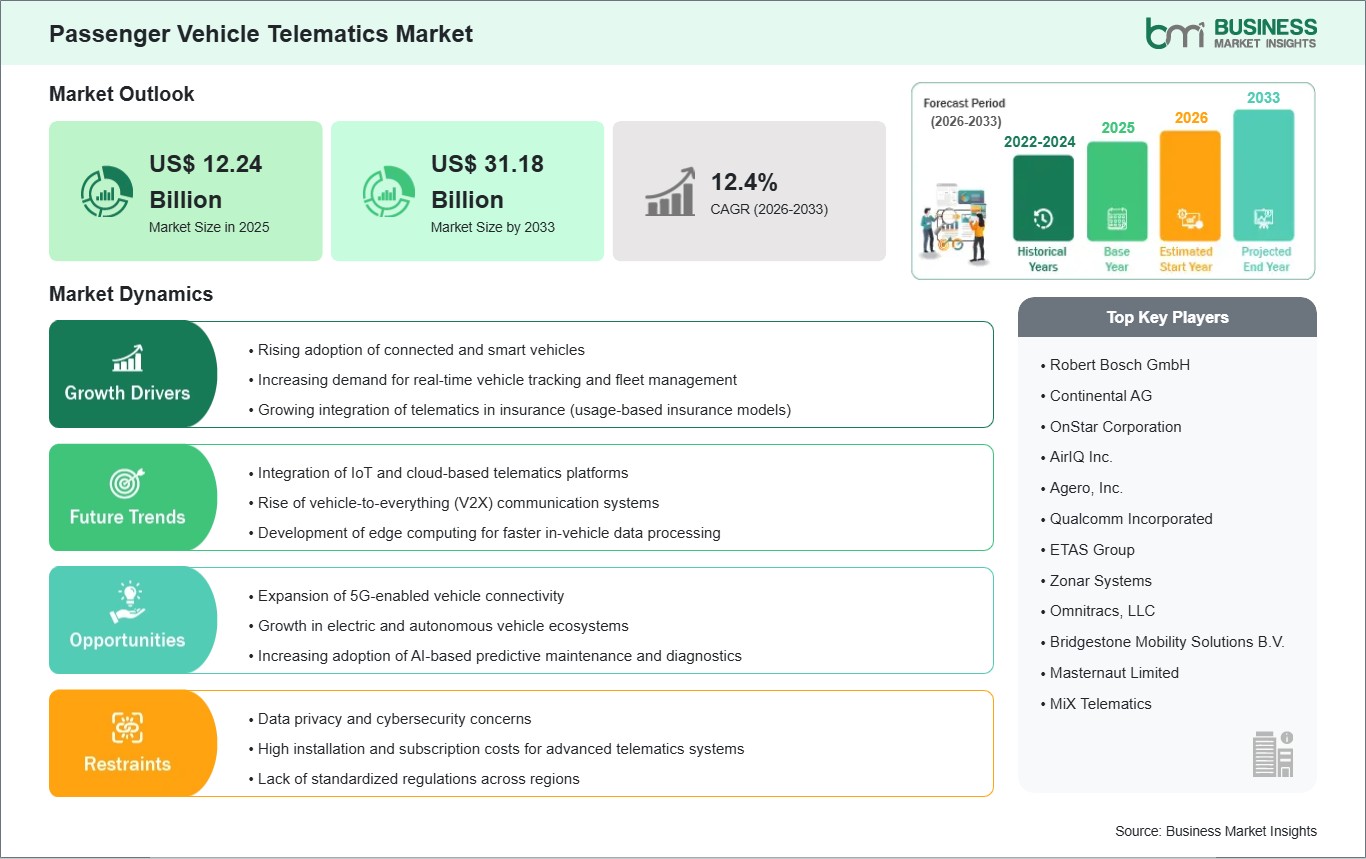

The passenger vehicle telematics market size is expected to reach US$ 31.18 billion by 2033 from US$ 12.24 billion in 2025. The market is estimated to record a CAGR of 12.4% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Passenger vehicle telematics refers to connected systems that collect, transmit, and interpret vehicle and driver data to support navigation, safety, diagnostics, remote assistance, and digital service delivery within passenger cars. These systems combine communication hardware, embedded software, and service platforms to create continuous links between vehicles, users, and mobility ecosystems.

Market momentum is supported by stronger consumer preference for connected driving experiences, wider integration of remote diagnostics, and tighter alignment between automotive electronics and software-led vehicle design. Automakers are positioning telematics as a standard capability rather than a premium add-on, particularly where service continuity, safety functionality, and data-enabled personalization influence purchasing decisions.

Within segmentation, hardware remains foundational because telematics control units, sensors, and communication modules establish operational reliability inside the vehicle. Software shapes service differentiation through interface design, analytics, and data orchestration, while services sustain long-term value through subscriptions, maintenance support, and platform management. Application breadth also strengthens the market, spanning fleet visibility, occupant protection, insurer-linked monitoring, and in-car digital experiences.

Technology architecture is evolving from isolated embedded functions toward hybrid models that combine onboard intelligence with smartphone connectivity and cloud-based processing. This transition improves flexibility across user profiles and vehicle classes while enabling feature updates, richer infotainment environments, and stronger coordination between safety alerts, usage data, and remote controls.

The competitive environment reflects convergence across automotive, electronics, software, and connectivity providers seeking tighter control over recurring service revenue and customer retention. Product strategies increasingly emphasize integrated platforms, cybersecurity readiness, scalable data handling, and seamless user experiences, making execution capability as important as component innovation in this sector.

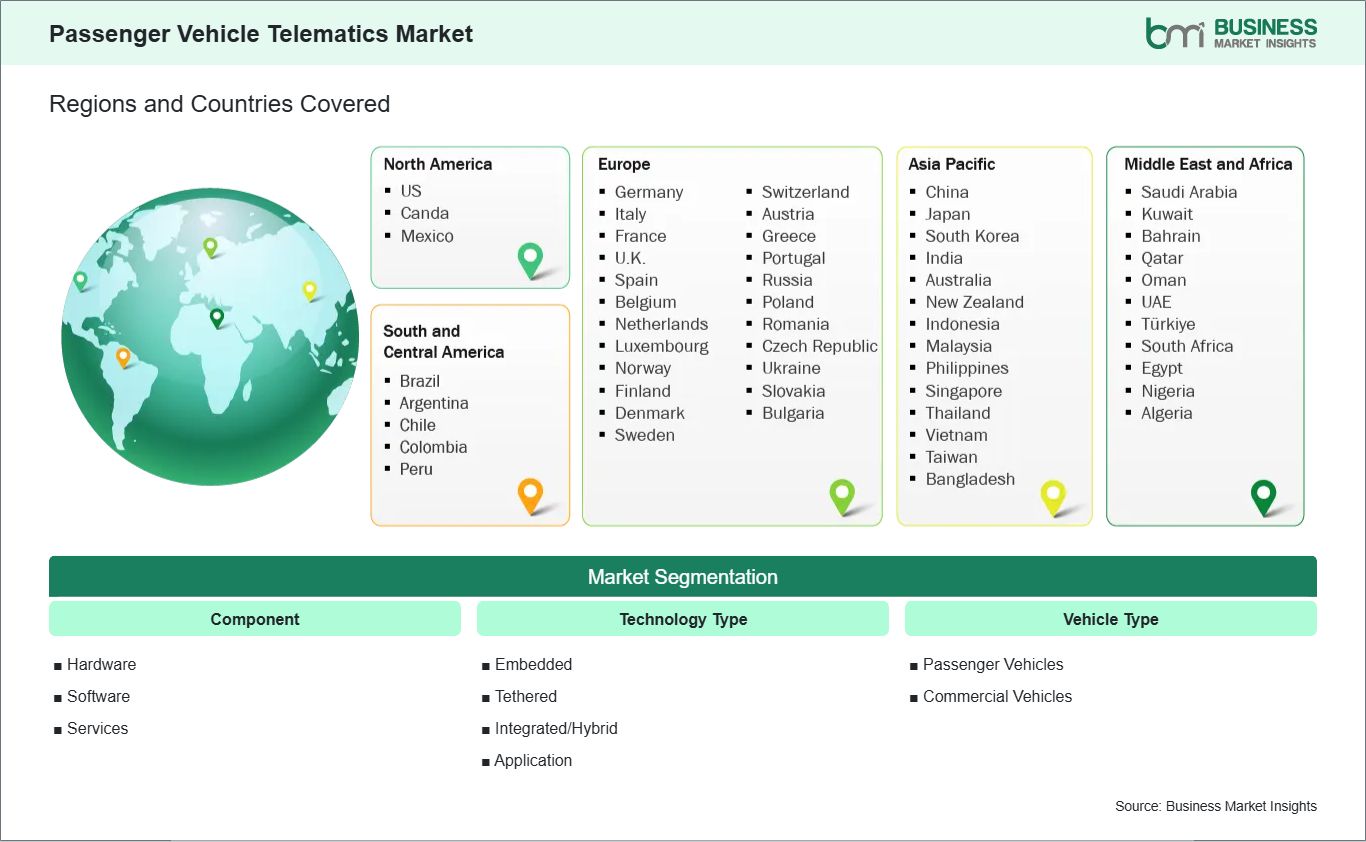

The passenger vehicle telematics market is segmented based on component, technology type, application, and vehicle type, reflecting its critical role in enhancing vehicle connectivity, real-time diagnostics, and passenger safety globally.

By Component

Hardware : Establishes in-vehicle connectivity, sensing, and data capture across telematics functions.

Software : Enables analytics, interface control, diagnostics, and service orchestration.

Services : Supports subscriptions, updates, assistance programs, and platform continuity.

By Technology Type

Embedded : Delivers always-on connectivity through factory-installed communication modules.

Tethered : Uses external devices to extend communication and app-based functionality.

Integrated/Hybrid : Combines onboard systems with mobile and cloud interaction.

Passenger Vehicle Telematics Market Drivers and Opportunities:

Expansion of Connected Vehicle Service Ecosystems

Automotive manufacturers are embedding more digital functions into passenger vehicles as buyers expect continuous connectivity, remote access, and smarter in-car interfaces. That shift raises the need for telematics architectures capable of linking onboard systems with cloud platforms, mobile applications, and service networks. As connectivity becomes part of core vehicle design, telematics deployment broadens across safety, convenience, and lifecycle support functions.

This transition reshapes value creation beyond the vehicle sale by enabling subscription services, feature activation, diagnostics, and customer engagement over time. In practical terms, telematics becomes relevant not only for data transfer but also for service continuity and brand retention. The market benefits because these systems support a more durable relationship between manufacturers, mobility platforms, insurers, and end users.

Integration of Telematics with Software-Defined Vehicle Platforms

Software-defined vehicle development is creating a favorable environment for telematics solutions that can support updates, feature management, predictive insights, and cross-platform service delivery. Innovation in vehicle computing architecture allows telematics systems to serve as a communication layer connecting sensors, applications, and digital control functions. This expands use cases across navigation personalization, remote diagnostics, and usage-linked services.

Future scope is broad as automakers refine centralized architectures and seek scalable digital business models across vehicle portfolios. Expansion opportunities are especially relevant where telematics supports modular services that can be configured by region, ownership model, or user preference. Over time, this strengthens the role of telematics as a commercial platform rather than only a connectivity feature within passenger mobility.

Passenger Vehicle Telematics Market Size and Share Analysis:

The Passenger Vehicle Telematics Market was valued at USD 12.24 Billion in 2025 and is projected to reach USD 31.18 Billion by 2033, expanding at a CAGR of 12.4% during 2026 - 2033. This trajectory reflects deeper integration of connected services into mainstream passenger mobility and a broader shift toward data-enabled vehicle functionality. The industry is moving from isolated telematics modules toward more unified digital ecosystems that support service continuity and vehicle intelligence.

From a component perspective, hardware retains strategic importance because physical connectivity infrastructure remains essential for dependable telematics performance. Software, however, is becoming a stronger differentiator as service layers, analytics capabilities, and interface experiences shape user value. Services maintain commercial significance by extending monetization beyond installation and reinforcing the continuity of digital vehicle engagement.

Across applications, infotainment and navigation hold a prominent position because they are directly visible to end users and closely tied to daily driving experience. Safety and security maintain strong relevance through emergency support and vehicle monitoring functions, while insurance telematics and fleet management continue to broaden utility through data-led operational and risk-based use cases.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Robert Bosch GmbH

Continental AG

OnStar Corporation

AirIQ Inc.

Agero, Inc.

Qualcomm Incorporated

ETAS Group

Zonar Systems

Omnitracs, LLC

Bridgestone Mobility Solutions B.V.

Masternaut Limited

MiX Telematics

Get more information on this report

Passenger Vehicle Telematics Market Report Coverage and Deliverables:

The "Passenger Vehicle Telematics Market Size and Forecast (2022:2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Passenger Vehicle Telematics market shows diverse regional adoption patterns influenced by regulatory maturity, digital infrastructure readiness, vehicle electronics integration, and consumer expectations for connected mobility. Globally, the market is moving toward broader standardization of onboard connectivity as telematics becomes more closely aligned with vehicle safety functions, remote service delivery, and software-centered ownership experiences. Regional differences now reflect how quickly each market converts connectivity from an optional feature into an everyday transportation utility.

North America maintains a mature operating environment shaped by strong consumer familiarity with connected services, established automotive digital ecosystems, and wide acceptance of subscription-based vehicle features. The region favors telematics offerings that combine convenience, diagnostics, infotainment continuity, and security functions within cohesive service platforms. Market development is also supported by insurer interest in behavior-linked models and by manufacturers seeking stronger retention through post-sale digital engagement.

Asia Pacific presents a dynamic expansion environment where vehicle digitization, smartphone-centric usage patterns, and large-scale automotive production support wider telematics integration. Demand formation differs across countries, yet the region consistently rewards solutions that balance affordability, feature relevance, and mobile connectivity. Local ecosystems are especially responsive to navigation enhancement, remote functions, and integrated digital experiences that align with broader smart mobility development.

Europe demonstrates sustained relevance through safety-oriented regulatory frameworks, strong engineering alignment with embedded systems, and consumer acceptance of connected vehicle functions that support compliance and convenience. Beyond Europe, emerging markets in the Middle East, Africa, and South and Central America are building telematics relevance through selective adoption tied to security, route visibility, and service modernization. These markets may progress unevenly, but they offer meaningful expansion space as connectivity infrastructure and digital vehicle expectations advance.

Get more information on this report

Passenger Vehicle Telematics Market Research Report Guidance:

The Passenger Vehicle Telematics market report includes qualitative and quantitative data in the passenger vehicle telematics market across component, technology type, application, vehicle type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the passenger vehicle telematics market .

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the passenger vehicle telematics market , including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the passenger vehicle telematics market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover passenger vehicle telematics market segments by component, technology type, application, vehicle type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the passenger vehicle telematics market . Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Passenger Vehicle Telematics Market News and Key Development:

The passenger vehicle telematics market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the passenger vehicle telematics market are:

June 2026, Huawei expanded its connected vehicle ecosystem with updates to HiCar 6.0, enhancing smartphone-to-vehicle connectivity, navigation, voice interaction, and infotainment integration. The development reflects growing demand for embedded telematics and connected car services in passenger vehicles.

March 2026, Ford introduced Ford Pro AI, a generative AI-powered telematics assistant that analyzes vehicle data and provides actionable insights. While initially focused on fleet applications, the launch highlights the broader trend of integrating AI into vehicle telematics platforms for predictive maintenance, diagnostics, and driver assistance.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Passenger Vehicle Telematics Market

Robert Bosch GmbH

Continental AG

OnStar Corporation

AirIQ Inc.

Agero, Inc.

Qualcomm Incorporated

ETAS Group

Zonar Systems

Omnitracs, LLC

Bridgestone Mobility Solutions B.V.

Masternaut Limited

MiX Telematics

Frequently Asked Questions

How big is the Passenger Vehicle Telematics Market?

The Passenger Vehicle Telematics Market is valued at US$ 12.24 Billion in 2025, it is projected to reach US$ 31.18 Billion by 2033.

What is the CAGR for Passenger Vehicle Telematics Market by (2026 - 2033)?

As per our report Passenger Vehicle Telematics Market, the market size is valued at US$ 12.24 Billion in 2025, projecting it to reach US$ 31.18 Billion by 2033. This translates to a CAGR of approximately 12.4% during the forecast period.

What segments are covered in this report?

The Passenger Vehicle Telematics Market report typically cover these key segments-

Component (Hardware, Software, Services)

Technology Type (Embedded, Tethered, Integrated/Hybrid), Application (Fleet Management, Safety & Security, Insurance Telematics, Infotainment & Navigation, Other Application)

Vehicle Type (Passenger Vehicles, Commercial Vehicles)

What is the historic period, base year, and forecast period taken for Passenger Vehicle Telematics Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Passenger Vehicle Telematics Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Passenger Vehicle Telematics Market?

The Passenger Vehicle Telematics Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Robert Bosch GmbH

Continental AG

OnStar Corporation

AirIQ Inc.

Agero, Inc.

Qualcomm Incorporated

ETAS Group

Zonar Systems

Omnitracs, LLC

Bridgestone Mobility Solutions B.V.

Masternaut Limited

MiX Telematics

Who should buy this report?

The Passenger Vehicle Telematics Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Passenger Vehicle Telematics Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Passenger Vehicle Telematics Market

Get Free Sample For Passenger Vehicle Telematics Market