provide advanced power management, flexible configurations, and enhanced internal components for greater reliability, enabling data centres to seamlessly scale power in response to growing IT demands. Basic, monitored and switched models are available now in North America, Europe, the Middle East and Africa (EMEA).

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Power Distribution Unit Market

Vertiv Group PLC

Schneider Electric SE

ABB Ltd.

Siemens AG

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Leviton Manufacturing Co. Ltd.

Curtis Industries Inc.

Frequently Asked Questions

How big is the Power Distribution Unit Market?

The Power Distribution Unit Market is valued at US$ 5.24 Billion in 2025, it is projected to reach US$ 14.79 Billion by 2033.

What is the CAGR for Power Distribution Unit Market by (2026 - 2033)?

As per our report Power Distribution Unit Market, the market size is valued at US$ 5.24 Billion in 2025, projecting it to reach US$ 14.79 Billion by 2033. This translates to a CAGR of approximately 13.85% during the forecast period.

What segments are covered in this report?

The Power Distribution Unit Market report typically cover these key segments-

Type (Basic, Metered, Others)

Phase (Single Phase, Three Phase)

Product Type (Rack Mount, Floor Mount, Wall Mount, Intelligent, and Others)

End User (Telecom & IT, BFSI, Healthcare, Manufacturing & Processing Industries, Automotive, Government & Defense, Energy)

What is the historic period, base year, and forecast period taken for Power Distribution Unit Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Power Distribution Unit Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Power Distribution Unit Market?

The Power Distribution Unit Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Vertiv Group PLC

Schneider Electric SE

ABB Ltd.

Siemens AG

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Leviton Manufacturing Co. Ltd.

Curtis Industries Inc.

Who should buy this report?

The Power Distribution Unit Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Power Distribution Unit Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Power Distribution Unit Market

Get Free Sample For Power Distribution Unit Market