01

Market Summery

Executive Summary and Global Market Analysis

Industrial systems for poultry conversion have become more central to food manufacturing strategy as processors seek tighter control over yield, hygiene, and labor-intensive production stages. These equipment lines handle each major step of transformation, from primary processing through secondary preparation and value-added finishing. Their role extends beyond mechanical throughput because equipment decisions increasingly affect product consistency, worker allocation, and compliance readiness. This makes the sector closely tied to both operational efficiency and downstream product portfolio expansion.

Market momentum is linked to the rising industrialization of poultry processing and the need for more uniform, scalable plant operations. Processors are upgrading from labor-heavy methods toward integrated equipment lines that can improve cut precision, reduce variability, and support safer food handling practices. This shift is especially relevant where producers need to manage higher product volumes while maintaining traceability and meeting retailer or export requirements. As a result, the industry is moving toward more automated, data-aware processing environments.

Segment patterns reflect both species focus and production-stage complexity. Chicken remains the core poultry type because it dominates mainstream processing flows and supports a wide range of fresh and further-processed products. Within equipment categories, evisceration, cut-up, and deboning systems attract strong attention because they directly influence usable yield, line speed, and product standardization. Product diversification also shapes investment, as processors increasingly require equipment that can support fresh processed, pre-cooked, cured, and specialized value-added outputs.

Technology development is moving beyond basic mechanization toward robotics, digital inspection, intelligent cutting, and more adaptive line control. Automation is increasingly being applied to tasks once dependent on operator judgment, including vent cutting, deboning, and defect detection. Equipment makers are also incorporating X-ray inspection, robotics, and intelligent software to raise precision and lower process variability. These advances are strengthening the connection between processing equipment and plant-wide performance management.

Competitive conditions are shaped by automation depth, line integration capability, and the ability to serve both primary and secondary processing requirements. Suppliers are differentiating through modular system design, digital tools, and broader offerings for deboning, inspection, and prepared product workflows. The market therefore reflects a transition toward more integrated processing platforms rather than isolated machinery purchases.

03

Segment Analysis

Poultry Processing Equipment Market Segmentation

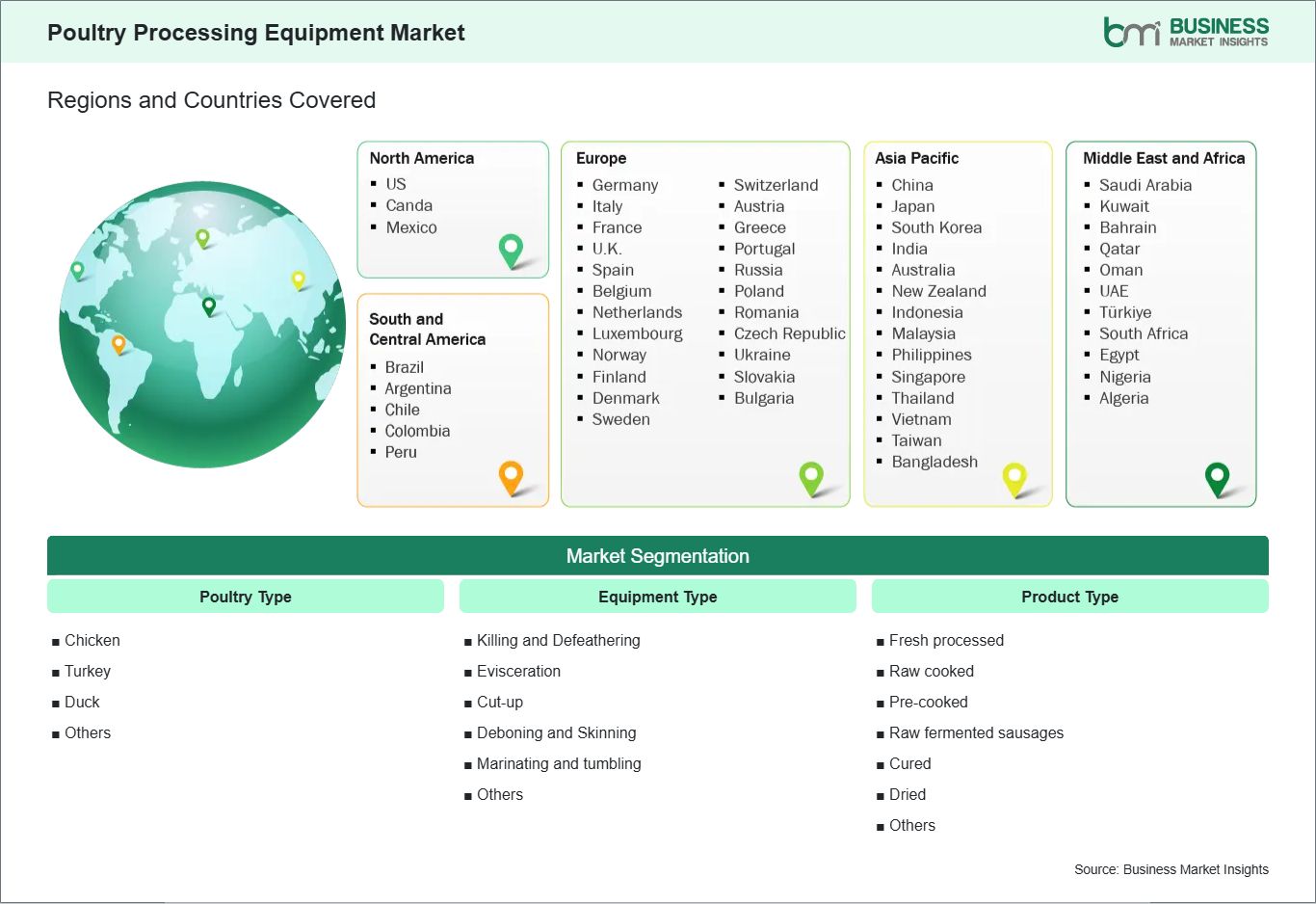

The Poultry Processing Equipment Market is segmented based on poultry type, equipment type, and product type highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Poulty Type

- Chicken: Dominates industrial processing due to broad consumption and standardized line requirements.

- Turkey: Supports larger-bird operations with specialized cutting and handling needs.

- Duck: Requires tailored processing for distinct carcass structure and product preparation.

- Others: Covers niche poultry categories with lower-volume equipment demand.

By Equipment Type

- Killing and Defeathering: Initiates line efficiency through controlled primary processing operations.

- Evisceration: Determines hygiene consistency and downstream carcass handling quality.

- Cut-up: Enables portioning precision for retail and foodservice product formats.

- Deboning and Skinning: Improves yield recovery and labor productivity in value-added lines.

- Marinating and tumbling: Enhances flavor absorption and prepared product uniformity.

- Others: Includes auxiliary systems supporting plant continuity and product handling.

By Product Type

- Fresh processed: Serves mainstream retail and foodservice supply channels.

- Raw cooked: Aligns with convenience-oriented intermediate product demand.

- Pre-cooked: Supports ready-to-heat applications with higher processing complexity.

- Raw fermented sausages: Addresses specialized processed meat production lines.

- Cured: Requires controlled processing for texture and shelf-life management.

- Dried: Fits preserved poultry products with targeted production requirements.

- Others: Includes additional processed formats shaped by regional consumption patterns.

04

Market Forces

Poultry Processing Equipment Market Drivers and Opportunities

Shift Toward Automated and Hygienic Poultry Processing Lines

Poultry processors are facing sustained pressure to improve line efficiency while maintaining food safety and product consistency. Manual operations can limit throughput, increase variability, and complicate hygiene management in high-volume plants. This has intensified the need for equipment that standardizes critical stages such as evisceration, cut-up, deboning, and inspection. Processors are therefore expanding investment in machinery that reduces dependency on manual precision while supporting more predictable plant performance.

The operational effect of this shift extends across labor planning, yield control, and plant compliance. Automated systems allow processors to manage repetitive and technically demanding tasks with greater consistency, which is particularly important in facilities serving retail, export, and prepared foods channels. Equipment modernization also supports traceability and inspection standards, making it relevant in markets where food quality assurance shapes commercial access. This context strengthens the market position of integrated poultry processing solutions across both mature and expanding production bases.

