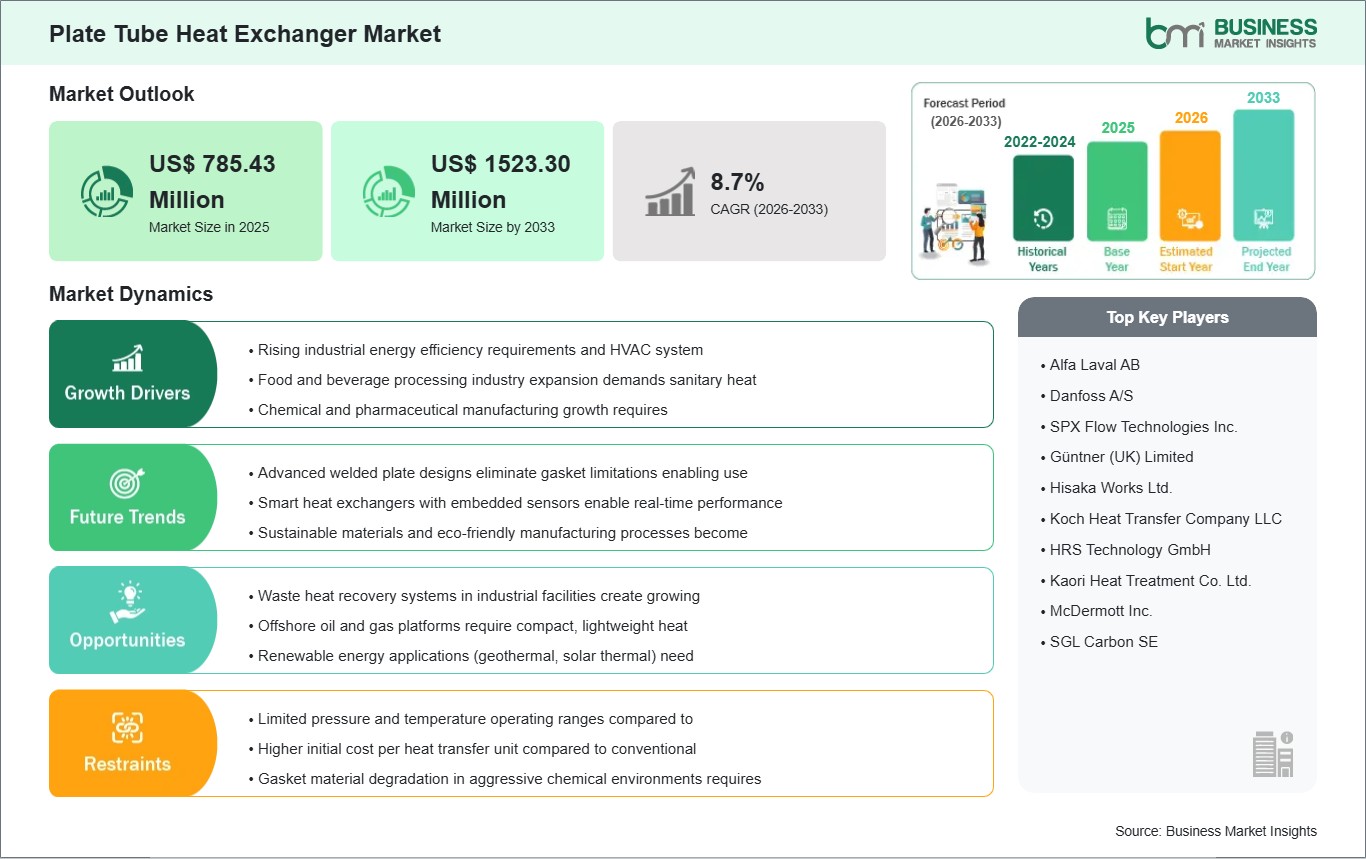

The plate tube heat exchanger market size is expected to reach US$ 1.52 billion by 2033 from US$ 0.78 billion in 2025. The market is estimated to record a CAGR of 8.70% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Plate tube heat exchangers are thermal transfer systems designed to combine plate-based flow efficiency with tube-side mechanical durability in demanding process environments. Their configuration supports compact heat recovery, strong pressure handling, and efficient thermal exchange across industrial duties where fluids differ in temperature, viscosity, or fouling behavior. These systems are selected when operators need a balance between serviceability, thermal performance, and material adaptability across corrosive or high-load applications. Their relevance continues to expand as industrial facilities modernize heat management infrastructure.

Procurement momentum is linked to plant-level efficiency targets, process intensification, and stricter operating expectations across energy and industrial sectors. Operators in power generation, oil and gas, chemicals, refrigeration, and marine settings increasingly evaluate exchanger technologies through lifecycle performance rather than initial hardware cost alone. This preference supports wider use of plate tube designs in installations where thermal recovery, footprint reduction, and maintenance accessibility influence capital allocation. As facilities seek more stable and efficient process control, these exchangers are becoming more integrated into equipment upgrade programs.

Segment positioning is shaped mainly by metallurgy and end-use operating conditions. Stainless steel remains highly relevant because it supports corrosion resistance, fabrication practicality, and broad process compatibility, while titanium and nickel alloys address more aggressive service environments. On the application side, power generation and oil and gas retain strong commercial importance because both depend on durable thermal systems that can operate under continuous and technically demanding conditions. Refrigeration, chemicals, and marine applications broaden the market by requiring tailored thermal configurations rather than standardized units.

Technology development is moving toward higher thermal efficiency, lower fouling tendency, and improved compatibility with harsher duty cycles. Manufacturers are refining welded and semi-welded designs, extending material options, and creating larger heat transfer platforms suited to energy transition projects and heavy industry. Product direction also reflects interest in reduced footprint and lower operating cost without compromising pressure capability. These advances strengthen the position of plate tube and adjacent hybrid exchanger concepts in modern industrial processing.

Competitive conditions are evolving through product specialization, capacity expansion, and application-led innovation. Suppliers are differentiating through engineered designs for high-pressure duties, broader manufacturing reach, and solutions tailored to sectors facing decarbonization and process efficiency demands. The market therefore reflects a technical competition centered on durability, thermal intensity, and adaptability across industrial operating environments.

