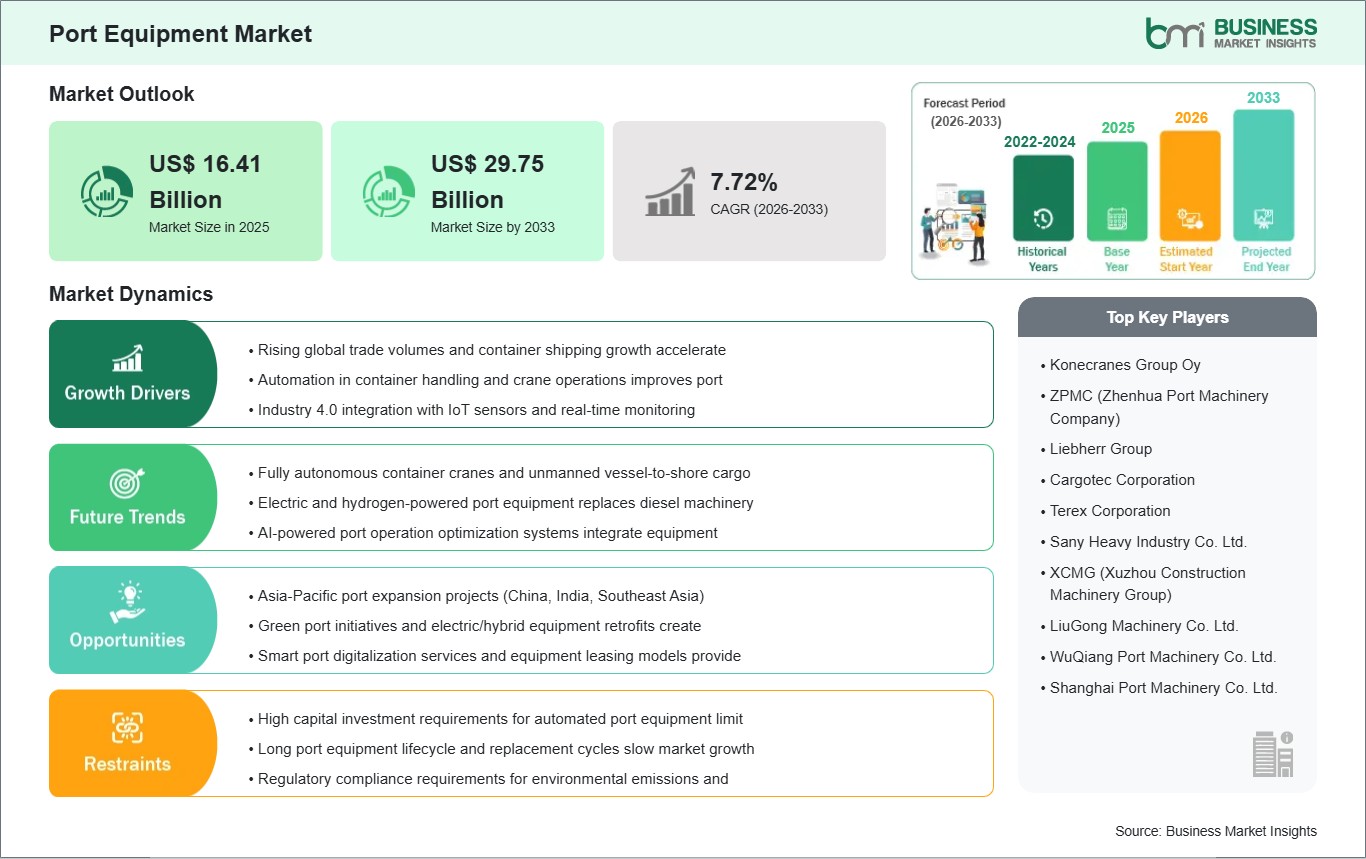

The port equipment market size is expected to reach US$ 29.75 billion by 2033 from US$ 16.41 billion in 2025. The market is estimated to record a CAGR of 7.72% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Cargo-handling machinery used in ports has moved from being purely mechanical infrastructure to becoming an important part of terminal productivity strategy. Equipment such as heavy forklifts, reach stackers, and container handlers directly influences container flow, yard density, and turnaround time across marine logistics networks. Their selection now reflects not only lifting performance, but also energy profile, digital compatibility, and suitability for different operating environments. This broadening role is reshaping how terminal operators approach fleet renewal and capital planning.

Market expansion is closely linked to the modernization of port infrastructure and the rising need for more efficient cargo movement. As trade volumes, vessel size, and service expectations place greater pressure on terminals, operators are investing in equipment that can improve throughput while reducing operational friction. Electrification and automation are becoming more prominent in procurement discussions because ports must balance productivity goals with emissions reduction and workforce efficiency. This creates a market environment centered on smarter and cleaner handling assets.

Segment behavior is evolving across both operating model and powertrain choice. Conventional machines still hold a large role due to their installed base and proven versatility, yet autonomous equipment is gaining attention where ports are building digitally managed yards. Diesel remains widely used in heavy-duty applications, but electric and hybrid systems are becoming more relevant as terminals plan lower-emission fleets. By equipment type, reach stackers and container handlers remain especially important because they combine flexibility, high stacking utility, and strong fit for intermodal and terminal operations.

Technology development is now centered on energy transition and operational intelligence. Equipment suppliers are introducing electric handling platforms, hybrid solutions, and smarter control architectures that align with terminal automation goals. These innovations reduce noise and emissions while improving predictability in high-cycle operating environments. The resulting technology path supports gradual movement from fuel-intensive fleets toward connected and more sustainable equipment ecosystems.

Competitive conditions are increasingly shaped by fleet electrification readiness, lifecycle support, and the ability to serve both conventional and advanced terminal models. Suppliers are differentiating through electric equipment launches, service agreements, and product portfolios aligned with automated port operations. The market therefore reflects a transition from hardware-focused competition toward platform-based competition centered on efficiency, uptime, and energy strategy.

Port Equipment Market - Strategic Insights:

Get more information on this report

Port Equipment Market Segmentation Analysis:

The port equipment market is segmented based on operation, power, equipment type, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Operation

Conventional: Maintains relevance in terminals prioritizing proven workflows and flexible deployment.

Autonomous: Gains traction where ports pursue digitally coordinated yard operations.

By Power

Diesel: Remains common in heavy-duty applications requiring high operating endurance.

Electric: Advances in terminals targeting lower emissions and quieter operations.

Hybrid: Bridges performance needs with incremental fleet decarbonization goals.

By Equipment Type

Heavy Forklifts: Handles non-containerized heavy loads and versatile yard duties.

Reach Stackers: Offers flexible container movement across port and intermodal environments.

Container Handlers: Supports high-frequency stacking and terminal space optimization.

Port Equipment Market Drivers and Opportunities:

Terminal Modernization and Cargo Handling Efficiency Requirements

Ports are upgrading operating models as larger vessels, tighter schedules, and more complex cargo flows raise pressure on yard performance. Traditional handling fleets often struggle to match current expectations for speed, consistency, and lower operating disruption across terminal networks. This has increased the need for equipment that improves container movement, yard positioning, and equipment utilization under demanding throughput conditions. As a result, operators are reassessing fleet composition through the lens of productivity, service reliability, and terminal space efficiency rather than simple replacement timing.

The impact of this shift extends into procurement priorities and long-term infrastructure planning. Terminal operators increasingly favor equipment that can integrate into digital control environments and support more predictable cargo handling cycles. Reach stackers, container handlers, and advanced yard machines are therefore gaining importance in ports seeking better operational discipline without large-scale layout redesign. This context strengthens the relevance of modern port equipment across both established ports and newer logistics gateways.

Electrification and Autonomous Equipment Deployment

A major opportunity is emerging through the overlap between port decarbonization goals and advances in intelligent handling equipment. Terminal operators are exploring electric and hybrid machines to reduce fuel dependency, local emissions, and maintenance intensity while preserving lifting performance. At the same time, autonomous and semi-autonomous operating models are becoming more credible as ports digitize yard planning and machine coordination. These developments create new pathways for fleet transformation, especially in terminals seeking both environmental improvement and greater operating consistency.

Future scope is strongest where suppliers can combine electrified platforms with service support and automation compatibility. Electric reach stackers, electric container handlers, and hybrid yard equipment illustrate how the sector is moving from isolated pilot concepts toward practical deployment decisions. As ports align capital spending with sustainability mandates and workforce optimization strategies, advanced powertrains and autonomous functions can reshape competitive positioning across the market.

Port Equipment Market Size and Share Analysis:

The port equipment market is projected to grow from US$ 16.41 billion in 2025 to US$ 29.75 billion by 2033. The market is estimated to record a CAGR of 7.72% from 2026 to 2033.

This trajectory indicates a market supported by sustained investment in cargo-handling productivity, terminal modernization, and cleaner equipment platforms. Growth also reflects the increasing strategic importance of equipment fleets in port competitiveness and service quality.

By operation and power, conventional diesel fleets still account for a substantial installed base, especially in ports managing heavy-duty and mixed cargo environments. However, electric and hybrid solutions are steadily improving their market position as terminals prioritize emissions reduction and fleet renewal. Autonomous systems remain a developing but increasingly visible direction within digitally advancing port ecosystems.

By equipment type, reach stackers occupy a strong role because they combine maneuverability, stacking flexibility, and suitability for intermodal handling. Container handlers also hold significant relevance in high-throughput yards where container density and rapid repositioning matter. Heavy forklifts retain importance in broader cargo applications that extend beyond standardized container movement.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Konecranes Group Oy

ZPMC (Zhenhua Port Machinery Company)

Liebherr Group

Cargotec Corporation

Terex Corporation

Sany Heavy Industry Co. Ltd.

