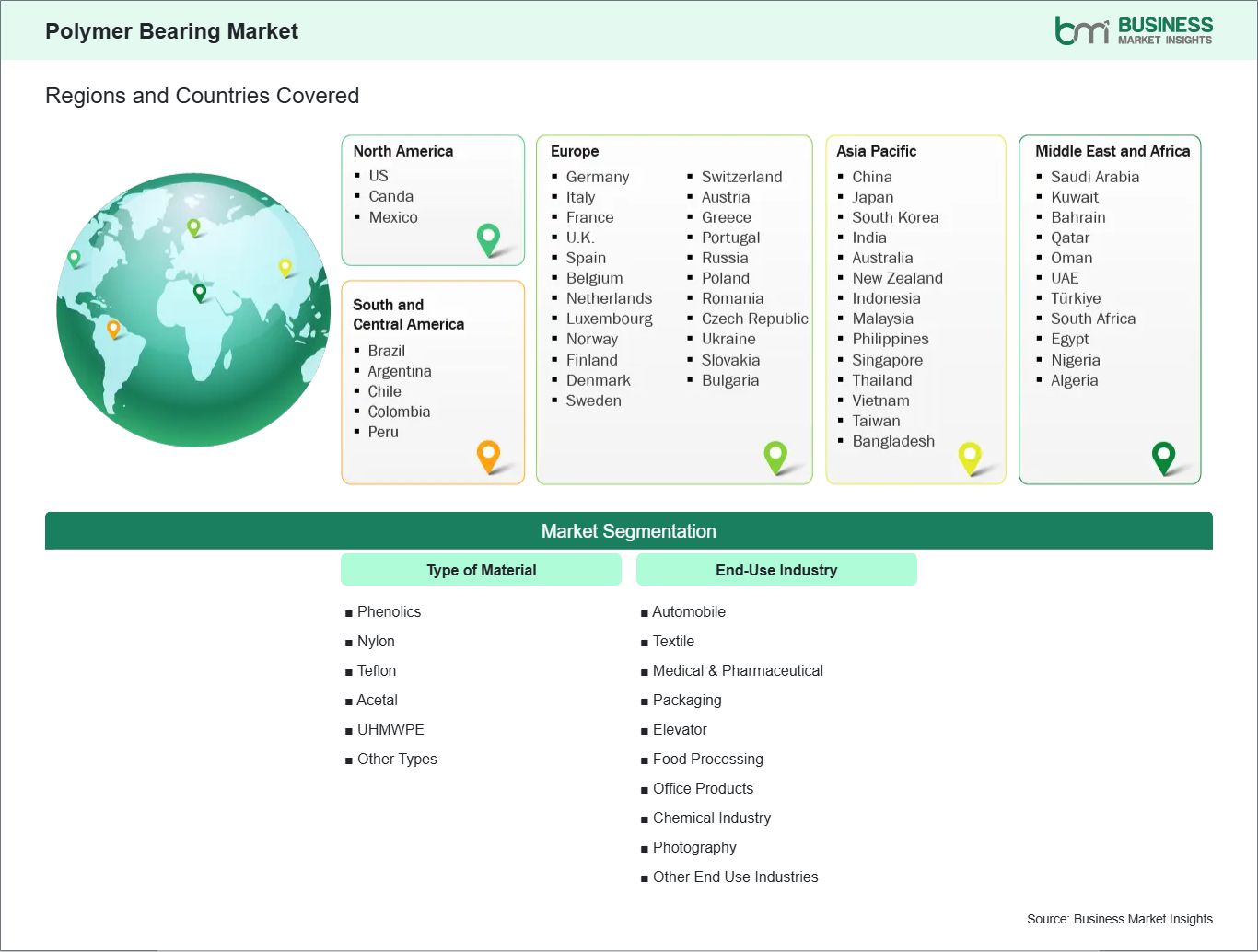

Type of Material (Phenolics, Nylon, Teflon, Acetal, UHMWPE, Other Types)

End-Use Industry (Automobile, Textile, Medical & Pharmaceutical, Packaging, Elevator, Food Processing, Office Products, Chemical Industry, Photography, Other End Use Industries)

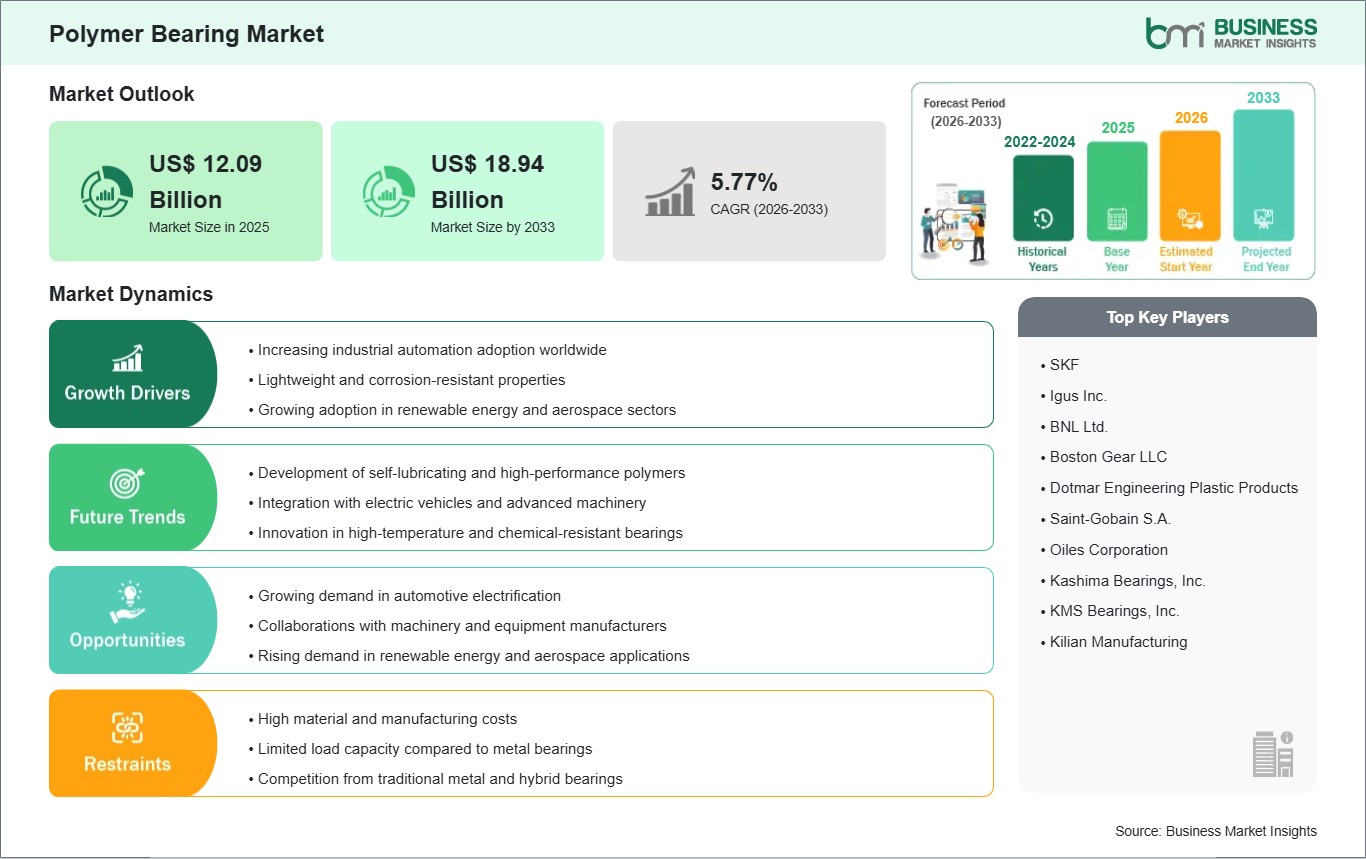

The Polymer Bearing Market size is expected to reach US$ 18.94 billion by 2033 from US$ 12.09 billion in 2025. The market is estimated to record a CAGR of 5.77% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global polymer bearing market is experiencing sustained growth, driven by increasing industrial automation, demand for lightweight machinery components, and the shift toward maintenance-free solutions. Polymer bearings, made from engineered plastics such as PTFE, PEEK, and polyamide composites, are valued for their low friction, corrosion resistance, and self-lubricating properties. These bearings are increasingly replacing traditional metal bearings in applications across automotive, aerospace, food processing, electronics, and industrial machinery sectors.

The growing emphasis on energy efficiency and cost reduction further enhances polymer bearings’ appeal, as they reduce frictional losses and operational maintenance requirements. Technological innovation is a key growth driver in the polymer bearing market. Manufacturers are developing high-performance composites, reinforced plastics, and hybrid bearings to improve load-bearing capacity, thermal resistance, and chemical tolerance.

Additive manufacturing is emerging as a viable production method, enabling complex geometries, rapid prototyping, and small-batch customization for specialized industrial applications. Research in high-temperature, wear-resistant, and electrically insulating polymers is expanding market adoption in aerospace, medical devices, and electronics. Competitive strategies in the polymer bearing market focus on product differentiation, vertical integration, and global expansion. Companies are leveraging proprietary material formulations, licensing technologies, and strategic partnerships with OEMs to gain competitive advantage. Sustainability is increasingly influencing design and manufacturing, with emphasis on recyclable materials, reduced lubricants, and energy-efficient production processes.

The market outlook remains positive, driven by technological advancements, industrial modernization, and growing demand for lightweight, low-maintenance, and high-performance bearing solutions.

Polymer Bearing Market - Strategic Insights:

Get more information on this report

Polymer Bearing Market Segmentation Analysis:

Key segments that contributed to the derivation of the polymer bearing market analysis are type of material and end‑use industry.

By Type of Material, the polymer bearing market is segmented into phenolics, nylon, Teflon, acetal, UHMWPE, and others. The phenolics segment dominated the market in 2025.

Based on End‑Use Industry, the polymer bearing market is classified into automobile, textile, medical & pharmaceutical, packaging, elevator, food processing, office products, chemical industry, photography, and others. The automobile segment dominated the market in 2025.

he polymer bearings market is witnessing rapid growth due to the increased use of automated technology in industries to increase efficiency, accuracy, and durability of machine parts. Polymer bearings have more advantages over metal bearings in terms of weight, corrosion resistance, lubrication, and maintenance. These advantages have made polymer bearings more suitable for use in automated assembly plants, robots, and high-speed conveyor systems. With the increase in the use of automated technology in manufacturing plants globally, the use of polymer bearings is witnessing rapid growth. Industries are looking for polymer bearings to address the issues of operating in adverse environments due to exposure to chemicals, moisture, and high temperatures. New-generation polymers such as polyamide, PTFE composites, and PEEK have been used to increase the wear resistance of bearings for use in automated plants. The lubrication-free operation of polymer bearings has made them more suitable for use in automated plants. In automated plants, bearings should not stop for lubrication, as this can cause huge losses in terms of production. Therefore, this has made the use of polymer bearings more suitable for use in automated plants.

The trend toward smart factories and Industry 4.0 is also accelerating polymer bearing usage. Sensors and predictive maintenance technologies often pair with polymer components to enhance machine monitoring and reduce failure risks. Companies across Europe, North America, and Asia are integrating polymer bearings into robotic arms, pick-and-place systems, and packaging equipment, as automation penetrates sectors ranging from consumer electronics to medical devices. With continuous technological improvements in polymer chemistry and bearing design, global industrial automation initiatives are expected to sustain long-term demand growth for polymer bearings in multiple manufacturing domains.

Growing demand in automotive electrification

The move towards electric vehicles is also opening new opportunities for the polymer bearing market. The preference for polymer bearings is high in electric vehicle drivelines, steering systems, braking systems, and auxiliary systems due to the light weight, corrosion resistance, and low friction properties of polymer bearings. The light weight is important for the moving parts in electric vehicles to enhance the efficiency of the batteries used in the electric vehicles. In addition, polymer bearings are capable of withstanding high temperatures with less lubrication, which is suitable for electric vehicles compared to traditional internal combustion engine-based vehicles.

Automakers in Europe, the US, Japan, and other countries are adopting polymer bearings in the electric vehicles they plan to introduce in the market in the near future. In electric vehicles, polymer bearings are used in the wheel hubs, electric motors, and gearboxes to reduce energy losses and extend the life of the electric motors. The growth in the electric vehicle market in countries such as China, the US, Germany, and Japan is directly influencing the growth in the polymer bearing market. The suppliers are also producing high-performance polymers suitable for the electric vehicle market.

In addition to EVs, the demand for polymer bearings is growing in autonomous and connected vehicles, where precision and low-maintenance components are critical. The integration of lightweight polymer bearings into braking systems, motor assemblies, and steering mechanisms helps optimize performance while minimizing noise and vibration. As governments worldwide provide incentives for EV adoption and manufacturers scale up production to meet climate goals, polymer bearings are becoming a standard component in modern automotive design. Overall, the rise of automotive electrification is expected to drive sustained global demand for polymer bearing solutions over the next decade.

Polymer Bearing Market Size and Share Analysis:

The polymer bearing market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type of material and end‑use industry, offering insights into their contribution to overall market performance.

By Type of Material, the phenolics subsegment dominated the market in 2025, driven by its excellent strength, shock resistance, and chemical resistance that make it suitable for multiple industrial applications.

Based on End‑Use Industry, the automobile subsegment dominated the market in 2025, owing to increasing use of polymer bearings in various automotive components.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

SKF

Igus Inc.

BNL Ltd.

Boston Gear LLC

Dotmar Engineering Plastic Products

SaintâGobain S.A.

Oiles Corporation

Kashima Bearings, Inc.

