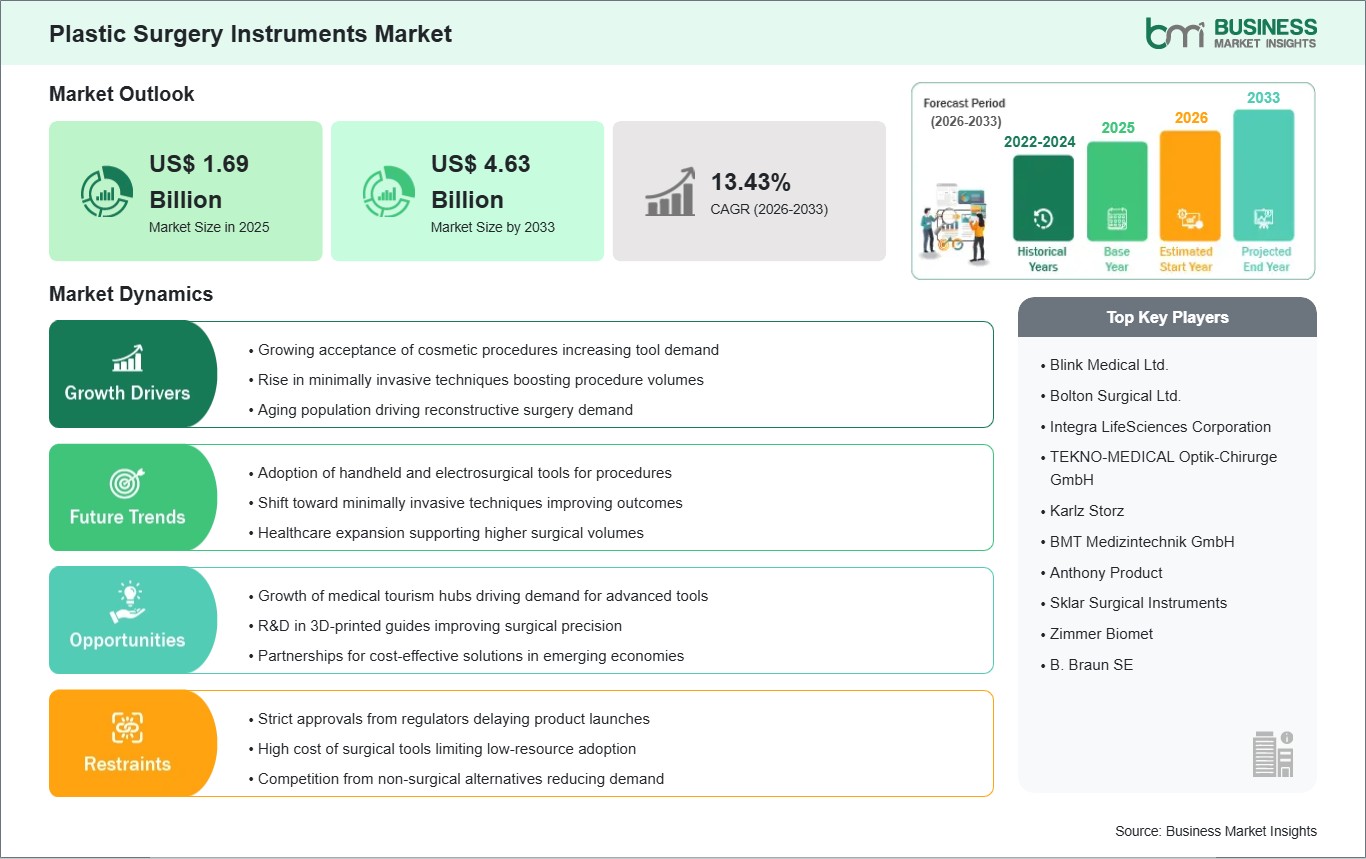

The Plastic Surgery Instruments Market size is expected to reach US$ 4.63 billion by 2033 from US$ 1.69 billion in 2025. The market is estimated to record a CAGR of 13.43% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Plastic surgery instruments are specialized, handheld, and energy-based tools designed for precise manipulation of skin, soft tissue, and bone. They are essential for both reconstructive surgeries after trauma or oncology and elective cosmetic procedures. Market growth is driven by the global normalization of aesthetic procedures influenced by social media, the rapid adoption of minimally invasive techniques that reduce patient recovery time, and increased demand from an aging population. Additionally, the shift toward Ambulatory Surgical Centers, which focus on high-volume outpatient procedures, is increasing demand for specialized, often single-use or durable instrument sets.

