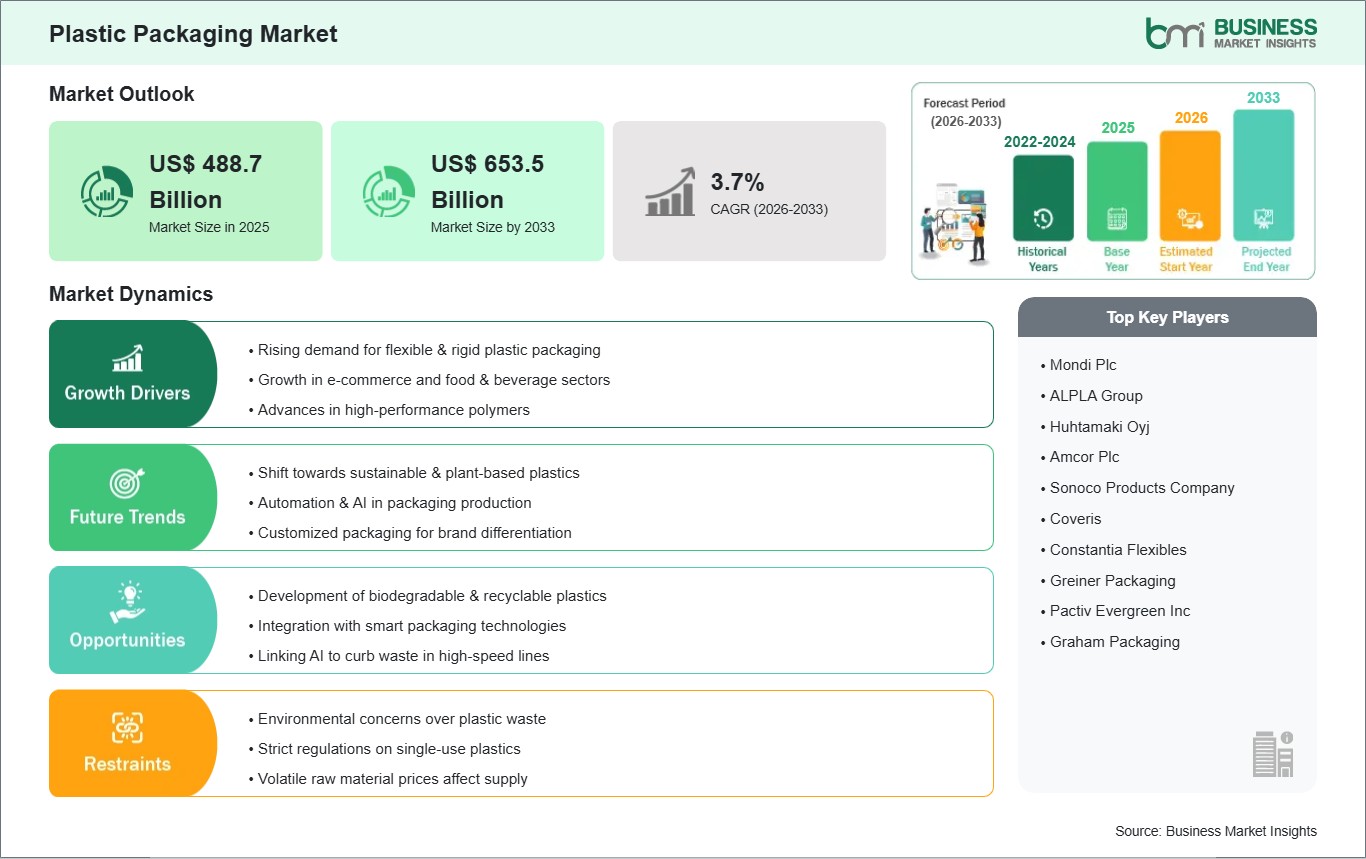

The Plastic Packaging Market size is expected to reach US$ 653.5 Billion by 2033 from US$ 488.7 Billion in 2025. The market is estimated to record a CAGR of 3.70% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Plastic Packaging serves as the primary logistical and preservation backbone for the global economy, encompassing rigid packaging (PET bottles, HDPE containers) and flexible packaging (films, pouches, wraps). These solutions offer distinct advantages, including significant reductions in transportation-related carbon emissions due to their low weight and high cost-efficiency compared to glass or metal. Growth is fueled by the explosive rise of e-commerce, the burgeoning demand for convenience foods and beverages, and the critical need for sterile medical and pharmaceutical packaging. Furthermore, the shift toward circular economy models is driving the adoption of Post-Consumer Recycled (PCR) resins and mono-material designs for easier recycling.

However, several challenges can restrain market growth: stringent global regulations and single-use plastic bans pose a constant compliance hurdle for manufacturers. Extreme price volatility of oil-based feedstocks, such as polyethylene and polypropylene, creates significant margin pressure and supply chain instability. Additionally, the industry faces constraints due to inadequate recycling infrastructure in emerging economies and growing consumer pushback against non-biodegradable waste. Despite these hurdles, the market holds immense opportunities in the universal mandate for sustainable materials, the accelerating deployment of bioplastics (PLA and PHA), and the increasing reliance on "Smart Packaging" (RFID and QR integration) for real-time traceability. The transition toward AI-driven material lightweighting and chemical recycling technologies is expected to create significant opportunities for market growth.

Plastic Packaging Market - Strategic Insights:

Get more information on this report

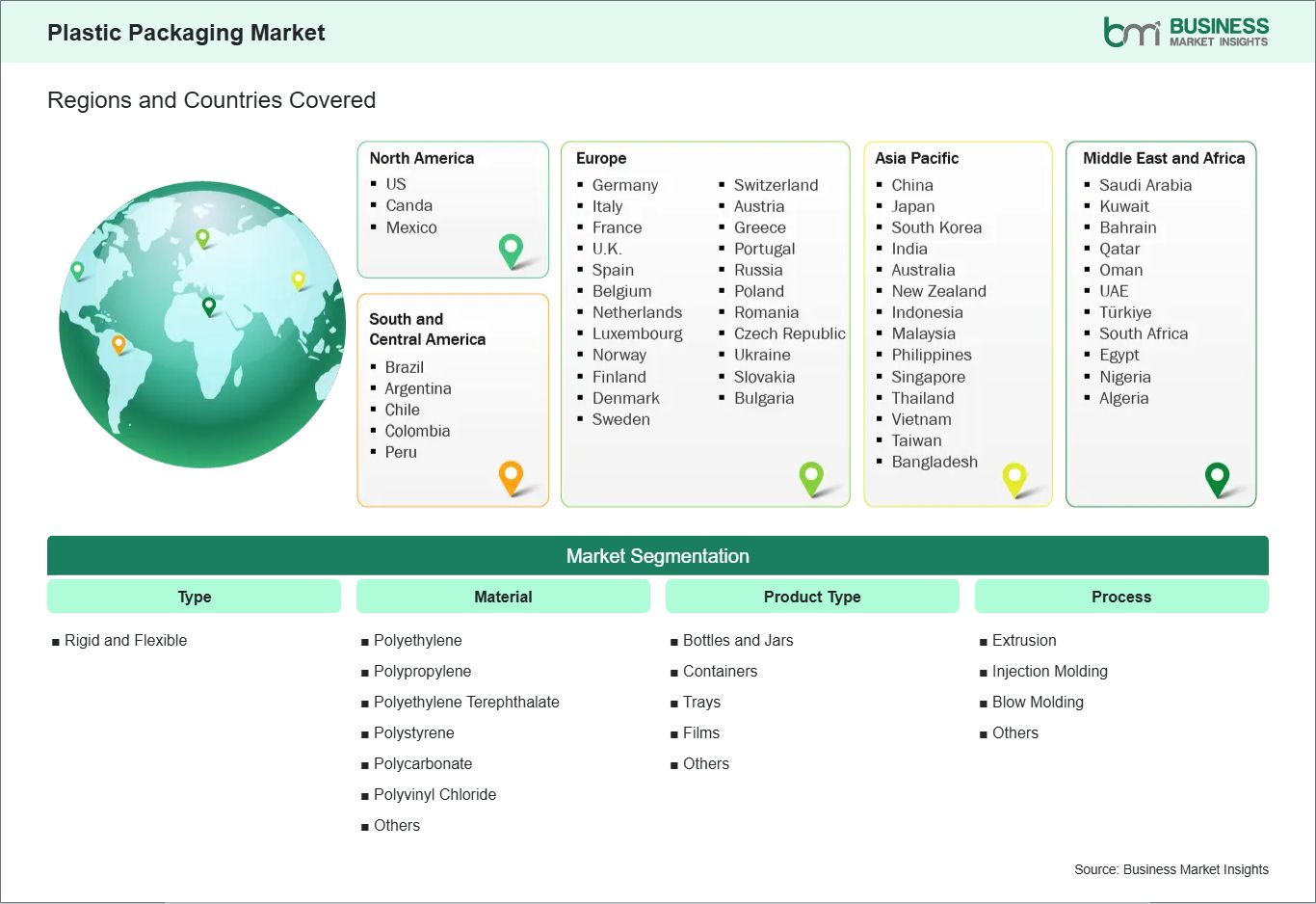

Plastic Packaging Market Segmentation Analysis:

Key segments that contributed to the derivation of the Plastic Packaging market analysis are type, material, product type, and process.

By Type, the market is segmented into Rigid and Flexible.

By Material, the market is segmented into Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene, Polycarbonate, Polyvinyl Chloride, and Others.

By Product Type, the market is segmented into Bottles and Jars, Containers, Trays, Films, and Others.

By Process, the market is segmented into Extrusion, Injection Molding, Blow Molding, and Others.

Plastic Packaging Market Drivers and Opportunities:

Urbanization, E-commerce, and Cost-Efficiency

The primary driver for the Plastic Packaging Market is the rapid growth of the global e-commerce and food delivery sectors, which demand lightweight, durable, and cost-effective materials for secure transit. As urban populations expand and lifestyles become increasingly fast-paced, there is a surging demand for "on-the-go" convenience, leading to a rise in single-serve portions and resealable formats. In the healthcare and pharmaceutical industries, plastic remains the preferred choice due to its superior barrier properties, ensuring the sterility and safety of life-saving medicines and medical devices. Furthermore, the inherent versatility of plastics, offering high impact resistance at a lower weight than glass or metal, allows brands to significantly reduce transportation costs and carbon emissions associated with shipping. This combination of functional performance and logistical economy ensures that plastic remains a foundational component of the global supply chain, particularly in emerging markets where organized retail is growing rapidly.

Circular Economy and Smart Packaging

A significant high-value opportunity lies in the transition toward a circular economy through the development of mono-material designs and advanced recycling technologies. With increasing regulatory pressure and consumer demand for sustainability, there is a massive market opening for packaging that utilizes high percentages of post-consumer recycled (PCR) content and bio-based polymers, such as PLA or PHA. Another major opportunity is the integration of Smart Packaging technologies, including QR codes, RFID tags, and freshness sensors. These digital features enhance supply chain transparency, provide anti-tamper security for pharmaceuticals, and allow brands to engage directly with consumers through interactive unboxing experiences. Manufacturers who innovate in "light-weighting", creating thinner yet more robust structures, can meet environmental mandates while lowering material usage. By bridging the gap between high-performance protection and eco-conscious design, companies can capture the rapidly growing segment of brands seeking to fulfill ambitious net-zero commitments without sacrificing product integrity.

Plastic Packaging Market Size and Share Analysis:

The Plastic Packaging market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type, material, product type, and process, offering insights into their contribution to overall market performance.

For instance, the Rigid segment holds a significant share of the market. This leadership is largely driven by the high demand for Bottles and Jars in the beverages and personal care industries. These products are frequently manufactured using the Blow Molding method, particularly for materials like Polyethylene Terephthalate (PET), which is favored for its clarity, strength, and recyclability. The market is also seeing a notable shift toward incorporating post-consumer recycled (PCR) resins in these rigid formats to meet rising sustainability targets.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Mondi Plc

ALPLA Group

Huhtamaki Oyj

Amcor Plc

Sonoco Products Company

Coveris

Constantia Flexibles

Greiner Packaging

Pactiv Evergreen Inc

Graham Packaging

Get more information on this report

Plastic Packaging Market Report Coverage and Deliverables:

The "Plastic Packaging Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Plastic Packaging market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Plastic Packaging market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Plastic Packaging market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Plastic Packaging market

Detailed company profiles, including SWOT analysis

Plastic Packaging Market Geographic Insights:

The geographical scope of the Plastic Packaging market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Plastic Packaging Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by the massive expansion of e-commerce and the food and beverage sector.

Growth is further bolstered by the rising demand for convenience-based packaging, such as pouches and sachets, which cater to the "single-serve" economy in emerging markets. Despite increasing environmental regulations and single-use plastic bans in countries like Japan and South Korea, the shift toward recycled PET (rPET) and mono-material flexible packaging ensures that Asia-Pacific remains the critical global hub for packaging innovation and supply chain resilience.

Get more information on this report

Plastic Packaging Market Research Report Guidance:

The report includes qualitative and quantitative data in the Plastic Packaging market across type, material, product type, process, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Plastic Packaging market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Plastic Packaging market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Plastic Packaging market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Plastic Packaging market segments by type, material, product type, process, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Plastic Packaging market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Plastic Packaging Market News and Key Development:

The Plastic Packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Plastic Packaging market are:

In October 2024, LyondellBasell (LYB) announced the acquisition of APK AG in Merseburg, Germany. APK will be fully integrated and continue as part of LYB. It is LYB’s ambition to further develop the company’s unique solvent-based technology for low-density polyethylene (LDPE) and build commercial plants in the future. This will enable LYB to produce new high-purity materials that can be used in applications like flexible packaging for personal care products, meeting the demands of customers and brand owners.

In April 2025, Amcor plc announced the successful completion of its all-stock combination with Berry Global. Through this combination, Amcor enhances its position as a global leader in consumer and healthcare packaging solutions with the unique material science and innovation capabilities required to revolutionize product development and meet customers’ and consumers’ sustainability aspirations.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Plastic Packaging Market

Mondi Plc

ALPLA Group

Huhtamaki Oyj

Amcor Plc

Sonoco Products Company

Coveris

Constantia Flexibles

Greiner Packaging

Pactiv Evergreen Inc

Graham Packaging

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Plastic Packaging Market?

The Plastic Packaging Market is valued at US$ 488.7 Billion in 2025, it is projected to reach US$ 653.5 Billion by 2033.

What is the CAGR for Plastic Packaging Market by (2026 - 2033)?

As per our report Plastic Packaging Market, the market size is valued at US$ 488.7 Billion in 2025, projecting it to reach US$ 653.5 Billion by 2033. This translates to a CAGR of approximately 3.70% during the forecast period.

What segments are covered in this report?

The Plastic Packaging Market report typically cover these key segments-

Type (Rigid and Flexible)

Material (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene, Polycarbonate, Polyvinyl Chloride, and Others)

Product Type (Bottles and Jars, Containers, Trays, Films, and Others)

Process (Extrusion, Injection Molding, Blow Molding, and Others)

What is the historic period, base year, and forecast period taken for Plastic Packaging Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Plastic Packaging Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Plastic Packaging Market?

The Plastic Packaging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Mondi Plc

ALPLA Group

Huhtamaki Oyj

Amcor Plc

Sonoco Products Company

Coveris

Constantia Flexibles

Greiner Packaging

Pactiv Evergreen Inc

Graham Packaging

Who should buy this report?

The Plastic Packaging Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Plastic Packaging Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Plastic Packaging Market

Get Free Sample For Plastic Packaging Market