Get more information on this report

Polymer Bearing Market Report Coverage and Deliverables:

The "Polymer Bearing Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Polymer Bearing Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Polymer Bearing Market trends, as well as drivers, restraints, and opportunities

Polymer Bearing Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Polymer Bearing Market

Detailed company profiles, including SWOT analysis

Polymer Bearing Market Geographic Insights:

The geographical scope of the Polymer Bearing Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regionally, the polymer bearing market exhibits diverse growth trends influenced by industrial activity, technological development, and application-specific demand. North America dominates the market, led by the U.S., where adoption is fueled by aerospace, automotive, and industrial machinery sectors. The region emphasizes high-performance polymer bearings for precision machinery, lightweight automotive components, and maintenance-free industrial applications. R&D investment, advanced manufacturing infrastructure, and strong OEM collaborations reinforce North America’s market leadership.

In the Asia Pacific, rapid industrialization, expanding automotive production, and growing electronics and manufacturing sectors drive polymer bearing demand. China, Japan, India, and South Korea are key contributors, focusing on both domestic and export-oriented production. The region benefits from cost-competitive manufacturing, rising automation, and increasing adoption of self-lubricating polymer components across industrial machinery and automotive applications.

Europe emphasizes sustainability, high-performance engineering, and regulatory compliance. Germany, Italy, and France lead polymer bearing adoption in industrial automation, aerospace, and food processing machinery. Manufacturers focus on high-load, wear-resistant, and chemically resistant bearings, supported by partnerships with precision engineering firms and OEMs.

The Middle East & Africa market is emerging, driven primarily by oil & gas, industrial machinery, and infrastructure projects. Investment in modern manufacturing facilities and maintenance-free industrial components in countries such as the UAE, Saudi Arabia, and South Africa is gradually expanding adoption.

South & Central America is developing steadily, with Brazil and Argentina at the forefront. Growth is supported by automotive, industrial, and food processing applications. Strategic collaborations with North American and European producers, coupled with localized manufacturing, are gradually establishing a reliable supply chain for polymer bearings in the region.

Get more information on this report

Polymer Bearing Market Research Report Guidance:

The report includes qualitative and quantitative data in the Polymer Bearing Market across type of material, end‑use industry, end use and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Polymer Bearing Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Polymer Bearing Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Polymer Bearing Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Polymer Bearing Market segments across type of material, end‑use industry, end use and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Polymer Bearing Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Polymer Bearing Market News and Key Development:

The Polymer Bearing Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the polymer bearing market are:

In April 2025, igus GmbH announced that it developed and launched new PTFE‑free, wear‑resistant polymer plain bearings by reformulating popular iglide materials without PTFE, enabling environmentally friendlier and regulatory‑ready bearing solutions for machinery, automotive, and industrial applications worldwide.

In February 2023, igus GmbH introduced xiros MT180 biocompatible polymer deep groove ball bearings, designed for medical technology applications (such as bio‑reactors, MRI equipment, and prosthetics) and certified to stringent biocompatibility standards.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Polymer Bearing Market

SKF

,

Igus Inc.

,

BNL Ltd.

,

Boston Gear LLC

,

Dotmar Engineering Plastic Products

,

Saint‑Gobain S.A.

,

Oiles Corporation

,

Kashima Bearings, Inc.

,

KMS Bearings, Inc.

,

Kilian Manufacturing

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Polymer Bearing Market?

The Polymer Bearing Market is valued at US$ 12.09 Billion in 2025, it is projected to reach US$ 18.94 Billion by 2033.

What is the CAGR for Polymer Bearing Market by (2026 - 2033)?

As per our report Polymer Bearing Market, the market size is valued at US$ 12.09 Billion in 2025, projecting it to reach US$ 18.94 Billion by 2033. This translates to a CAGR of approximately 5.77% during the forecast period.

What segments are covered in this report?

The Polymer Bearing Market report typically cover these key segments-

Type of Material (Phenolics, Nylon, Teflon, Acetal, UHMWPE, Other Types)

End-Use Industry (Automobile, Textile, Medical & Pharmaceutical, Packaging, Elevator, Food Processing, Office Products, Chemical Industry, Photography, Other End Use Industries)

What is the historic period, base year, and forecast period taken for Polymer Bearing Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Polymer Bearing Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Polymer Bearing Market?

The Polymer Bearing Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

SKF

,

Igus Inc.

,

BNL Ltd.

,

Boston Gear LLC

,

Dotmar Engineering Plastic Products

,

SaintâÂÂGobain S.A.

,

Oiles Corporation

,

Kashima Bearings, Inc.

,

KMS Bearings, Inc.

,

Kilian Manufacturing

Who should buy this report?

The Polymer Bearing Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Polymer Bearing Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Polymer Bearing Market

Get Free Sample For Polymer Bearing Market