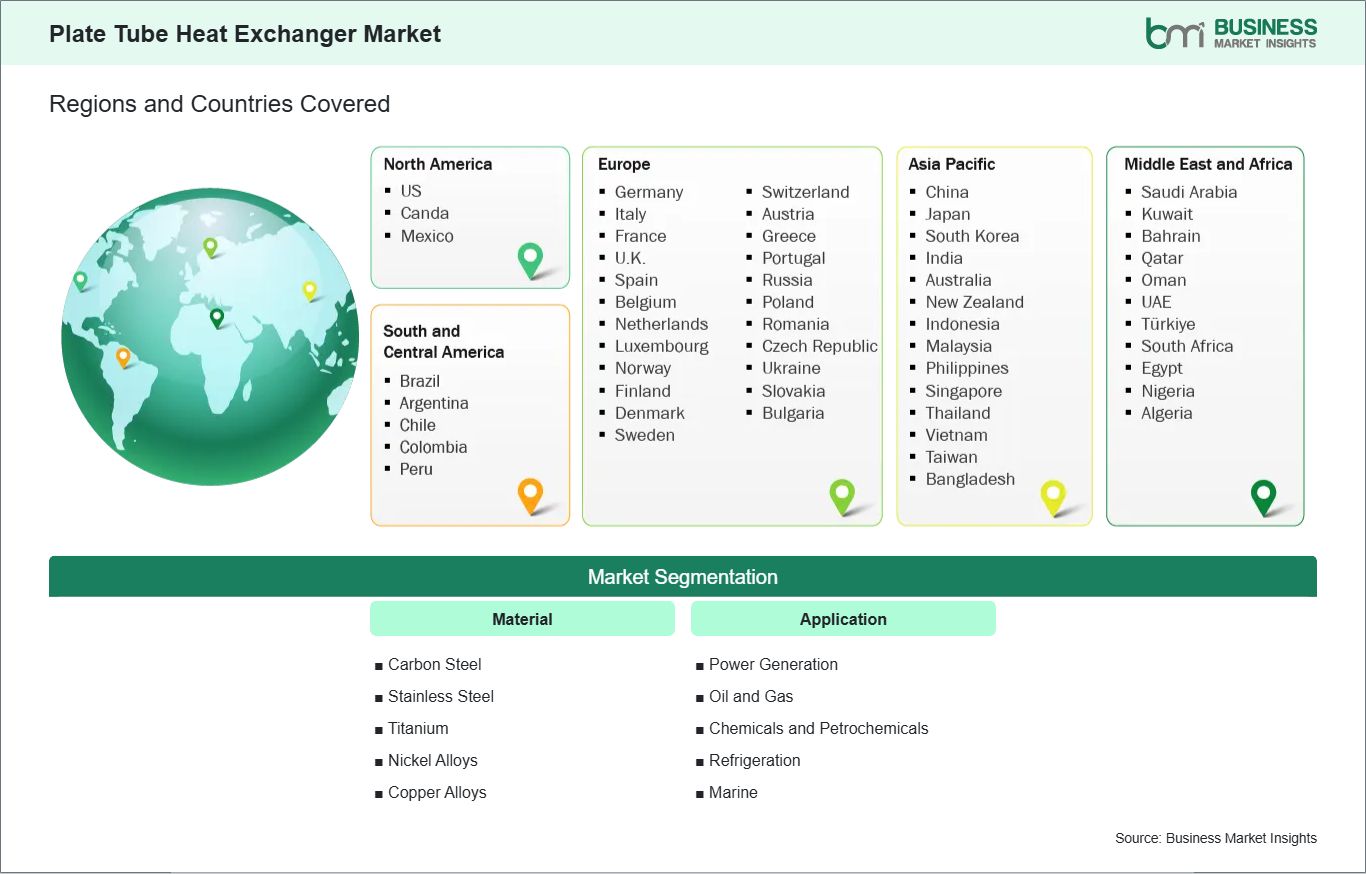

The plate tube heat exchanger market is segmented based on material and application, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Material

Carbon Steel: Chosen for cost-conscious duties with manageable corrosion exposure.

Titanium: Handles aggressive media and marine conditions with strong durability.

Nickel Alloys: Supports severe chemical environments and elevated thermal stress.

Copper Alloys: Performs well in applications requiring strong thermal conductivity.

By Application

Power Generation: Relies on efficient heat transfer for continuous plant operation.

Oil and Gas: Requires rugged exchangers for pressure-intensive and corrosive process streams.

Chemicals and Petrochemicals: Prioritizes material resilience and process-specific thermal control.

Refrigeration: Favors compact systems with effective cooling performance and service access.

Marine: Uses corrosion-resistant equipment for constrained and demanding onboard environments.

Plate Tube Heat Exchanger Market Drivers and Opportunities:

Industrial Focus on Thermal Efficiency and Process Reliability

Industrial operators are placing greater attention on heat recovery, stable operating conditions, and equipment efficiency as energy costs and process complexity reshape capital priorities. In this setting, exchanger selection increasingly centers on technologies that improve thermal transfer while accommodating pressure, corrosion, and maintenance constraints. Plate tube heat exchangers address these needs by combining compact transfer characteristics with mechanical strength suited to demanding plant conditions. Their use becomes more attractive where downtime, energy loss, and service limitations directly affect operating margins across power, chemicals, and hydrocarbon processing environments.

