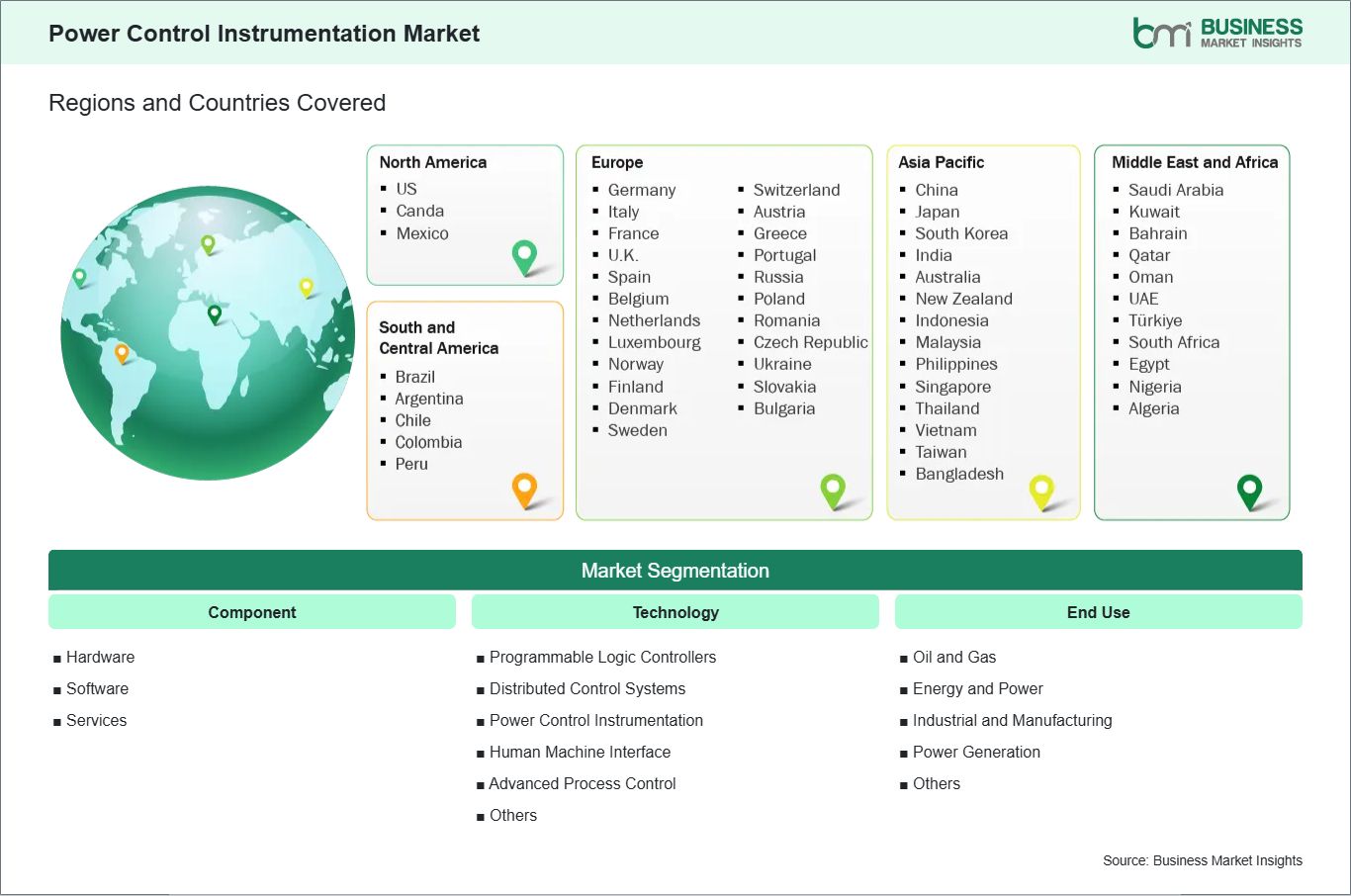

Technology (Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Power Control Instrumentation, Human Machine Interface (HMI), Advanced Process Control (APC), Others)

End Use (Oil and Gas, Energy and Power, Industrial and Manufacturing, Power Generation, Others)