XCMG (Xuzhou Construction Machinery Group)

LiuGong Machinery Co. Ltd.

WuQiang Port Machinery Co. Ltd.

Shanghai Port Machinery Co. Ltd.

Get more information on this report

Port Equipment Market Report Coverage and Deliverables:

The "Port Equipment Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Port Equipment Market Geographic Insights:

The Port Equipment market shows diverse regional adoption patterns influenced by cargo throughput needs, terminal electrification agendas, automation readiness, and port infrastructure investment. Across the global landscape, procurement priorities are changing as ports seek equipment that can support larger cargo flows while improving yard control and environmental performance. Regional demand, therefore, reflects differences in trade intensity, terminal maturity, and regulatory direction around emissions and digital operations.

North America reflects a modernization-oriented market where operators emphasize resilient terminal performance, equipment uptime, and cleaner handling technologies. Ports in the region are increasingly evaluating electric equipment and smarter fleet management as part of broader logistics efficiency strategies. Demand is supported by the need to improve container yard productivity while aligning operations with sustainability and service expectations.

Asia Pacific remains central to market development because the region combines major port capacity, expanding trade activity, and continuing infrastructure investment. Terminal operators across the region are placing more attention on productivity-enhancing fleets that can support denser yard operations and long-term automation plans. This environment creates strong relevance for both advanced conventional equipment and emerging electric or autonomous handling solutions.

Europe presents a more transition-focused pattern shaped by decarbonization policies, mature logistics infrastructure, and interest in lower-emission yard equipment. Electrified port equipment is gaining stronger traction in the region as operators look for practical pathways to reduce local emissions without sacrificing handling capability. Beyond these established regions, emerging markets in the Middle East, Africa, and Latin America offer additional opportunities as trade gateways expand and terminal operators invest in fleet modernization.

Get more information on this report

Port Equipment Market Research Report Guidance:

The Port Equipment market report includes qualitative and quantitative data in the port equipment market across operation, power, equipment type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the port equipment market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the port equipment market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the port equipment market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover port equipment market segments by operation, power, equipment type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the port equipment market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Port Equipment Market News and Key Development:

The port equipment market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In May 2026, Hutchison Ports’ BEST terminal announced the acquisition of three next-generation ship-to-shore (STS) cranes from ZPMC, strengthening terminal handling capacity for ultra-large container vessels. The new cranes feature extended outreach and higher lifting capability to support growing vessel sizes and port throughput.

In July 2025, MITSUI E&S Co., Ltd. (Head Office: Chuo-ku, Tokyo: President and CEO: Takeyuki Takahashi; hereinafter "MITSUI E&S") has replaced the conventional diesel engine generator set installed on a near-zero-emission Rubber Tired Gantry Cranes (RTG*) which MITSUI E&S delivered to Utoc Corporation (Representative Director and President: Nobuo Shiotsu; hereinafter "Utoc") at the Yokohama Port Minami-Honmoku Pier Container Terminal with a hydrogen fuel cell power pack.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Port Equipment Market

Konecranes Group Oy

ZPMC (Zhenhua Port Machinery Company)

Liebherr Group

Cargotec Corporation

Terex Corporation

Sany Heavy Industry Co. Ltd.

XCMG (Xuzhou Construction Machinery Group)

LiuGong Machinery Co. Ltd.

WuQiang Port Machinery Co. Ltd.

Shanghai Port Machinery Co. Ltd.

Frequently Asked Questions

How big is the Port Equipment Market?

The Port Equipment Market is valued at US$ 16.41 Billion in 2025, it is projected to reach US$ 29.75 Billion by 2033.

What is the CAGR for Port Equipment Market by (2026 - 2033)?

As per our report Port Equipment Market, the market size is valued at US$ 16.41 Billion in 2025, projecting it to reach US$ 29.75 Billion by 2033. This translates to a CAGR of approximately 7.72% during the forecast period.

What segments are covered in this report?

The Port Equipment Market report typically cover these key segments-

Operation (Conventional, Autonomous)

Power (Diesel, Electric, Hybrid)

Equipment Type (Heavy Forklifts, Reach Stackers, Container Handlers)

What is the historic period, base year, and forecast period taken for Port Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Port Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Port Equipment Market?

The Port Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Konecranes Group Oy

ZPMC (Zhenhua Port Machinery Company)

Liebherr Group

Cargotec Corporation

Terex Corporation

Sany Heavy Industry Co. Ltd.

XCMG (Xuzhou Construction Machinery Group)

LiuGong Machinery Co. Ltd.

WuQiang Port Machinery Co. Ltd.

Shanghai Port Machinery Co. Ltd.

Who should buy this report?

The Port Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Port Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Port Equipment Market

Get Free Sample For Port Equipment Market