The market impact is visible in projects where plant modernization depends on better thermal management rather than wholesale process redesign. Facilities seeking performance improvement often prioritize equipment that can be integrated into existing systems while enhancing heat exchange efficiency and serviceability. This makes plate tube systems commercially relevant in applications where operational continuity outweighs low-cost standardization. As more sectors evaluate lifecycle efficiency and resilience together, the industry gains traction through technically specific replacement and upgrade demand.

Advanced Materials and High-Performance Hybrid Designs

A clear opportunity is emerging through exchanger designs that combine material sophistication with application-specific engineering. Industrial users are seeking systems that can tolerate harsher fluids, support more compact layouts, and maintain performance under tougher duty cycles. In response, manufacturers are expanding welded and semi-welded platforms, broadening alloy choices, and introducing larger high-capacity designs aimed at energy transition and heavy industrial service. These developments improve suitability for corrosive chemicals, marine environments, advanced cooling duties, and thermal systems linked to modern power infrastructure.

Future scope is especially promising in projects where footprint, efficiency, and durability must be optimized simultaneously. High-performance materials such as titanium and nickel alloys support expansion into applications where conventional exchanger formats face operational limits. At the same time, innovation in compact heavy-duty platforms creates room for deployment in new process configurations and retrofit programs. This opens a pathway for the market to compete on engineering value, not merely on equipment replacement cycles.

Plate Tube Heat Exchanger Market Size and Share Analysis:

The plate tube heat exchanger market is projected to grow from US$ 0.78 billion in 2025 to US$ 1.52 billion by 2033. The market is estimated to record a CAGR of 8.70% from 2026 to 2033.

This growth path indicates a sector moving into broader industrial relevance as operators place more emphasis on energy efficiency, compact thermal systems, and application-specific process equipment. The market’s trajectory reflects strengthening acceptance in technically demanding environments rather than volume-led commoditization.

By material, stainless steel holds a central position because it offers a practical balance of corrosion resistance, cost control, and fabrication flexibility. Titanium and nickel alloys maintain importance in severe-duty environments where media aggressiveness and long service life shape procurement decisions. Carbon steel and copper alloys remain applicable in selected duties where operating conditions align with their economic and thermal characteristics.

By application, power generation retains strong influence due to its constant requirement for efficient thermal transfer and reliable equipment operation. Oil and gas and chemicals also represent significant demand centers because process intensity and fluid complexity favor engineered exchanger solutions. Refrigeration and marine segments contribute additional scope through compact installation requirements and corrosion-sensitive operating settings.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Alfa Laval AB

Danfoss A/S

SPX Flow Technologies Inc.

Güntner (UK) Limited

Hisaka Works Ltd.

Koch Heat Transfer Company LLC

HRS Technology GmbH

Kaori Heat Treatment Co. Ltd.

McDermott Inc.

SGL Carbon SE

Get more information on this report

Plate Tube Heat Exchanger Market Report Coverage and Deliverables:

The "Plate Tube Heat Exchanger Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Plate Tube Heat Exchanger market shows diverse regional adoption patterns influenced by industrial heat recovery priorities, process plant complexity, metallurgy requirements, and energy infrastructure investment. Across the global landscape, deployment is shaped by the need for compact and durable heat transfer equipment that can perform reliably in high-load environments. Regional differences emerge from the structure of local industries, the prevalence of heavy process sectors, and the pace of thermal system modernization.

North America presents a replacement and optimization-oriented market environment where operators seek high-performance thermal equipment for established industrial assets. Demand is tied closely to oil and gas processing, chemical production, refrigeration infrastructure, and power-related thermal systems. Buyers in the region tend to emphasize lifecycle reliability, maintainability, and compatibility with stringent operating standards when selecting advanced exchanger platforms.