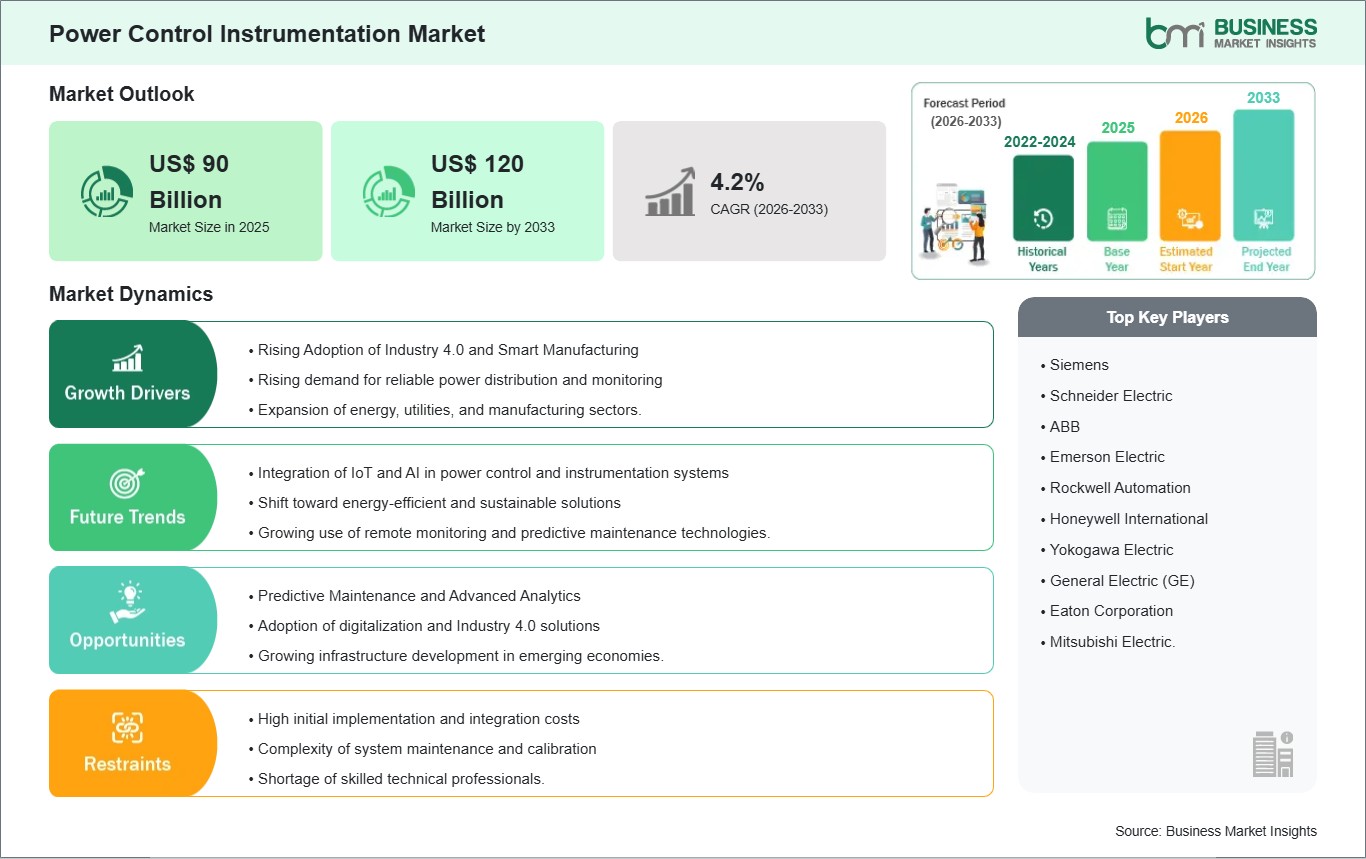

The Power Control Instrumentation Market size is expected to reach US$ 120 Billion by 2033 from US$ 90 Billion in 2025. The market is estimated to record a CAGR of 3.66% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Power Control Instrumentation is altering global industrial production by providing real-time monitoring, automation, and data-driven decision-making. Its popularity is growing in areas like as automotive, electronics, medicines, consumer products, and energy. The integration of IoT, AI, robotics, and digital twins has made formerly time-consuming and error-prone processes more efficient. These technologies increase productivity, minimize downtime, improve product quality, and enable faster reactions to changes in demand or production requirements. Rising demand for mass customisation, Industry 4.0 initiatives, and flexible manufacturing methods are all important drivers of market growth. Furthermore, advances in predictive maintenance, cloud-based analytics, and smart supply chain integration are increasing operational efficiency, allowing firms to reduce inefficiencies while gaining a competitive advantage.

