01

Market Summery

Executive Summary and Global Market Analysis

Plastic injection molding machines are production systems that melt polymer materials and inject them into molds to manufacture repeatable plastic components at an industrial scale. Their role extends across mass manufacturing environments where precision, cycle consistency, material flexibility, and output efficiency shape equipment selection. The category includes electric, hydraulic, and hybrid configurations, each aligned with different processing needs, plant economics, and quality requirements. As molded parts remain central to consumer and industrial supply chains, this equipment base continues to anchor plastics conversion activity.

Procurement patterns are being shaped by the need for tighter tolerances, lower energy consumption, and improved manufacturing visibility. Processors are modernizing machine fleets to improve part consistency, reduce scrap, and support automated production cells that operate with less manual intervention. Demand from packaging, automotive, healthcare, and consumer goods manufacturing sustains equipment replacement and capacity expansion, particularly where production speed and repeatability determine competitiveness. This operating context supports a measured but durable market expansion profile.

Segment positioning reflects a clear shift in buyer priorities rather than a uniform transition across all machine classes. Electric systems are gaining stronger relevance in applications that require cleanliness, accuracy, and energy control, while hydraulic platforms remain important for heavy-duty molding and cost-sensitive operations. Hybrid machines occupy the middle ground by combining force capability with better process efficiency. Across end users, packaging and automotive applications remain especially influential because they combine high production volumes with strict dimensional and productivity requirements.

Technology development is moving beyond mechanical performance toward digitally managed manufacturing. Machine builders are embedding connectivity, process monitoring, predictive maintenance tools, and AI-assisted controls into molding platforms to improve uptime and process stability. At the same time, equipment is being adapted to handle recycled content, micro-molded parts, and more complex geometries without undermining throughput. This evolution is redefining machine value around flexibility, operating intelligence, and sustainability readiness.

Competitive conditions are becoming more structured around innovation depth, regional manufacturing reach, and the ability to support integrated production systems. Suppliers are strengthening their position through electric platform launches, partnerships, automation capabilities, and localized commercial strategies. The market therefore reflects a balance between established machine architectures and a newer emphasis on digital performance, efficient energy use, and application-specific engineering.

03

Segment Analysis

Plastic Injection Molding Machine Market Segmentation

The plastic injection molding machine market is segmented based on type and end user, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Type

- Electric: Preferred for precision molding, lower energy draw, and cleaner operating conditions.

- Hydraulic: Remains suitable for high-force applications and rugged industrial production settings.

- Hybrid: Combines control efficiency with force capability for balanced processing performance.

By End User

- Automotive: Relies on repeatable molding for interior, exterior, and under-the-hood plastic parts.

- Consumer Goods: Supports fast-cycle production for diverse product designs and frequent SKU changes.

- Packaging: Commands attention through high-volume output, short cycles, and thin-wall molding needs.

- Healthcare: Requires accuracy, cleanliness, and controlled processing for regulated molded components.

- Other End User: Covers specialized applications shaped by material behavior and product complexity.

04

Market Forces

Plastic Injection Molding Machine Market Drivers and Opportunities

Shift Toward Automated and Energy-Efficient Production Lines

Manufacturers are recalibrating capital spending as production economics place greater emphasis on energy use, repeatability, and labor efficiency. Injection molding operations increasingly require machines that can integrate with automation systems, monitor process variables continuously, and maintain stable output across long production runs. This need is accelerating replacement of older equipment with electric and hybrid platforms that offer better control, lower utility intensity, and stronger compatibility with digital factory environments. As end users seek tighter process discipline, machine selection is becoming a strategic operational decision rather than a purely mechanical one.

The effect on the market is visible in purchasing behavior across sectors where downtime, inconsistency, and waste directly affect margins. Automotive, healthcare, and packaging processors are prioritizing equipment that improves part quality while supporting connected manufacturing workflows. In regions with high labor costs or stricter sustainability expectations, the business case for automated and efficient molding systems becomes even stronger. This makes advanced machine platforms more relevant not only for new facilities, but also for modernization programs across mature manufacturing bases.

