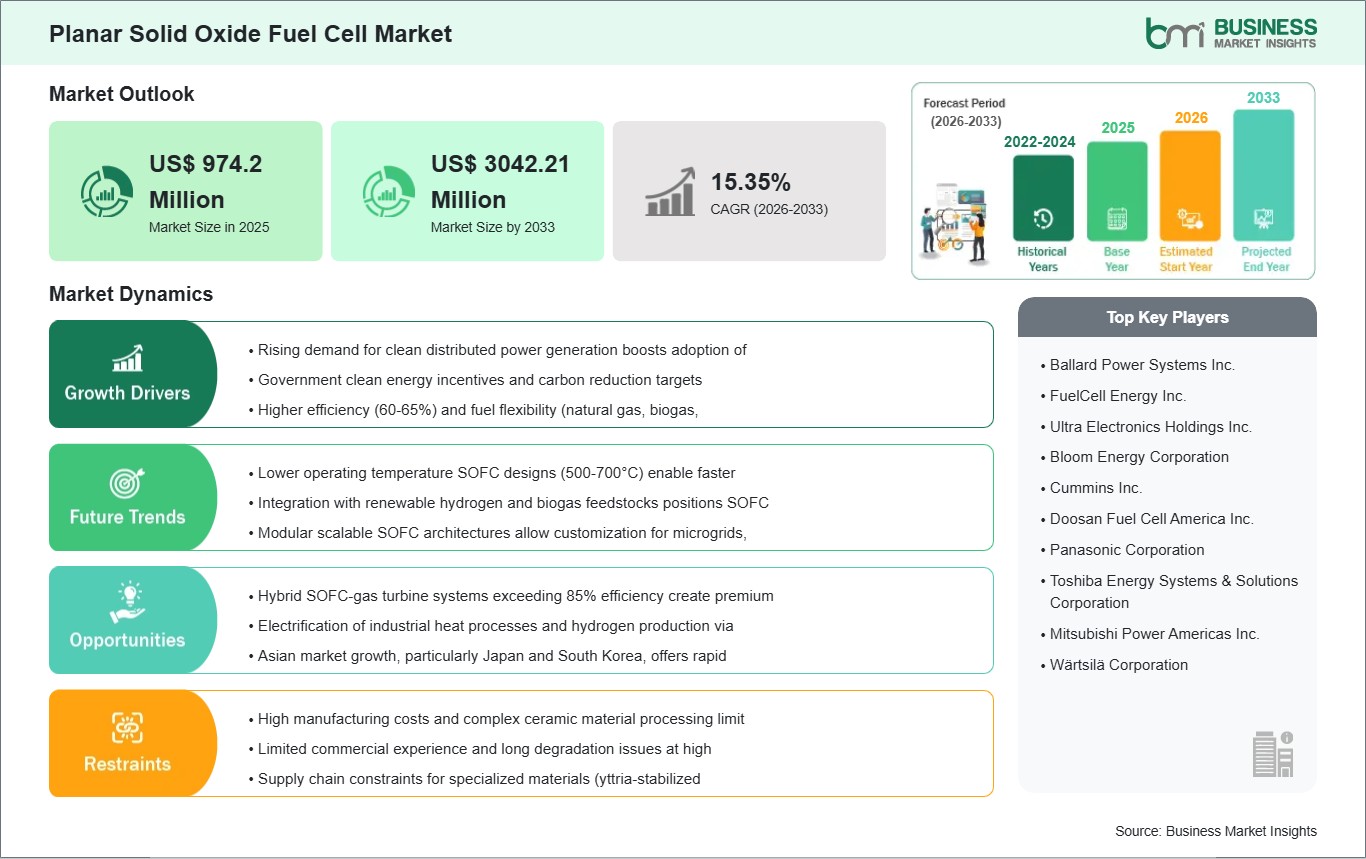

The planar solid oxide fuel cell market size is expected to reach US$ 3.04 billion by 2033 from US$ 0.97 billion in 2025. The market is estimated to record a CAGR of 15.35% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Planar solid oxide fuel cells are high-temperature electrochemical devices that convert hydrogen, natural gas, biogas, and related fuels into electricity through flat-cell stack architectures. Their configuration supports shorter current pathways, higher power density, and compact system design, making them suitable for distributed energy applications where efficiency, fuel flexibility, and thermal integration are commercially important. Planar structures also align well with stack-based manufacturing approaches, although sealing and thermal durability remain central engineering considerations. These attributes position the market within the broader transition toward cleaner on-site and grid-supportive power systems.

Commercial attention is strengthening as energy users seek low-emission generation platforms capable of stable output under variable grid conditions. The technology appeals to facilities that require continuous electricity with the added benefit of usable heat, particularly in settings where resilience, fuel optionality, and lower local emissions influence procurement decisions. Rising interest in hydrogen-ready systems and natural-gas-compatible transitional technologies also expands the relevance of planar SOFC platforms across industrial, commercial, and infrastructure-led projects.

Segment expansion reflects the breadth of deployment pathways rather than a single end-market concentration. Lower power bands remain relevant for compact and modular systems, while mid-range and higher-output configurations support commercial buildings, energy hubs, and distributed power assets. Stationary applications currently define the market’s practical center of gravity because they best match the technology’s operating profile, thermal recovery potential, and stack integration requirements. End-use demand is especially shaped by combined heat and power installations and power generation environments that value continuous, efficient operation.

The technology landscape is evolving through improvements in intermediate-temperature operation, stack durability, sealing methods, electrode materials, and manufacturing readiness. Developers are working to reduce thermal stress and extend operating life while preserving efficiency and lowering system complexity. Progress in anode-supported designs, fuel processing integration, and thermal management is steadily improving commercial viability for planar formats. These refinements are particularly relevant for applications requiring repeatable performance over long operating cycles.

The competitive environment remains innovation-led, with emphasis on licensing models, system integration, manufacturing scale-up, and regional commercialization partnerships. Market positioning increasingly depends on stack longevity, cost structure, deployment flexibility, and the ability to serve both power generation and cogeneration use cases. Strategic moves in Europe and Asia, along with larger project announcements tied to on-site power demand, indicate a market shifting from technical validation toward more structured commercial rollout.

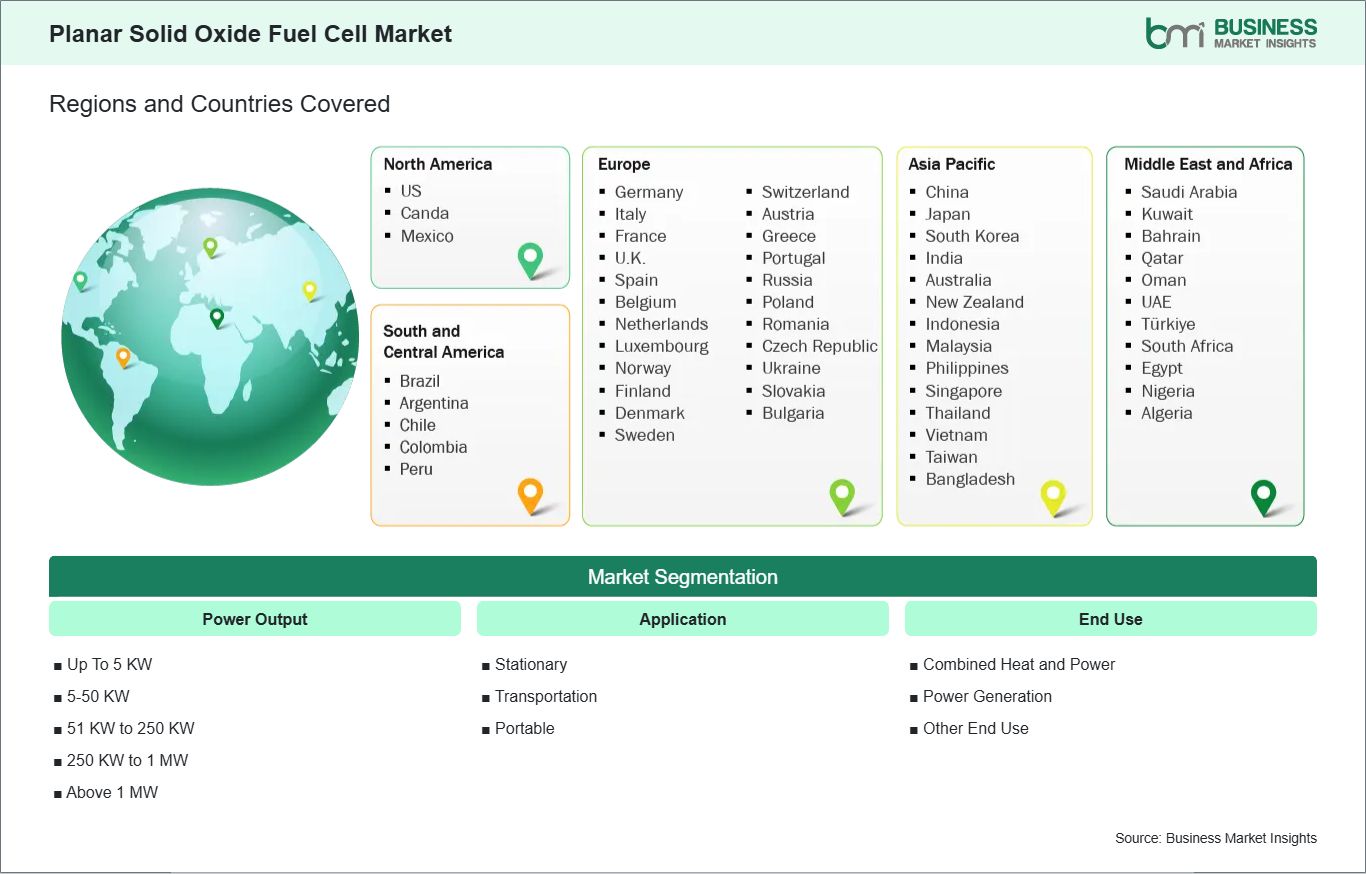

The planar solid oxide fuel cell market is segmented based on power output, application, end use, highlighting distinct operational priorities and evolving deployment strategies across various end uses.

By Power Output

Up To 5 KW: Best suited to compact systems requiring localized and modular electricity supply.

5-50 KW: Supports small commercial and distributed installations with flexible deployment economics.

51 KW to 250 KW: Addresses medium-scale sites balancing efficiency, footprint, and operational continuity.

250 KW to 1 MW: Fits institutional and industrial energy systems seeking dependable on-site generation.

Above 1 MW: Serves large facilities requiring scalable stack architecture and integrated thermal utilization.

By Application

Stationary: Aligns strongly with continuous-duty operations and site-level energy resilience needs.

Transportation: Gains relevance where fuel flexibility and high-efficiency auxiliary propulsion systems matter.

Portable: Remains niche, centered on remote applications needing compact off-grid power capability.

By End Use

Combined Heat and Power: Captures value through simultaneous electricity generation and thermal recovery.

Power Generation: Appeals to users prioritizing reliable output and reduced grid dependence.

Other End Use: Includes specialized deployments shaped by operational conditions and system design needs.

Planar Solid Oxide Fuel Cell Market Drivers and Opportunities:

Expansion of High-Efficiency Distributed Power Systems

Energy users are reassessing conventional power arrangements as grid strain, energy security concerns, and decarbonization targets reshape procurement decisions. Planar SOFC systems address this shift through high electrical efficiency, fuel flexibility, and compatibility with on-site generation models. Their flat-stack architecture allows compact deployment while supporting cogeneration, which improves total energy utilization in buildings and industrial facilities. This combination makes the technology increasingly relevant for installations that value operational continuity and thermal integration over intermittent generation profiles.

The market impact extends beyond equipment selection into broader energy system design. Facilities planning resilient infrastructure are placing greater emphasis on technologies that can maintain output, use existing fuel networks, and transition toward lower-carbon fuels over time. In that context, planar SOFC systems fit applications where efficient baseload power and heat recovery strengthen commercial feasibility. Their relevance is reinforced by partnerships targeting grid-independent on-site power across industrial and commercial settings in Europe and by large deployment models emerging in Asia.

Intermediate-Temperature and Durable Stack Innovation

A major opportunity lies in technology refinement that improves durability while lowering operational strain. Recent development paths focus on intermediate-temperature performance, advanced electrolytes, improved electrodes, enhanced sealing, and stronger thermal management. These advances can reduce degradation pressure, simplify materials requirements, and improve manufacturability without discarding the efficiency benefits associated with solid oxide platforms. Planar systems stand to benefit directly because their commercial progress depends heavily on stack life, seal integrity, and repeatable long-duration performance.

Future expansion is likely to come from applications where durability and scalable manufacturing matter as much as efficiency. As system developers improve stack lifetime and production readiness, the addressable market broadens across stationary power, combined heat and power, and large on-site installations linked to data, logistics, and advanced manufacturing infrastructure. Platform launches oriented toward durability and lower manufacturing cost signal a path toward wider commercial acceptance. This creates room for planar SOFC suppliers to compete not only on technical output, but also on lifecycle economics and deployment confidence.

Planar Solid Oxide Fuel Cell Market Size and Share Analysis:

The planar solid oxide fuel cell market is projected to grow from US$ 0.97 billion in 2025 to US$ 3.04 billion by 2033. The market is estimated to record a CAGR of 15.35% from 2026 to 2033.

This trajectory indicates a market moving from early commercial scaling toward broader deployment across distributed energy systems. Expansion is supported by demand for efficient on-site generation, improved stack engineering, and stronger alignment with low-emission power strategies.

By power output, the market is led by mid-range and higher-capacity systems that align with commercial and industrial operating requirements. These bands are better positioned to capture the advantages of planar stack architecture, especially where users seek efficient electricity production with practical system footprint and integration potential. Lower-output categories retain relevance in modular and localized use cases, but larger systems hold stronger strategic weight in commercial adoption.

By application, stationary use commands the largest share of market activity due to its compatibility with continuous operation and heat recovery. This application category best reflects the strengths of planar SOFC systems, particularly in distributed generation and combined heat and power environments. Transportation and portable uses remain important development tracks, though their commercial maturity is comparatively narrower.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Ballard Power Systems Inc.

FuelCell Energy Inc.

Ultra Electronics Holdings Inc.

Bloom Energy Corporation

Cummins Inc.

Doosan Fuel Cell America Inc.

Panasonic Corporation

Toshiba Energy Systems & Solutions Corporation

Mitsubishi Power Americas Inc.

Wärtsilä Corporation

Get more information on this report

Planar Solid Oxide Fuel Cell Market Report Coverage and Deliverables:

The "Planar Solid Oxide Fuel Cell Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Planar Solid Oxide Fuel Cell market shows diverse regional adoption patterns influenced by energy security priorities, fuel infrastructure maturity, decarbonization pathways, and industrial policy direction. Across global markets, commercialization is advancing where end users value efficient on-site power, thermal recovery, and lower-emission alternatives to conventional distributed generation. Regional progress also reflects differences in hydrogen strategy, natural gas availability, manufacturing readiness, and project financing structures.

North America maintains a strong commercial foundation because the region combines technology development capability with demand for resilient distributed energy systems. Market activity is shaped by data-intensive facilities, commercial campuses, and infrastructure operators seeking continuous on-site generation with lower emissions and improved power quality. The region also benefits from established fuel cell expertise and demonstration pathways that support movement from pilot deployments toward larger operating projects.

Asia Pacific presents a different momentum profile, with expansion linked closely to industrial scale, infrastructure-led energy planning, and national interest in advanced fuel cell systems. South Korea remains especially relevant due to manufacturing progress and utility-linked project development, while broader regional adoption is supported by interest in compact, efficient power solutions for urban and industrial settings. The region’s ability to connect commercialization with large project execution gives it strategic importance in the market’s next phase.

Europe advances through policy-backed decarbonization, industrial collaboration, and rising interest in grid-independent on-site power for commercial and industrial users. The region is also becoming more prominent in partnership-based deployment models that combine energy services with solid oxide platforms designed for scalable rollout. Beyond these major centers, emerging markets in the Middle East, Africa, and parts of Latin America may create selective opportunities where reliable distributed generation, fuel flexibility, and heat-integrated systems match local infrastructure constraints.

Get more information on this report

Planar Solid Oxide Fuel Cell Market Research Report Guidance:

The Planar Solid Oxide Fuel Cell market report includes qualitative and quantitative data in the planar solid oxide fuel cell market across power output, application, end use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the planar solid oxide fuel cell market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the planar solid oxide fuel cell market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the planar solid oxide fuel cell market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover planar solid oxide fuel cell market segments by power output, application, end use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the planar solid oxide fuel cell market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Planar Solid Oxide Fuel Cell Market News and Key Development:

The planar solid oxide fuel cell market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In April 2026, Ceres today launched Ceres® Endura™, its flagship solid oxide stack platform designed to meet the surging demand for resilient, efficient, onsite power for data centres and other energy intensive applications. From a single production facility, Ceres’ partners can unlock access to both the power and hydrogen markets from a shared platform. Fuel flexibility allows for operation on natural gas today, while supporting hydrogen and other low carbon fuels tomorrow.

In July 2025, Ceres and Doosan Fuel Cell announced that mass market production of fuel cell stacks using Ceres' solid oxide technology has commenced. Doosan Fuel Cell will manufacture the stacks and fuel cell power systems at its dedicated factory in South Korea with the ability to produce a combined generational capacity of 50MW of electrical power each year.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Energy Agency (IEA)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Planar Solid Oxide Fuel Cell Market

Ballard Power Systems Inc.

FuelCell Energy Inc.

Ultra Electronics Holdings Inc.

Bloom Energy Corporation

Cummins Inc.

Doosan Fuel Cell America Inc.

Panasonic Corporation

Toshiba Energy Systems & Solutions Corporation

Mitsubishi Power Americas Inc.

Wärtsilä Corporation

Frequently Asked Questions

How big is the Planar Solid Oxide Fuel Cell Market?

The Planar Solid Oxide Fuel Cell Market is valued at US$ 974.2 Million in 2025, it is projected to reach US$ 3042.21 Million by 2033.

What is the CAGR for Planar Solid Oxide Fuel Cell Market by (2026 - 2033)?

As per our report Planar Solid Oxide Fuel Cell Market, the market size is valued at US$ 974.2 Million in 2025, projecting it to reach US$ 3042.21 Million by 2033. This translates to a CAGR of approximately 15.35% during the forecast period.

What segments are covered in this report?

The Planar Solid Oxide Fuel Cell Market report typically cover these key segments-

Power Output (Up To 5 KW, 5-50 KW, 51 KW to 250 KW, 250 KW to 1 MW, Above 1 MW)

Application (Stationary, Transportation, and Portable)

End Use (Combined Heat and Power, Power Generation, Other End Use)

What is the historic period, base year, and forecast period taken for Planar Solid Oxide Fuel Cell Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Planar Solid Oxide Fuel Cell Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Planar Solid Oxide Fuel Cell Market?

The Planar Solid Oxide Fuel Cell Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Ballard Power Systems Inc.

FuelCell Energy Inc.

Ultra Electronics Holdings Inc.

Bloom Energy Corporation

Cummins Inc.

Doosan Fuel Cell America Inc.

Panasonic Corporation

Toshiba Energy Systems & Solutions Corporation

Mitsubishi Power Americas Inc.

Wärtsilä Corporation

Who should buy this report?

The Planar Solid Oxide Fuel Cell Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Planar Solid Oxide Fuel Cell Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Planar Solid Oxide Fuel Cell Market

Get Free Sample For Planar Solid Oxide Fuel Cell Market