On the other hand, market expansion faces several hurdles. High initial technological investments, challenges in integrating historical systems with current instrumentation, cyber-security issues, and a scarcity of experienced workers in sophisticated manufacturing technologies can all hinder adoption. Regulatory compliance and a lack of standardization in some places also stifle market growth. Despite these challenges, the sector still has enormous prospects. The adoption of energy-efficient and sustainable manufacturing methods, the expansion of smart factory setups in emerging economies, and the application of AI-driven optimization to reduce costs and increase productivity are all projected to boost growth. Overall, the Power Control Instrumentation market is expected to grow steadily in the long run as businesses continue to engage in digitalization, industrial automation, and smart manufacturing technologies.

Power Control Instrumentation Market - Strategic Insights:

Get more information on this report

Power Control Instrumentation Market Segmentation Analysis:

Key segments that contributed to the derivation of the Power Control Instrumentation market analysis are component, technology, and end use.

By Component, the Power Control Instrumentation market is divided into Hardware, Software, and Services. The hardware segment dominated the market in 2024, fueled by increasing investments in IoT sensors, robotics, and automation equipment, which are essential for enabling real-time monitoring and control in industrial operations.

By Technology, the market is categorized into Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Power Control Instrumentation, Human Machine Interface (HMI), Advanced Process Control (APC), Machine Execution Systems (MES), and Others. Machine Execution Systems (MES) held the largest share in 2024, as manufacturers focused on real-time production monitoring, efficiency optimization, predictive maintenance, and quality control.

By End Use, the market is segmented into Oil and Gas, Energy and Power, Industrial and Manufacturing, Power Generation, Automotive, and Others. The automotive sector accounted for the largest market share in 2024, reflecting strong adoption of automation, robotics, connected manufacturing solutions, and digital twin technologies to enable flexible and efficient production.

Power Control Instrumentation Market Drivers and Opportunities:

Rising Adoption of Industry 4.0 and Smart Manufacturing

The global manufacturing industry has undergone a transformational transition characterized by major changes brought about by the emergence of Industry 4.0 as it embraces the integration of the Internet of Things (IoT), artificial intelligence (AI), big data analytics, cloud computing, and other innovative technologies to facilitate the automation, interconnectivity, and intelligent decision-making based on real-time data. The implementation of advanced instrumentation systems provides manufacturers with the ability to monitor and control their manufacturing processes in real-time through the deployment of intelligent sensors and intelligent controllers, capable of receiving instantaneous input from these devices regarding operational conditions and events throughout the manufacturing process.

Through collecting accurate production data throughout the manufacturing process, manufacturers can obtain real-time information regarding their manufacturing operations, enabling them to effectively manage their assets (equipment and materials) as well as enabling them to perform predictive maintenance which will help prevent equipment failure and minimize both the amount of downtime and associated costs incurred by maintaining the equipment.

Predictive Maintenance and Advanced Analytics

With the rising complexity of modern industrial operations, unscheduled equipment downtime has become a key business risk, affecting productivity, operational efficiency, and profitability. When combined with predictive maintenance technologies, power control instrumentation enables businesses to monitor equipment health in real time and discover early warning signals of probable breakdowns before they cause costly disruptions. Advances in AI-driven analytics, machine learning, and cloud computing allow predictive maintenance systems to evaluate massive volumes of operational data—from sensors, controllers, and machinery—and discover patterns, anomalies, and performance trends. This enables producers to schedule maintenance in advance rather than reactively, avoiding unexpected downtime, maximizing spare parts inventory, and prolonging the lives of important assets.

Power Control Instrumentation Market Size and Share Analysis:

By Component, the Power Control Instrumentation market is divided into Hardware, Software, and Services. The hardware segment dominated the market in 2024, fueled by increasing investments in IoT sensors, robotics, and automation equipment, which are essential for enabling real-time monitoring and control in industrial operations. Hardware forms the backbone of power control systems, enabling real-time monitoring, precise control, and seamless integration across industrial operations.

By Technology, the market is categorized into Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Power Control Instrumentation, Human Machine Interface (HMI), Advanced Process Control (APC), Machine Execution Systems (MES), and Others. Machine Execution Systems (MES) held the largest share in 2024, as manufacturers focused on real-time production monitoring, efficiency optimization, predictive maintenance, and quality control. MES platforms enable seamless coordination between production, supply chain, and operational resources, ensuring timely decision-making and optimized throughput.

By End Use, the market is segmented into Oil and Gas, Energy and Power, Industrial and Manufacturing, Power Generation, Automotive, and Others. The automotive sector accounted for the largest market share in 2024, reflecting strong adoption of automation, robotics, connected manufacturing solutions, and digital twin technologies to enable flexible and efficient production. These technologies enable flexible, efficient, and high-quality production lines, meeting the growing demand for mass customization and faster time-to-market in the automotive industry.

Power Control Instrumentation Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Siemens

Schneider Electric

ABB

Emerson Electric

Rockwell Automation

Honeywell International

Yokogawa Electric

General Electric (GE)

Eaton Corporation

Mitsubishi Electric.

Get more information on this report

Power Control Instrumentation Market Report Coverage and Deliverables:

The Power Control Instrumentation Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Power Control Instrumentation market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Power Control Instrumentation market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Power Control Instrumentation market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Power Control Instrumentation market

Detailed company profiles, including SWOT analysis

Power Control Instrumentation Market Geographic Insights:

The geographical scope of the Power Control Instrumentation market report is divided into five regions: North America, Asia Pacific, Europe, Middle East &; Africa, and South & Central America. The Power Control Instrumentation market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia, Pacific Power Control Instrumentation market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The primary driver of growth in this region is the rising industrial output, huge investments in the Industry 4.0 technologies, and government initiatives that encourage the adoption of automation, digitalization as well as smart factory development.

The demand is very high in sectors such as automotive, electronics, pharmaceuticals, food & beverages, and consumer goods. The market growth is facilitated through investments in advanced manufacturing infrastructures, mainly robotics, predictive maintenance systems, and data, driven production platforms. The combined efforts of governments, technology providers, and manufacturing companies to innovation, workforce upskilling, and the adoption of smart factory ecosystems further facilitate the market growth.

Get more information on this report

Power Control Instrumentation Market Research Report Guidance:

The report includes qualitative and quantitative data in the Power Control Instrumentation market across component, technology, and end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Power Control Instrumentation market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Power Control Instrumentation market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Power Control Instrumentation market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 10 cover Power Control Instrumentation market segments by type, destination, and end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Power Control Instrumentation market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

Power Control Instrumentation Market News and Key Development:

The Power Control Instrumentation market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Power Control Instrumentation market are:

In April 2025, ABB introduced high performance versatile pressure transmitters to US market. ABB’s new P-300 versatile pressure transmitter series is now available in the United States, ensuring high accuracy and ease of use over a broad range of applications in the petrochemical, chemical, power, pulp and paper, and other industrial sectors.

In November 2024, Tektronix announced a new lineup of breakthrough power devices set to accelerate innovation in industries demanding greater power capacity and efficiency. The new TICP Series IsoVu™ isolated current probes are the world's first to utilize RF isolation, delivering exceptional precision and safety when measuring fast-changing current across both low- and high-voltage systems. The EA-PSB 20000 Triple series is a 3-channel, bidirectional power supply and electronic load with energy recovery that delivers higher test coverage, density, and capacity across multiple channels within a single device.

Key Sources Referred:

International Federation of Robotics (IFR)World Economic Forum (WEF) – Future of Manufacturing ReportsInternational Energy Agency (IEA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Power Control Instrumentation Market

Siemens

Schneider Electric

ABB

Emerson Electric

Rockwell Automation

Honeywell International

Yokogawa Electric

General Electric (GE)

Eaton Corporation

Mitsubishi Electric.

Frequently Asked Questions

How big is the Power Control Instrumentation Market?

The Power Control Instrumentation Market is valued at US$ 90 Billion in 2025, it is projected to reach US$ 120 Billion by 2033.

What is the CAGR for Power Control Instrumentation Market by (2026 - 2033)?

As per our report Power Control Instrumentation Market, the market size is valued at US$ 90 Billion in 2025, projecting it to reach US$ 120 Billion by 2033. This translates to a CAGR of approximately 3.66% during the forecast period.

What segments are covered in this report?

The Power Control Instrumentation Market report typically cover these key segments-

Component (Hardware, Software, Services)

Technology (Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Power Control Instrumentation, Human Machine Interface (HMI), Advanced Process Control (APC), Others)

End Use (Oil and Gas, Energy and Power, Industrial and Manufacturing, Power Generation, Others)

What is the historic period, base year, and forecast period taken for Power Control Instrumentation Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Power Control Instrumentation Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Power Control Instrumentation Market?

The Power Control Instrumentation Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Siemens

Schneider Electric

ABB

Emerson Electric

Rockwell Automation

Honeywell International

Yokogawa Electric

General Electric (GE)

Eaton Corporation

Mitsubishi Electric.

Who should buy this report?

The Power Control Instrumentation Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Power Control Instrumentation Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Power Control Instrumentation Market

Get Free Sample For Power Control Instrumentation Market