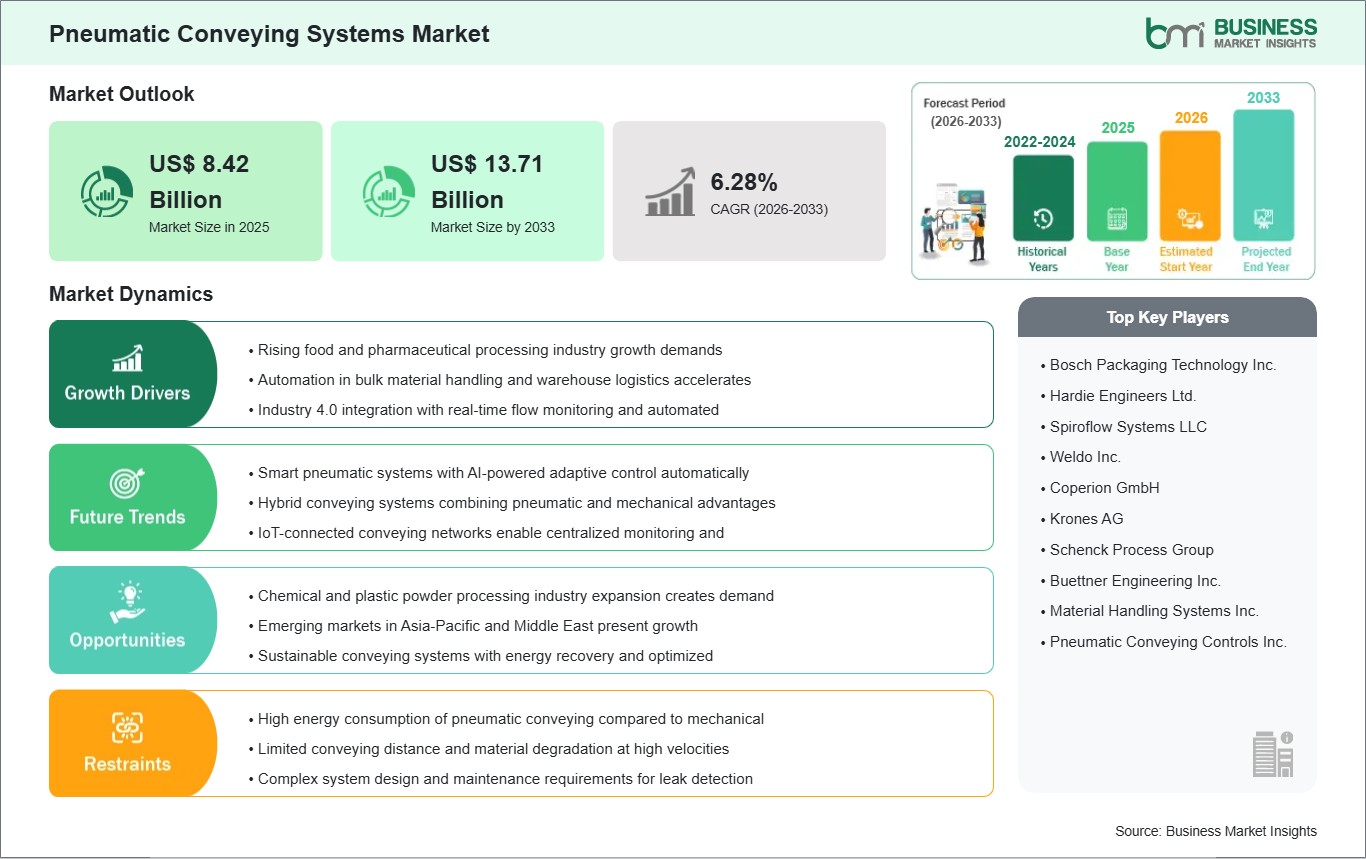

The pneumatic conveying systems market size is expected to reach US$ 13.71 billion by 2033 from US$ 8.42 billion in 2025. The market is estimated to record a CAGR of 6.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Enclosed material transport systems that use pressure differentials to move dry bulk solids have become increasingly important in modern process industries. Their appeal lies in contamination control, layout flexibility, and the ability to connect storage, dosing, mixing, and packaging operations within a continuous handling architecture. These systems are especially useful where dust containment, product integrity, and plant cleanliness influence equipment design. As industrial production becomes more automated, pneumatic conveying fits naturally into closed-loop processing lines.

Market expansion reflects a shift toward automated bulk handling that reduces manual contact and improves operational consistency. Processors are modernizing plants to support hygienic production, lower dust exposure, and more reliable transfer of powders and granules between critical stages. This need is pronounced in food, pharmaceutical, chemicals, and power-related applications where housekeeping, safety, and throughput directly affect plant economics. Buyers are therefore evaluating conveying systems not only as transport equipment, but also as process control infrastructure.

Segment demand varies according to material sensitivity, plant layout, and transfer distance. Positive pressure systems remain widely used for long-distance and multi-point transport, while vacuum systems are favored where cleanliness and controlled pickup matter most. Combination systems gain relevance in complex installations requiring flexible routing and staged handling. On the operational side, dense-phase conveying is preferred for fragile or abrasive materials, whereas dilute-phase conveying suits faster movement of materials that can tolerate higher air velocity.

Technology development is increasingly focused on energy management, smart controls, and material-specific handling performance. New controller platforms, test infrastructure, and blower improvements are refining how operators manage feed rates, pressure conditions, and conveying reliability. Suppliers are also improving system adaptability for dense-phase applications that require gentler transfer and lower particle degradation. This evolution is making pneumatic conveying more precise, more monitorable, and better aligned with digital plant operations.

The competitive environment is shaped by engineering capability, application knowledge, and the ability to deliver customized systems for different bulk solids. Market positioning depends on performance in dense and dilute conveying modes, automation compatibility, and support for highly regulated or technically demanding verticals. Competitive differentiation is therefore moving toward controllability, energy efficiency, and tested material-handling expertise rather than purely mechanical supply.

Pneumatic Conveying Systems Market - Strategic Insights:

Get more information on this report

Pneumatic Conveying Systems Market Segmentation Analysis:

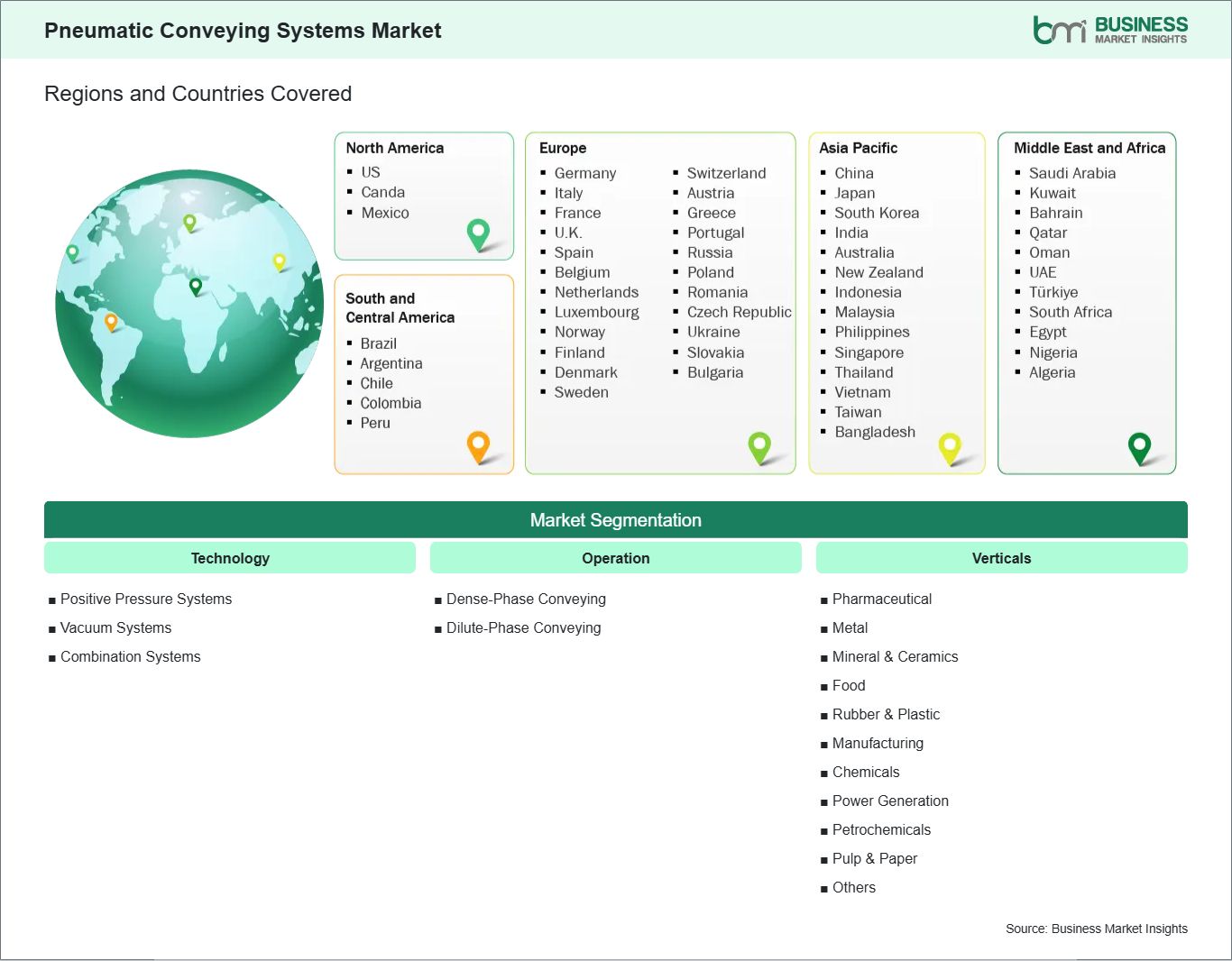

The pneumatic conveying systems market is segmented based on technology, operation, and industry vertical, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Technology

Positive Pressure Systems: Suited to longer routes and centralized discharge requirements.

Vacuum Systems: Preferred for controlled pickup and cleaner localized transfer.

Combination Systems: Addresses facilities needing flexible routing across multiple process stages.

By Operation

Dense-Phase Conveying: Protects fragile, abrasive, and segregating materials during transfer.

Dilute-Phase Conveying: Enables higher-speed movement for resilient bulk solids.

By Industry Vertical

Pharmaceutical: Requires contamination control, accuracy, and enclosed powder handling.

Metal, Mineral & Ceramics: Handles abrasive materials under demanding process conditions.

Food, and Rubber & Plastic: Supports clean transfer across mixed ingredient and resin applications.

Manufacturing: Integrates with automated lines for repeatable bulk material movement.

Chemicals: Prioritizes containment, reactor charging, and process safety.

Power Generation: Moves ash and related materials within utility and thermal systems.

Petrochemicals: Requires dependable transport for powders and process intermediates.

Pulp & Paper: Supports bulk additive and material transfer within continuous operations.

Others: Covers specialized installations shaped by unique material flow behavior.

Pneumatic Conveying Systems Market Drivers and Opportunities:

Rising Need for Enclosed, Automated Bulk Material Handling

Industrial plants are under stronger pressure to improve cleanliness, reduce manual intervention, and maintain consistent handling of powders and granules. Conventional open conveying methods often create dust, product loss, and uneven transfer conditions that complicate compliance and quality management. Pneumatic conveying systems address these constraints through enclosed transport, easier automation, and compatibility with upstream and downstream process equipment. Their fit is strongest in sectors where hygiene, worker safety, and material containment directly affect operational performance and plant design decisions.

The impact of this shift is widening across industries that process sensitive, fine, or hazardous bulk materials. Food and pharmaceutical plants value enclosed transfer to reduce contamination risk, while chemical and power facilities focus on containment, reliability, and handling efficiency. As manufacturers pursue better process discipline and reduced housekeeping burdens, pneumatic conveying moves from auxiliary equipment status toward a more central role in plant engineering. This increases its relevance in both retrofit projects and newly automated production environments.

Smart Dense-Phase Systems and Application Testing Infrastructure

A significant opportunity is emerging in advanced dense-phase conveying supported by digital control and full-scale material testing. Operators increasingly want proof that a conveying system can protect particle integrity, limit segregation, and perform consistently under real process conditions. Suppliers are responding with controller upgrades, specialized test centers, and material-specific engineering that improve design confidence before full installation. This trend is especially valuable in chemicals, metals, cement, food, and energy applications where bulk material behavior can vary sharply under pressure and velocity changes.

Future expansion is likely to come from systems that combine lower material stress with smarter monitoring and commissioning support. Facilities seeking higher efficiency and less trial-and-error during project planning are more likely to favor suppliers offering tested performance parameters and adaptable control architecture. That creates room for stronger market penetration in industries with difficult conveying profiles and high process risk. Smart dense-phase solutions therefore represent a pathway toward higher-value, engineering-led competition in this sector.

Pneumatic Conveying Systems Market Size and Share Analysis:

The pneumatic conveying systems market is projected to grow from US$ 8.42 billion in 2025 to US$ 13.71 billion by 2033. The market is estimated to record a CAGR of 6.28% from 2026 to 2033.

This growth path indicates steady expansion tied to automation investment, hygiene-focused processing, and the modernization of bulk material handling operations. The sector is benefiting from its ability to support both productivity goals and tighter process control within enclosed industrial environments.

By technology, positive pressure systems retain a strong market position because they are well suited to long conveying distances and centralized transfer networks. Vacuum systems remain influential where contained pickup and localized movement are operational priorities. Combination systems are gaining attention in complex plants that require routing flexibility across multiple handling points.

By verticals, food and pharmaceutical applications hold strong relevance due to cleanliness and contamination-control requirements. Chemicals, power generation, and petrochemicals also account for substantial demand because these sectors rely on enclosed transport for powders, ash, and sensitive intermediates. Manufacturing, minerals, and pulp-related uses broaden the market’s application base through varied material handling needs.

Pneumatic Conveying Systems Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Bosch Packaging Technology Inc.

Hardie Engineers Ltd.

Spiroflow Systems LLC

Weldo Inc.

Coperion GmbH

Krones AG

Schenck Process Group

Buettner Engineering Inc.

Material Handling Systems Inc.

Pneumatic Conveying Controls Inc.

Get more information on this report

Pneumatic Conveying Systems Market Report Coverage and Deliverables:

The "Pneumatic Conveying Systems Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Pneumatic Conveying Systems Market Geographic Insights:

The Pneumatic Conveying Systems market shows diverse regional adoption patterns influenced by industrial automation priorities, hygiene standards, bulk solids complexity, and the maturity of process manufacturing sectors. Across the global landscape, demand is closely linked to industries that require enclosed transfer of powders, granules, and abrasive materials under controlled operating conditions. The market’s regional profile therefore reflects differences in food processing, pharmaceuticals, chemicals, minerals, and energy infrastructure.

North America presents a technically mature market where processors emphasize reliability, containment, and integration with automated plant systems. Demand in the region is shaped by pharmaceutical production, food handling, specialty chemicals, and industrial manufacturing that require accurate and hygienic material movement. Buyers often prefer systems that reduce dust exposure, simplify plant layouts, and improve process consistency across multiple handling stages.

Asia Pacific reflects a broader industrial expansion story, supported by manufacturing growth, process industry investment, and wider use of bulk solids handling technologies. Demand is especially relevant in chemicals, food processing, power-related applications, and materials industries where plant modernization is reshaping equipment needs. The opening of new pneumatic conveying test infrastructure in India also highlights the region’s increasing importance for engineered dense-phase system evaluation and project planning.

Europe remains important due to its advanced process engineering base, strict product handling standards, and strong focus on efficient industrial operations. The region favors technologies that support precise material transfer, lower product degradation, and more predictable process control across regulated sectors. Beyond these major markets, emerging regions offer selective growth potential where industrialization, food production capacity, and energy-related materials handling create space for enclosed conveying solutions.

Get more information on this report

Pneumatic Conveying Systems Market Research Report Guidance:

The Pneumatic Conveying Systems report includes qualitative and quantitative data in the pneumatic conveying systems market across technology, operation, industry vertical, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the pneumatic conveying systems market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the pneumatic conveying systems market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the pneumatic conveying systems market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover pneumatic conveying systems market segments by technology, operation, industry vertical, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the pneumatic conveying systems market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Pneumatic Conveying Systems Market News and Key Development:

The pneumatic conveying systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In April 2026, Qlar is opening a new Test Center for reliable pneumatic conveying in Bangalore, India, supporting customers in the metals, cement and energy sectors. As the first Test Center in Asia with a conveyor line of 680 metres, the facility is one of the most powerful of its kind and enables realistic testing for dense-phase applications. With the facility, Qlar is strengthening its position as a provider of practical test infrastructure for material handling in demanding industries.

May 2026, Piab introduced the piEVO vacuum ejector pump, designed specifically for pneumatic vacuum conveyors handling powders, granules, and small parts. The new product offers improved vacuum generation, easier maintenance, and retrofit compatibility for existing conveying systems.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Pneumatic Conveying Systems Market

Bosch Packaging Technology Inc.

Hardie Engineers Ltd.

Spiroflow Systems LLC

Weldo Inc.

Coperion GmbH

Krones AG

Schenck Process Group

Buettner Engineering Inc.

Material Handling Systems Inc.

Pneumatic Conveying Controls Inc.

Frequently Asked Questions

How big is the Pneumatic Conveying Systems Market?

The Pneumatic Conveying Systems Market is valued at US$ 8.42 Billion in 2025, it is projected to reach US$ 13.71 Billion by 2033.

What is the CAGR for Pneumatic Conveying Systems Market by (2026 - 2033)?

As per our report Pneumatic Conveying Systems Market, the market size is valued at US$ 8.42 Billion in 2025, projecting it to reach US$ 13.71 Billion by 2033. This translates to a CAGR of approximately 6.28% during the forecast period.

What segments are covered in this report?

The Pneumatic Conveying Systems Market report typically cover these key segments-

Operation (Dense-Phase Conveying, and Dilute-Phase Conveying)

Verticals (Pharmaceutical, Metal, Mineral & Ceramics, Food, and Rubber & Plastic, Manufacturing, Chemicals, Power Generation, Petrochemicals, Pulp & Paper, Others)

What is the historic period, base year, and forecast period taken for Pneumatic Conveying Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Pneumatic Conveying Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Pneumatic Conveying Systems Market?

The Pneumatic Conveying Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Bosch Packaging Technology Inc.

Hardie Engineers Ltd.

Spiroflow Systems LLC

Weldo Inc.

Coperion GmbH

Krones AG

Schenck Process Group

Buettner Engineering Inc.

Material Handling Systems Inc.

Pneumatic Conveying Controls Inc.

Who should buy this report?

The Pneumatic Conveying Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Pneumatic Conveying Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Pneumatic Conveying Systems Market

Get Free Sample For Pneumatic Conveying Systems Market