Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Battery Electric Vehicles (BEVs))

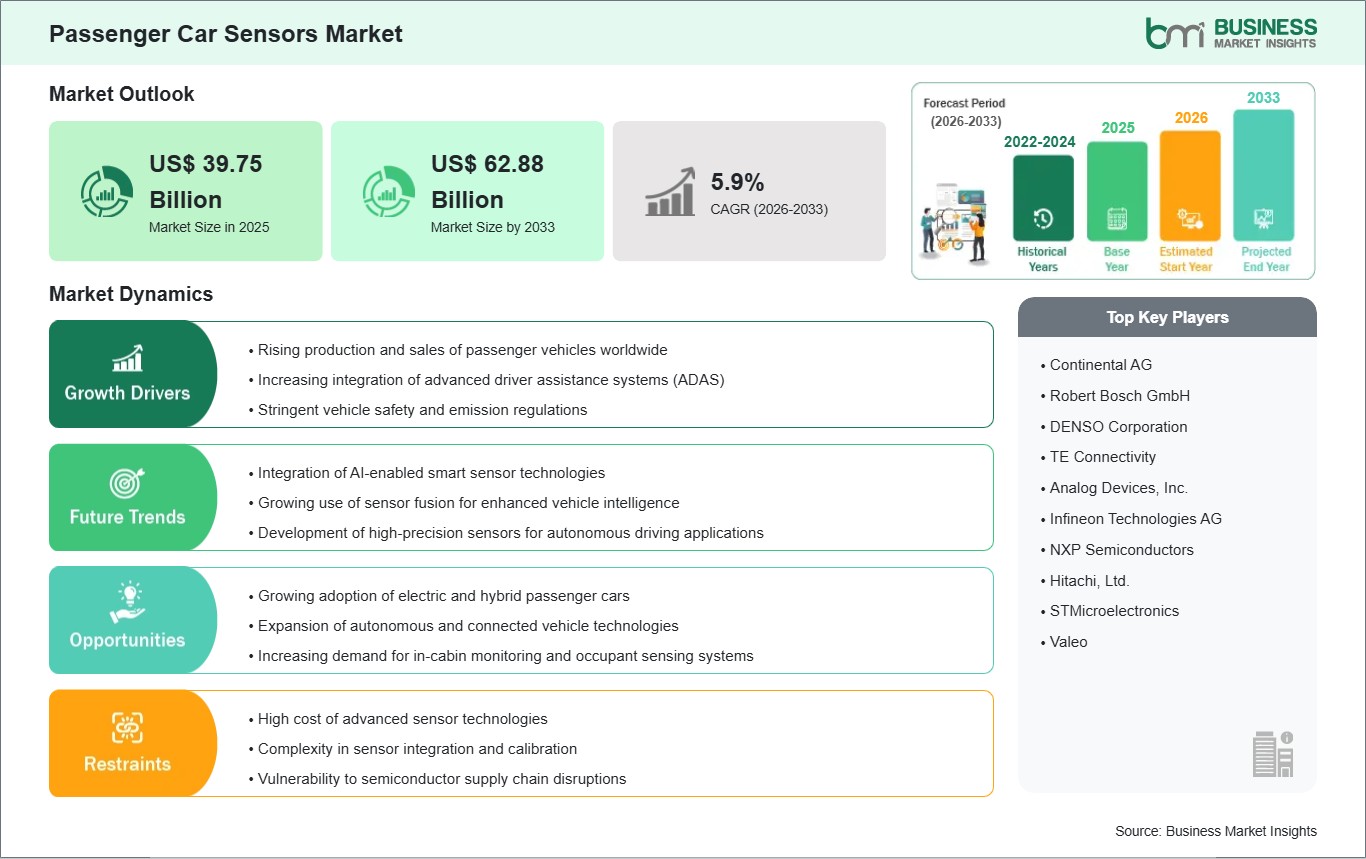

The passenger car sensors market size is expected to reach US$ 62.88 billion by 2033 from US$ 39.75 billion in 2025. The market is estimated to record a CAGR of 5.9% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Passenger car sensors are electronic components that detect physical conditions and convert them into signals for vehicle control systems. They support measurement, monitoring, and response functions across safety, comfort, propulsion, and connectivity architectures. Their role has expanded as passenger vehicles incorporate greater electronic content and more software-defined functions.

Rising utilization of driver assistance features, emissions control systems, and cabin intelligence continues to broaden sensor integration. Automakers require accurate real-time inputs to improve decision-making across braking, steering, battery management, and occupant protection functions. This requirement strengthens procurement across both legacy vehicle platforms and newer electrified models.

From a segmentation perspective, the market reflects a balanced mix of sensing requirements across thermal, pressure, positional, speed, and proximity monitoring. Application demand remains closely tied to powertrain management, safety systems, advanced driver assistance functions, body electronics, and connected infotainment environments. Propulsion diversification further reshapes sensor selection, calibration requirements, and system architecture priorities.

Technology evolution within this sector is centered on miniaturization, higher processing compatibility, stronger durability, and improved signal reliability. Sensor modules are increasingly engineered for integration with domain controllers and centralized vehicle computing systems. This transition supports better data fusion, lower latency, and more responsive operation in complex passenger vehicle environments.

The competitive environment is defined by product refinement, platform compatibility, and the ability to support multiple vehicle categories with consistent performance. Suppliers are focusing on broader sensing portfolios and tighter alignment with vehicle electronics roadmaps. As design cycles accelerate, the market continues to reward engineering depth, validation capability, and scalable manufacturing execution.

Passenger Car Sensors Market - Strategic Insights:

Get more information on this report

Passenger Car Sensors Market Segmentation Analysis:

The passenger car sensors market is segmented based on type, application, and propulsion type, reflecting its critical role in optimizing vehicle performance, improving fuel efficiency, and ensuring passenger safety.

By Type

Temperature Sensors : Support thermal regulation across engines, batteries, cabins, and electronic control units.

Pressure Sensors : Monitor fluid, air, and combustion conditions for stable vehicle system performance.

Position Sensors : Enable precise component tracking in steering, throttle, transmission, and seating systems.

Speed Sensors : Deliver motion data essential for braking, drivetrain coordination, and stability control.

Proximity Sensors : Improve detection capability for parking, obstacle awareness, and occupant interaction features.

Other Type : Covers specialized sensing functions tailored to emerging electronic and comfort applications.

By Application

Powertrain Systems : Maintain operational accuracy across propulsion, emissions management, and thermal control functions.

Safety & Security Systems : Strengthen occupant protection, intrusion sensing, and vehicle condition monitoring capabilities.

Advanced Driver Assistance Systems (ADAS) : Supply environmental and positional inputs for assisted driving decisions.

Body Electronics & Comfort Systems : Enhance convenience features through responsive sensing across interior systems.

Infotainment & Connectivity Systems : Support user interaction, device integration, and smart in-cabin functionality.

By Propulsion Type

Internal Combustion Engine (ICE) Vehicles : Retain broad sensor demand across engine control and exhaust monitoring.

Hybrid Electric Vehicles (HEVs) : Require mixed sensing architectures for engine-electric coordination and energy balancing.

Plug-in Hybrid Electric Vehicles (PHEVs) : Combine charging, battery, and combustion monitoring within one platform.

Battery Electric Vehicles (BEVs) : Emphasize thermal, positional, and high-efficiency sensing across electrified systems.

Passenger Car Sensors Market Drivers and Opportunities:

Integration of Advanced Vehicle Electronics

Passenger vehicles now incorporate more electronic control functions across propulsion, braking, steering, and cabin management. This shift creates a stronger need for continuous sensing inputs that can support accurate system response. As more functions become software-coordinated, automakers expand deployment of sensors that deliver stable signals under changing operating conditions and support dependable control logic across the vehicle platform.

The impact extends beyond individual components because sensing reliability directly influences safety, efficiency, and user experience. In this context, sensor integration becomes increasingly relevant for manufacturers seeking consistent performance across conventional and electrified passenger vehicles. The market benefits from this transition as vehicle design priorities move toward higher functional density, stronger diagnostics capability, and improved coordination between mechanical and digital subsystems.

Expansion of Electrified and Connected Passenger Vehicles

Electrified and connected vehicle programs are opening new application areas for advanced sensing technologies. Battery thermal monitoring, cabin intelligence, predictive maintenance, and connected diagnostics create practical use cases that extend beyond traditional engine-focused systems. This trend encourages innovation in compact, durable, and software-compatible sensor designs that can operate across diverse passenger vehicle architectures and support evolving feature sets.

Future scope remains broad as automakers refine electrical platforms, digital cockpits, and integrated control domains. Expansion across hybrid and battery-based propulsion systems increases the relevance of sensors that can support energy management and real-time operational visibility. The opportunity for this market lies in enabling smarter vehicle behavior, more adaptive system performance, and a more seamless connection between hardware sensing and software intelligence.

Passenger Car Sensors Market Size and Share Analysis:

The Passenger Car Sensors Market was valued at USD 39.75 Billion in 2025 and is projected to reach USD 62.88 Billion by 2033, expanding at a CAGR of 5.9% during 2026 - 2033. This trajectory reflects sustained incorporation of sensing technologies across modern passenger vehicles as electronic content rises and system responsiveness becomes more central to vehicle design.

Type-based positioning indicates strong relevance for temperature, pressure, position, and speed sensors because they serve foundational monitoring functions across core vehicle systems. Proximity sensors also hold strategic importance as parking support, cabin detection, and assisted driving features gain wider integration. The broader type landscape remains shaped by application specificity and platform architecture choices.

Application leadership is closely associated with powertrain systems and safety-oriented functions, where sensor accuracy directly influences system performance and control quality. Advanced driver assistance systems continue to strengthen their role within demand formation as vehicle intelligence expands. Body electronics, comfort features, and infotainment environments add further depth by broadening sensor use beyond traditional mechanical monitoring.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Continental AG

Robert Bosch GmbH

DENSO Corporation

TE Connectivity

Analog Devices, Inc.

Infineon Technologies AG

NXP Semiconductors

Hitachi, Ltd.

STMicroelectronics

Valeo

Get more information on this report

Passenger Car Sensors Market Report Coverage and Deliverables:

The "Passenger Car Sensors Market Size and Forecast (2022:2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Passenger Car Sensors Market Geographic Insights:

The Passenger Car Sensors market shows diverse regional adoption patterns influenced by vehicle production structures, regulatory priorities, electronic feature penetration, and the pace of propulsion transition. At the global level, manufacturers are aligning sensor strategies with broader shifts toward safer, smarter, and more connected passenger vehicles. Demand formation differs by platform maturity, but system integration intensity remains a common theme across the industry.

North America reflects strong alignment with premium safety functions, digital vehicle interfaces, and integrated control architectures. Passenger vehicle platforms in this region often prioritize sensing performance that supports assisted driving, cabin monitoring, and higher-value electronic content. Development activity also benefits from close interaction between vehicle manufacturers, semiconductor suppliers, and software-focused engineering ecosystems.

Asia Pacific maintains a broad industrial base with substantial passenger vehicle production and a wide spectrum of technology adoption levels. The region combines large-scale manufacturing capacity with rising deployment of advanced electronics in both mainstream and higher-specification models. Electrification momentum, supplier diversification, and continued refinement of local vehicle platforms support a strong operational environment for sensor integration.

Europe emphasizes technical precision, emissions compliance, and advanced safety architecture, which sustains consistent demand for sophisticated sensing systems. Emerging markets across the Middle East and Africa and South and Central America are advancing at different speeds, shaped by affordability, import structures, and vehicle mix. Even so, feature migration from higher-end platforms continues to widen the long-term addressable scope across these regions.

Get more information on this report

Passenger Car Sensors Market Research Report Guidance:

The Passenger Car Sensors market report includes qualitative and quantitative data in the passenger car sensors market across type, application, propulsion type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the passenger car sensors market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the passenger car sensors market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the passenger car sensors market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover passenger car sensors market segments by type, application, propulsion type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the passenger car sensors market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Passenger Car Sensors Market News and Key Development:

The passenger car sensors market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In September 2025, Valeo, the global leader in Advanced Driver Assistance Systems (ADAS) and Capgemini, announced a new collaboration for the testing and validation of a new, complete, and integrated ADAS system up to Level 2+. With this solution, Valeo and Capgemini address a major challenge in modern mobility: reinforcing safety around vehicles to help reduce accidents, improve driver assistance and advance the development of autonomous vehicles.

In October 2025, OMNIVISION, a leading global developer of semiconductor technology, including advanced digital imaging, analog and display solutions, announced its latest-generation automotive image sensor: the OX08D20 8‑megapixel (MP) CMOS image sensor with TheiaCel™ technology. This new device is an upgrade to the popular OX08D10 sensor for exterior cameras used in advanced driver assistance systems (ADAS) and autonomous driving (AD). The device will be introduced at AutoSens Europe (Booth 300), taking place October 7‑9, 2025, in Barcelona, Spain, where OMNIVISION is the lead sponsor.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Passenger Car Sensors Market

Continental AG

Robert Bosch GmbH

DENSO Corporation

TE Connectivity

Analog Devices, Inc.

Infineon Technologies AG

NXP Semiconductors

Hitachi, Ltd.

STMicroelectronics

Valeo

Frequently Asked Questions

How big is the Passenger Car Sensors Market?

The Passenger Car Sensors Market is valued at US$ 39.75 Billion in 2025, it is projected to reach US$ 62.88 Billion by 2033.

What is the CAGR for Passenger Car Sensors Market by (2026 - 2033)?

As per our report Passenger Car Sensors Market, the market size is valued at US$ 39.75 Billion in 2025, projecting it to reach US$ 62.88 Billion by 2033. This translates to a CAGR of approximately 5.9% during the forecast period.

What segments are covered in this report?

The Passenger Car Sensors Market report typically cover these key segments-

Type (Temperature Sensors, Pressure Sensors, Position Sensors, Speed Sensors, Proximity Sensors, Other Type)

Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Electric Vehicles (HEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Battery Electric Vehicles (BEVs))

What is the historic period, base year, and forecast period taken for Passenger Car Sensors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Passenger Car Sensors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Passenger Car Sensors Market?

The Passenger Car Sensors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Continental AG

Robert Bosch GmbH

DENSO Corporation

TE Connectivity

Analog Devices, Inc.

Infineon Technologies AG

NXP Semiconductors

Hitachi, Ltd.

STMicroelectronics

Valeo

Who should buy this report?

The Passenger Car Sensors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Passenger Car Sensors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Passenger Car Sensors Market

Get Free Sample For Passenger Car Sensors Market