Smart Machines for Recycled Materials and Precision Applications

A notable opportunity is emerging at the intersection of digital control, material flexibility, and specialty molding. Processors increasingly need machines capable of managing recycled polymers, complex resin behavior, and application-specific tolerances without compromising cycle performance. Equipment innovation is responding through AI-supported controls, connected process monitoring, and machine designs suited to high-precision or micro-molding conditions. These developments expand the usefulness of advanced systems in packaging, medical products, and technical consumer goods where material variation and dimensional consistency must be tightly controlled.

Longer term, this opportunity extends into plant architectures built around data-rich and adaptive production cells. Machine suppliers that combine molding hardware with software intelligence, automation interfaces, and application engineering can address a wider range of production problems. That creates room for stronger penetration in industries moving toward circular material use, clean manufacturing, and higher product customization. In this setting, smart injection molding machines become not only conversion tools, but also operational platforms that improve resource utilization and process confidence.

05

Size and Share Analysis

Plastic Injection Molding Machine Market Size and Share Analysis

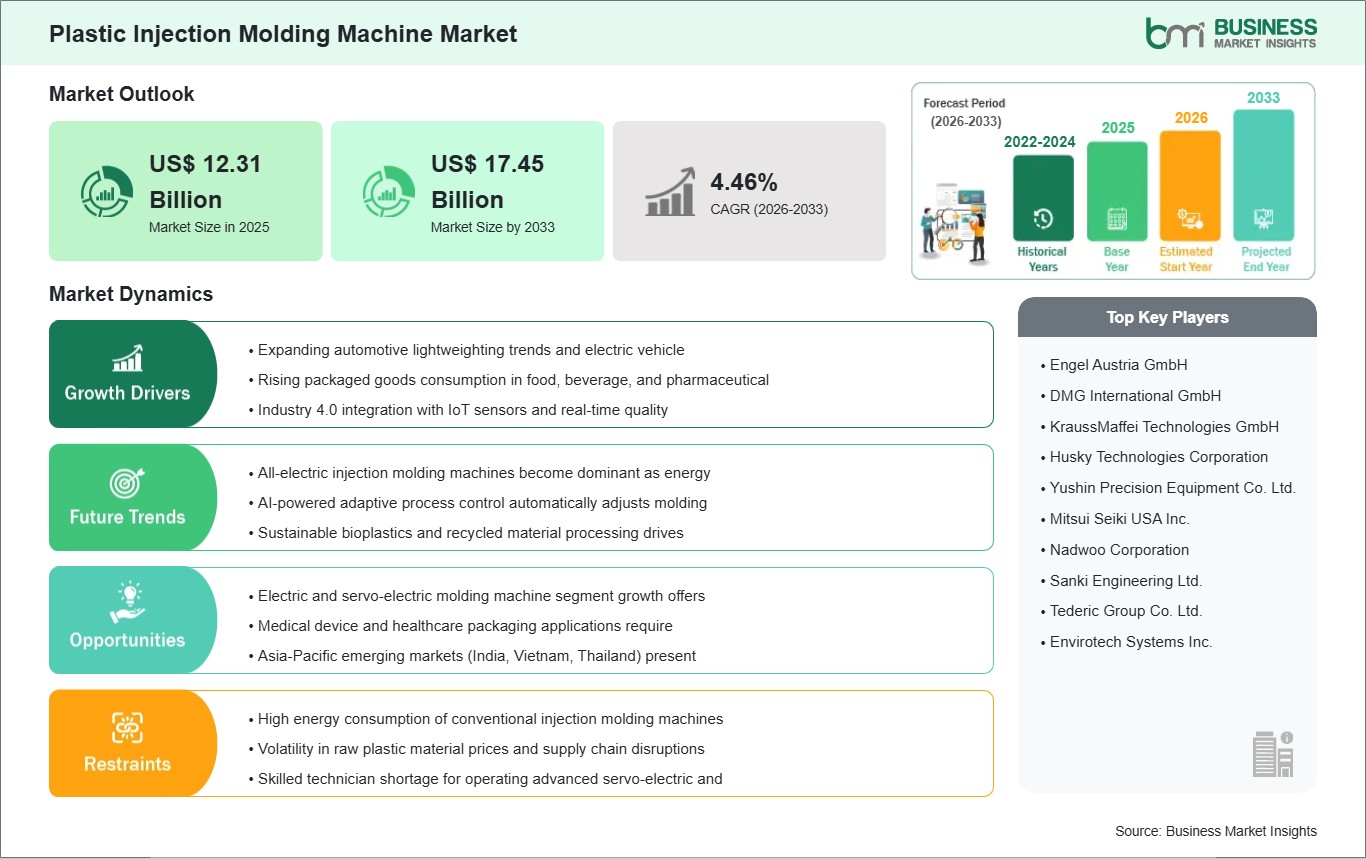

The plastic injection molding machine market is projected to grow from US$ 12.31 billion in 2025 to US$ 17.45 billion by 2033. The market is estimated to record a CAGR of 4.46% from 2026 to 2033.

This trajectory indicates a steady expansion pattern shaped by equipment modernization, replacement demand, and continued use of molded plastics across core manufacturing sectors. The industry is advancing through incremental technology improvement rather than abrupt structural change, which supports a stable competitive environment.

By type, electric machines hold the strongest strategic momentum because manufacturers increasingly value precision, lower energy consumption, and digital process compatibility. Hydraulic systems continue to retain a substantial position where higher force and broad processing flexibility remain important. Hybrid machines add relevance in operations seeking a practical balance between control performance and industrial robustness.

By end user, packaging remains highly influential due to its volume intensity and continuous production requirements. Automotive also represents a major demand center because molded components are embedded across interior, structural, and functional applications. Healthcare and consumer goods sustain equipment utilization through precision parts, regulated production settings, and rapid product turnover.

07

Report Coverage

Plastic Injection Molding Machine Market Report Coverage and Deliverables

The "Plastic Injection Molding Machine Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Plastic Injection Molding Machine Market Geographic Insights

The Plastic Injection Molding Machine market shows diverse regional adoption patterns influenced by manufacturing depth, automation maturity, resin processing needs, and industrial investment cycles. Global demand remains tied to the breadth of plastics processing across packaging, transport components, medical products, and consumer applications. Market progression differs by region because equipment upgrades depend on labor economics, energy efficiency priorities, and the pace of factory digitalization.

North America reflects a replacement-led environment in which processors emphasize precision production, connected machinery, and operational reliability. Equipment demand is shaped by high-value molding applications in automotive, healthcare, and technical parts manufacturing. Buyers in the region tend to prioritize systems that reduce waste, support automation, and maintain consistent performance across complex production programs.

Asia Pacific remains central to the industry due to its extensive manufacturing base, strong tooling ecosystems, and broad downstream consumption of molded plastic components. Regional demand benefits from packaging output, electronics-linked processing, automotive manufacturing, and cost-competitive production networks. The market also shows strong receptiveness to both large-capacity hydraulic systems and newer electric platforms as producers upgrade capabilities without slowing throughput.

Europe presents a more efficiency-oriented landscape shaped by sustainability goals, technical specialization, and advanced process engineering requirements. Machine selection in the region increasingly reflects interest in energy-conscious production, automation integration, and materials management compatible with circular manufacturing objectives. Outside the major established regions, emerging markets offer selective opportunities where industrialization, consumer packaging demand, and healthcare capacity expansion support new molding investments.

10

Industry Activity

Recent Developments

The plastic injection molding machine market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- In May 2026, At Plast 2026, ENGEL presents innovation as a dialogue with industry: not only technologies, but an integrated ecosystem of solutions, digital assistants, AI-based systems and automation designed to deliver value, efficiency and quality across manufacturing processes. For injection moulders, this means solutions that help stabilise production, reduce scrap, make better use of available resources and improve cost efficiency across a broad range of applications.

- In March 2026, In March 2026, ARBURG introduced its new electric ALLROUNDER TREND machine series, designed for standard molding applications with faster setup times, lower operating costs, and simplified maintenance. The launch reflects growing demand for energy-efficient and automation-ready molding equipment.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations