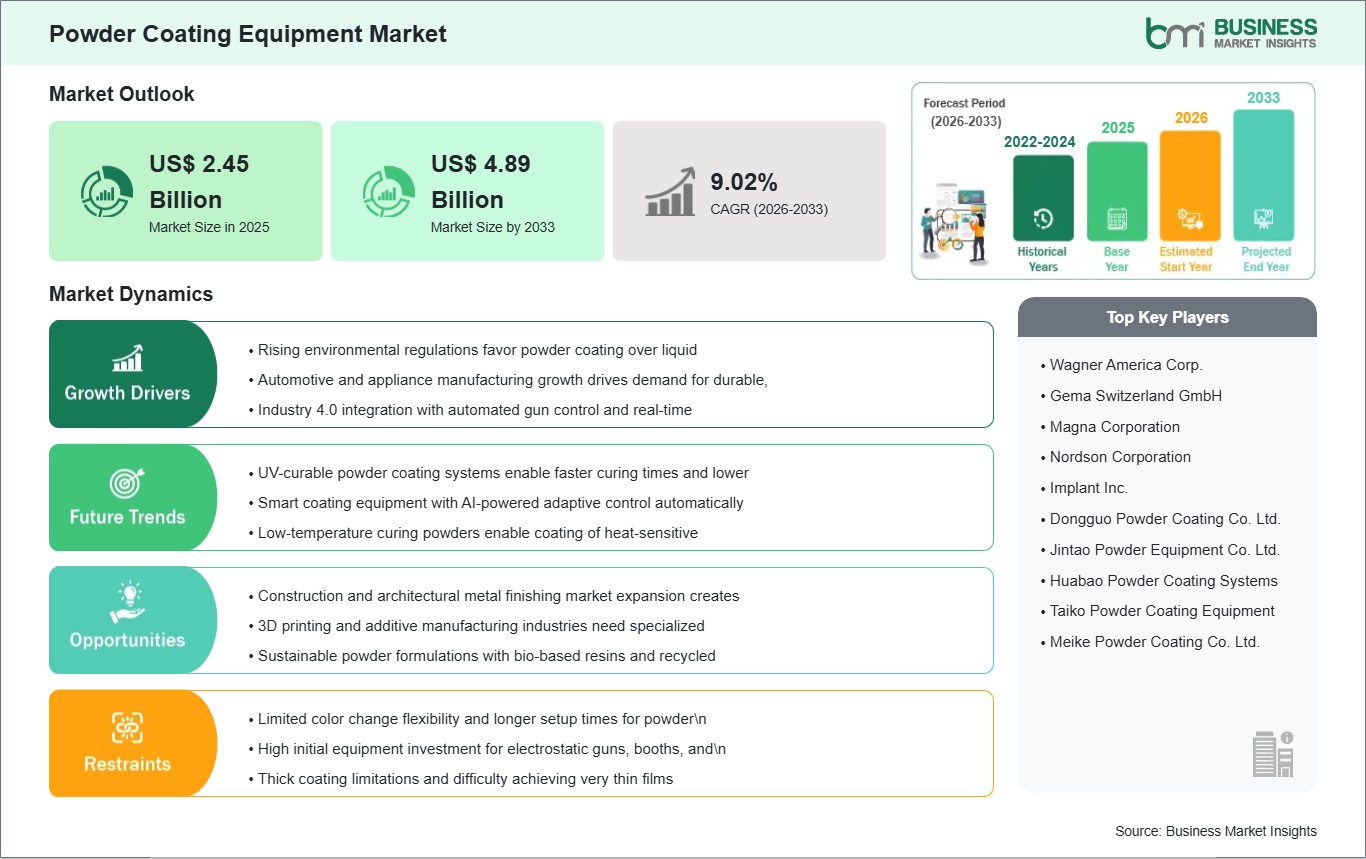

The Powder Coating Equipment Market size is expected to reach US$ 4.89 billion by 2033 from US$ 2.45 billion in 2025. The market is estimated to record a CAGR of 9.02% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Powder coating equipment includes the machinery and application systems used to produce, convey, apply, recover, and cure dry coating materials on metal and other substrates. These systems span upstream production components such as extruders, kneaders, grinders, and cooling equipment, alongside downstream spray and finishing infrastructure. Their industrial relevance stems from the need for durable surface finishing, material efficiency, and lower-emission coating processes across high-volume manufacturing environments. This positions the sector at the intersection of industrial automation, surface engineering, and environmental compliance.

Market advancement is tied to the continued preference for efficient finishing systems that can support high throughput and coating consistency. Manufacturers in automotive, construction, aerospace, and general industrial operations are prioritizing equipment that improves transfer efficiency, minimizes overspray losses, and integrates more effectively with automated production lines. Powder coating equipment aligns with these requirements because it supports repeatable finishing quality while reducing solvent-related process burdens. As industrial users modernize coating lines, equipment demand is becoming more closely linked to productivity and sustainability objectives.

Segmentation trends reveal a market shaped by both process-stage needs and end-use coating performance. Extruders, kneaders, grinders, and cooling systems remain critical within powder production workflows, while resin compatibility influences downstream equipment requirements and process configuration. Polyester and epoxy-based applications continue to anchor many industrial finishing environments due to their broad utility across fabricated components and engineered surfaces. From an industry perspective, automotive and general industrial use remain central because they combine scale, repeatability requirements, and broad coating line deployment.

Technology development is now centered on automation, precision control, and application efficiency. Suppliers are emphasizing smarter powder delivery, tighter process monitoring, and more advanced test environments to support consistent coating performance across complex geometries and high-mix production settings. Improvements in laboratory capability, system integration, and automated application platforms are reinforcing the shift toward more engineered coating operations. This evolution is strengthening the role of equipment selection in broader manufacturing optimization efforts.

Competitive activity reflects a market where innovation, system integration, and service support shape differentiation. Equipment suppliers are expanding development capacity, showcasing new coating technologies, and improving application infrastructure to meet changing industrial requirements. The industry therefore reflects a steady transition from standard finishing hardware toward more connected and performance-oriented coating systems.

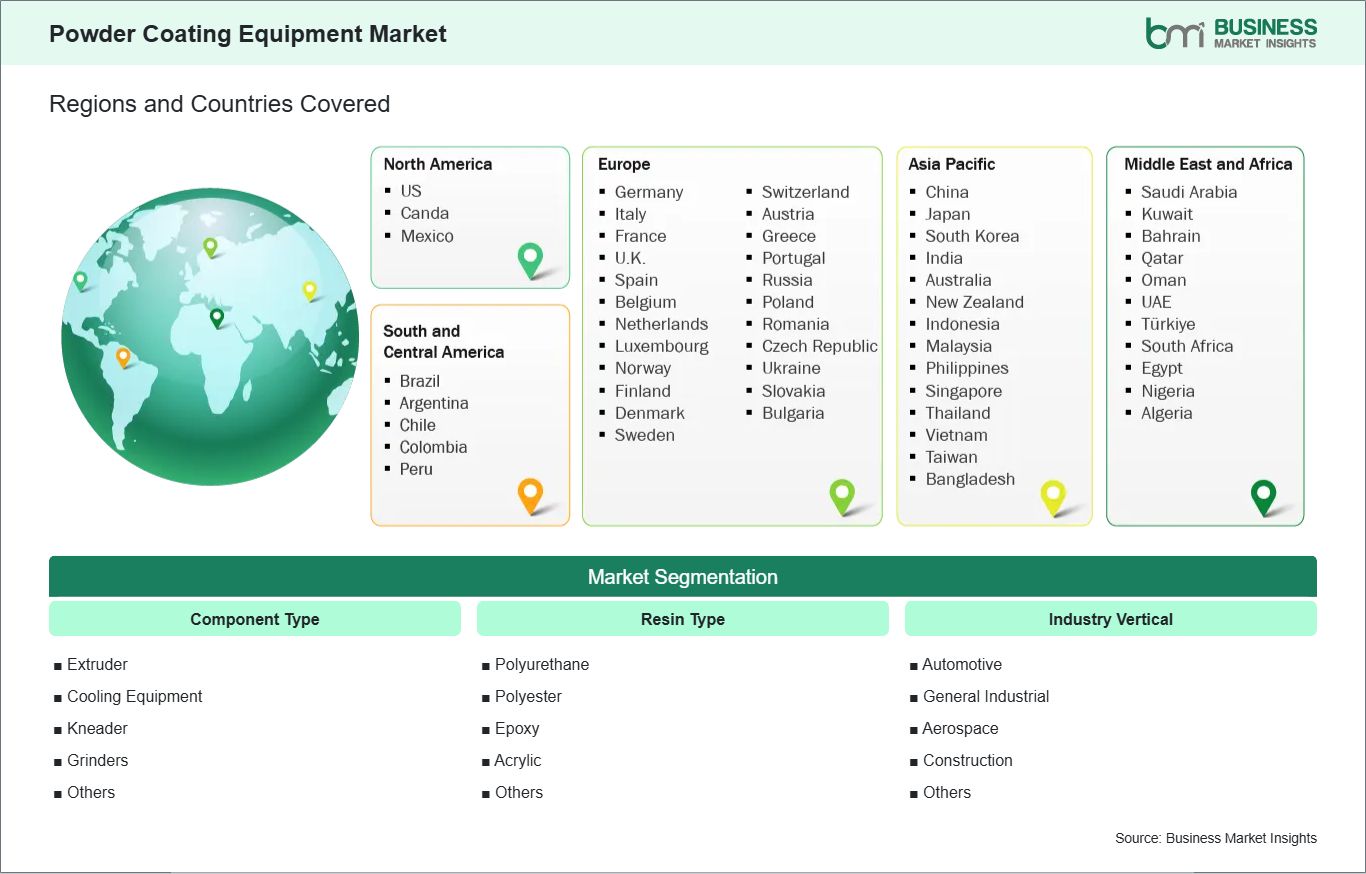

The Powder Coating Equipment Market is segmented based on component type, resin type, and industry vertical, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Component Type

Extruder: Forms uniform powder material during core production processing.

Cooling Equipment: Stabilizes processed material before downstream size reduction.

Kneader: Blends resin and additives for consistent formulation quality.

Grinders: Reduces processed material into application-ready powder particles.

Others: Covers auxiliary systems supporting powder production continuity.

By Resin Type

Polyurethane: Serves specialty coatings requiring performance and finish flexibility.

Polyester: Supports broad industrial use with outdoor durability advantages.

Epoxy: Fits protective applications needing adhesion and chemical resistance.

Acrylic: Addresses finishes requiring clarity and surface appearance precision.

Others: Includes additional resin chemistries for targeted coating demands.

By Industry Vertical

Automotive: Requires repeatable coating quality for high-throughput manufactured components.

General Industrial: Uses powder systems across diverse fabricated metal applications.

Aerospace: Prioritizes precision finishing and controlled coating performance.

Construction: Applies coatings for durability in architectural and infrastructure components.

Others: Includes additional industries with specialized surface finishing needs.

Powder Coating Equipment Market Drivers and Opportunities:

Industrial Shift Toward Efficient and Lower-Emission Finishing Systems

Manufacturers are reevaluating surface finishing operations as they seek better material utilization, cleaner processes, and tighter production control. Conventional liquid coating methods can involve solvent handling complexity, overspray inefficiency, and greater environmental management burdens in large-scale industrial settings. Powder coating equipment addresses these concerns by enabling dry finishing workflows that support durable coverage and more controlled material use. This has increased the appeal of integrated powder coating lines in sectors where finishing quality and process efficiency directly affect output economics.

The broader impact of this shift is visible in capital investment decisions across automotive, industrial fabrication, and engineered product manufacturing. Equipment buyers increasingly favor systems that can align with automated production cells, reduce process waste, and improve coating repeatability across complex parts. In this context, powder coating equipment has become more relevant not only as finishing infrastructure, but also as a lever for operational standardization and environmental performance. This strengthens the market’s role within modern manufacturing upgrades.

Automation-Ready Coating Lines and Advanced Process Integration

A significant opportunity lies in equipment platforms designed for automated, precision-led coating operations. As manufacturers manage more complex geometries, mixed production batches, and quality-sensitive finishes, coating systems must deliver tighter control over powder flow, application consistency, and process repeatability. This creates strong relevance for automated booths, smarter application systems, and integrated upstream production equipment that can work within coordinated manufacturing environments. Facilities seeking higher throughput and lower rework rates are especially aligned with this direction.

Future scope expands further where suppliers combine application technology with advanced testing, customer support, and system-level engineering. New development infrastructure and more capable laboratories indicate that equipment competition is moving toward solution depth rather than standalone hardware supply. This creates room for broader deployment across automotive, aerospace, and industrial finishing users that require tailored coating performance and scalable process control. As coating lines become more digital and quality-sensitive, integrated equipment ecosystems gain stronger strategic value.

Powder Coating Equipment Market Size and Share Analysis:

The Powder Coating Equipment Market is projected to grow from US$ 2.45 billion in 2025 to US$ 4.89 billion by 2033. The market is estimated to record a CAGR of 9.02% from 2026 to 2033.

This growth path indicates a market supported by manufacturing line modernization, environmental process preferences, and continued investment in durable industrial finishing. It also reflects the importance of coating efficiency within broader production economics.

By component type and resin use, extruders, grinders, and related upstream production systems hold strong relevance because they shape powder consistency and process reliability. Polyester and epoxy applications remain commercially important due to their wide industrial suitability and established presence in surface finishing workflows. Other resin categories contribute targeted demand where specialized performance characteristics matter.

By industry vertical, automotive and general industrial applications occupy a leading position because they require large-scale, repeatable, and quality-sensitive finishing operations. Construction also contributes meaningful demand where coated components must balance durability with appearance. Aerospace remains a more specialized but technically significant segment due to stricter finishing expectations and process control requirements.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Wagner America Corp.

Gema Switzerland GmbH

Magna Corporation

Nordson Corporation

Implant Inc.

Dongguo Powder Coating Co. Ltd.

Jintao Powder Equipment Co. Ltd.

Huabao Powder Coating Systems

Taiko Powder Coating Equipment

Meike Powder Coating Co. Ltd.

Get more information on this report

Powder Coating Equipment Market Report Coverage and Deliverables:

The "Powder Coating Equipment Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Powder Coating Equipment market shows diverse regional adoption patterns influenced by manufacturing intensity, environmental regulation, automation readiness, and finishing quality requirements. Across the global industry, equipment demand aligns with the need for efficient coating workflows that support durable finishes and better material utilization. Regional differences are shaped by industrial mix, export manufacturing activity, and the pace of plant modernization.

North America reflects a market where manufacturers place strong emphasis on automated finishing lines, process efficiency, and coating consistency across industrial applications. Demand is supported by automotive, engineered products, and industrial fabrication environments that require repeatable surface treatment at commercial scale. Equipment interest in the region increasingly centers on systems that can reduce waste and integrate with advanced production setups.

Asia Pacific presents a broader expansion environment because it combines large manufacturing capacity with ongoing investment in industrial finishing infrastructure. Coating line modernization in the region is influenced by rising output requirements, export-oriented production, and stronger attention to operational precision. This supports demand for both upstream powder production components and downstream application systems across diversified end-use sectors.

Europe shows a more compliance- and engineering-focused pattern, supported by environmental priorities, advanced manufacturing standards, and steady demand for high-performance finishes. Equipment selection in the region often emphasizes process control, quality assurance, and integration into efficient factory operations. Beyond these major regions, emerging markets offer additional opportunity where industrialization and fabrication activity create new need for scalable coating infrastructure.

Get more information on this report

Powder Coating Equipment Market Research Report Guidance:

The Powder Coating Equipment market report includes qualitative and quantitative data in the Powder Coating Equipment Market across component type, resin type, industry vertical, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Powder Coating Equipment Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Powder Coating Equipment Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Powder Coating Equipment Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Powder Coating Equipment Market segments by component type, resin type, industry vertical, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Powder Coating Equipment Market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Powder Coating Equipment Market News and Key Development:

The Powder Coating Equipment Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In June 2026, Nordson Corporation expanded its latest automated powder coating systems, focusing on high-transfer efficiency spray guns and integrated control units. The upgrade targets automotive and appliance manufacturers aiming to reduce overspray and improve coating consistency in high-volume production lines.

In November 2025, Graco Inc. (NYSE:GGG) announced today that it has acquired Red Devil Equipment Company, known in the market as Radia, in a transaction valued at $69 million. With annual revenue of more than $30 million, Radia is a manufacturer of mixing, shaking, and automated material handling equipment for the growing paint and coatings industry.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Powder Coating Equipment Market

Wagner America Corp.

Gema Switzerland GmbH

Magna Corporation

Nordson Corporation

Implant Inc.

Dongguo Powder Coating Co. Ltd.

Jintao Powder Equipment Co. Ltd.

Huabao Powder Coating Systems

Taiko Powder Coating Equipment

Meike Powder Coating Co. Ltd.

Frequently Asked Questions

How big is the Powder Coating Equipment Market?

The Powder Coating Equipment Market is valued at US$ 2.45 Billion in 2025, it is projected to reach US$ 4.89 Billion by 2033.

What is the CAGR for Powder Coating Equipment Market by (2026 - 2033)?

As per our report Powder Coating Equipment Market, the market size is valued at US$ 2.45 Billion in 2025, projecting it to reach US$ 4.89 Billion by 2033. This translates to a CAGR of approximately 9.02% during the forecast period.

What segments are covered in this report?

The Powder Coating Equipment Market report typically cover these key segments-

Component Type (Extruder, Cooling Equipment, Kneader, Grinders, Others)

Resin Type (Polyurethane, Polyester, Epoxy, Acrylic, Others)

Industry Vertical (Automotive, General Industrial, Aerospace, Construction, Others)

What is the historic period, base year, and forecast period taken for Powder Coating Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Powder Coating Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Powder Coating Equipment Market?

The Powder Coating Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Wagner America Corp.

Gema Switzerland GmbH

Magna Corporation

Nordson Corporation

Implant Inc.

Dongguo Powder Coating Co. Ltd.

Jintao Powder Equipment Co. Ltd.

Huabao Powder Coating Systems

Taiko Powder Coating Equipment

Meike Powder Coating Co. Ltd.

Who should buy this report?

The Powder Coating Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Powder Coating Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Powder Coating Equipment Market

Get Free Sample For Powder Coating Equipment Market