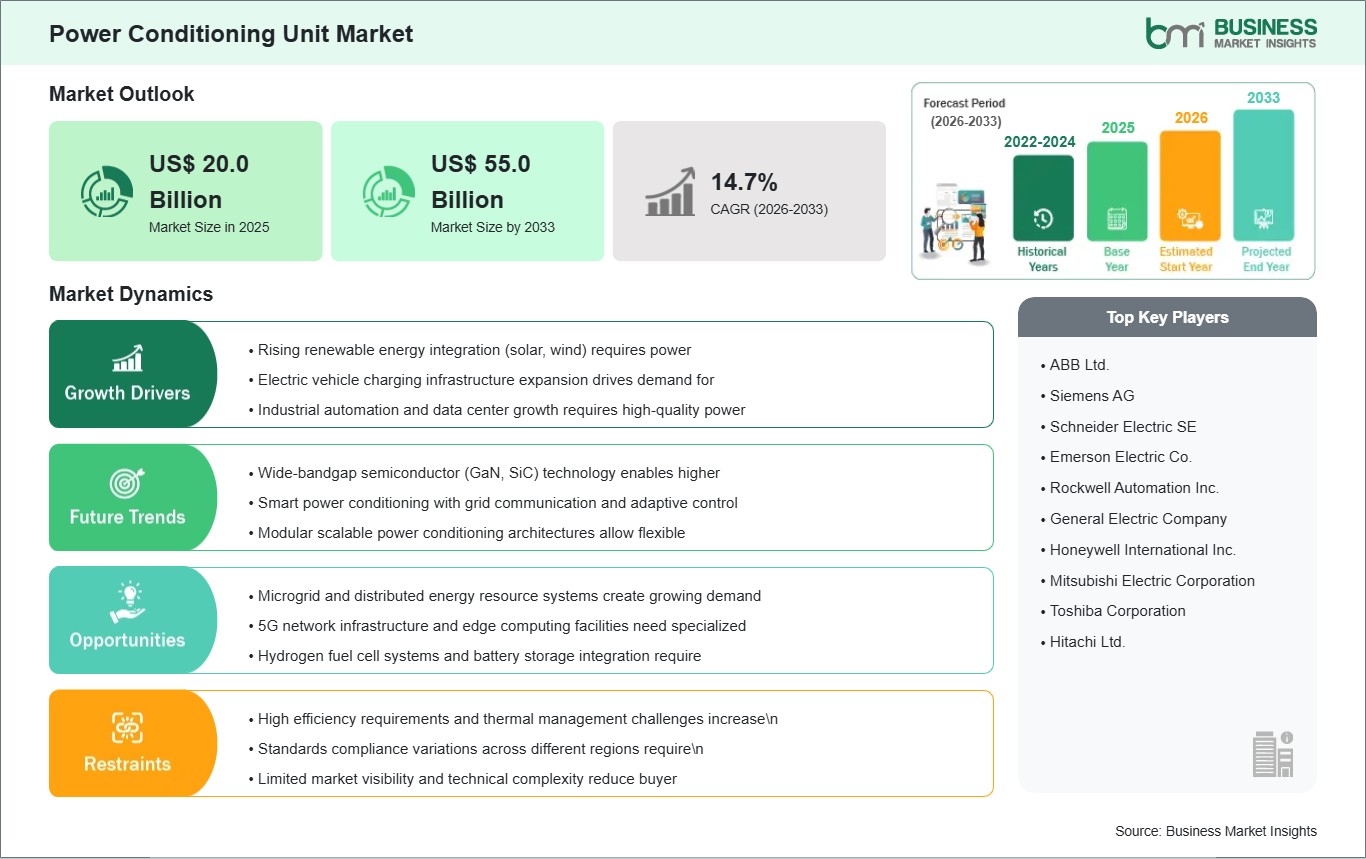

The Power Conditioning Unit Market size is expected to reach US$ 55.0 billion by 2033 from US$ 20.0 billion in 2025. The market is estimated to record a CAGR of 14.7% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Power conditioning units are electrical systems designed to stabilize, regulate, filter, and optimize power supplied to sensitive loads and mission-critical equipment. They address disturbances such as voltage fluctuation, harmonics, transients, and waveform irregularities that can impair performance or shorten asset life. Their relevance has expanded as digital infrastructure, automated facilities, medical systems, and electrified transport networks become more dependent on reliable power quality. This positions the sector as an important layer between unstable supply conditions and performance-sensitive end-use systems.

Market momentum is being shaped by the rising operational cost of poor power quality across commercial, industrial, and institutional environments. Modern facilities increasingly rely on electronically controlled equipment that is more vulnerable to distortion, interruptions, and unstable voltage conditions. As energy systems become more decentralized and load profiles more complex, users are placing greater emphasis on conditioning solutions that can protect assets and maintain continuity. This is reinforcing procurement interest across both retrofit and new-installation environments.

Segment patterns reflect differences in performance requirement and installation scale. Active units hold a strong position where dynamic correction, harmonic filtering, and precise regulation are necessary, while passive units remain relevant in simpler or more cost-sensitive applications. By phase, three-phase systems are especially important in commercial buildings, industrial facilities, and transport-related infrastructure where larger loads and complex electrical environments are common. Single-phase units retain a meaningful role in residential and smaller commercial settings.

Technology development is moving toward smarter power management, broader monitoring capability, and tighter integration with efficient electrical infrastructure. Product innovation increasingly combines protection, digital visibility, and energy-conscious operation to support demanding loads in industrial and commercial environments. Advanced systems are also being designed to manage wider voltage ranges and lower harmonic distortion, reflecting the need for conditioned power in more variable operating conditions. This raises the strategic importance of product performance beyond traditional backup or protection functions.

Competitive conditions are shaped by the ability to address multiple power quality problems within increasingly sophisticated end-use environments. Suppliers are differentiating through digital control, application-specific reliability, and solutions aligned with commercial, industrial, and critical-facility requirements. The market therefore reflects a shift from basic electrical protection toward more intelligent and integrated power quality infrastructure.

Power Conditioning Unit Market - Strategic Insights:

Get more information on this report

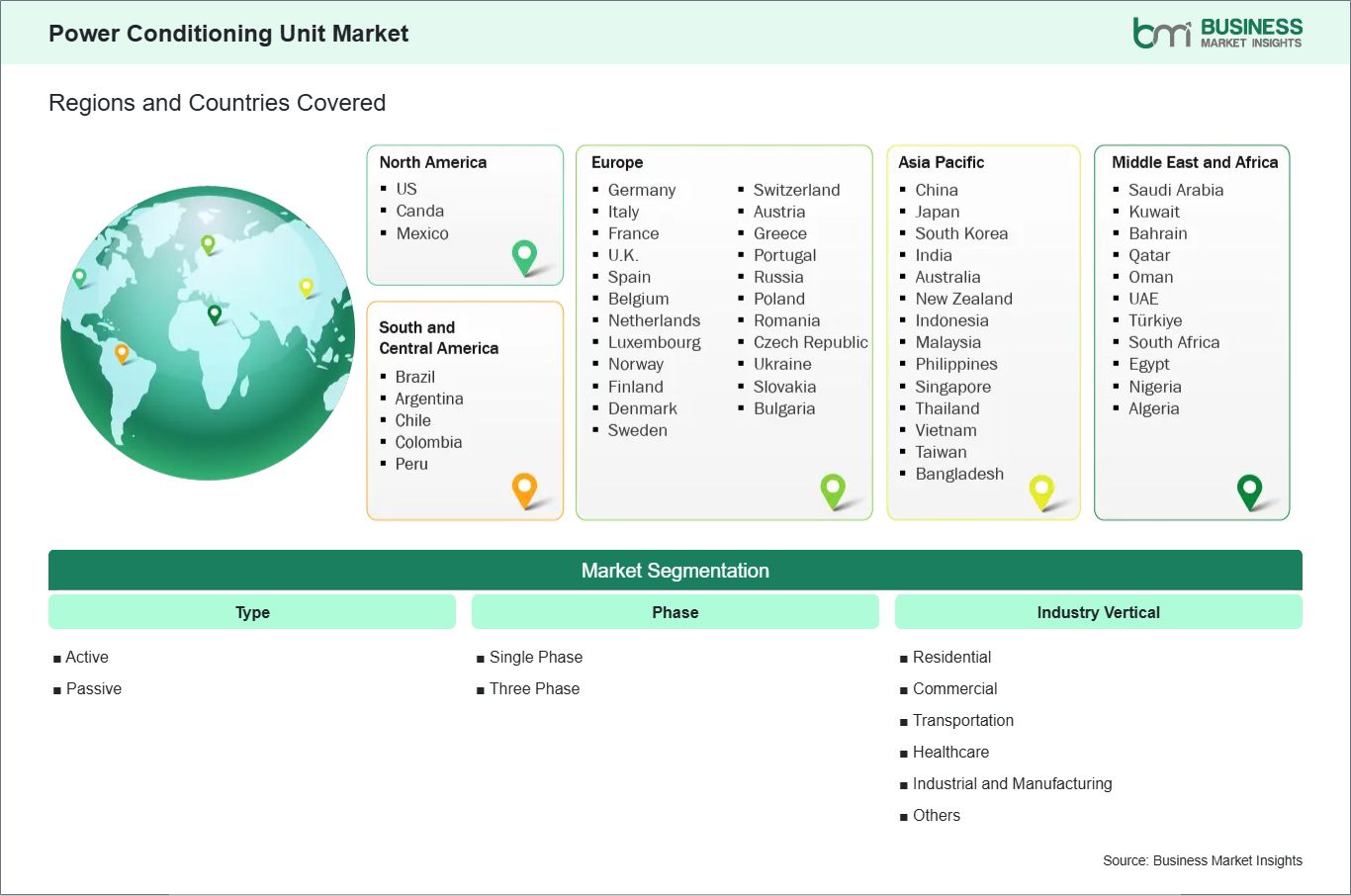

Power Conditioning Unit Market Segmentation Analysis:

The Power Conditioning Unit Market is segmented based on Type, Phase, Industry Vertical, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Type

Active: Provides dynamic compensation for harmonics, voltage variation, and power quality events.

Passive: Offers stable filtering for less complex electrical correction needs.

By Phase

Single Phase: Fits smaller installations with moderate load sensitivity.

Three Phase: Supports complex facilities requiring higher-capacity conditioned power.

By Industry Vertical

Residential: Serves homes using sensitive electronics and connected energy systems.

Commercial: Protects offices, retail sites, and digital infrastructure assets.

Transportation: Supports electrified mobility systems and transport power reliability.

Healthcare: Safeguards medical devices requiring stable and clean electricity.

Industrial and Manufacturing: Secures automated equipment from costly power disturbances.

Others: Covers additional sectors with power quality management requirements.

Power Conditioning Unit Market Drivers and Opportunities:

Greater Exposure to Power Quality Disturbances in Digitized Facilities

Electrical environments are becoming more demanding as facilities deploy automation, digital controls, connected equipment, and electronically sensitive loads. These systems can be affected by harmonics, voltage sags, transients, and waveform instability that conventional supply arrangements do not always mitigate effectively. This creates a stronger need for power conditioning units that can regulate supply quality and reduce risk to operationally important equipment. The requirement is especially visible in settings where downtime, data loss, or equipment degradation carries significant financial or safety consequences.

The market effect extends across commercial complexes, healthcare facilities, industrial plants, and transportation-linked infrastructure. Operators in these environments are prioritizing conditioning solutions not only for protection, but also for continuity and predictable equipment behavior under variable load conditions. This makes power conditioning units more relevant as facilities modernize and integrate more advanced electrical assets. Their commercial value increasingly lies in protecting system performance rather than merely correcting occasional anomalies.

Intelligent Conditioning Solutions for High-Sensitivity and High-Growth Applications

A significant opportunity is emerging through the shift toward smarter and more application-focused power quality infrastructure. End users increasingly want conditioning systems that combine regulation, monitoring, energy efficiency, and broader compatibility with mission-critical operations. This creates room for solutions tailored to industrial automation, commercial reliability, healthcare systems, and data-intensive environments where electrical disturbances can cause disproportionate disruption. Intelligent conditioning platforms are therefore gaining strategic importance in facilities that need both power protection and operational visibility.

Future scope is strengthened by the expansion of electrified infrastructure, distributed energy environments, and higher-density digital loads. As users connect more sensitive systems to increasingly complex electrical networks, the need for adaptable active conditioning solutions becomes more pronounced. This supports wider deployment across three-phase installations and technically demanding sectors where conditioned power supports uptime, efficiency, and asset protection. The market’s opportunity therefore extends beyond correction into broader electrical optimization.

Power Conditioning Unit Market Size and Share Analysis:

The Power Conditioning Unit Market size is expected to reach US$ 55.0 billion by 2033 from US$ 20.0 billion in 2025. The market is estimated to record a CAGR of 14.7% from 2026 to 2033.

This growth path indicates a market supported by the rising importance of power quality across digitally intensive and electrically complex end-use settings. It also reflects the increasing role of conditioning infrastructure in maintaining continuity and equipment integrity.

By type and phase, active systems hold a strong commercial position where dynamic correction and advanced filtering are required for sensitive loads. Three-phase units also maintain greater strategic importance in larger facilities due to their compatibility with commercial and industrial electrical configurations. Passive and single-phase products remain relevant in less complex or smaller-scale applications.

By industry vertical, industrial and manufacturing and commercial environments account for substantial demand because they rely heavily on automation, controlled processes, and uptime-sensitive electrical assets. Healthcare also represents a significant application area due to the need for stable power in clinically critical settings. Transportation and residential segments add further market depth as electrification and connected systems expand.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

ABB Ltd.

