01

Market Summery

Executive Summary and Global Market Analysis

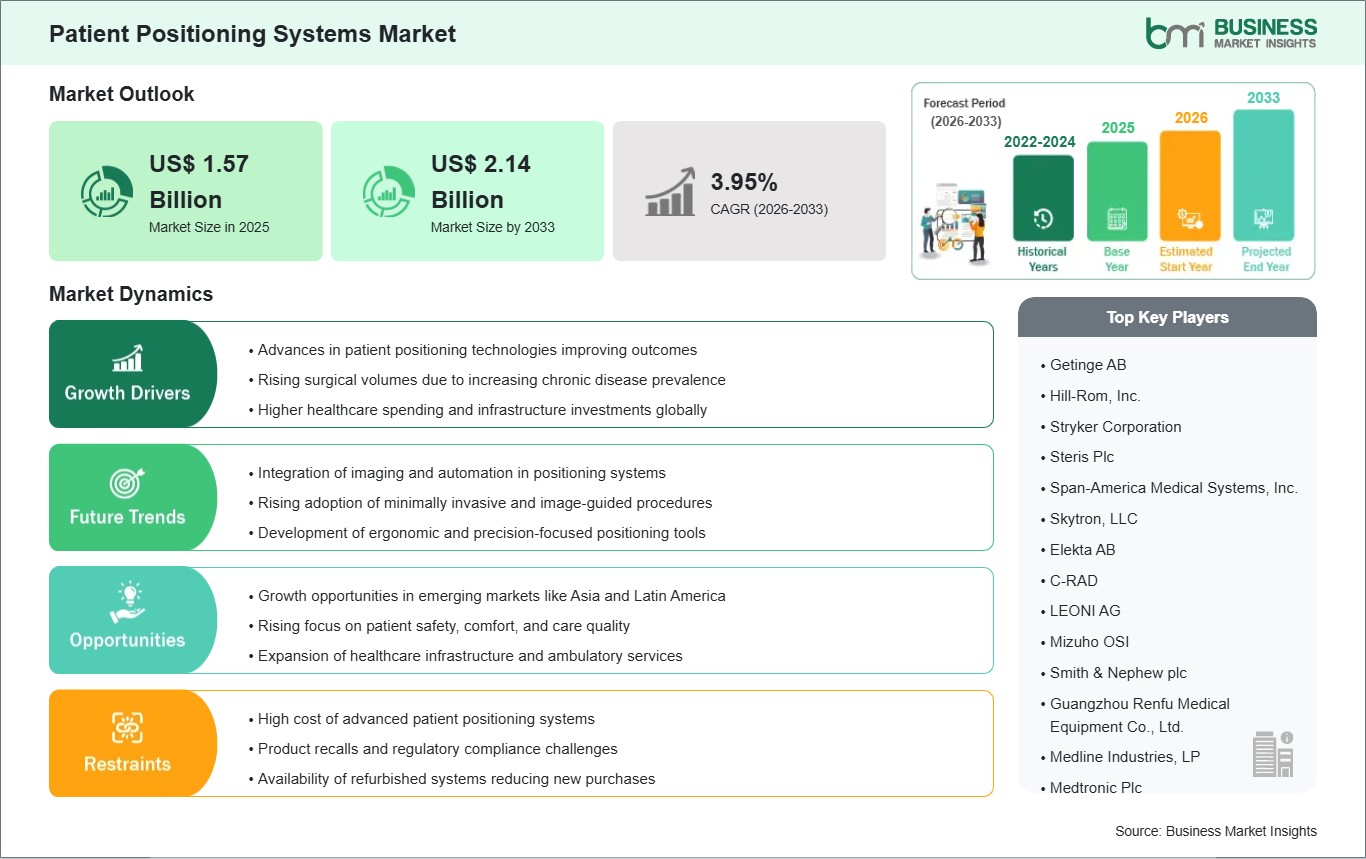

Patient positioning systems are specialized medical devices and accessories that support, stabilize, and immobilize patients in specific anatomical postures during clinical procedures. These systems provide significant strategic value by enhancing procedural safety and improving clinical outcomes in hospitals, diagnostic centers, and ambulatory surgical centers (ASCs). Market growth is primarily driven by the global increase in minimally invasive and robotic-assisted surgeries, the rapid rise in diagnostic imaging volumes for chronic disease detection, and the growing demand for ergonomic designs that reduce physical strain on healthcare staff. Additionally, the transition toward Ambulatory Surgical Centers (ASCs) is increasing the demand for compact, multi-functional positioning equipment that enables rapid patient turnover while maintaining safety.

Several challenges may limit market growth. High capital expenditure and ongoing maintenance costs for motorized and integrated systems can be prohibitive for smaller facilities and public hospitals. Extended product replacement cycles for heavy-duty surgical tables often delay the adoption of new technological innovations. Furthermore, the industry is constrained by stringent regulatory compliance and safety standards, which can result in prolonged product development timelines and potential recalls in cases of mechanical or software failures.

Despite these challenges, the market presents substantial opportunities due to increasing healthcare investments in emerging economies such as China, India, and Brazil, as well as the rapid adoption of AI-integrated intelligent imaging tables. The growth of portable positioning aids for home-care settings and the development of 3D-printed, patient-specific immobilization devices are also anticipated to drive long-term market expansion.

03

Segment Analysis

Patient Positioning Systems Market Segmentation

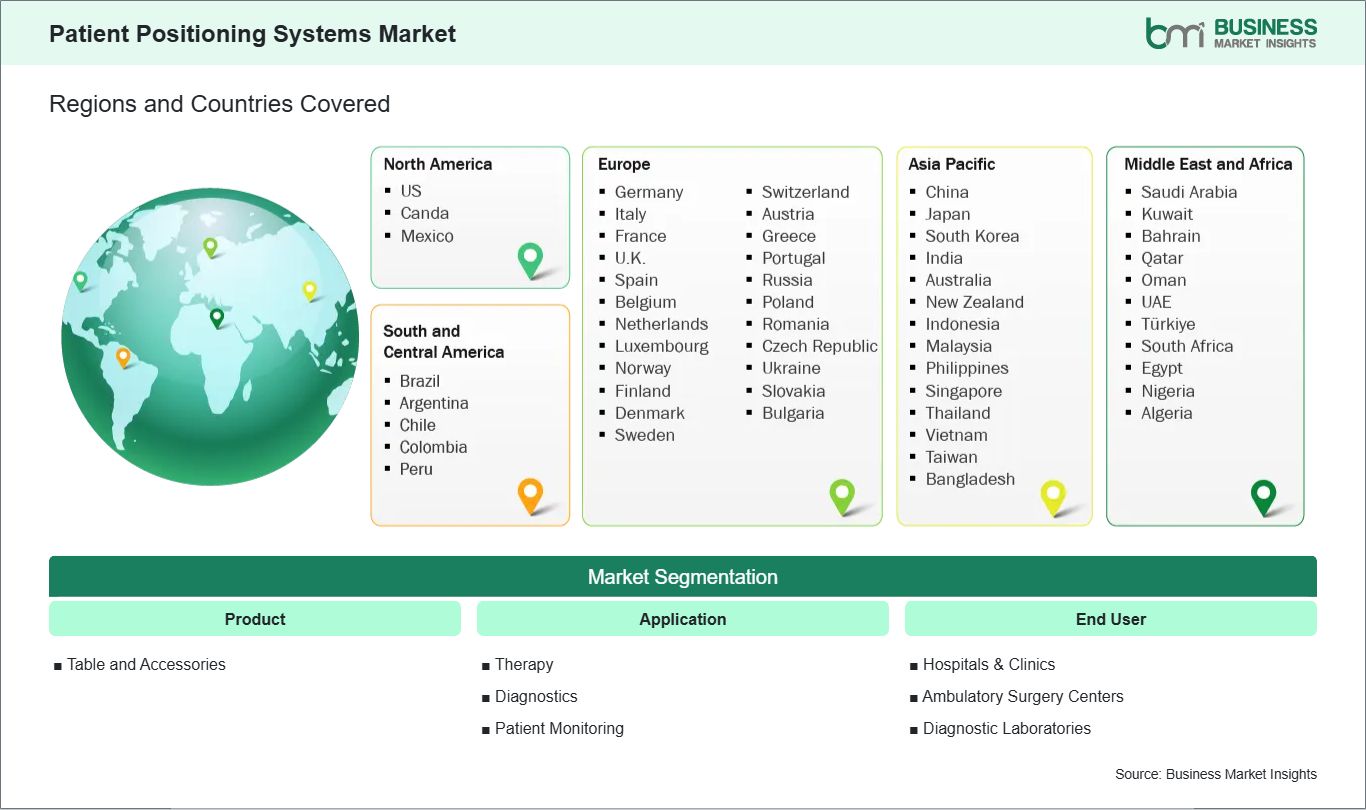

Key segments that contributed to the derivation of the Patient Positioning Systems market analysis are product, application, and end user.

- By Product, the market is segmented into Table and Accessories.

- By Application, the market is divided into Therapy, Diagnostics, and Patient Monitoring.

- By End User, the market is categorized into Hospitals & Clinics, Ambulatory Surgery Centers, and Diagnostic Laboratories.

04

Market Forces

Patient Positioning Systems Market Drivers and Opportunities

>Rising Surgical Complexity and the Digitalization of Procedural Workflows

The primary driver of the patient positioning systems market is the global increase in complex surgical and diagnostic procedures due to an aging population. The rising prevalence of chronic diseases, especially cancer and orthopedic conditions, also contributes significantly, as these cases require precise and consistent positioning for treatments such as radiation therapy and joint replacements. Additionally, the adoption of minimally invasive surgery and robotic assistance is accelerating demand for advanced systems, since these techniques require stable patient positioning and specific anatomical access. As a result, healthcare facilities are replacing manual tables with motorized, modular systems. Technological advancements, particularly the integration of AI-powered imaging, are further driving growth. New systems use 3D sensors to automate positioning for X-ray and CT scans, which reduces setup times and limits radiation exposure.

Furthermore, the expansion of healthcare infrastructure and increased government funding, especially in Asia-Pacific and the Middle East, is creating significant new demand for high-end operating room equipment. These factors, combined with demographic changes, surgical innovation, and AI-driven automation, are supporting steady and advanced growth in the global patient positioning systems market.

Smart Smart-Room Connectivity and Outpatient Agility

A significant opportunity exists in the integration of Patient Positioning Systems with Internet of Things (IoT) technologies and Smart Operating Room (OR) ecosystems. Next-generation tables are being engineered to interface directly with surgical navigation software, automatically adjusting tilt and height according to the surgeon`s real-time digital plan. This automation reduces cognitive load and enhances procedural safety. Additionally, the development of agile positioning equipment for Ambulatory Surgical Centers (ASCs) represents a major growth area. As surgical volumes shift to lower-cost outpatient settings, there is increasing demand for lightweight, easy-to-clean, and multifunctional tables capable of seamless transition from surgery to recovery.

The expansion of single-use, hygienic positioning accessories also presents a significant market opportunity, as hospitals increasingly prioritize disposable pads and wedges to comply with stricter infection control standards and reduce sterilization costs. In addition to traditional materials, the emergence of pressure-sensing smart cushions introduces a novel advancement. These cushions incorporate sensors that notify staff of localized pressure increases, thereby enabling real-time prevention of hospital-acquired pressure ulcers. Manufacturers specializing in ergonomic one-touch automation and those developing carbon-fiber radiolucent platforms for hybrid imaging and surgical suites are well positioned to lead the Patient Positioning Systems market.

05

Size and Share Analysis

Patient Positioning Systems Market Size and Share Analysis

The Patient Positioning Systems market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product, application, and end user, offering insights into their contribution to overall market performance.

Based on product, the Tables and Accessories subsegment demonstrates a significant market presence, serving as the primary source of capital and consumable investments within the sector. Surgical and radiolucent imaging tables are essential in operating rooms, driven by increasing demand for equipment compatible with real-time X-ray, CT, and MRI guidance. Additionally, the Accessories subsegment, particularly radiotherapy immobilization products and single-use disposable pads, is experiencing notable growth. These accessories are increasingly vital for cancer therapy and infection control, as they offer high-speed thermal surface tracking and antimicrobial protection necessary for precise radiation delivery and minimization of cross-contamination risk.

07

Report Coverage

Patient Positioning Systems Market Report Coverage and Deliverables

The "Patient Positioning Systems Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Patient Positioning Systems market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Patient Positioning Systems market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Patient Positioning Systems market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Patient Positioning Systems market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Patient Positioning Systems Market Geographic Insights

The geographical scope of the Patient Positioning Systems market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America continues to lead the market, supported by an advanced network of hospitals and ambulatory surgical centers (ASCs) that prioritize ergonomic, motorized systems to improve surgical throughput. Europe holds a strong second position, with a focus on Safe Patient Handling regulations that promote the adoption of lateral transfer and prone positioning devices to safeguard healthcare workers. The Asia Pacific region is experiencing the most rapid growth, driven by substantial government investments in hospital infrastructure in China and India, as well as an increasing number of complex neurosurgical and orthopedic procedures.

The Asia-Pacific Patient Positioning Systems Market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China serves as a primary growth driver, shifting from basic manual tables to advanced radiolucent carbon-fiber systems designed for hybrid operating rooms. India is experiencing increased demand for specialized positioning accessories in private specialty hospitals, supporting the expansion of its medical tourism sector. In Japan, the market demonstrates strong demand for bariatric and geriatric-friendly positioning solutions tailored to its super-aging population. South Korea is at the forefront of integrating robotic-assisted positioning devices.

10

Industry Activity

Recent Developments

The Patient Positioning Systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Patient Positioning Systems market are:

- In January 2026, Baxter launched the Dynamo Series smart stretcher in the U.S., designed to enhance patient safety, prevent falls, and simplify positioning for a range of procedures. The device integrates advanced technologies to improve patient comfort and workflow efficiency, strengthening Baxter`s presence in the patient positioning system market.

- In April 2025, Arjo launched the Maxi Move 5 patient floor lift, featuring motion-assist and powered dynamic positioning systems to improve patient safety, comfort, and caregiver efficiency. The device strengthens Arjo`s global leadership in patient handling and expands its presence across hospitals and long-term care facilities.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations