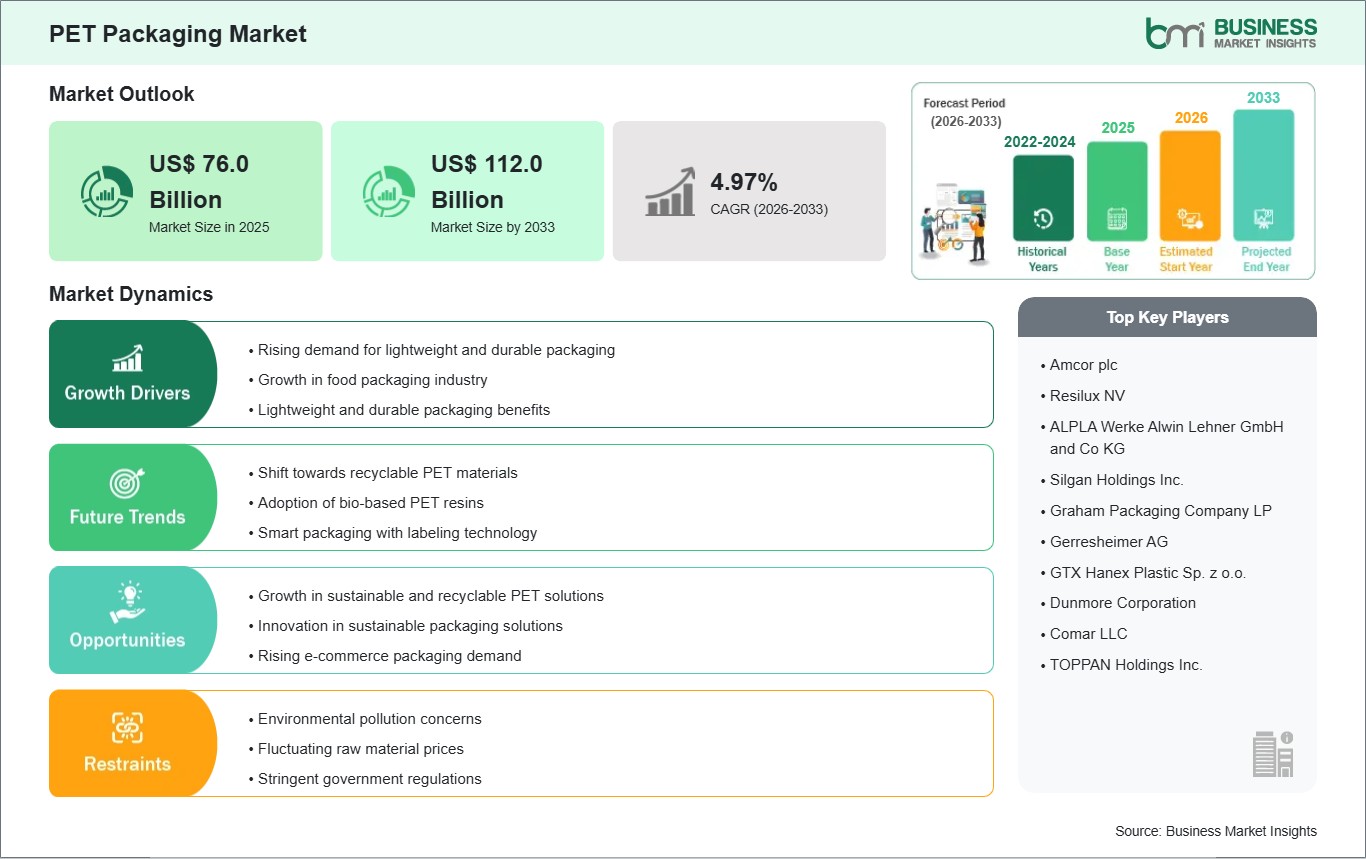

The PET Packaging Market size is expected to reach US$ 112. billion by 2033 from US$ 76. billion in 2025. The market is estimated to record a CAGR of 4.97% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The PET packaging industry is witnessing tremendous growth, mainly attributed to the increasing demand for lightweight, strong, and eco-friendly packaging materials for food, beverages, personal care, and pharmaceutical applications. Polyethylene terephthalate (PET) is a highly transparent, strong, and barrier-resistant material, which can be recycled, making it a preferred choice for packaging applications like bottles, containers, films, and trays.

The increasing demand for convenient, portable, and longer shelf-life packages is also propelling the industry, especially for single-serve, ready-to-consume packages. Sustainability is another major factor that is significantly impacting the PET industry. The world is moving towards a more circular economy, and initiatives are being taken to reduce plastic waste, especially from PET materials. The adoption of recycled PET (rPET) and bio-based PET is not only a compliance to regional regulations but also a competitive advantage for companies to showcase their commitment to the environment.

In addition, lightweighting initiatives are enabling cost efficiency, reduced transportation emissions, and minimized raw material usage without compromising packaging performance. Technological innovation is central to PET packaging growth. Advanced barrier coatings, multilayer structures, and enhanced thermoforming capabilities are expanding the applicability of PET in high-demand sectors, including carbonated beverages, dairy, and pharmaceuticals. Manufacturers are also exploring PET hybrid solutions, combining PET with other materials to improve barrier performance, mechanical strength, and aesthetic appeal. Competitive dynamics are characterized by global resin producers, packaging converters, and brand-driven partnerships.

Companies are investing in capacity expansions, collaborative R&D programs, and localized production to meet regional demand efficiently. Regulatory compliance, product quality, and sustainability credentials are critical differentiators in a market where consumer and industrial expectations continue to evolve rapidly. The PET packaging market is defined by the intersection of high-performance material requirements, sustainability imperatives, and innovation in design and functionality. Suppliers capable of delivering recyclable, lightweight, and multifunctional PET solutions are well-positioned to capture growth in both mature and emerging markets.

PET Packaging Market - Strategic Insights:

Get more information on this report

PET Packaging Market Segmentation Analysis:

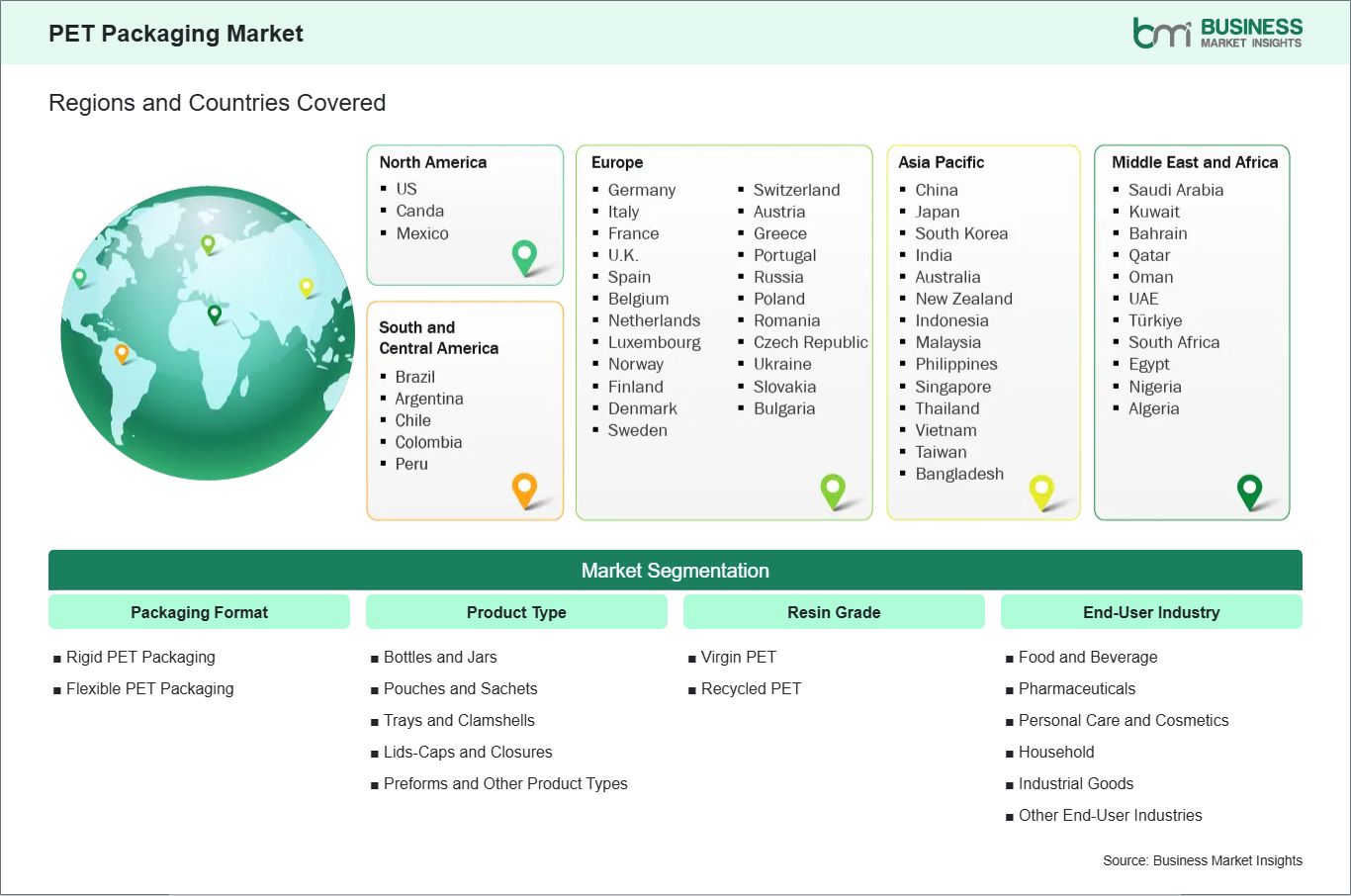

Key segments that contributed to the derivation of the PET packaging market analysis are packaging format, product type, resin grade, and end‑user industry.

By Packaging Format, the PET packaging market is segmented into rigid PET packaging and flexible PET packaging. The rigid PET packaging segment dominated the market in 2025.

Based on Product Type, the PET packaging market is classified into bottles and jars, pouches and sachets, trays and clamshells, lids‑caps and closures, and preforms and other product types. The bottles and jars segment dominated the market in 2025.

On the Basis of Resin Grade, the PET packaging market is categorized into virgin PET and recycled PET. The virgin PET segment dominated the market in 2025.

In Terms of End‑User Industry, the PET packaging market is segmented into food and beverage, pharmaceuticals, personal care and cosmetics, household, industrial goods, and other end‑user industries. The food and beverage segment dominated the market in 2025.

PET Packaging Market Drivers and Opportunities:

Rising demand for lightweight and durable packaging

The need for PET packaging is rising due to the need for a lightweight and strong packaging solution. It has the advantage of being transparent and having impact resistance and barrier properties. It can be used for beverage packaging, foodstuffs, personal care products, and household goods. Its ability to preserve the quality of the product while reducing weight is driving its adoption in different industries.

Manufacturers are using PET packaging to increase convenience and safety. Its ability to increase the durability of products during transportation and extend the shelf life of products while minimizing spoilage is driving its adoption. Its transparency also helps in making products more visible and appealing to customers. It has become a widely accepted solution due to its ability to provide convenience.

Innovation in the different types of packaging formats and designs of PET is also increasing the scope of the market. This is because the molding and barrier technology of PET are allowing the development of customized designs and sizes, thereby protecting the packaged products from environmental factors like oxygen and moisture.

Growth in sustainable and recyclable PET solutions

Sustainability is bringing about major changes in the PET packaging industry. The emphasis is on the use of recyclable, reusable, and biobased PET materials, which can help reduce the impact of waste on the environment. The innovations in the PET industry can help reduce waste, support the circular economy, and achieve the global sustainability agenda. The use of PET packaging materials that can be recycled multiple times or made from renewable resources is gaining popularity among brands and customers.

The eco-friendly innovations in the PET industry also include lightweighting and multi-layered barrier solutions, which can help reduce the use of materials while maintaining the quality of the product. The innovations in the PET industry are ensuring that companies are meeting the regulations and corporate sustainability agendas while maintaining the quality of the product.

In this context, ongoing research and development activities are further enhancing the scope of the adoption of sustainable PET solutions. This is because the latest technology and resin formulations are capable of providing improved performance, shelf life, and safety, thus contributing to the environment-friendly cause. With the ongoing focus on the environment-friendly cause in different sectors, sustainable PET solutions are likely to propel the growth of the market.

PET Packaging Market Size and Share Analysis:

The PET packaging market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within packaging format, product type, resin grade, and end‑user industry, offering insights into their contribution to overall market performance.

By Packaging Format, the rigid PET packaging subsegment dominated the market in 2025, driven by high demand for bottles and jars offering clarity, shelf impact, and barrier performance.

Based on Product Type, the bottles and jars subsegment dominated the market in 2025, supported by its extensive use in beverages, edible oils, and other liquids.

On the Basis of Resin Grade, the virgin PET subsegment dominated the market in 2025, owing to its stable melt consistency and suitability for high‑speed bottling lines.

In Terms of End‑User Industry, the food and beverage subsegment dominated the market in 2025, driven by rising consumption of bottled water, carbonated drinks, and dairy products.

PET Packaging Market Report Coverage and Deliverables:

The "PET Packaging Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

PET Packaging Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

PET Packaging Market trends, as well as drivers, restraints, and opportunities

PET Packaging Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the PET Packaging Market

Detailed company profiles, including SWOT analysis

PET Packaging Market Geographic Insights:

The geographical scope of the PET Packaging Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional-level dynamics in the PET packaging market reveal distinct demand patterns shaped by industrial maturity, regulatory frameworks, and consumer preferences. North America is the dominant market, driven by advanced packaging infrastructure, large-scale beverage and food industries, and strong adoption of sustainable PET solutions. The

United States and Canada lead in the use of rPET and lightweight PET bottles for carbonated beverages, dairy products, and personal care items. Regulatory support for recycling initiatives and brand-driven sustainability goals reinforce demand for environmentally friendly packaging solutions.

Europe represents a mature and sustainability-focused market, with Germany, France, and Italy emphasizing high adoption of recycled PET, bio-based PET, and eco-friendly packaging innovations. Strict EU regulations on single-use plastics, recycling mandates, and packaging waste reduction drive investments in circular PET solutions, while consumers increasingly favor recyclable and high-quality packaging.

Asia Pacific is a rapidly growing region, led by China, India, and Japan, due to increasing urbanization, rising disposable incomes, and growing consumption of beverages and convenience foods. High-volume packaging demand is met through both domestic and global PET suppliers. Sustainability initiatives are gaining momentum, particularly in developed APAC markets, prompting adoption of rPET and lightweight PET solutions.

Middle East & Africa is an emerging market where rising urbanization, beverage consumption, and retail modernization drive PET packaging adoption. Demand is largely concentrated in urban centers and premium beverage segments, with sustainability and recyclability gradually influencing product development. South & Central America shows steady growth, primarily in Brazil and Mexico, driven by expanding beverage and food industries. Cost-efficiency is a critical factor, but rising awareness of recyclability and environmental compliance is prompting gradual adoption of rPET and innovative PET packaging solutions.

Get more information on this report

PET Packaging Market Research Report Guidance:

The report includes qualitative and quantitative data in the PET Packaging Market packaging format, product type, resin grade, end‑user industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the PET Packaging Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the PET Packaging Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the PET Packaging Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover PET Packaging Market segments across packaging format, product type, resin grade, end‑user industry, and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 12 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 13 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 14 provides detailed profiles of the major companies operating in the PET Packaging Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 15, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

PET Packaging Market News and Key Development:

The PET Packaging Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the PET packaging market are:

In April 2024, Amcor plc announced that it launched a first‑ever 1‑liter polyethylene terephthalate (PET) carbonated soft drink bottle made from 100% post‑consumer recycled (PCR) material, aimed at helping beverage brands meet sustainability targets and regulatory requirements for recycled content in PET packaging.

In December 2024, Berry Global Group, Inc. collaborated with VOID Technologies to launch a high‑performance, sustainable polyethylene film for pet food packaging applications a recyclable film designed to boost strength and puncture resistance while enabling mono‑material recycling readiness in flexible PET‑related packaging structures.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - PET Packaging Market

Amcor plc

Resilux NV

ALPLA Werke Alwin Lehner GmbH and Co KG

Silgan Holdings Inc.

Graham Packaging Company LP

Gerresheimer AG

GTX Hanex Plastic Sp. z o.o.

Dunmore Corporation

Comar LLC

TOPPAN Holdings Inc.

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the PET Packaging Market?

The PET Packaging Market is valued at US$ 76.0 Billion in 2025, it is projected to reach US$ 112.0 Billion by 2033.

What is the CAGR for PET Packaging Market by (2026 - 2033)?

As per our report PET Packaging Market, the market size is valued at US$ 76.0 Billion in 2025, projecting it to reach US$ 112.0 Billion by 2033. This translates to a CAGR of approximately 4.97% during the forecast period.

What segments are covered in this report?

The PET Packaging Market report typically cover these key segments-

Packaging Format (Rigid PET Packaging, Flexible PET Packaging)

Product Type (Bottles and Jars, Pouches and Sachets, Trays and Clamshells, Lids-Caps and Closures, Preforms and Other Product Types)

Resin Grade (Virgin PET, Recycled PET)

End-User Industry (Food and Beverage, Pharmaceuticals, Personal Care and Cosmetics, Household, Industrial Goods, Other End-User Industries)

What is the historic period, base year, and forecast period taken for PET Packaging Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the PET Packaging Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in PET Packaging Market?

The PET Packaging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The PET Packaging Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the PET Packaging Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For PET Packaging Market

Get Free Sample For PET Packaging Market