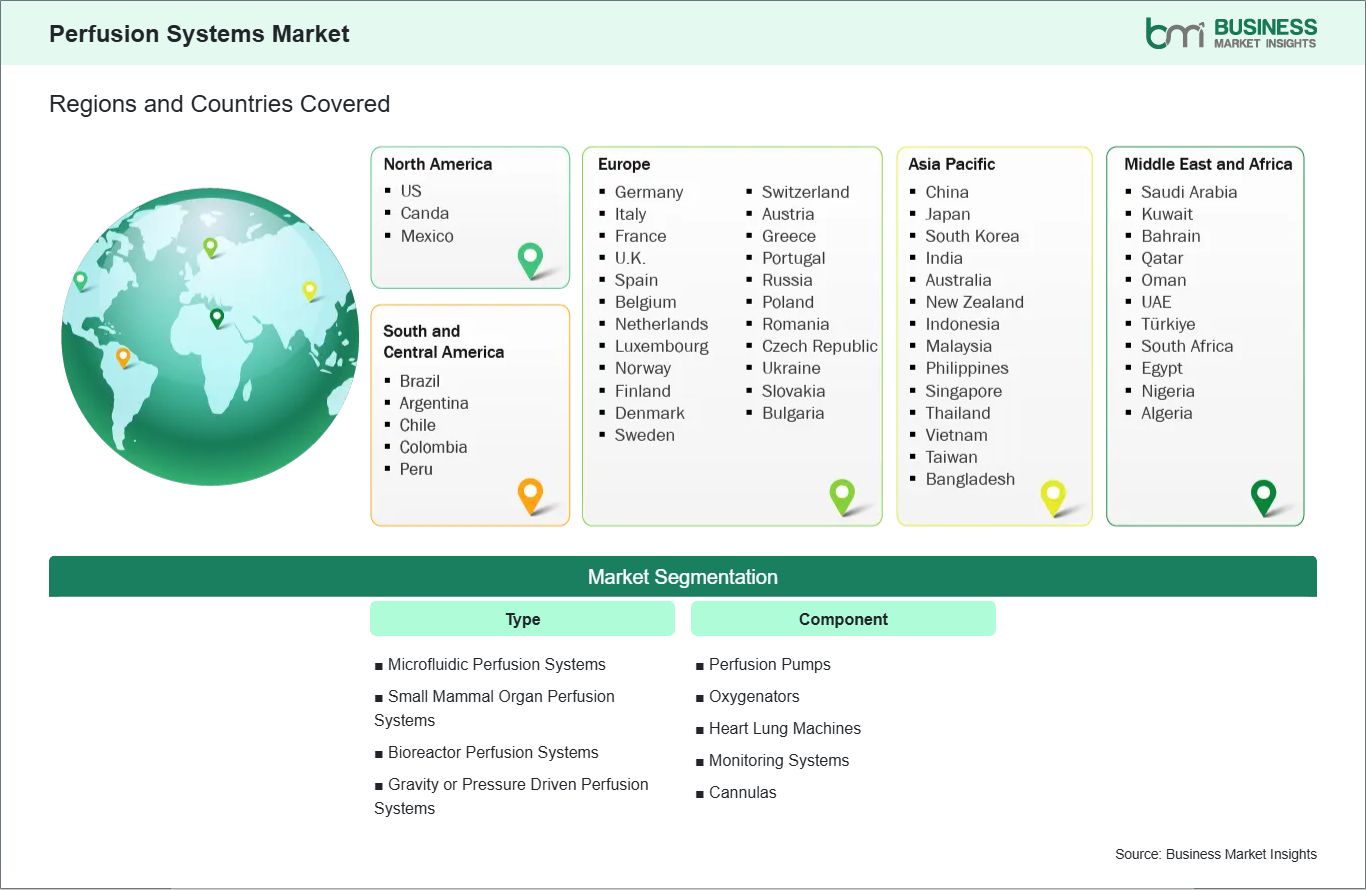

Type (Microfluidic Perfusion Systems, Small Mammal Organ Perfusion Systems, Bioreactor Perfusion Systems, and Gravity or Pressure Driven Perfusion Systems)

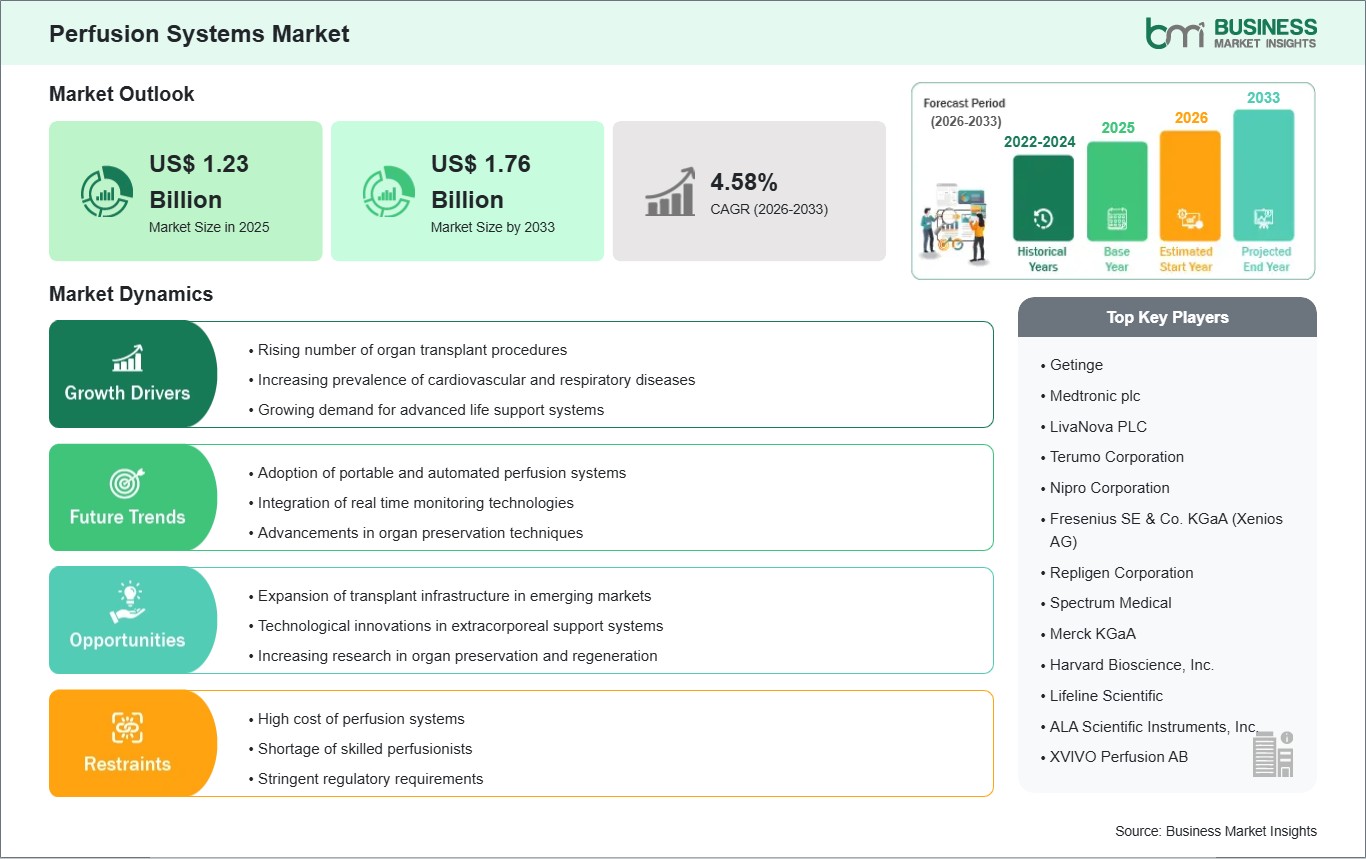

The Perfusion Systems Market size is expected to reach US$ 1.76 billion by 2033 from US$ 1.23 billion in 2025. The market is estimated to record a CAGR of 4.58% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Perfusion systems are advanced medical devices engineered to maintain continuous circulation of blood or physiological substitutes through organs or tissues, thereby preserving viability outside the body or during surgical procedures. These systems provide significant strategic value by enabling complex cardiac repairs and increasing the availability of viable donor organs in hospitals, specialized transplant centers, and biopharmaceutical laboratories. Market growth is primarily driven by the global increase in cardiovascular diseases (CVDs), the rapid rise in organ transplant procedures, and the growing incidence of respiratory failure necessitating extracorporeal membrane oxygenation (ECMO) support. Additionally, the adoption of normothermic perfusion technology is markedly enhancing graft survival rates by reducing ischemic injury and facilitating real-time metabolic assessment before transplantation.

However, several challenges can restrain market growth: extremely high capital and per-procedure costs often limit the availability of advanced perfusion systems to top-tier urban medical centers, particularly in emerging economies. A critical shortage of certified clinical perfusionists, the specialized staff required to operate these systems, creates an operational bottleneck for many hospitals. Additionally, the industry faces constraints due to stringent regulatory pathways for Class III medical devices and the complex logistical requirements of maintaining a warm organ transport chain.

Despite these challenges, the market presents substantial opportunities, including the integration of Artificial Intelligence (AI) for predictive organ viability analytics and the rapid deployment of portable, transport-ready perfusion modules. The growth of perfusion-based bioprocessing in pharmaceutical research and development, along with the advancement of bio-compatible, heparin-coated consumables, is anticipated to drive long-term market expansion.

Perfusion Systems Market - Strategic Insights:

Get more information on this report

Perfusion Systems Market Segmentation Analysis:

Key segments that contributed to the derivation of the Perfusion Systems market analysis are type and component.

By Type, the market is segmented into Microfluidic Perfusion Systems, Small‑Mammal Organ Perfusion Systems, Bioreactor Perfusion Systems, and Gravity or Pressure‑Driven Perfusion Systems.

By Component, the market is divided into Perfusion Pumps, Oxygenators, Heart‑Lung Machines, Monitoring Systems, and Cannulas.

Perfusion Systems Market Drivers and Opportunities:

Rising Transplant Volumes and the Integration of AI-Driven Assessment

A critical global shortage of transplantable organs, combined with the increasing incidence of end-stage organ failure, serves as the primary driver for the Perfusion Systems Market. The growing demand for organ transplantation is a foundational catalyst, as healthcare systems seek to expand the donor pool by utilizing marginal or extended criteria organs that require machine support to remain viable. This trend is further accelerated by the adoption of normothermic machine perfusion (NMP), which maintains organs in a functional state and enables real-time metabolic testing. NMP significantly reduces organ discard rates and improves post-transplant patient outcomes.

Technological advancements, particularly the integration of artificial intelligence (AI) and machine learning, represent a significant market driver. AI algorithms now analyze perfusion parameters to predict organ viability with greater accuracy than manual assessment. Additionally, the rising prevalence of cardiovascular diseases (CVDs) sustains high demand for cardiopulmonary bypass systems, which continue to generate the largest share of market revenue. Collectively, these factors, the ongoing transplant crisis, innovations in organ preservation, and AI-driven precision, support a robust growth trajectory for the global perfusion systems market.

Portable Ex Vivo Platforms and Xenotransplantation Research

A significant opportunity exists in the integration of perfusion systems with portable, mobile organ care platforms. Next-generation devices are being developed as clinics-on-wheels, enabling organs to be perfused and monitored during extended ground or air transport. This advancement effectively eliminates geographic barriers between donors and recipients. Additionally, the development of automated cell perfusion for biomanufacturing represents a major growth area. As demand for biologics and cell therapies increases, there is a substantial market for bioreactor-integrated perfusion systems that deliver continuous nutrient supply and waste removal for large-scale cell cultures.

The expansion of xenotransplantation and bio-artificial organ research presents a distinct opportunity, as manufacturers are developing specialized platforms to assess the viability of genetically modified animal organs and 3D-bioprinted tissues. In addition to hardware advancements, the emergence of dual-temperature hybrid consoles, which can alternate between hypothermic and normothermic modes, provides high-volume transplant centers with opportunities to optimize capital equipment utilization. Manufacturers prioritizing single-use, disposable perfusion circuits and those advancing closed-loop auto-pilot perfusion control are positioned to lead the most innovative and high-margin segments of the global perfusion systems market.

Perfusion Systems Market Size and Share Analysis:

The Perfusion Systems market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within type and component, offering insights into their contribution to overall market performance.

Based on type, the Cardiopulmonary Perfusion Systems and Bioreactor Perfusion Systems subsegment holds a significant market presence, reflecting the dual demand from clinical surgery and pharmaceutical R&D. Cardiopulmonary Systems are indispensable for the Cardiac Surgery vertical, maintaining a dominant market share due to the high volume of bypass and valve replacement procedures requiring extracorporeal circulation. A notable trend is the surge in the Microfluidic Perfusion Systems and Small-Mammal Organ Perfusion Systems subsegments, which are registering higher interest in drug discovery and personalized medicine. These micro-scale systems are becoming essential for Organ-on-a-Chip research, allowing pharmaceutical companies to simulate human physiological responses with high accuracy, thereby reducing the reliance on traditional animal testing and accelerating the clinical trial pipeline.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Getinge

Medtronic plc

LivaNova PLC

Terumo Corporation

Nipro Corporation

Fresenius SE & Co. KGaA (Xenios AG)

Repligen Corporation

Spectrum Medical

Merck KGaA

Harvard Bioscience, Inc.

Lifeline Scientific

ALA Scientific Instruments, Inc.

XVIVO Perfusion AB

Get more information on this report

Perfusion Systems Market Report Coverage and Deliverables:

The "Perfusion Systems Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Perfusion Systems market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Perfusion Systems market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Perfusion Systems market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Perfusion Systems market

Detailed company profiles, including SWOT analysis

Perfusion Systems Market Geographic Insights:

The geographical scope of the Perfusion Systems market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America continues to lead the market, supported by a high volume of organ transplant procedures and advanced cardiovascular surgical centers in the United States and Canada. Europe represents a mature market, characterized by a strong focus on normothermic machine perfusion (NMP) research and the presence of well-established organ procurement organizations. The Asia Pacific region is the fastest-growing market, propelled by substantial investments in healthcare infrastructure and an increasing prevalence of heart and lung diseases in China and India.

The Asia-Pacific Perfusion Systems Market is segmented into China, Japan, South Korea, India, Australia, and the rest of the region. China serves as a primary growth driver, with increased domestic production of heart-lung machines and a significant rise in certified transplant centers. In India, market expansion is supported by the growth of private specialty hospitals and increased cardiac healthcare expenditure. Japan maintains a leading position in high-precision perfusion technology, particularly for pediatric and geriatric populations. Australia is experiencing a gradual transition toward mobile and portable extracorporeal membrane systems.

Get more information on this report

Perfusion Systems Market Research Report Guidance:

The report includes qualitative and quantitative data in the Perfusion Systems market across type, component, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Perfusion Systems market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Perfusion Systems market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Perfusion Systems market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Perfusion Systems market segments by type, component, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Perfusion Systems market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Perfusion Systems Market News and Key Development:

The Perfusion Systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Perfusion Systems market are:

In January 2026, Bridge to Life™ received FDA De Novo clearance for its VitaSmart™ Hypothermic Oxygenated Perfusion (HOPE) System, the first device cleared in the U.S. for hypothermic oxygenated perfusion of donor livers. The system supports Donation after Brain Death (DBD) and Circulatory Death (DCD) donors, offering improved organ utilization, workflow efficiency, and enhanced patient outcomes.

In August 2025, LivaNova launched its Essenz Perfusion System in China, expanding access to its next-generation heart-lung machine and patient monitoring platform. The system, designed in collaboration with over 300 perfusionists worldwide, aims to enhance patient safety, workflow efficiency, and clinical outcomes during cardiopulmonary bypass procedures.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Frequently Asked Questions

How big is the Perfusion Systems Market?

The Perfusion Systems Market is valued at US$ 1.23 Billion in 2025, it is projected to reach US$ 1.76 Billion by 2033.

What is the CAGR for Perfusion Systems Market by (2026 - 2033)?

As per our report Perfusion Systems Market, the market size is valued at US$ 1.23 Billion in 2025, projecting it to reach US$ 1.76 Billion by 2033. This translates to a CAGR of approximately 4.58% during the forecast period.

What segments are covered in this report?

The Perfusion Systems Market report typically cover these key segments-

Type (Microfluidic Perfusion Systems, Small Mammal Organ Perfusion Systems, Bioreactor Perfusion Systems, and Gravity or Pressure Driven Perfusion Systems)

What is the historic period, base year, and forecast period taken for Perfusion Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Perfusion Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Perfusion Systems Market?

The Perfusion Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Getinge

Medtronic plc

LivaNova PLC

Terumo Corporation

Nipro Corporation

Fresenius SE & Co. KGaA (Xenios AG)

Repligen Corporation

Spectrum Medical

Merck KGaA

Harvard Bioscience, Inc.

Lifeline Scientific

ALA Scientific Instruments, Inc.

XVIVO Perfusion AB

Who should buy this report?

The Perfusion Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Perfusion Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Perfusion Systems Market

Get Free Sample For Perfusion Systems Market