Siemens AG

Schneider Electric SE

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Mitsubishi Electric Corporation

Toshiba Corporation

Hitachi Ltd.

Get more information on this report

Power Conditioning Unit Market Report Coverage and Deliverables:

The "Power Conditioning Unit Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Power Conditioning Unit Market Geographic Insights:

The Power Conditioning Unit market shows diverse regional adoption patterns influenced by grid quality conditions, electrical infrastructure modernization, digital load intensity, and industrial power reliability requirements. Across the global landscape, demand is rising where facilities need better protection against harmonic distortion, voltage instability, and operational disruption linked to poor power quality. Regional differences reflect the pace of electrification, industrial automation, and investment in mission-critical infrastructure.

North America reflects a mature but evolving market where commercial buildings, healthcare facilities, and industrial sites are investing in more intelligent power quality solutions. The region’s strong base of sensitive digital and operational equipment supports continued demand for active conditioning technologies and three-phase installations. Equipment selection increasingly favors solutions that combine monitoring, efficiency, and robust protection under variable load conditions.

Asia Pacific presents a strong expansion environment because the region combines industrial capacity growth, infrastructure development, and rising deployment of advanced electrical equipment. Demand is reinforced by the need to stabilize power in commercial, industrial, and transport-related settings where load complexity is increasing. This supports stronger relevance for both active and phase-specific conditioning systems across new and upgraded installations.

Europe shows a more efficiency- and compliance-oriented pattern shaped by advanced infrastructure, strict operational standards, and broader emphasis on energy-aware electrical systems. Conditioning technologies in the region are increasingly linked to resilient facility design and improved performance in complex power environments. Beyond the major regions, emerging markets offer additional opportunity where power instability, facility expansion, and industrial modernization create stronger need for conditioned electrical supply.

Get more information on this report

Power Conditioning Unit Market Research Report Guidance:

The Power Conditioning Unit market report includes qualitative and quantitative data in the Power Conditioning Unit Market across Type, Phase, Industry Vertical, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Power Conditioning Unit Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Power Conditioning Unit Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Power Conditioning Unit Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Power Conditioning Unit Market segments by Type, Phase, Industry Vertical, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Power Conditioning Unit Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Power Conditioning Unit Market News and Key Development:

The Power Conditioning Unit Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In March 2026, Vertiv (NYSE: VRT), a global leader in critical digital infrastructure, today announced the Vertiv™ PowerUPS 6000 Industrial uninterruptible power supply (UPS) system, designed to deliver reliable power protection for commercial and industrial (C&I) markets. The solution supports operations for industries including manufacturing, transportation, oil and gas, pharmaceuticals, food and beverage, packaging, and steel.

In March 2025, Intelligent power management company Eaton is showcasing its latest innovations at Elecrama 2025, reinforcing its commitment to sustainable, efficient, and customer-centric power solutions. With a strong focus on Make in India, Eaton unveils cutting-edge products designed to enhance reliability and performance across critical applications, including data centers, renewable energy, and industrial power distribution.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Power Conditioning Unit Market

ABB Ltd.

Siemens AG

Schneider Electric SE

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Mitsubishi Electric Corporation

Toshiba Corporation

Hitachi Ltd.

Frequently Asked Questions

How big is the Power Conditioning Unit Market?

The Power Conditioning Unit Market is valued at US$ 20.0 Billion in 2025, it is projected to reach US$ 55.0 Billion by 2033.

What is the CAGR for Power Conditioning Unit Market by (2026 - 2033)?

As per our report Power Conditioning Unit Market, the market size is valued at US$ 20.0 Billion in 2025, projecting it to reach US$ 55.0 Billion by 2033. This translates to a CAGR of approximately 14.7% during the forecast period.

What segments are covered in this report?

The Power Conditioning Unit Market report typically cover these key segments-

Type (Active, Passive)

Phase (Single Phase, Three Phase)

Industry Vertical (Residential, Commercial, Transportation, Healthcare, Industrial and Manufacturing, and Others)

What is the historic period, base year, and forecast period taken for Power Conditioning Unit Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Power Conditioning Unit Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Power Conditioning Unit Market?

The Power Conditioning Unit Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB Ltd.

Siemens AG

Schneider Electric SE

Emerson Electric Co.

Rockwell Automation Inc.

General Electric Company

Honeywell International Inc.

Mitsubishi Electric Corporation

Toshiba Corporation

Hitachi Ltd.

Who should buy this report?

The Power Conditioning Unit Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Power Conditioning Unit Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Power Conditioning Unit Market

Get Free Sample For Power Conditioning Unit Market