Value-Added Poultry Products and Intelligent Secondary Processing

A major opportunity is emerging from the expansion of value-added poultry formats that require more advanced secondary processing capability. As processors broaden offerings across pre-cooked, marinated, portioned, and specialty products, equipment requirements shift toward flexible lines with higher precision and tighter process control. Intelligent deboning, accurate cut-up systems, and automated inspection tools become more important in this environment because they help plants protect yield while supporting product differentiation. This increases the strategic weight of technologically advanced equipment beyond primary slaughter functions.

Future scope is strongest where processors combine value-added product expansion with digital process improvement. Equipment that integrates robotics, X-ray inspection, adaptive cutting, and line-level automation can help plants improve profitability while meeting evolving product specifications. This opens room for suppliers that offer broader system integration and application-specific configurations for secondary processing. As product mix becomes more complex, intelligent equipment platforms can capture a larger role in long-term plant investment planning.

05

Size and Share Analysis

Poultry Processing Equipment Market Size and Share Analysis

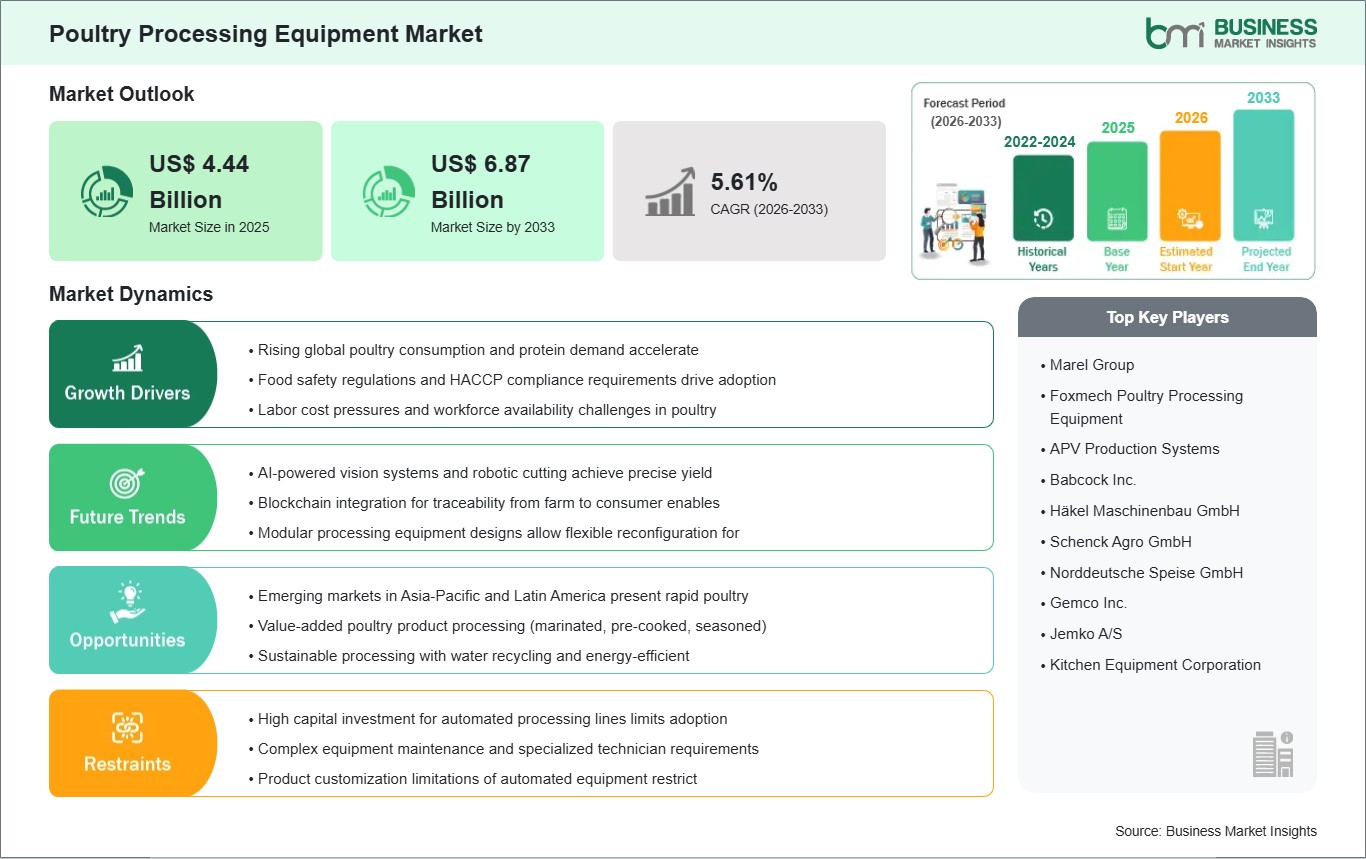

The Poultry Processing Equipment Market is projected to grow from US$ 4.44 billion in 2025 to US$ 6.87 billion by 2033. The market is estimated to record a CAGR of 5.61% from 2026 to 2033.

This growth profile indicates a market advancing through equipment modernization, broader processed poultry output, and tighter plant efficiency requirements. The sector is benefiting from the linkage between automation investment and commercial-scale poultry production.

By poultry type and equipment category, chicken-oriented systems hold the strongest position because they align with the largest processing flows and the broadest product mix. Evisceration, cut-up, and deboning equipment also occupy central importance because these stages shape usable yield, hygiene control, and downstream value addition. Primary processing remains essential, yet secondary processing systems are becoming more commercially influential.

By product type, fresh processed products retain foundational importance across the industry due to their wide distribution and high throughput requirements. Pre-cooked and other value-added categories are also becoming more relevant as processors seek differentiated offerings and stronger margin structures. This supports equipment demand across both conventional line stages and more advanced finishing operations.

07

Report Coverage

Poultry Processing Equipment Market Report Coverage and Deliverables

The "Poultry Processing Equipment Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Poultry Processing Equipment Market Geographic Insights

The Poultry Processing Equipment market shows diverse regional adoption patterns influenced by poultry consumption structures, plant modernization levels, labor economics, and food safety requirements. Across the global industry, equipment investment is strongest where processors need scalable production, tighter hygiene control, and broader value-added product capability. Regional variation therefore reflects both processing intensity and the pace of automation within commercial poultry plants.

North America remains a key market because processors in the region are pursuing intelligent automation, product traceability, and more efficient labor utilization across poultry plants. Investment is reinforced by the scale of commercial poultry operations and the need to maintain consistent output for retail and foodservice channels. Equipment interest is particularly strong in deboning, inspection, and other secondary processing stages that affect yield and product uniformity.

Asia Pacific presents a different expansion profile, shaped by rising poultry processing industrialization, broader protein demand, and plant upgrades aimed at efficiency and standardization. Processors in the region are increasingly evaluating automation and digital tools that can improve throughput while reducing manual dependency in demanding production environments. This creates room for both primary processing systems and more advanced secondary processing lines tailored to evolving product portfolios.

Europe advances through engineering-led modernization, compliance-focused production, and stronger emphasis on integrated processing technology. Processors in the region often prioritize precision equipment, inspection capability, and flexible systems that support higher-value poultry products. Beyond these established regions, emerging markets across the Middle East, Africa, and Latin America offer selective opportunities as poultry consumption, local processing capacity, and food manufacturing investment continue to broaden.

10

Industry Activity

Recent Developments

The Poultry Processing Equipment Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- In June 2026, Merck announced the acquisition of poultry technology company Targan, which develops automated systems for chick sex identification and in-ovo / early-life poultry processing solutions. The deal strengthens Merck’s position in animal health automation and advanced poultry production technologies.

- In July 2025, Wayne-Sanderson Farms has announced the acquisition of Georgia-based Harrison Poultry, a major producer of high-quality chicken known for its proprietary “Golden Goodness” range of traditional, international, and halal poultry products. The sale is effective immediately and includes transfer of all Harrison Poultry assets to Wayne-Sanderson Farms, including live production, hatchery, feed mill, manufacturing, production and transportation facilities and equipment in association with Harrison’s Bethlehem and Crawfordville area operations. Integrated operations will begin immediately, and the company expects minimal changes as day-to-day operations continue as normal.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations