01

Market Summery

Executive Summary and Global Market Analysis

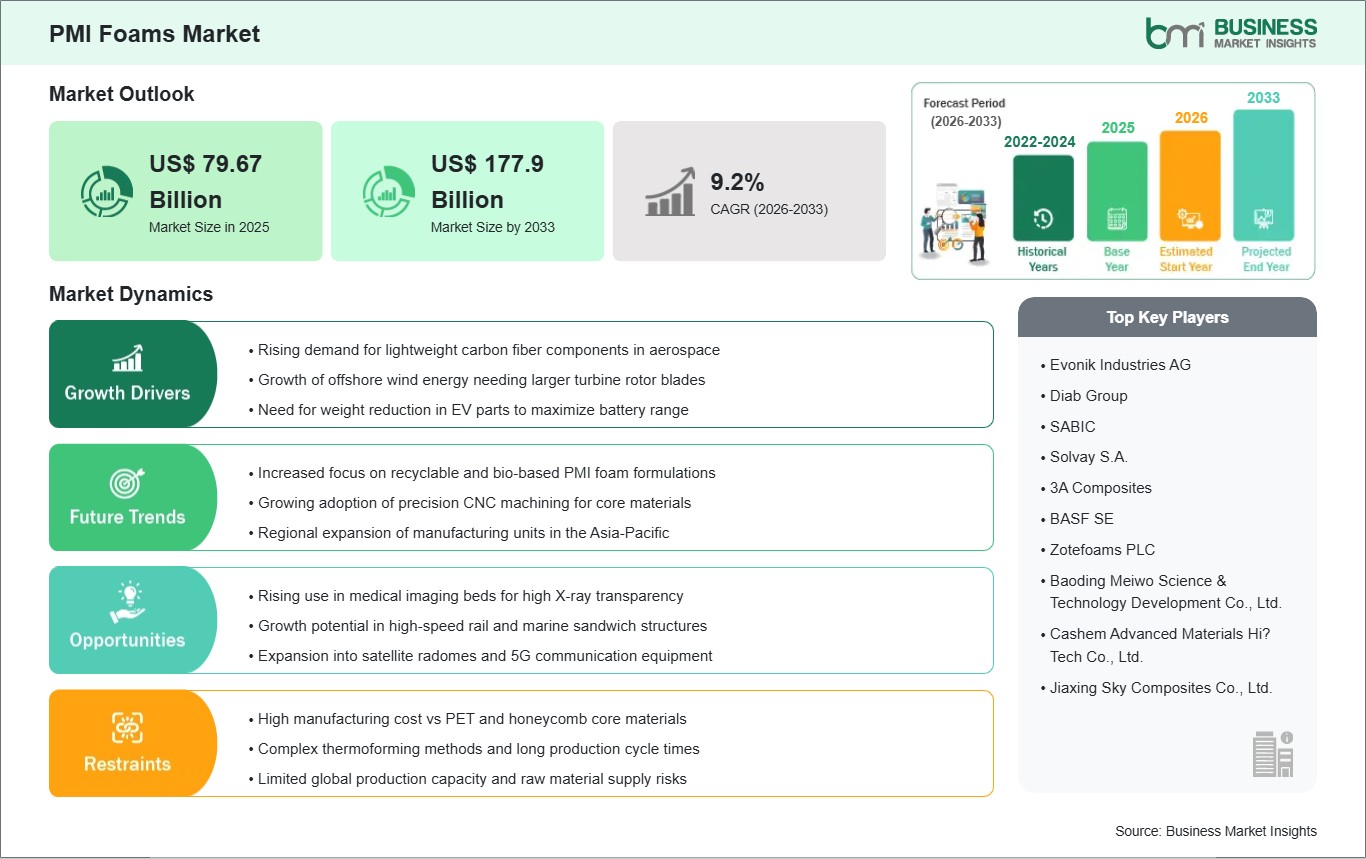

Polymethacrylimide (PMI) foams represent a specialized class of rigid, closed-cell structural materials that have become an essential cornerstone of modern composite engineering. Defined by their exceptional strength-to-weight ratio, high thermal stability, and superior resistance to compression creep, these foams serve as a critical core material in high-performance sandwich structures. In the aerospace industry, they enable the production of ultra-lightweight components that must withstand the rigorous temperatures and pressures of autoclave processing, which often exceed 180°C. Beyond structural integrity, PMI foams offer excellent dielectric properties and fire, smoke, and toxicity (FST) compliance, making them indispensable for applications ranging from 5G radomes to high-speed rail interiors.

However, the market faces significant challenges, primarily rooted in the complex and capital-intensive chemical processing required for production. The high cost of raw materials and specialized manufacturing nodes often results in a premium price point, which can restrain adoption in cost-sensitive industrial sectors. Additionally, technical hurdles related to ensuring cell uniformity across large-scale sheets and navigating global supply chain volatility for precursor chemicals can impact market stability.

