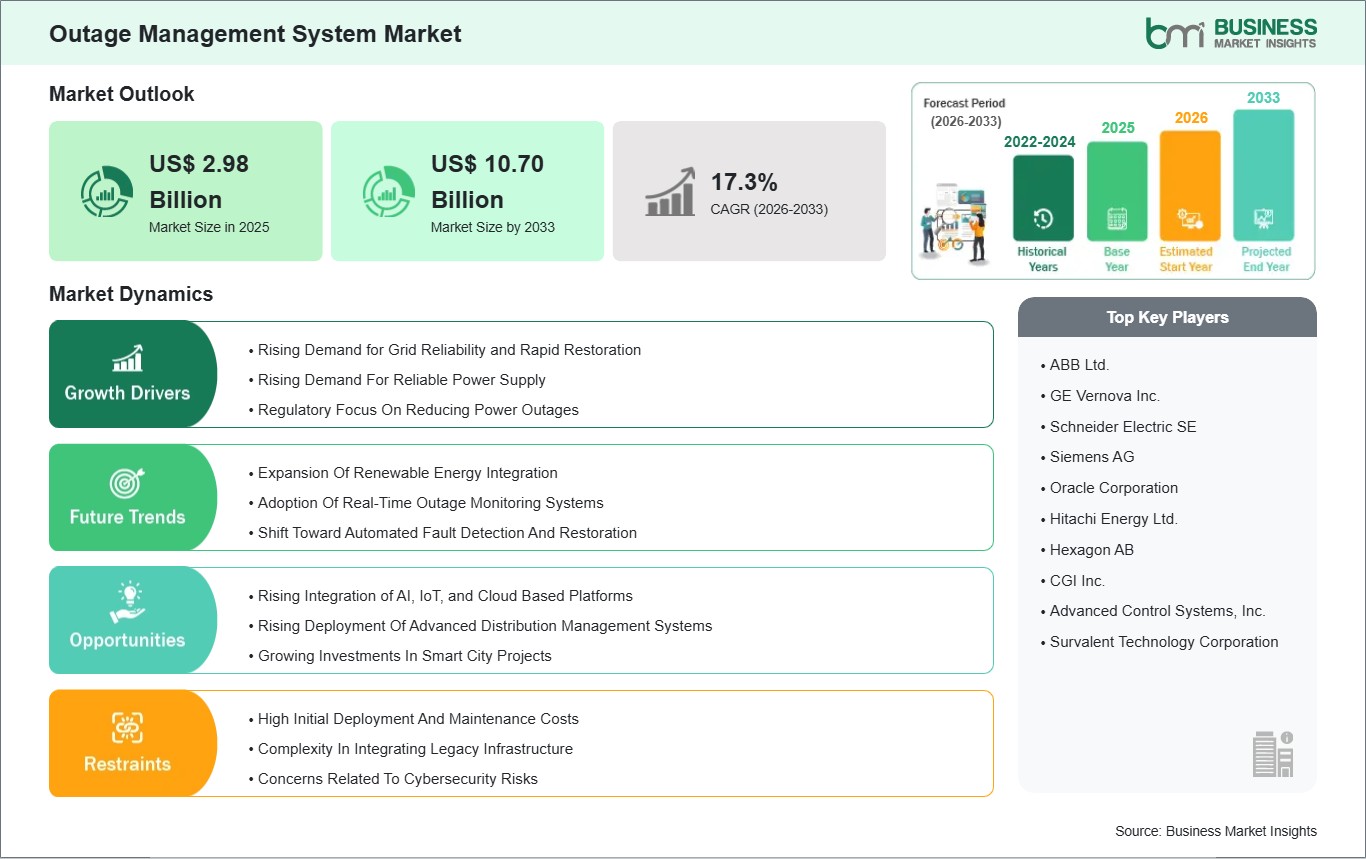

The Outage Management System market size is expected to reach US$ 10.70 billion by 2033 from US$ 2.98 billion in 2025. The market is estimated to record a CAGR of 17.3% from 2026 to 2033.

Executive Summary and Global Market Analysis:

An outage management system (OMS) refers to a specialized software platform engineered to identify, track, and facilitate the restoration of power during electrical grid disturbances. By integrating data from geographic information systems (GIS), advanced metering infrastructure (AMI), and supervisory control and data acquisition (SCADA) systems, an OMS enables utilities to localize faults and optimize the deployment of repair crews. This technology is fundamental to maintaining grid reliability and minimizing the System Average Interruption Duration Index (SAIDI) for utility providers. Market expansion is being propelled by the global requirement for grid modernization, the rising frequency of climate-induced weather events, and substantial institutional investment in smart grid infrastructure to support a more resilient energy ecosystem.

However, several factors may restrain market progression. The high capital intensity associated with deploying comprehensive OMS platforms, particularly when integrating with decades-old legacy assets, remains a significant hurdle for smaller municipal and cooperative utilities. The industry also faces technical challenges regarding the data quality gap in GIS records, as inaccurate spatial data can undermine the effectiveness of automated fault-location algorithms. Additionally, the increasing digitalization of grid operations has expanded the attack surface for sophisticated cyber threats, necessitating complex and ongoing investments in network security and data encryption. These hurdles, compounded by a persistent shortage of specialized personnel proficient in both electrical engineering and big-data analytics, increase operational complexity and the total cost of ownership.

Despite these hurdles, the market outlook remains favorable. Opportunities are emerging through the adoption of artificial intelligence and machine learning, which enable predictive outage modeling by correlating historical data with real-time weather patterns. The expansion of distributed energy resources (DERs) and microgrids is gaining traction, necessitating more sophisticated OMS capabilities for bidirectional power flow management. Furthermore, the growth of cloud-native and SaaS deployment models aligns with global goals for operational scalability and cost-efficiency. Collectively, these innovations position the outage management system industry for sustained long-term development as a cornerstone of the transition toward a decentralized and self-healing smart grid.

Outage Management System Market - Strategic Insights:

Get more information on this report

Outage Management System Market Segmentation Analysis:

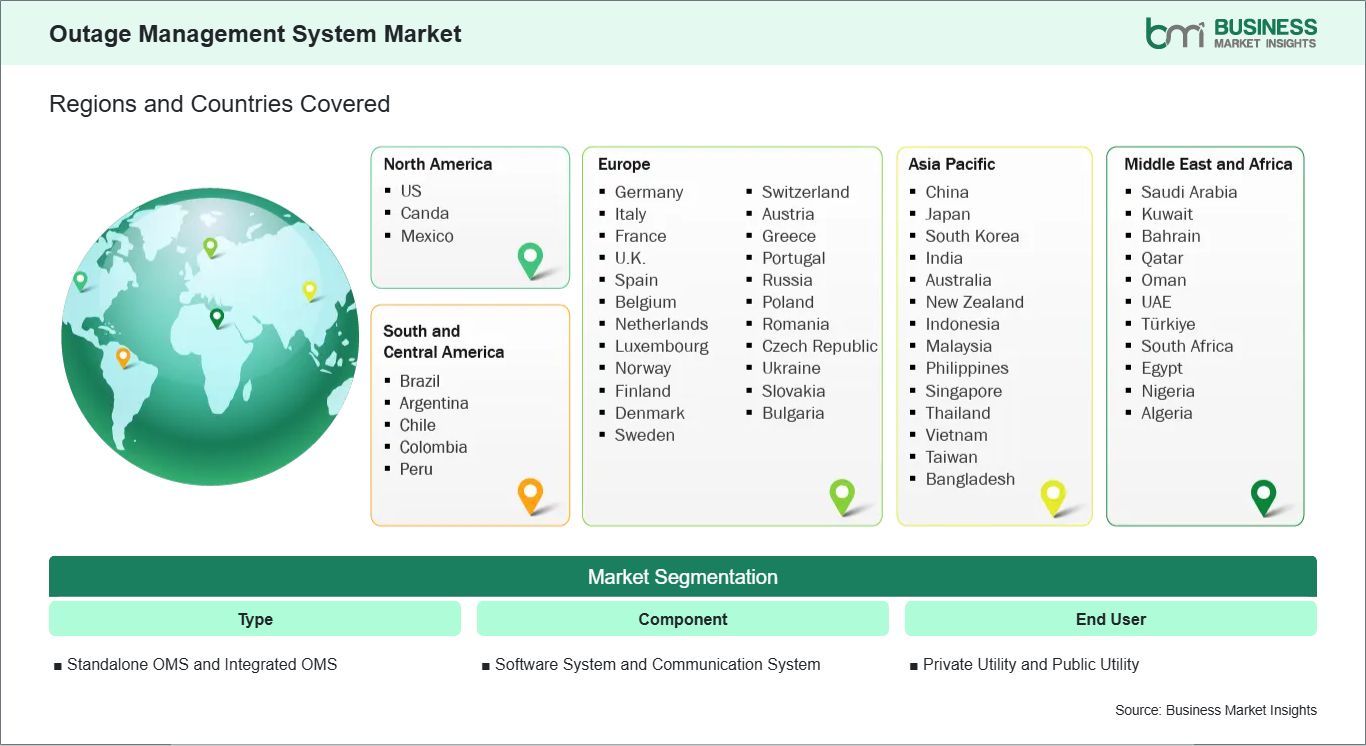

Key segments that contributed to the derivation of the Outage Management System market analysis are type, component, and end user.

By Type, the market is segmented into Standalone OMS and Integrated OMS.

By Component, the market is divided into Software System and Communication System.

By End User, the market is categorized into Private Utility and Public Utility.

Outage Management System Market Drivers and Opportunities:

Rising Demand for Grid Reliability and Rapid Restoration

The outage management system (OMS) market is being driven by the growing need for reliable electricity supply, efficient fault detection, and rapid service restoration. With rising global energy demand and increasing dependence on digital infrastructure, utilities are under pressure to minimize downtime and improve customer satisfaction. OMS platforms provide real‑time visibility into grid conditions, enabling operators to quickly identify outages, dispatch crews, and restore service. The expansion of smart grids and distributed energy resources is amplifying demand, as these complex networks require advanced monitoring and coordination tools. Regulatory mandates emphasizing resilience, service quality, and disaster preparedness are reinforcing adoption, particularly in regions prone to extreme weather events. Additionally, the rising integration of renewable energy sources is creating operational challenges that OMS solutions help address. Collectively, grid modernization, regulatory compliance, and the need for efficient outage response are propelling sustained growth in the global outage management system market.

Rising Integration of AI, IoT, and Cloud‑Based Platforms

Opportunities in the outage management system market are expanding through the integration of artificial intelligence, IoT sensors, and cloud‑based platforms. AI‑enabled OMS solutions can deliver predictive insights, automate fault detection, and optimize crew dispatch, reducing downtime and operational costs. IoT‑connected devices such as smart meters and sensors are creating new pathways for adoption, offering granular visibility into grid performance and enabling proactive maintenance. Cloud‑based OMS platforms are gaining traction due to their scalability, cost efficiency, and ability to support remote collaboration, making them ideal for utilities of all sizes. The growing emphasis on customer engagement is opening opportunities, as OMS solutions increasingly integrate with mobile apps and communication platforms to provide real‑time outage updates and service transparency. Additionally, the expansion of microgrids, renewable integration, and smart city projects is driving demand for advanced OMS capabilities. Vendors who focus on developing interoperable, AI‑driven, and cloud‑enabled solutions are well‑positioned to capture growth, underscoring a transformative trajectory for the global outage management system market.

Outage Management System Market Size and Share Analysis:

Based on Type, the Standalone OMS subsegment holds a strong presence in the market. These systems are indispensable for utilities seeking dedicated platforms to manage outages, offering reliability and focused functionality. The Integrated OMS subsegment is essential for organizations adopting advanced grid modernization strategies, combining OMS with other utility systems such as GIS, SCADA, and CIS to enhance efficiency and real‑time decision‑making.

Outage Management System Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

ABB Ltd.

GE Vernova Inc.

