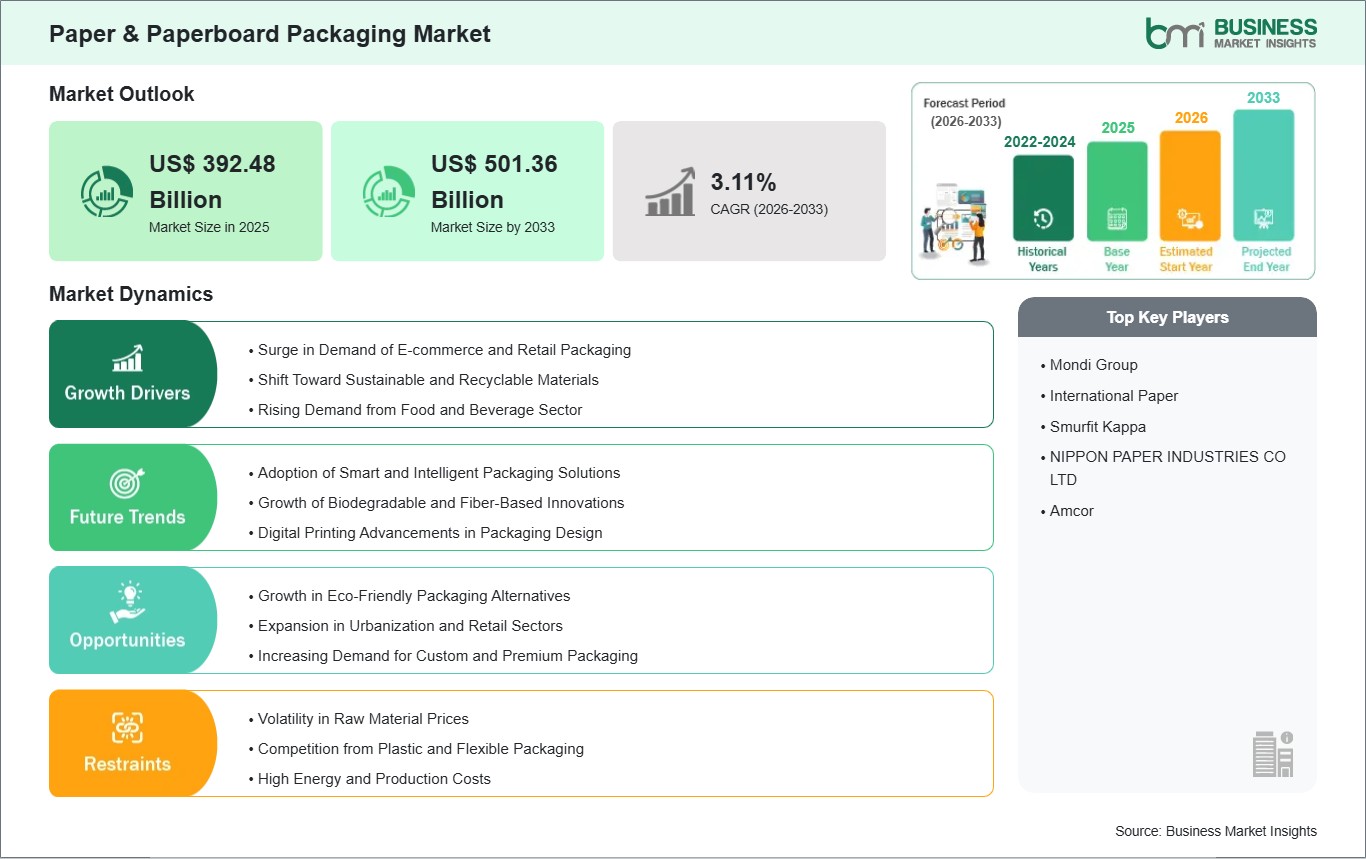

The Paper & Paperboard Packaging Market size is expected to reach US$ 501.36 Billion by 2033 from US$ 392.48 Billion in 2025. The market is estimated to record a CAGR of 3.11% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The paper and paperboard packaging market, at a global level, is witnessing a paradigm shift, driven by a higher emphasis on sustainability, environmental responsibility, and a circular economy approach at a global level. This has led to a transformation of the paper and paperboard packaging market, not only in terms of functionality but also as a tool to create brand differentiation, consumer engagement, and communicate sustainability messages to consumers. There has been a higher awareness of environmental issues, particularly with regard to plastic usage, along with stringent government regulations in various countries to restrict plastic usage, thereby driving the paper and paperboard packaging market. Advances in material science have also led to a higher performance level of paper and paperboard-based packaging, thereby making them suitable to meet consumer and logistical needs.

Despite a positive growth pattern, the paper and paperboard packaging industry is facing several challenges, such as a greater reliance on forestry-based materials, which is causing a fluctuating pattern of supply and cost for the industry. Additionally, technology challenges are also faced by the industry in different packaging materials, such as liquid or oxygen-sensitive packaging materials. However, due to an increasing focus on sustainable packaging by different brands around the world, the demand for sustainable packaging is also increasing. The paper and paperboard packaging industry is seen as a key enabler of sustainable packaging solutions around the world.

Paper & Paperboard Packaging Market - Strategic Insights:

Get more information on this report

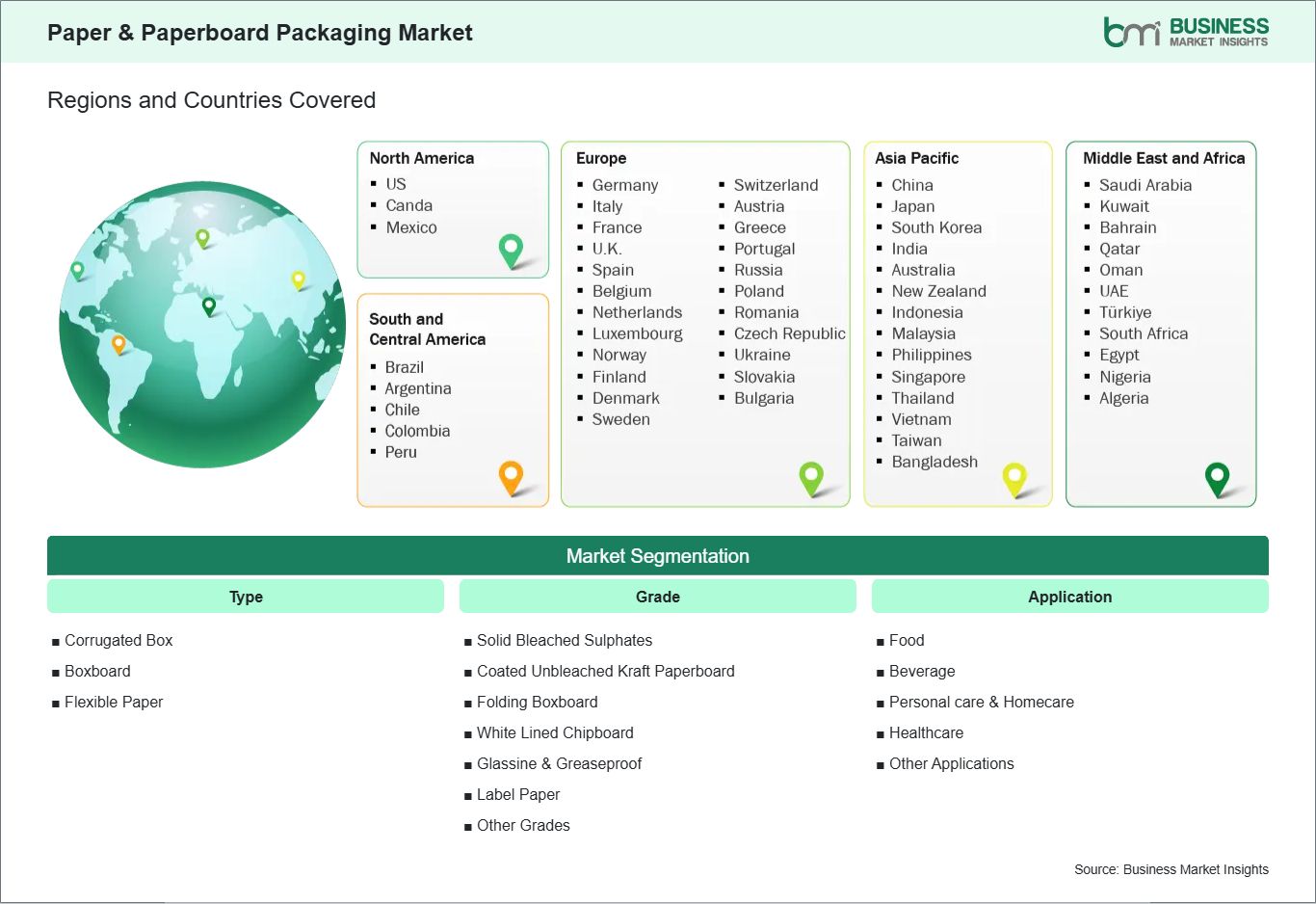

Paper & Paperboard Packaging Market Segmentation Analysis:

Key segments that contributed to the derivation of the paper & paperboard packaging market analysis are type, grade, and application.