Despite these restraints, the market is entering a phase of lucrative expansion. The global push for sustainability is driving a "lightweighting" revolution in the automotive and wind energy sectors, where PMI foams minimize resin uptake and maximize fuel or energy efficiency. Furthermore, the emergence of Urban Air Mobility (UAM) and the rapid development of 6G telecommunications infrastructure present substantial growth avenues for manufacturers. By integrating advanced foam cores into next-generation intelligent systems, the industry is poised to overcome historical cost barriers through economies of scale and specialized material innovation.

03

Segment Analysis

PMI Foams Market Segmentation

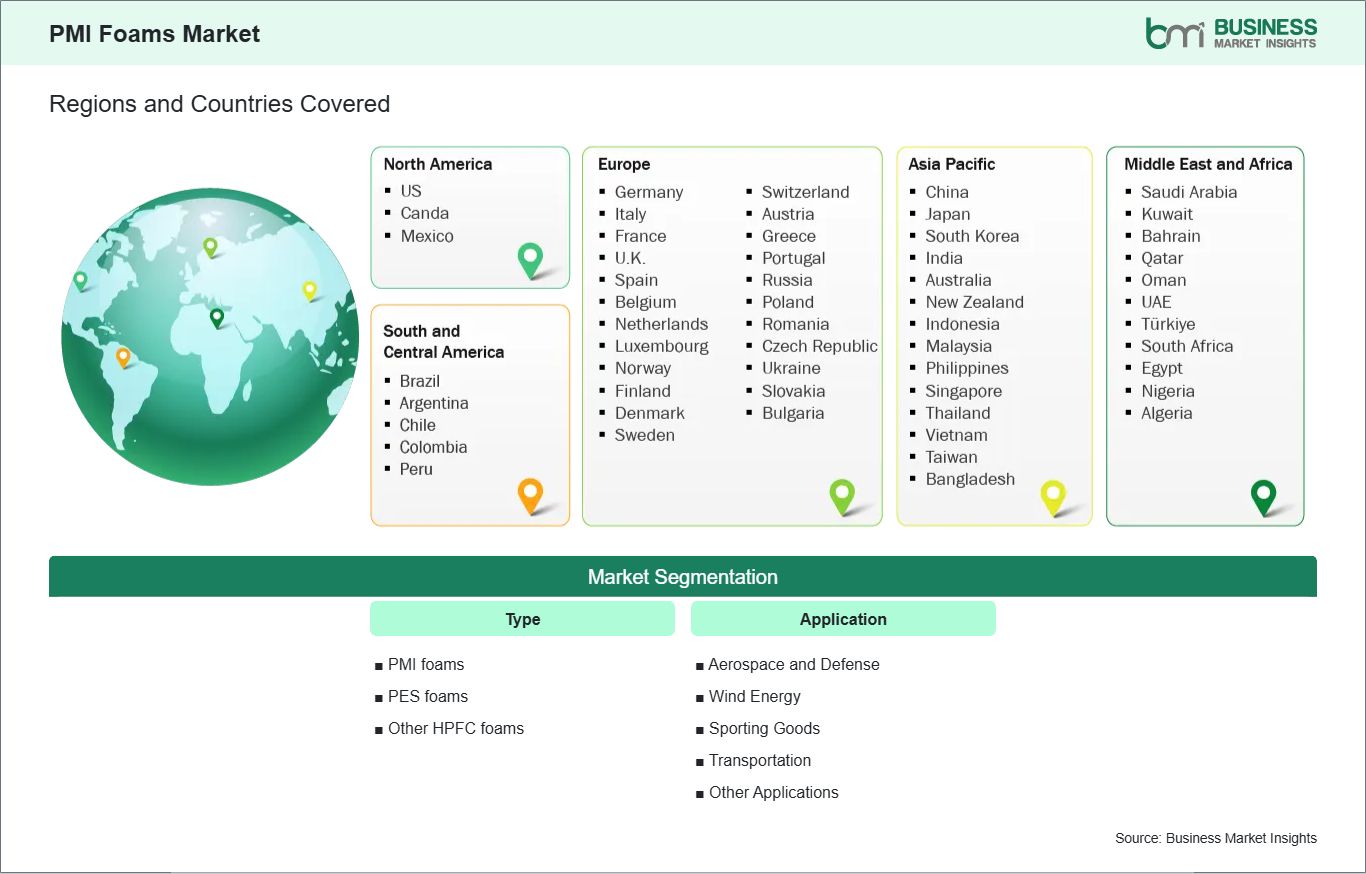

Key segments that contributed to the derivation of the PMI Foams market analysis are type and application.

- By Type, the market is segmented into PMI foams, PES foams, and Other HPFC foams.

- By Application, the market is categorized into Aerospace and Defense, Wind Energy, Sporting Goods, Transportation, and Others.

04

Market Forces

PMI Foams Market Drivers and Opportunities

Rising Adoption of Composite Materials in Aerospace &Defense Sector

The primary catalyst for the expansion of the polymethacrylimide foam market is the relentless pursuit of weight reduction within the global aviation and defense industries. As aerospace original equipment manufacturers focus on enhancing fuel efficiency and increasing payload capacities, there has been a significant transition toward carbon-fiber-reinforced polymer sandwich structures. PMI foam is uniquely positioned as the core material of choice for these advanced composites due to its peerless specific strength and stiffness. Unlike traditional core materials that may collapse or outgas under extreme conditions, these foams maintain their dimensional stability during high-pressure and high-temperature autoclave processing. This thermal resilience allows engineers to co-cure the foam core with advanced resin systems in a single production step, significantly streamlining manufacturing timelines while ensuring structural integrity.

In the defense subsector, the driver is further amplified by the increasing complexity of unmanned aerial vehicles and stealth technology. The material's exceptional fatigue resistance and impact strength make it ideal for airframe sections exposed to high dynamic loads, such as helicopter rotor blades and pressure bulkheads. Furthermore, because the foam features a fine, closed-cell structure, it minimizes resin absorption during vacuum infusion, ensuring the final component remains as light as possible. This combination of high-temperature processing compatibility and superior mechanical performance ensures that as the next generation of commercial and military aircraft becomes more composite-intensive, the reliance on high-performance structural foams will continue to intensify across the global aerospace supply chain.

Expansion into Renewable Energy and 6G Infrastructure

A transformative opportunity for the market lies in the rapid scaling of renewable energy infrastructure and the burgeoning requirements of next-generation telecommunications. In the wind energy sector, the shift toward offshore installations has necessitated the development of much larger turbine blades to capture higher wind speeds. As these blades reach immense lengths, the demand for lightweight core materials that provide high shear strength and resistance to long-term fatigue becomes paramount. PMI foams offer a distinct advantage here, as their high-performance characteristics allow for the construction of stiffer, more durable blades that can withstand the harsh, repetitive stresses of maritime environments without the weight penalties associated with legacy materials. This shift toward "green" energy projects represents a major untapped volume market for foam producers.

Parallel to energy, the evolution of telecommunications toward 6G and advanced satellite constellations presents a highly specialized and lucrative avenue. PMI foams possess a dielectric constant and loss tangent nearly identical to air, making them virtually "invisible" to electromagnetic waves. This signal transparency is critical for the development of radomes and antenna covers that must protect sensitive electronics without interfering with ultra-high-frequency transmissions. As the world moves toward a hyper-connected era requiring massive MIMO antenna systems and high-throughput satellite links, the need for structural materials that double as wave-transparent shields will skyrocket. This dual-track opportunity in renewable energy and high-frequency communication ensures that the market can diversify away from its traditional aerospace core, tapping into the foundational technologies of the future global economy.

05

Size and Share Analysis

PMI Foams Market Size and Share Analysis

The PMI Foams market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type and application, offering insights into their contribution to overall market performance.

In terms of type, the PMI foams sub-segment maintains the largest share of the market due to its unrivaled mechanical properties and thermal resistance compared to other high-performance cores.

By application, the Aerospace and Defense sub-segment accounts for the most significant portion of revenue, driven by the critical necessity for weight reduction in structural airframe components.

07

Report Coverage

PMI Foams Market Report Coverage and Deliverables

The "PMI Foams Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- PMI Foams market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- PMI Foams market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- PMI Foams market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the PMI Foams market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

PMI Foams Market Geographic Insights

The geographical scope of the PMI Foams market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

In North America, market activity is anchored by a high concentration of aerospace and defense manufacturing, where the material's superior strength-to-weight ratio is vital for advanced military aviation and satellite programs. Europe maintains a sophisticated market presence characterized by stringent environmental regulations and a strong emphasis on sustainability, driving the integration of high-performance foams into eco-efficient rail systems and automotive lightweighting initiatives. The Asia-Pacific region serves as a primary engine for growth, fueled by the rapid expansion of offshore wind energy capacity and the domestic development of commercial aircraft manufacturing hubs.

In the Middle East & Africa, the market is evolving through the modernization of telecommunications infrastructure and the specification of high-performance materials in large-scale smart city giga-projects. Meanwhile, South & Central America are witnessing steady development as regional industrial sectors undergo digital transformation and seek more durable, high-performance core materials for local transportation and sporting goods manufacturing. This diversified regional footprint ensures market resilience as global economies increasingly prioritize high-efficiency, lightweight material solutions.

10

Industry Activity

Recent Developments

The PMI Foams market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the PMI Foams market are:

- In November 2025, Zotefoams completed the acquisition of Overseas Konstellation Company S.A., a prominent producer of high-quality technical foams based in Anglesola, Spain. This strategic acquisition allowed Zotefoams to enhance its manufacturing footprint in continental Europe and broaden its specialized product offering, which included high-performance PMI foams. The move directly supported the company's long-term "Expanding Beyond the Core" growth strategy by strengthening its ability to deliver advanced structural materials to a wider European client base.

- In September 2024, Evonik upgraded the production process for its high-performance PMI foams, specifically the ROHACELL® brand, at its primary facility in Darmstadt, Germany, to rely exclusively on electricity from renewable energy sources. This strategic shift allowed the company's High Performance Polymers business line to eliminate 3,400 metric tons of carbon dioxide emissions from its annual operations.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade Indicators World Trade Organization (WTO) International Monetary Fund (IMF) International Trade Administration (ITA) Company website Company annual reports Company investor presentations