Schneider Electric SE

Siemens AG

Oracle Corporation

Hitachi Energy Ltd.

Hexagon AB

CGI Inc.

Advanced Control Systems, Inc.

Survalent Technology Corporation

Get more information on this report

Outage Management System Market Report Coverage and Deliverables:

The "Outage Management System Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Outage Management System Market Geographic Insights:

The geographical scope of the Outage Management System market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains a preeminent position within the global industry, a standing solidified by the region's advanced utility infrastructure and the aggressive modernization of aging electrical grids. The regional landscape is characterized by high-stakes investments in the United States and Canada, where the transition toward Advanced Distribution Management Systems (ADMS) and smart grid architectures has become a strategic priority. This market leadership is further supported by stringent regulatory mandates from the Federal Energy Regulatory Commission (FERC) and the North American Electric Reliability Corporation (NERC), which require utilities to uphold rigorous reliability metrics (SAIDI/SAIFI) and minimize restoration times during frequent climate-induced weather events.

Technological progression in the United States and Canada is largely driven by a decisive shift toward AI-Powered Predictive Outage Models and Cloud-Native Platforms. These advanced systems utilize machine learning to analyze historical data, weather patterns, and real-time grid health to anticipate potential asset failures before they occur. Furthermore, the region is witnessing an increasing utilization of Integrated Outage Management Systems (OMS) that provide a seamless interface with Geographic Information Systems (GIS) and Advanced Metering Infrastructure (AMI). This focus on "Intelligent Grid Visibility" allows North American utilities to automate fault localization and streamline mobile workforce dispatching, significantly reducing the economic impact of large-scale power interruptions.

Get more information on this report

Outage Management System Market Research Report Guidance:

The report includes qualitative and quantitative data in the Outage Management System market across type, component, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by type, component, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Outage Management System Market News and Key Development:

The Outage Management System market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Outage Management System market are:

In December 2025, ABB announced an agreement to acquire IPEC Limited, a UK-based provider of electrical infrastructure monitoring and diagnostics technology. The acquisition strengthens ABB`s predictive maintenance and monitoring capabilities, enabling early detection of equipment failures and reducing downtime across critical sectors, including utilities and data centers. The integration is expected to enhance grid reliability and support advanced outage prevention solutions.

In November 2025, Schneider Electric launched the One Digital Grid Platform, an AI-enabled solution designed to help utilities modernize grid operations. The platform integrates planning, asset management, and operational tools while providing real-time outage restoration estimates to improve response during storms and grid disruptions. The launch strengthens digital grid capabilities and supports more resilient and efficient outage management for utilities.

Key Sources Referred:

World Bank & Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Outage Management System Market

ABB Ltd.

GE Vernova Inc.

Schneider Electric SE

Siemens AG

Oracle Corporation

Hitachi Energy Ltd.

Hexagon AB

CGI Inc.

Advanced Control Systems, Inc.

Survalent Technology Corporation

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Outage Management System Market?

The Outage Management System Market is valued at US$ 2.98 Billion in 2025, it is projected to reach US$ 10.70 Billion by 2033.

What is the CAGR for Outage Management System Market by (2026 - 2033)?

As per our report Outage Management System Market, the market size is valued at US$ 2.98 Billion in 2025, projecting it to reach US$ 10.70 Billion by 2033. This translates to a CAGR of approximately 17.3% during the forecast period.

What segments are covered in this report?

The Outage Management System Market report typically cover these key segments-

Type (Standalone OMS, Integrated OMS)

Component (Software System, Communication System)

End User (Private Utility, Public Utility)

What is the historic period, base year, and forecast period taken for Outage Management System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Outage Management System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Outage Management System Market?

The Outage Management System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB Ltd.

GE Vernova Inc.

Schneider Electric SE

Siemens AG

Oracle Corporation

Hitachi Energy Ltd.

Hexagon AB

CGI Inc.

Advanced Control Systems, Inc.

Survalent Technology Corporation

Who should buy this report?

The Outage Management System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Outage Management System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Outage Management System Market

Get Free Sample For Outage Management System Market