By type, the paper & paperboard packaging market is segmented into corrugated box, boxboard, and flexible paper. The corrugated box subsegment dominated the market in 2025.

Based on grade, the paper & paperboard packaging market is classified into solid bleached sulphates (SBS), coated unbleached kraft paperboard (CUK/SUS), folding boxboard (FBB), white lined chipboard (WLC), glassine & greaseproof, label paper, and other grades. The solid bleached sulphates (SBS) subsegment dominated the market in 2025.

In terms of application, the paper & paperboard packaging market is divided into food, beverage, personal care & homecare, healthcare, and other applications. The food subsegment dominated the market in 2025.

Paper & Paperboard Packaging Market Drivers and Opportunities:

Surge in Demand of E-commerce and Retail Packaging

The global paper and paperboard packaging market is experiencing a remarkable surge, largely fueled by the expansion of e‑commerce and evolving retail demands. As consumer expectations continue to shift toward convenience, speed, and reliability, packaging has become an essential element not just for product protection but also for enhancing the overall customer experience. Paper and paperboard offer significant advantages in this context due to their versatility, lightweight nature, and strength, making them suitable for a wide range of products, from fragile items to bulk shipments. Packaging now serves as a strategic touchpoint where businesses can convey brand value and leave a lasting impression on consumers.

The growing prominence of e‑commerce has also prompted innovation in packaging design, emphasizing both functionality and aesthetics. Companies are investing in modular, foldable, and customizable packaging solutions that improve efficiency while providing a premium unboxing experience. Features such as reinforced corners, reusable inserts, and high-quality printing allow brands to deliver products securely while communicating their identity and values through packaging. The demand for packaging that balances protection, visual appeal, and user convenience has therefore become a key driver in the global market, transforming packaging into an integral part of the consumer journey.

In addition, the growing sophistication of global supply chains necessitates packaging solutions that maximize storage, transportation, and handling efficiency. Packaging designs that reduce material consumption, transportation costs, and structural failure are now essential for businesses to operate efficiently. As these factors combine to support the growth of e-commerce, improved consumer experience, and supply chain optimization, the opportunities for paper and paperboard packaging to satisfy several business needs at once will only continue to grow. As the global market for packaging develops further, it is likely to become a means to achieve business efficiency and brand awareness.

Growth in Eco-Friendly Packaging Alternatives

Sustainability is also a key driving factor for the global paper and paperboard packaging market. With the increasing realization of the challenges facing the environment, companies are focusing more and more on packaging materials that are sustainable and have a positive impact on the environment. Paper and paperboard are seen to be an important part of sustainable packaging due to their recyclable nature and the ability to be reused multiple times. The focus on sustainable packaging is changing the standards of the industry and is encouraging companies to be innovative in the materials and methods being developed for packaging. Companies are also recognizing the importance of sustainability and are focusing on it as an integral part of packaging.

Innovation in eco-friendly packaging has focused on enhancing performance while reducing environmental impact. Minimalistic designs, lightweight structures, and modular formats allow packaging to meet functional requirements while using fewer resources. Water-based coatings, biodegradable adhesives, and reusable inserts further increase sustainability without compromising product protection or aesthetic appeal. Businesses are increasingly integrating sustainability considerations into the early stages of packaging development, ensuring that products are designed with environmental responsibility in mind. This approach helps brands strengthen their reputation, meet consumer expectations for ethical practices, and demonstrate a proactive commitment to global environmental goals.

Beyond design and materials, the growth of eco-friendly packaging has implications across the entire supply chain. From sourcing renewable raw materials to optimizing manufacturing processes and improving recyclability, companies are adopting holistic strategies that reduce environmental footprints. Paper and paperboard packaging are now recognized as versatile solutions capable of delivering both performance and sustainability. As consumer and corporate demand for environmentally responsible packaging continues to grow, the global market is likely to witness further innovation, with paper-based materials playing a central role in shaping the future of packaging across industries.

Paper & Paperboard Packaging Market Size and Share Analysis:

The paper & paperboard packaging market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, grade, and application, highlighting their respective contributions to overall market performance.

By type, the Corrugated Box subsegment dominated the Paper & Paperboard Packaging market in 2025. Corrugated boxes offer excellent strength, durability, and protection for a wide range of goods, making them highly suitable for logistics and shipping applications, which drives their widespread adoption.

Based on grade, the Solid Bleached Sulphates (SBS) subsegment dominated the Paper & Paperboard Packaging market in 2025. SBS provides superior printability, stiffness, and hygienic properties, making it ideal for high-quality packaging, supporting strong demand for this grade.

In terms of application, the Food subsegment dominated the Paper & Paperboard Packaging market in 2025. Food packaging requires safety, barrier protection, and sustainability, reinforcing the dominance of this segment in the market.

Paper & Paperboard Packaging Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Mondi Group

International Paper

Smurfit Kappa

NIPPON PAPER INDUSTRIES CO LTD

Amcor

Get more information on this report

Paper & Paperboard Packaging Market Report Coverage and Deliverables:

The "Paper & Paperboard Packaging Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Paper & Paperboard Packaging market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Paper & Paperboard Packaging market trends, as well as drivers, restraints, and opportunities

Paper & Paperboard Packaging market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Paper & Paperboard Packaging market

Detailed company profiles, including SWOT analysis

Paper & Paperboard Packaging Market Geographic Insights:

The geographical scope of the Paper & Paperboard Packaging market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Paper & Paperboard Packaging market in North America is expected to grow during the forecast period.

North America is the leading segment in the global paper and paperboard packaging industry due to a mix of industrial infrastructure, technological capabilities, and early adopters of sustainability initiatives. It has been at the forefront in enforcing stringent environmental regulations and business sustainability initiatives that encourage the use of renewable and recyclable materials instead of conventional plastic materials. This has led to a high demand for paperboard cartons, corrugated containers, molded fiber packaging materials, and more in various industries like food and beverages, personal care, pharmaceuticals, and e-commerce. There is a growing trend in North American consumers towards eco-friendly packaging materials that highlight sustainability, recyclability, and eco-innovation in packaging, thus prompting manufacturers to develop innovative packaging solutions in terms of lightweight materials, high-quality coatings, and attractive graphics that meet functional and brand requirements.

Additionally, there is a strong recycling system in place in North America, which includes recycling collected materials and reintroducing recycled fibers into new packaging materials in line with the circular economy framework. There is a significant investment in research and development activities by North American manufacturers in exploring new avenues in the use of paperboard packaging materials in high-barrier packaging and liquid packaging applications, which were previously dominated by plastic materials. Despite these advancements, challenges remain, including regional disparities in recycling capabilities, raw material price fluctuations, and supply chain logistics in meeting the demand across urban and rural areas. North America continues to act as a global benchmark for sustainable packaging adoption, driving technological innovation, regulatory compliance, and environmentally responsible practices in the paper and paperboard packaging sector worldwide.

Get more information on this report

Paper & Paperboard Packaging Market Research Report Guidance:

The report includes qualitative and quantitative data in the Paper & Paperboard Packaging market across type, grade, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Paper & Paperboard Packaging market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Paper & Paperboard Packaging market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Paper & Paperboard Packaging market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Paper & Paperboard Packaging market segments by type, grade, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Paper & Paperboard Packaging market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Paper & Paperboard Packaging Market News and Key Development:

The paper & paperboard packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the paper & paperboard packaging market are:

In November 2025, Graphic Packaging International announced that its new recycled paperboard mill in Waco, Texas, began producing its first commercially saleable paperboard rolls ahead of schedule, marking a major expansion of its sustainable paperboard production capacity for global packaging applications.

In July 2025, Sappi North America announced that it had completed and begun commercial production following the US$ 500 million expansion and conversion of Paper Machine No. 2 (PM2) at its Somerset Mill in Maine, effectively doubling its paperboard capacity for high‑performance solid bleached sulfate (SBS) packaging grades to better meet rising sustainable packaging demand worldwide.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Paper & Paperboard Packaging Market

Mondi Group

International Paper

Smurfit Kappa

NIPPON PAPER INDUSTRIES CO LTD

Amcor

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Paper & Paperboard Packaging Market?

The Paper & Paperboard Packaging Market is valued at US$ 392.48 Billion in 2025, it is projected to reach US$ 501.36 Billion by 2033.

What is the CAGR for Paper & Paperboard Packaging Market by (2026 - 2033)?

As per our report Paper & Paperboard Packaging Market, the market size is valued at US$ 392.48 Billion in 2025, projecting it to reach US$ 501.36 Billion by 2033. This translates to a CAGR of approximately 3.11% during the forecast period.

What segments are covered in this report?

The Paper & Paperboard Packaging Market report typically cover these key segments-

Application (Food, Beverage, Personal care & Homecare, Healthcare, Other Applications)

What is the historic period, base year, and forecast period taken for Paper & Paperboard Packaging Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Paper & Paperboard Packaging Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Paper & Paperboard Packaging Market?

The Paper & Paperboard Packaging Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Mondi Group

International Paper

Smurfit Kappa

NIPPON PAPER INDUSTRIES CO LTD

Amcor

Who should buy this report?

The Paper & Paperboard Packaging Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Paper & Paperboard Packaging Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Paper & Paperboard Packaging Market

Get Free Sample For Paper & Paperboard Packaging Market