However, several challenges may limit market growth. High capital costs for advanced energy-based systems often restrict adoption in smaller private clinics. Stringent regulatory requirements, including the transition to new Medical Device Regulations in Europe, increase compliance costs and delay the introduction of innovative micro-tools. The industry also faces competition from non-surgical alternatives, such as injectables and laser therapies, which can reduce demand for traditional surgical procedures requiring specialized instruments.

Despite these challenges, the market offers significant opportunities. Growth in medical tourism hubs in Asia and Latin America and the adoption of 3D-printed, patient-specific surgical guides are expanding the market. The rise of robotic-assisted plastic surgery and the development of gender-specific ergonomic handles are also expected to drive long-term growth.

Plastic Surgery Instruments Market - Strategic Insights:

Get more information on this report

Plastic Surgery Instruments Market Segmentation Analysis:

Key segments that contributed to the derivation of the Plastic Surgery Instruments market analysis are type, procedure, and end user.

By Type, the market is segmented into Handheld Instruments, Electrosurgical Instruments, and Other Plastic Surgery Instruments.

By Procedure, the market is divided into Cosmetic Surgery and Reconstructive Surgery.

By End User, the market is categorized into Dermatology Clinics, Hospitals, and Other End Users.

Plastic Surgery Instruments Market Drivers and Opportunities:

Aesthetic Normalization and the Surge in Minimally Invasive Reconstruction

The primary driver of the Plastic Surgery Instruments Market is the global increase in both cosmetic and reconstructive procedure volumes. The growing influence of social media and the prevalence of selfie culture serve as dominant catalysts, reducing the social stigma associated with aesthetic procedures and promoting prejuvenation trends among younger populations. This trend is further supported by the adoption of minimally invasive and electrosurgical techniques. As surgeons increasingly favor smaller incisions, the demand for bipolar and monopolar electrosurgical systems, which provide greater precision and reduced operative times, is surpassing that for traditional handheld instruments.

Additionally, the aging global population is a significant factor, as older adults more frequently seek reconstructive surgeries for age-related tissue degeneration and skin cancer repairs. The rise in body contouring procedures following substantial weight loss has also generated a new patient cohort requiring complex surgical interventions. Collectively, these factors, normalization of aesthetic procedures, advancements in surgical technology, and demographic changes, are driving sustained growth in the global plastic surgery supply chain.

AI-Integrated Robotics and 3D-Printed Custom Toolsets

A significant opportunity exists in the integration of plastic surgery instruments with robotic-assisted systems and AI-driven navigation. Next-generation robotic platforms are under development for super-microsurgery, allowing surgeons to perform complex lymphatic and nerve repairs with a level of stability and precision beyond human capability. Additionally, the advancement of 3D-printed, patient-specific surgical guides and instruments represents a major growth area. Utilizing preoperative imaging to produce custom templates for facial reconstruction enables manufacturers to enhance anatomical accuracy and achieve improved aesthetic symmetry.

The expansion of single-use, ergonomic handheld instruments presents a lucrative opportunity for ambulatory surgical centers (ASCs), which prioritize disposable tools to reduce costs and minimize infection risks associated with traditional sterilization. In addition to hardware innovations, the emergence of augmented reality (AR) overlay systems introduces a new frontier, integrating instruments with headsets that project the patient's internal vascular anatomy onto the skin surface during surgery. Manufacturers emphasizing titanium-alloy lightweight designs and pioneering regenerative aesthetic add-ons, such as fat-transfer cannulas, are well positioned to lead the plastic surgery instruments market.

Plastic Surgery Instruments Market Size and Share Analysis:

The Plastic Surgery Instruments market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, procedure, and end user, offering insights into their contribution to overall market performance.

Based on procedure, the Cosmetic Surgery and Reconstructive Surgery subsegment holds a significant share of the market, with increasingly interconnected drivers. Cosmetic Surgery remains essential, driven by the widespread acceptance of procedures such as rhinoplasty and breast augmentation. A key trend is the growth of the Reconstructive Surgery subsegment, particularly in Oncology-Related Repair and Congenital Correction, which are experiencing increased demand. In these fields, plastic surgery instruments are critical for Functional Aesthetics, as specialized microsurgical kits facilitate the complex vascular and nerve suturing necessary for successful tissue flap transfers and limb salvage.

Plastic Surgery Instruments Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Blink Medical Ltd.

Bolton Surgical Ltd.

Integra LifeSciences Corporation

TEKNO-MEDICAL Optik-Chirurge GmbH

Karlz Storz

BMT Medizintechnik GmbH

Anthony Product

Sklar Surgical Instruments

Zimmer Biomet

B. Braun SE

Get more information on this report

Plastic Surgery Instruments Market Report Coverage and Deliverables:

The "Plastic Surgery Instruments Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Plastic Surgery Instruments market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Plastic Surgery Instruments market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Plastic Surgery Instruments market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Plastic Surgery Instruments market

Detailed company profiles, including SWOT analysis

Plastic Surgery Instruments Market Geographic Insights:

The geographical scope of the Plastic Surgery Instruments market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America remains the leading region in the global market, supported by the highest volume of surgical aesthetic procedures and a significant concentration of board-certified surgeons employing advanced handheld and electrosurgical instruments. Europe sustains strong demand for reconstructive and aesthetic instruments, especially in Germany and France, where there is a marked preference for high-quality stainless steel and titanium micro-instruments. The Asia Pacific region is identified as the fastest-growing market, driven by expanding medical tourism in South Korea and Thailand and increasing disposable incomes in China and India.

The Asia-Pacific plastic surgery instruments market is segmented into China, Japan, South Korea, India, Australia, and the rest of Asia Pacific. South Korea continues to serve as a global center for facial and bone contouring, resulting in elevated demand for specialized rasps, osteotomes, and chisels. In China, market expansion is attributed to the increasing prevalence of minimally invasive 'lunch-time' procedures that require specialized needles and cannulas. India is experiencing growth in reconstructive surgeries following trauma and congenital repairs, while Australia demonstrates consistent growth in breast augmentation and body contouring instrumentation.

Get more information on this report

Plastic Surgery Instruments Market Research Report Guidance:

The report includes qualitative and quantitative data in the Plastic Surgery Instruments market across type, procedure, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Plastic Surgery Instruments market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Plastic Surgery Instruments market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Plastic Surgery Instruments market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Plastic Surgery Instruments market segments by type, procedure, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Plastic Surgery Instruments market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Plastic Surgery Instruments Market News and Key Development:

The Plastic Surgery Instruments market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Plastic Surgery Instruments market are:

In July 2025, ZEISS Medical Technology launched the PENTERO® 800 S surgical microscope in China, approved by the NMPA. Designed for neuro, spine, ENT, and plastic/reconstructive surgery, the device features 4K 3D visualization, enhanced magnification, and ergonomic design, strengthening high-end surgical capabilities in the Chinese market.

In January 2025, MicroAire Surgical Instruments acquired NEOSYAD, integrating its AdiMate® device and Adipure® single-use kit into MicroAire`s portfolio. The technology, approved under EU MDR, combines infiltration, liposuction, and adipose tissue preparation in a single system, reducing operating times and ensuring high-quality fat for lipofilling procedures. This acquisition strengthens MicroAire`s leadership in the global plastic and reconstructive surgery instruments market.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Plastic Surgery Instruments Market

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Frequently Asked Questions

How big is the Plastic Surgery Instruments Market?

The Plastic Surgery Instruments Market is valued at US$ 1.69 Billion in 2025, it is projected to reach US$ 4.63 Billion by 2033.

What is the CAGR for Plastic Surgery Instruments Market by (2026 - 2033)?

As per our report Plastic Surgery Instruments Market, the market size is valued at US$ 1.69 Billion in 2025, projecting it to reach US$ 4.63 Billion by 2033. This translates to a CAGR of approximately 13.43% during the forecast period.

What segments are covered in this report?

The Plastic Surgery Instruments Market report typically cover these key segments-

Type (Handheld Instruments, Electrosurgical Instruments, and Other Plastic Surgery Instruments)

Procedure (Cosmetic Surgery and Reconstructive Surgery)

End User (Dermatology Clinics, Hospitals, and Other End Users)

What is the historic period, base year, and forecast period taken for Plastic Surgery Instruments Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Plastic Surgery Instruments Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Plastic Surgery Instruments Market?

The Plastic Surgery Instruments Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Blink Medical Ltd.

Bolton Surgical Ltd.

Integra LifeSciences Corporation

TEKNO-MEDICAL Optik-Chirurge GmbH

Karlz Storz

BMT Medizintechnik GmbH

Anthony Product

Sklar Surgical Instruments

Zimmer Biomet

B. Braun SE

Who should buy this report?

The Plastic Surgery Instruments Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Plastic Surgery Instruments Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Plastic Surgery Instruments Market

Get Free Sample For Plastic Surgery Instruments Market