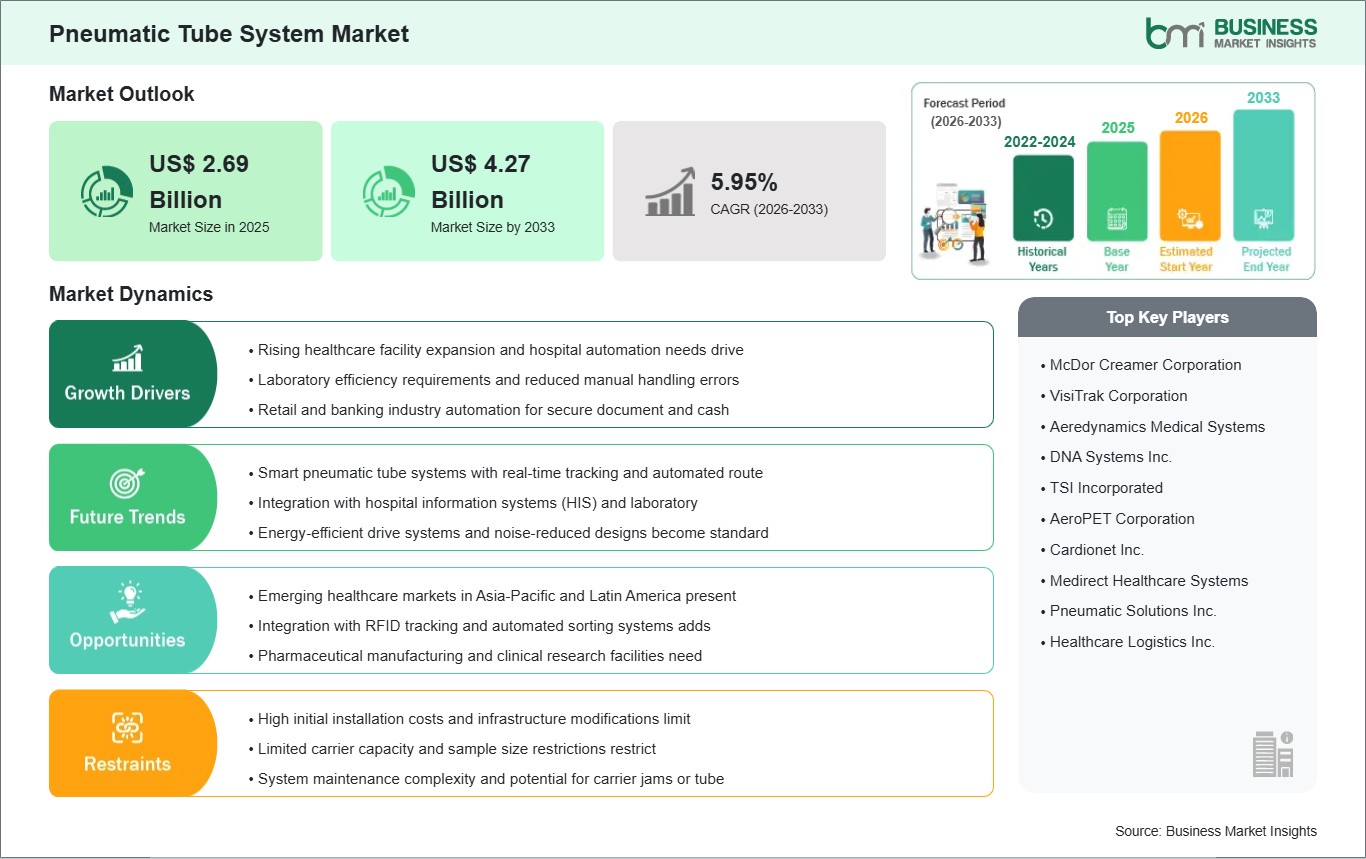

The pneumatic tube system market size is expected to reach US$ 4.27 billion by 2033 from US$ 2.69 billion in 2025. The market is estimated to record a CAGR of 5.95% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Automated carrier transport systems that move lightweight items through sealed tube networks have become increasingly relevant in facilities that depend on rapid internal distribution. These systems reduce walking time, shorten delivery cycles, and improve control over high-frequency movements inside hospitals, factories, offices, and retail premises. Their utility is strongest where items must travel securely between departments without adding congestion to staff workflows. As organizations digitize operations, pneumatic tube systems are being re-evaluated as practical infrastructure for internal logistics.

Market momentum is supported by the need to improve response speed, reduce manual transport steps, and strengthen operational traceability. Hospitals use these systems to move specimens, blood products, and medications between nursing stations, laboratories, and pharmacies, while commercial facilities apply them to cash and document handling. Industrial users also value them for the controlled transfer of small components and paperwork across production zones. This broad relevance supports steady deployment across settings where internal time savings translate directly into service efficiency.

Segment behavior differs according to installation scale and operational complexity. Single-phase systems remain appropriate for simpler routing environments, whereas three-phase systems align with higher-capacity and more demanding movement patterns. By configuration, multiline systems offer a stronger fit for larger facilities with multiple destinations, while point-to-point and single-line systems remain useful in more focused layouts. Fully automatic systems are gaining preference because they improve throughput consistency and reduce operator dependence in high-volume environments.

Technology development is moving toward smarter routing, real-time monitoring, and system integration with broader facility platforms. Modern systems incorporate sensors, software interfaces, and automation features that improve dispatch accuracy, visibility, and error reduction. Healthcare settings, in particular, are linking pneumatic tube workflows more closely with laboratory and hospital information systems. At the same time, product development is paying closer attention to operational reliability, noise control, and the safe transport of sensitive contents.

Competitive conditions are shaped by installation expertise, service capability, and the ability to tailor networks for different building types. Suppliers increasingly differentiate through automation depth, maintenance support, software integration, and design flexibility across healthcare and commercial environments. The market, therefore, reflects a gradual shift from basic transport functionality toward a more intelligent and facility-specific logistics platform.

Pneumatic Tube System Market - Strategic Insights:

Get more information on this report

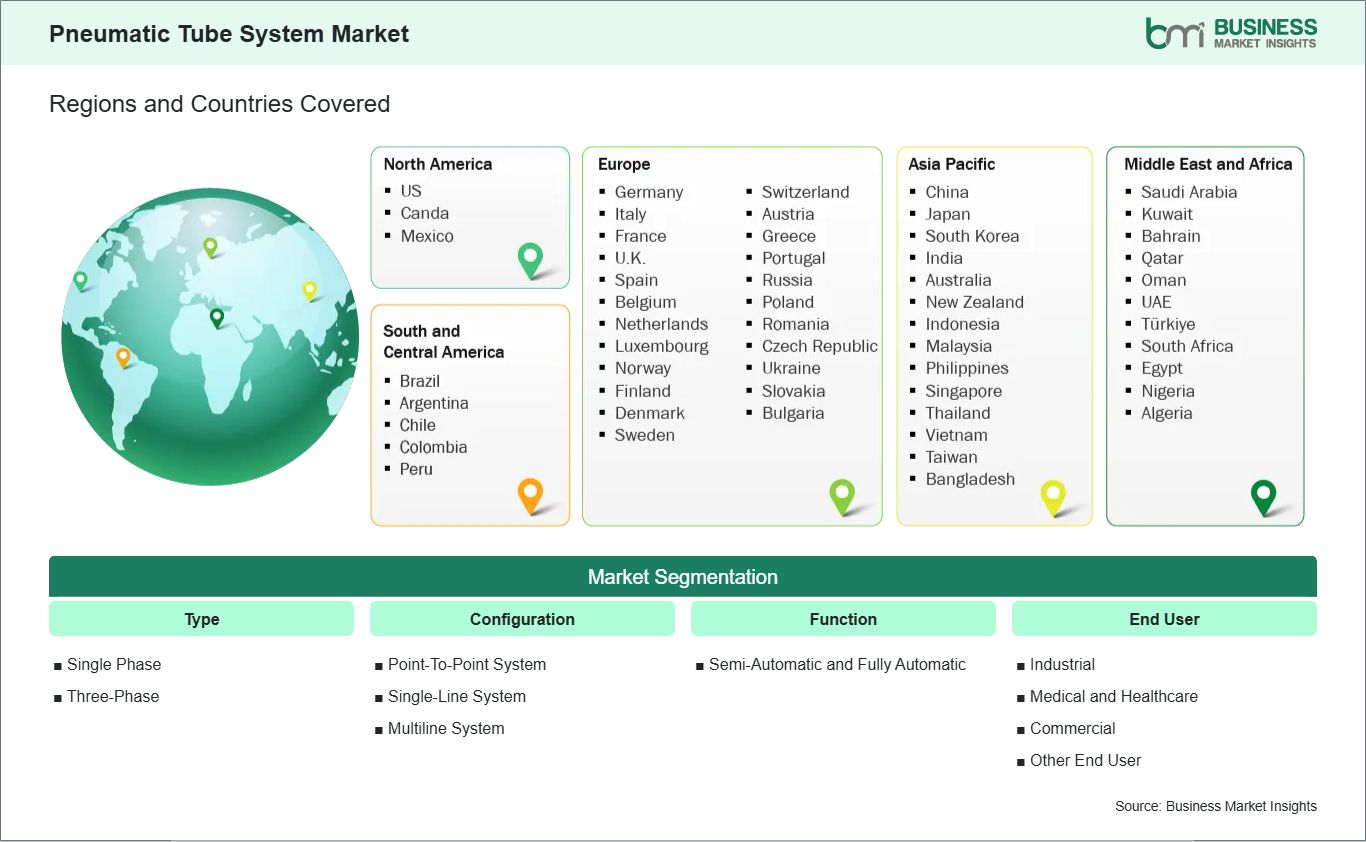

Pneumatic Tube System Market Segmentation Analysis:

The pneumatic tube system market is segmented based on type, configuration, function, and end user, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Type

Single Phase – Fits facilities with straightforward transport demands and simpler electrical integration.

Three-Phase – Supports larger systems requiring stronger operational continuity and network performance.

By Configuration

Point-To-Point System – Serves direct transfers between fixed locations with minimal routing complexity.

Single-Line System – Handles sequential carrier movement in compact facility layouts.

Multiline System – Accommodates larger buildings with multiple departments and routing priorities.

By Function

Semi-Automatic – Suits facilities balancing manual control with moderate transport efficiency.

Fully Automatic – Enhances throughput, routing accuracy, and workflow consistency.

By End User

Industrial – Moves documents, components, and small items across controlled work areas.

Medical and Healthcare – Prioritizes rapid transport of samples, medicines, and blood products.

Commercial – Supports secure internal transfer of cash, records, and small packages.

Other End User – Covers specialized environments with time-sensitive internal logistics needs.

Pneumatic Tube System Market Drivers and Opportunities:

Need for Faster and More Controlled Internal Logistics

Facilities are under greater pressure to reduce non-productive staff movement and improve the speed of internal item transfer. Manual transport methods consume labor time, introduce handoff delays, and complicate traceability in environments where timely delivery matters. Pneumatic tube systems address these issues by creating a dedicated internal transport network for high-frequency, lightweight loads. Their utility is particularly strong where service quality depends on dependable movement of samples, medicines, documents, or cash between operational nodes.

The effect of this need is especially visible in hospitals and commercial environments with repetitive internal delivery tasks. Healthcare operators seek faster turnaround between diagnostic, pharmacy, and clinical departments, while commercial users look for secure routing of cash and sensitive paperwork. Industrial sites also benefit where documents and components need controlled transit without interrupting production flows. This makes pneumatic tube systems increasingly relevant as infrastructure for labor efficiency and internal coordination rather than only as a convenience tool.

Smart Routing and Facility System Integration

A notable opportunity lies in the transition from standalone transport networks to integrated intelligent logistics systems. Newer pneumatic tube platforms incorporate software controls, sensors, and interfaces that allow routing decisions, performance monitoring, and dispatch workflows to operate more efficiently. In healthcare settings, this integration can align tube deliveries with hospital information systems, laboratory workflows, and contact-minimized operations. These capabilities elevate system value by improving accuracy, reducing bottlenecks, and strengthening visibility over carrier movement.

Future scope is likely to expand where facilities want automated infrastructure that connects physical movement with digital operations. Multiline and fully automatic networks are well positioned in this context because they support more destinations, higher carrier volumes, and reduced operator intervention. As building operators place greater emphasis on traceability, reliability, and integrated maintenance support, smarter pneumatic tube systems can move into a broader range of medical, industrial, and commercial use cases.

Pneumatic Tube System Market Size and Share Analysis:

The pneumatic tube system market is projected to grow from US$ 2.69 billion in 2025 to US$ 4.27 billion by 2033. The market is estimated to record a CAGR of 5.95% from 2026 to 2033.

This growth profile indicates a market supported by consistent infrastructure spending on internal logistics, especially in sectors where time-sensitive movement and workflow efficiency remain important. The industry is advancing through application-led adoption rather than broad-based commoditization.

By type and configuration, three-phase and multiline systems hold stronger strategic relevance for larger and more complex facilities. Their suitability for higher-capacity and multi-destination movement aligns well with institutions seeking broader network coverage. Point-to-point and single-line systems continue to serve focused installations where route simplicity and direct transfer remain sufficient.

By end user, medical and healthcare accounts for the most influential application base because hospitals require rapid and repeatable transfer of sensitive items. Commercial facilities also contribute meaningful demand through secure internal movement of cash and documents. Industrial use adds further scope where controlled small-load transport supports plant coordination and administrative efficiency.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

McDor Creamer Corporation

VisiTrak Corporation

Aeredynamics Medical Systems

DNA Systems Inc.

TSI Incorporated

AeroPET Corporation

Cardionet Inc.

Medirect Healthcare Systems

Pneumatic Solutions Inc.

Healthcare Logistics Inc.

Get more information on this report

Pneumatic Tube System Market Report Coverage and Deliverables:

The "Pneumatic Tube System Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Pneumatic Tube System Market Geographic Insights:

The Pneumatic Tube System market shows diverse regional adoption patterns influenced by healthcare infrastructure quality, facility automation priorities, commercial security needs, and internal logistics modernization. Across the global landscape, usage is concentrated in environments where rapid movement of small, time-sensitive loads improves service speed and workflow discipline. Adoption patterns therefore vary according to hospital investment, commercial building complexity, and the maturity of automated facility operations.

North America maintains a strong position because the region combines advanced hospital networks, established commercial applications, and a broad focus on workflow optimization. Healthcare facilities in particular value pneumatic tube systems for specimen transfer, medication dispatch, and internal logistics coordination across large campuses. Commercial and institutional sites also support demand where secure movement of cash and sensitive documents remains operationally important.

Asia Pacific shows expanding relevance as healthcare capacity, urban commercial infrastructure, and industrial modernization continue to develop across major economies. Facilities in the region are placing more emphasis on efficient intra-building transport that reduces manual workloads and supports service continuity. Public procurement and tender activity also indicate sustained interest in pneumatic tube systems for institutional installations, especially where hospital efficiency and operational safety are priorities.

Europe presents a comparatively system-oriented environment shaped by hospital modernization, building automation, and strong attention to operational reliability. The region favors installations that combine secure transport with lower disruption to clinical and administrative workflows. Beyond the major established markets, emerging regions offer selective opportunities where hospital expansion, commercial formalization, and infrastructure upgrades create new demand for internal transport systems.

Get more information on this report

Pneumatic Tube System Market Research Report Guidance:

The Pneumatic Tube System market report includes qualitative and quantitative data in the pneumatic tube system market across type, configuration, function, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the pneumatic tube system market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the pneumatic tube system market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the pneumatic tube system market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover pneumatic tube system market segments by type, configuration, function, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the pneumatic tube system market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Pneumatic Tube System Market News and Key Development:

The pneumatic tube system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In Feb 2026, -TransLogic, a Swisslog Healthcare company and a leading supplier in transport automation, has launched MYtranslogic, a breakthrough cloud-based repository, for North America healthcare facilities. The platform, developed in partnership with DevIQ, provides enhanced access to TransLogic tube system monitoring, helping prevent minor issues from escalating into system service interruptions that prove costly to patient care and staff efficiency.

September 2025, Aerocom Systems expanded deployment of high-capacity pneumatic tube systems across hospitals and industrial facilities in Europe and Asia.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Pneumatic Tube System Market

McDor Creamer Corporation

VisiTrak Corporation

Aeredynamics Medical Systems

DNA Systems Inc.

TSI Incorporated

AeroPET Corporation

Cardionet Inc.

Medirect Healthcare Systems

Pneumatic Solutions Inc.

Healthcare Logistics Inc.

Frequently Asked Questions

How big is the Pneumatic Tube System Market?

The Pneumatic Tube System Market is valued at US$ 2.69 Billion in 2025, it is projected to reach US$ 4.27 Billion by 2033.

What is the CAGR for Pneumatic Tube System Market by (2026 - 2033)?

As per our report Pneumatic Tube System Market, the market size is valued at US$ 2.69 Billion in 2025, projecting it to reach US$ 4.27 Billion by 2033. This translates to a CAGR of approximately 5.95% during the forecast period.

What segments are covered in this report?

The Pneumatic Tube System Market report typically cover these key segments-

End User (Industrial, Medical and Healthcare, Commercial, Other End User)

What is the historic period, base year, and forecast period taken for Pneumatic Tube System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Pneumatic Tube System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Pneumatic Tube System Market?

The Pneumatic Tube System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

McDor Creamer Corporation

VisiTrak Corporation

Aeredynamics Medical Systems

DNA Systems Inc.

TSI Incorporated

AeroPET Corporation

Cardionet Inc.

Medirect Healthcare Systems

Pneumatic Solutions Inc.

Healthcare Logistics Inc.

Who should buy this report?

The Pneumatic Tube System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Pneumatic Tube System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Pneumatic Tube System Market

Get Free Sample For Pneumatic Tube System Market