Asia Pacific reflects a broader expansion profile linked to industrial buildout, marine activity, refining operations, and refrigeration demand across manufacturing networks. The region benefits from continued investment in process industries that require compact thermal systems capable of serving both conventional and modernized plant configurations. Material choice and application fit remain especially important here because plant operators often balance scale, performance, and cost sensitivity within fast-moving industrial programs.

Europe shows a more efficiency-centered pattern shaped by energy transition goals, engineering specialization, and tight process performance expectations. Industrial users in the region increasingly favor exchanger systems that support lower energy intensity, reliable heat recovery, and compact installation in constrained operating environments. Beyond these established regions, selective opportunities are emerging in the Middle East, Africa, and Latin America where refining, marine infrastructure, and industrial cooling needs create room for technically robust exchanger deployment.

Get more information on this report

Plate Tube Heat Exchanger Market Research Report Guidance:

The Plate Tube Heat Exchanger market report includes qualitative and quantitative data in the plate tube heat exchanger market across material and application and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the plate tube heat exchanger market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the plate tube heat exchanger market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the plate tube heat exchanger market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover plate tube heat exchanger market segments by material, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the plate tube heat exchanger market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Plate Tube Heat Exchanger Market News and Key Development:

The plate tube heat exchanger market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In June 2026, Alfa Laval announces the launch of TS45, the company’s largest semi-welded plate heat exchanger to date, engineered to secure competitiveness and resilience by meeting growing demands for high-capacity, high-pressure heat transfer across energy transition, industrial, and energy efficiency applications. Developed to support industries facing rising energy demand and high efficiency requirements, TS45 expands Alfa Laval’s semi-welded portfolio into duties traditionally served by shell and tube technologies. The new TS45 enables customers to scale up heat transfer performance while maintaining a compact footprint, high energy efficiency, and full serviceability.

In February 2026, Danfoss launched the B3-260C brazed plate heat exchanger specifically for cooling distribution units (CDUs) used in data centers. The product addresses increasing demand for efficient thermal management in AI and hyperscale computing facilities

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Plate Tube Heat Exchanger Market

Alfa Laval AB

Danfoss A/S

SPX Flow Technologies Inc.

Güntner (UK) Limited

Hisaka Works Ltd.

Koch Heat Transfer Company LLC

HRS Technology GmbH

Kaori Heat Treatment Co. Ltd.

McDermott Inc.

SGL Carbon SE

Frequently Asked Questions

How big is the Plate Tube Heat Exchanger Market?

The Plate Tube Heat Exchanger Market is valued at US$ 785.43 Million in 2025, it is projected to reach US$ 1523.30 Million by 2033.

What is the CAGR for Plate Tube Heat Exchanger Market by (2026 - 2033)?

As per our report Plate Tube Heat Exchanger Market, the market size is valued at US$ 785.43 Million in 2025, projecting it to reach US$ 1523.30 Million by 2033. This translates to a CAGR of approximately 8.7% during the forecast period.

What segments are covered in this report?

The Plate Tube Heat Exchanger Market report typically cover these key segments-

Material (Carbon Steel, Stainless Steel, Titanium, Nickel Alloys, Copper Alloys)

Application (Power Generation, Oil and Gas, Chemicals and Petrochemicals, Refrigeration, Marine)

What is the historic period, base year, and forecast period taken for Plate Tube Heat Exchanger Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Plate Tube Heat Exchanger Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Plate Tube Heat Exchanger Market?

The Plate Tube Heat Exchanger Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Alfa Laval AB

Danfoss A/S

SPX Flow Technologies Inc.

Güntner (UK) Limited

Hisaka Works Ltd.

Koch Heat Transfer Company LLC

HRS Technology GmbH

Kaori Heat Treatment Co. Ltd.

McDermott Inc.

SGL Carbon SE

Who should buy this report?

The Plate Tube Heat Exchanger Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Plate Tube Heat Exchanger Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Plate Tube Heat Exchanger Market

Get Free Sample For Plate Tube Heat Exchanger Market